Hedges in the Warehouse

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hedge Funds Oversight, Report of the Technical Committee Of

Hedge Funds Oversight Consultation Report TECHNICAL COMMITTEE OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS MARCH 2009 This paper is for public consultation purposes only. It has not been approved for any other purpose by the IOSCO Technical Committee or any of its members. Foreword The IOSCO Technical Committee has published for public comment this consultation report on Hedge Funds Oversight. The Report makes preliminary recommendations of regulatory approaches that may be used to mitigate the regulatory risks posed by hedge funds. The Report will be finalised after consideration of comments received from the public. How to Submit Comments Comments may be submitted by one of the three following methods on or before 30 April 2009. To help us process and review your comments more efficiently, please use only one method. 1. E-mail • Send comments to Greg Tanzer, Secretary General, IOSCO at the following email address: [email protected] • The subject line of your message should indicate “Public Comment on the Hedge Funds Oversight: Consultation Report”. • Please do not submit any attachments as HTML, GIF, TIFF, PIF or EXE files. OR 2. Facsimile Transmission Send a fax for the attention of Greg Tanzer using the following fax number: + 34 (91) 555 93 68. OR 3. Post Send your comment letter to: Greg Tanzer Secretary General IOSCO 2 C / Oquendo 12 28006 Madrid Spain Your comment letter should indicate prominently that it is a “Public Comment on the Hedge Funds Oversight: Consultation Report” Important: All comments will be made available publicly, unless anonymity is specifically requested. Comments will be converted to PDF format and posted on the IOSCO website. -

2020.12.03 RSIC Meeting Materials

WILLIAM (BILL) H. HANCOCK, CPA RONALD P. WILDER, PH. D CHAIR VICE-CHAIR 1 PEGGY G. BOYKIN, CPA ALLEN R. GILLESPIE, CFA COMMISSIONER COMMISSIONER WILLIAM (BILL) J. CONDON, JR. JD, MA, CPA REBECCA M. GUNNLAUGSSON, PH. D COMMISSIONER COMMISSIONER EDWARD N. GIOBBE, MBA REYNOLDS WILLIAMS, JD, CFP COMMISSIONER COMMISSIONER _____________________________________________________________________________________ Commission Meeting Agenda Thursday, December 3, 2020 at 9:30 a.m. MEETING PARTICIPANTS WILL APPEAR VIA TELECONFERENCE Teleconference Streaming Via RSIC.SC.GOV RSIC Presentation Center Open for Public Access to Teleconference I. Call to Order and Consent Agenda A. Adoption of Proposed Agenda B. Approval of September 2020 Minutes II. Chair’s Report III. Committee Reports IV. CEO’s Report V. CIO’s Report A. Quarterly Investment Performance Update VI. Strategic Investment Topic Presentation – Rebalancing VII. Chinese Public Company Investment Discussion VIII. Delegated Investment Report IX. Executive Session – Discuss investment matters pursuant to S.C. Code Sections 9-16- 80 and 9-16-320; to discuss personnel matters pursuant to S.C. Code Ann. Section 30-4-70(a)(1); and receive advice from legal counsel pursuant to S.C. Code Section 30-4-70(a)(2). X. Potential Action Resulting from Executive Session XI. Adjournment NOTICE OF PUBLIC MEETING This notice is given to meet the requirements of the S.C. Freedom of Information Act and the Americans with Disabilities Act. Furthermore, this facility is accessible to individuals with disabilities, and special accommodations will be provided if requested in advance. 1201 MAIN STREET, SUITE 1510, COLUMBIA, SC 29201 // (P) 803.737.6885 // (F) 803.737.7070 // WWW.RSIC.SC.GOV 2 AMENDED DRAFT South Carolina Retirement System Investment Commission Meeting Minutes September 10, 2020 9:30 a.m. -

Hedge Fund Performance During the Internet Bubble Bachelor Thesis Finance

Hedge fund performance during the Internet bubble Bachelor thesis finance Colby Harmon 6325661 /10070168 Thesis supervisor: V. Malinova 1 Table of content 1. Introduction p. 3 2. Literature reviews of studies on mutual funds and hedge funds p. 5 2.1 Evolution of performance measures p. 5 2.2 Studies on performance of mutual and hedge funds p. 6 3. Deficiencies in peer group averages p. 9 3.1 Data bias when measuring the performance of hedge funds p. 9 3.2 Short history of hedge fund data p. 10 3.3 Choice of weight index p. 10 4. Hedge fund strategies p. 12 4.1 Equity hedge strategies p. 12 4.1.1 Market neutral strategy p. 12 4.2 Relative value strategies p. 12 4.2.1 Fixed income arbitrage p. 12 4.2.2 Convertible arbitrage p. 13 4.3 Event driven strategies p. 13 4.3.1 Distressed securities p. 13 4.3.2 Merger arbitrage p. 14 4.4 Opportunistic strategies p. 14 4.4.1 Global macro p. 14 4.5 Managed futures p. 14 4.5.1 Trend followers p. 15 4.6 Recent performance of different strategies p. 15 5. Data description p. 16 6. Methodology p. 18 6.1 Seven factor model description p. 18 6.2 Hypothesis p. 20 7. Results p. 21 7.1 Results period 1997-2000 p. 21 7.2 Results period 2000-2003 p. 22 8. Discussion of results p. 23 9. Conclusion p. 24 2 1. Introduction A day without Internet today would be cruel and unthinkable. -

Arbitrage Pricing Theory∗

ARBITRAGE PRICING THEORY∗ Gur Huberman Zhenyu Wang† August 15, 2005 Abstract Focusing on asset returns governed by a factor structure, the APT is a one-period model, in which preclusion of arbitrage over static portfolios of these assets leads to a linear relation between the expected return and its covariance with the factors. The APT, however, does not preclude arbitrage over dynamic portfolios. Consequently, applying the model to evaluate managed portfolios contradicts the no-arbitrage spirit of the model. An empirical test of the APT entails a procedure to identify features of the underlying factor structure rather than merely a collection of mean-variance efficient factor portfolios that satisfies the linear relation. Keywords: arbitrage; asset pricing model; factor model. ∗S. N. Durlauf and L. E. Blume, The New Palgrave Dictionary of Economics, forthcoming, Palgrave Macmillan, reproduced with permission of Palgrave Macmillan. This article is taken from the authors’ original manuscript and has not been reviewed or edited. The definitive published version of this extract may be found in the complete The New Palgrave Dictionary of Economics in print and online, forthcoming. †Huberman is at Columbia University. Wang is at the Federal Reserve Bank of New York and the McCombs School of Business in the University of Texas at Austin. The views stated here are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of New York or the Federal Reserve System. Introduction The Arbitrage Pricing Theory (APT) was developed primarily by Ross (1976a, 1976b). It is a one-period model in which every investor believes that the stochastic properties of returns of capital assets are consistent with a factor structure. -

Securitization & Hedge Funds

SECURITIZATION & HEDGE FUNDS: COLLATERALIZED FUND OBLIGATIONS SECURITIZATION & HEDGE FUNDS: CREATING A MORE EFFICIENT MARKET BY CLARK CHENG, CFA Intangis Funds AUGUST 6, 2002 INTANGIS PAGE 1 SECURITIZATION & HEDGE FUNDS: COLLATERALIZED FUND OBLIGATIONS TABLE OF CONTENTS INTRODUCTION........................................................................................................................................ 3 PROBLEM.................................................................................................................................................... 4 SOLUTION................................................................................................................................................... 5 SECURITIZATION..................................................................................................................................... 5 CASH-FLOW TRANSACTIONS............................................................................................................... 6 MARKET VALUE TRANSACTIONS.......................................................................................................8 ARBITRAGE................................................................................................................................................ 8 FINANCIAL ENGINEERING.................................................................................................................... 8 TRANSPARENCY...................................................................................................................................... -

Hedge Performance: Insurer Market Penetration and Basis Risk

CORE Metadata, citation and similar papers at core.ac.uk Provided by Research Papers in Economics This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: The Financing of Catastrophe Risk Volume Author/Editor: Kenneth A. Froot, editor Volume Publisher: University of Chicago Press Volume ISBN: 0-226-26623-0 Volume URL: http://www.nber.org/books/froo99-1 Publication Date: January 1999 Chapter Title: Index Hedge Performance: Insurer Market Penetration and Basis Risk Chapter Author: John Major Chapter URL: http://www.nber.org/chapters/c7956 Chapter pages in book: (p. 391 - 432) 10 Index Hedge Performance: Insurer Market Penetration and Basis Risk John A. Major Index-based financial instruments bring transparency and efficiency to both sides of risk transfer, to investor and hedger alike. Unfortunately, to the extent that an index is anonymous and commoditized, it cannot correlate perfectly with a specific portfolio. Thus, hedging with index-based financial instruments brings with it basis risk. The result is “significant practical and philosophical barriers” to the financing of propertykasualty catastrophe risks by means of catastrophe derivatives (Foppert 1993). This study explores the basis risk be- tween catastrophe futures and portfolios of insured homeowners’ building risks subject to the hurricane peril.’ A concrete example of the influence of market penetration on basis risk can be seen in figures 10.1-10.3. Figure 10.1 is a map of the Miami, Florida, vicin- John A. Major is senior vice president at Guy Carpenter and Company, Inc. He is an Associate of the Society of Actuaries. -

Risk Parity an Alternative Approach to Asset Allocation

FEATURE Risk Parity An Alternative Approach to Asset Allocation Alexander Pekker, PhD, CFA®, ASA, Meghan P. Elwell, JD, AIFA®, and Robert G. Smith III, CIMC®, AIF® ollowing the financial crisis of tors, traditional RP strategies fall short respectively, but a rather high Sharpe 2008, many members of the of required return targets and leveraged ratio, 0.86. In other words, while the investment management com- RP strategies do not provide enough portfolio is unlikely to meet the expected F munity, including Sage,intensified their potential benefits to outweigh their return target of many institutional inves- scrutiny of mean-variance optimization risks. Instead we advocate a liability- tors (say, 7 percent or higher), its effi- (MVO) and modern portfolio theory based approach that incorporates risk ciency, or “bang for the buck” (i.e., return (MPT) as the bedrock of asset alloca- budgeting, a key theme of RP, as well as per unit of risk, in excess of the risk-free tion (Elwell and Pekker 2010). Among tactical asset allocation. rate), is quite strong. various alternative approaches to asset How does this sample RP portfo- What is Risk Parity? allocation, risk parity (RP) has been in the lio compare with a sample MVO port- news lately (e.g., Nauman 2012; Summers As noted above, an RP portfolio is one folio? A sample MVO portfolio with a 2012), especially as some hedge funds, where risk, defined as standard deviation return target of 7 percent is shown in such as AQR, and large plan sponsors, of returns, is distributed evenly among table 2. Unlike the sample RP portfolio, such as the San Diego County Employees all potential asset classes;1 table 1 shows the MVO portfolio is heavily allocated Retirement Association, have advocated a sample (unleveraged) RP portfolio toward equities, and it has much higher its adoption. -

Mitigating Tax Risks of Hedge Fund Investments in Loans

CLIENT MEMORANDUM MITIGATING TAX RISKS OF HEDGE FUND INVESTMENTS IN LOANS The tax risks for offshore hedge funds of investing in loans, whether directly or through derivatives, are attracting more attention. (See, for example, “Hedge Funds See Tax Issue,” Wall Street Journal, page C2, January 5, 2007.) We understand that these investments are also playing a larger role in funds’ arbitrage strategies in the credit-derivatives markets. Offshore hedge funds have been making these investments for years and generally take the position that the activity does not constitute a US trade or business and therefore does not result in US taxation. The funds rely on a special safe harbor rule that trading in stocks and securities by non-US persons, even if conducted in the United States, is generally not treated as constituting a US trade or business. By contrast, there is a substantial risk that regularly negotiating and originating loans in the US does constitute a US trade or business, and that the income and gain from such a business is subject to an effective federal tax rate of up to approximately 55% when earned by a non-US corporation (such as an offshore hedge fund). Engaging in a US trade or business also requires the filing of US tax returns. Because of this risk of US taxation, most offshore hedge funds investing in loans avoid regularly originating loans. They instead invest in loans either by purchasing the loans in a secondary market or investing in derivatives on the loans. Such funds also usually take steps to minimize the risk that the seller or counterparty in these transactions might be treated as their agent, which would potentially result in the loan-origination activity of the agent being attributed to the fund, causing the fund to be treated as engaged in a US trade or business. -

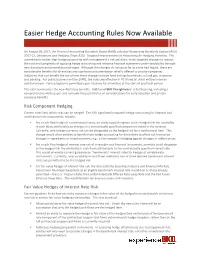

Easier Hedge Accounting Rules Now Available

Easier Hedge Accounting Rules Now Available On August 28, 2017, the Financial Accounting Standards Board (FASB) released Accounting Standards Update (ASU) 2017-12, Derivatives and Hedging (Topic 815): Targeted Improvements to Accounting for Hedging Activities. The amendments better align hedge accounting with management’s risk activities, make targeted changes to reduce the cost and complexity of applying hedge accounting and enhance financial statement understandability through new disclosure and presentation changes. Although the changes do not go as far as some had hoped, there are considerable benefits for all entities and significant documentation relief is offered to private companies. Industries that can benefit the most from these changes include food and agribusinesses, oil and gas, insurance and banking. For public business entities (PBE), the rules are effective in 2019 and all other entities have an additional year. Early adoption is permitted upon issuance for all entities at the start of any fiscal period. This alert summarizes the new ASU’s key benefits. Additional BKD Thoughtware® is forthcoming, including a comprehensive white paper and narrowly focused articles on considerations for early adoption and private company benefits. Risk Component Hedging Current rules limit which risks can be hedged. The ASU significantly expands hedge accounting for financial and nonfinancial risk components, notably: . For a cash flow hedge of a nonfinancial asset, an entity could designate as the hedged risk the variability in cash flows attributable to changes in a contractually specified component stated in the contract. Currently, only foreign currency risk can be designated as the hedged risk for a nonfinancial item. This change would allow entities to benefit from hedge accounting for derivatives to offset risk from price changes in ingredients or inventory items, e.g., a tire company’s hedging against changes in rubber prices. -

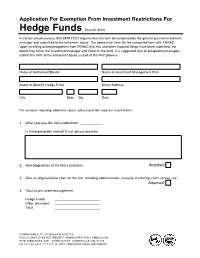

Application for Exemption from Investment Restrictions For

Application For Exemption From Investment Restrictions For Hedge Funds (Issued: 8/03) In certain circumstances, 840 CMR 19.02 requires that this form be completed by the general partner/investment manager and submitted to the retirement board. The board must then file the completed form with PERAC. Upon receiving acknowledgement from PERAC that this and other required filings have been submitted, the board may retain the investment manager and invest in the fund. It is suggested that all prospective managers submit this form to the retirement board as part of the RFP process. Name of Retirement Board Name of Investment Management Firm Name of Specific Hedge Fund Street Address City State Zip Date For answers requiring additional space, please provide separate attachments. 1. What year was the firm established? ____________ Is it independently owned? If not, please describe. 2. Give biographies of the firm’s principals. Attached 3. Give an organizational chart for the firm, including administration, analysts, marketing, client service, etc. Attached 4. Total assets under management: Hedge Funds _________________________ Other (describe) _________________________ Total _________________________ COMMONWEALTH OF MASSACHUSETTS PUBLIC EMPLOYEE RETIREMENT ADMINISTRATION COMMISSION FIVE MIDDLESEX AVE., THIRD FLOOR, SOMERVILLE, MA 02145 PH 617 666 4446 TTY 617 591 8917 WEB WWW.MASS.GOV/PERAC 5. List each hedge fund currently under management. Name Year Established Current Market Value ____________________________________ __________ ____________________ -

Formulating Hedging Strategies for Financial Risk Mitigation in Competitive U.S

Scholars' Mine Masters Theses Student Theses and Dissertations Spring 2008 Formulating hedging strategies for financial risk mitigation in competitive U.S. electricity markets Karthik Viswanathan Follow this and additional works at: https://scholarsmine.mst.edu/masters_theses Part of the Systems Engineering Commons Department: Recommended Citation Viswanathan, Karthik, "Formulating hedging strategies for financial risk mitigation in competitive U.S. electricity markets" (2008). Masters Theses. 6832. https://scholarsmine.mst.edu/masters_theses/6832 This thesis is brought to you by Scholars' Mine, a service of the Missouri S&T Library and Learning Resources. This work is protected by U. S. Copyright Law. Unauthorized use including reproduction for redistribution requires the permission of the copyright holder. For more information, please contact [email protected]. FORMULATING HEDGING STRATEGIES FOR FINANCIAL RISK MITIGATION IN COMPETITIVE U.S. ELECTRICITY MARKETS by KARTHIK VISWANATHAN A THESIS Presented to the Faculty of the Graduate School of the UNIVERSITY OF MISSOURI - ROLLA In Partial Fulfillment of the Requirements for the Degree MASTER OF SCIENCE IN SYSTEMS ENGINEERING 2008 Approved by _______________________________ _______________________________ David Enke, Advisor Cihan Dagli _______________________________ Badrul Chowdhury © 2008 Karthik Viswanathan All Rights Reserved iii ABSTRACT In the competitive electricity industry, there exists some level of price risk for electricity in the form of price volatility. In order to perform efficient risk mitigation, it is necessary to have a good understanding on the future electricity demand and volatility. Electricity demand forecasting which drives the demand for fuels is first discussed. A method to predict future demand levels of electricity using a single factor mean reversion model is proposed. -

ABSTRACT LUCY, ZACHARY MARC. Analysis of Fixed Volume Swaps For

ABSTRACT LUCY, ZACHARY MARC. Analysis of Fixed Volume Swaps for Hedging Financial Risk at Large-Scale Wind Projects (Under the direction of Dr. Jordan Kern). Large scale wind power projects are increasingly selling power directly into wholesale electricity markets without the benefits of stable (fixed price) off-take agreements. As a result, many wind power producers are incentivized to use financial hedging contracts to mitigate exposure to price risk. One particular hedging contract - the “fixed volume price swap” - has gained prevalence, but it poses several liabilities for wind power producers that reduce its effectiveness. In this paper, we explore problems associated with fixed volume swaps and examine two different interventions to improve contract performance for wind power producers. Using a hypothetical wind power project in the Southwest Power Pool (SPP) market as a case study, we first look at how “shape risk” (an imbalance between actual wind power production and hourly production targets specified by contract terms) negatively impacts contract performance and whether this could be remedied through improved contract design. Using a multi-objective optimization algorithm, we find examples of alternative contract parameters (hourly wind power production targets) that are more effective at increasing revenues during low performing months and do so at a lower cost than conventional fixed volume swaps. Then we examine how “basis risk” (a discrepancy in market prices between the “node” where the wind project injects power into the grid, and the regional hub price) can negatively impact contract performance. We statistically manipulate basis risk as a proxy for the effects of increased transmission and its effect on contract performance.