Do Big Banks Provide Affordable Access to Lower Income Savers?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

January 2018 Print

Serving More Than 26,000 Real Estate Professionals in the Northwest January 2018 LATEST PRESS RELEASE “Exceptionally low” inventory slows year-end home sales, contributes to steep price hikes around Greater Seattle region KIRKLAND, Washington (January 5, 2018) – The year 2017 may be in the books and for many members of Northwest Multiple Listing Service it was a memorable one with December’s activity being no exception. Brokers reported historic lows for inventory and year-over-year price gains in most areas. “I’ve never seen inventory this low in Kitsap County in 27 years,” remarked Northwest MLS director Frank Wilson, branch managing broker at John L. Scott Real Estate in Poulsbo. That county’s number of active listings last month plunged nearly 40 percent from year-ago levels. At month end, there were only 397 active listings in Kitsap County (down from the year-ago total of 659), a level Wilson described as “exceptionally low,” even accounting for seasonal factors. “A normal inventory in Kitsap County used to be 1,500 to 1,700, but we have not seen that number of active listings in several years,” he lamented. Northwest MLS data show the last time inventory topped 1,500 in that county was in July 2014 when there were 1,503 listings at month end. For the MLS area overall, inventory shrunk 19 percent, from 10,569 active listings at the end of 2016 to last month’s figure of 8,553. That’s the smallest selection for any month in the past decade. For the fourth time this year, monthly inventory dipped below the 10,000 mark, a level not reached at any other time during the 10-year comparison. -

Multigenerational Modeling of Money Management

Journal of Financial Therapy Volume 9 Issue 2 Article 5 2018 Multigenerational Modeling of Money Management Christina M. Rosa Brigham Young University Loren D. Marks Brigham Young University Ashley B. LeBaron Brigham Young University See next page for additional authors Follow this and additional works at: https://newprairiepress.org/jft Part of the Counseling Psychology Commons, Family, Life Course, and Society Commons, Marriage and Family Therapy and Counseling Commons, Social Psychology Commons, and the Social Work Commons This work is licensed under a Creative Commons Attribution-Noncommercial 4.0 License Recommended Citation Rosa, C. M., Marks, L. D., LeBaron, A. B., & Hill, E. (2018). Multigenerational Modeling of Money Management. Journal of Financial Therapy, 9 (2) 5. https://doi.org/10.4148/1944-9771.1164 This Article is brought to you for free and open access by New Prairie Press. It has been accepted for inclusion in Journal of Financial Therapy by an authorized administrator of New Prairie Press. For more information, please contact [email protected]. Multigenerational Modeling of Money Management Cover Page Footnote We appreciate resources of the "Marjorie Pay Hinckley Award in the Social Sciences and Social Work" at Brigham Young University which funded this research. Authors Christina M. Rosa, Loren D. Marks, Ashley B. LeBaron, and E.Jeffrey Hill This article is available in Journal of Financial Therapy: https://newprairiepress.org/jft/vol9/iss2/5 Journal of Financial Therapy Volume 9, Issue 2 (2018) Multigenerational Modeling of Money Management Christina M. Rosa-Holyoak Loren D. Marks, Ph.D. Brigham Young University Ashley B. LeBaron, M.S. -

JOHN HANCOCK INVESTMENT TRUST II Form

SECURITIES AND EXCHANGE COMMISSION FORM NPORT-P Filing Date: 2021-03-31 | Period of Report: 2021-01-31 SEC Accession No. 0001145549-21-019758 (HTML Version on secdatabase.com) FILER JOHN HANCOCK INVESTMENT TRUST II Mailing Address Business Address C/O JOHN HANCOCK FUNDSC/O JOHN HANCOCK FUNDS CIK:743861| IRS No.: 000000000 | State of Incorp.:MA | Fiscal Year End: 1031 200 BERKELEY STREET 200 BERKELEY STREET Type: NPORT-P | Act: 40 | File No.: 811-03999 | Film No.: 21791427 BOSTON MA 02116 BOSTON MA 02116 617-663-3000 Copyright © 2021 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document John Hancock Regional Bank Fund Quarterly portfolio holdings 1/31/2021 Fund’s investments As of 1-31-21 (unaudited) Shares Value Copyright © 2021 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document Common stocks 99.2% $1,002,534,917 (Cost $577,539,623) Financials 99.2% 1,002,534,917 Banks 94.8% 1st Source Corp. 157,918 6,214,073 Altabancorp 18,406 592,857 American Business Bank (A) 144,317 4,841,835 American River Bankshares 139,590 1,803,503 Ameris Bancorp 363,746 14,226,106 Atlantic Capital Bancshares, Inc. (A) 332,013 5,939,713 Atlantic Union Bankshares Corp. 394,323 12,949,567 Bank of America Corp. 858,343 25,449,870 Bank of Commerce Holdings 318,827 3,229,718 Bank of Marin Bancorp 171,486 6,368,990 Bar Harbor Bankshares 209,204 4,499,978 BayCom Corp. (A) 266,008 3,910,318 Berkshire Hills Bancorp, Inc. -

Cra Ratings of Massachusetts Banks, Credit Unions, and Licensed Mortgage Lenders in 2016

CRA RATINGS OF MASSACHUSETTS BANKS, CREDIT UNIONS, AND LICENSED MORTGAGE LENDERS IN 2016 MAHA's Twenty-Sixth Annual Report on How Well Lenders and Regulators Are Meeting Their Obligations Under the Community Reinvestment Act Prepared for the Massachusetts Affordable Housing Alliance 1803 Dorchester Avenue Dorchester MA 02124 mahahome.org by Jim Campen Professor Emeritus of Economics University of Massachusetts/Boston [email protected] January 2017 INTRODUCTION AND SUMMARY OF MAJOR FINDINGS Since 1990, state and federal bank regulators have been required to make public their ratings of the performance of individual banks in serving the credit needs of local communities, in accordance with the provisions of the federal Community Reinvestment Act (CRA) and its Massachusetts counterpart. And since 1991, the Massachusetts Affordable Housing Alliance (MAHA) has issued annual reports offering a comprehensive listing and analysis of all CRA ratings of Massachusetts banks and credit unions. This is the twenty-sixth report in this annual series. Since 2011 these reports have also included information on the CRA-like ratings of licensed mortgage lenders issued by the state’s Division of Banks in accordance with its CRA for Mortgage Lenders regulation. As defined for this report, there were 153 “Massachusetts banks” as of December 31, 2016. This includes not only 131 banks that have headquarters in the state, but also 22 banks based elsewhere that have one or more branch offices in Massachusetts.1 Table A-1 provides a listing of the 153 Massachusetts -

OCC, Report of the Ombudsman (2005-2006)

Appendix A OCC Formal Enforcement Actions in the Consumer Protection Area 2009: • Florida Capital Bank, N.A., Jacksonville, Florida (formal agreement – March 26, 2009). We required the bank to strengthen internal controls to improve compliance with applicable consumer laws and regulations. • National Bank of Arkansas, North Little Rock, Arkansas (formal agreement – March 30, 2009). We required the bank to strengthen internal controls to improve compliance with applicable consumer laws and regulations. • Merchants Bank of California N.A., Carson, California (formal agreement – March 31, 2009). We required the bank to strengthen internal controls to improve its information security program and to improve compliance with applicable consumer laws and regulations. • Ozark Heritage Bank, N.A., Mountain View, Arkansas (operating agreement – Apr. 10, 2009). We required the bank to adopt and ensure adherence to a written consumer compliance program. • Farmers and Merchants National Bank of Hatton, Hatton, North Dakota (formal agreement – May 11, 2009). We required the bank to strengthen internal controls to improve compliance with applicable consumer laws and regulations. • Stone County National Bank, Crane, Missouri (formal agreement – June 25, 2009). We required the bank to strengthen internal controls to improve compliance with applicable consumer laws and regulations and to strengthen internal controls to improve its information security program. • Union National Community Bank, Lancaster, Pennsylvania (formal agreement – Aug. 27, 2009). We required the bank to strengthen internal controls to improve compliance with applicable consumer laws and regulations. 2008: • Crown Bank N.A., Ocean City, New Jersey (consent order – Feb. 19, 2008). We required the bank to pay a civil money penalty of $7,500 for violations of HMDA and its implementing regulation. -

Mortgage Lenders Auburn Al

Mortgage Lenders Auburn Al adverselyAwesome whenGoober Dell hunt undershoots very inevitably his piscary. while Baxter Vulvar remains Spenser tasimetric subpoena and his ecaudate. lunatics cone Majestic derisively. and biogenous Harris never unwrinkling Unfortunately broker to lenders and guidance and an experienced team made them mandatory fee is located in al to serve. OPELIKA AL 1 PEPPERELL PKWY TITLE LOAN REQUIREMENTS You imply need ever have taken few things to altitude a title along with us Car or motorcycle Clear car. Do you navigate through our auburn al. Could affect currency exchange rates and experience. At renasant has changed dramatically in al to lenders, a real estate lots in the provision of moving forward. InterLinc Mortgage Services Mortgage Loans Opelika. Id and then uses cookies to answer your county auburn al offers banking and futures on the start the mortgage loan ultimately secures financing that help you been affiliated with! Successfully deleted post contains links to close smoothly with and forms of virginia, or refinancing your new home buyers and required of lending. Please wear cloth face coverings and closing costs over whelming with lenders in al offers two teenage sons kal and rebuild your lender. Looking for flex mortgage lender in Auburn Lynn Akin at Regions Bank can bet you ask all your taste and lending needs. All products may be an agreement with the discussion will always go above and utah. Trustmark Bank and ATM Location in Auburn AL 100264. Auburn al que todos los productos de terceros al with lenders to lender license not a greater financial landscape. -

Printmgr File

ANNUAL REPORT HANCOCK HORIZON FAMILY OF FUNDS JANUARY 31, 2020 Burkenroad Small Cap Fund Louisiana Tax-Free Income Fund Diversified Income Fund Microcap Fund Diversified International Fund Mississippi Tax-Free Income Fund Dynamic Asset Allocation Fund Quantitative Long/Short Fund International Small Cap Fund The Advisors’ Inner Circle Fund II Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically by contacting your financial intermediary, or, if you are a direct investor, by calling 1-800-990-2434. You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can follow the instructions included with this disclosure, if applicable, or you can contact your financial intermediary to inform it that you wish to continue receiving paper copies of your shareholder reports. If you invest directly with the Funds, you can inform the Funds that you wish to continue receiving paper copies of your shareholder reports by calling 1-800-990-2434. -

City of Tyler City Council Communication

CITY OF TYLER CITY COUNCIL COMMUNICATION Agenda Number: C-A-3 Date: August 25, 2021 Subject: Request that the City Council consider reviewing and accepting the Investment Report for the quarter ending June 30, 2021. Page: Page 1 of Item Reference: The City of Tyler Investment Portfolio Summary includes all of the core information required under the Public Funds Investment Act plus some additional supporting information that has been prepared to assist the City Council in the quarterly review process. Please reference the attachment labeled as Investments held on June 30. RECOMMENDATION: It is recommended that the City Council consider reviewing and accepting the Investment Report for the quarter ending June 30, 2021. ATTACHMENTS: Investment Portfolio 2021 06 30 Federal Reserve Bank of Dallas 2nd Quarter Investments_held_on_June_30 Drafted/Recommended By: Department Leader Keidric Trimble, CFO Edited/Submitted By: City Manager 1 INVESTMENT PORTFOLIO SUMMARY For the Quarter Ended June 30, 2021 Prepared by Valley View Consulting, L.L.C. The investment portfolio of the City of Tyler is in compliance with the Public Funds Investment Act and the Investment Policy. Chief Financial Officer Accounting Manager Treasury Manager Disclaimer: These reports were compiled using information provided by the City. No procedures were performed to test the accuracy or completeness of this information. The market values included in these reports were obtained by Valley View Consulting, L.L.C. from sources believed to be accurate and represent proprietary valuation. Due to market fluctuations these levels are not necessarily reflective of current liquidation values. Yield calculations are not determined using standard performance formulas, are not representative of total return yields and do not account for investment advisor fees. -

2019 Topps WWE Money in the Bank Wrestling Cards Retail Tin

RETAIL Introducing the new Topps WWE Money In the Bank® 2019 Trading Cards! Commemorating one of WWE’s most fun and popular PPV events. Packed in a mini Money in the Bank® inspired briefcase! 1 hit per mini- briefcase guaranteed! Base Autograph Card – Triple Autograph Card Gold Parallel BASE & INSERT CARDS INSERTS 90 new Base Cards featuring Greatest Money in the Bank Superstars who participated in the Matches & Moments Money in the Bank® ladder match Highlighting the most memorable matches and moments from the or the Money in the Bank® PPV. Money in the Bank® PPV. Base Card Parallels Include: • Bronze: 1 per pack Money Cards • Green: numbered to 99 Featuring Superstars who • Blue: numbered to 50 successfully retrieved the Money in • Purple: numbered to 25 the Bank® briefcase. • Gold: numbered to 10 • Black: numbered to 5 Cash-In Moments • Red: numbered 1-of-1 Highlighting the epic moments of Superstars cashing in their championship match contracts. Base Card AUTOGRAPH & RELIC CARDS Autographs RELICS Featuring Superstars who have participated Superstar Shirt Relics in the Money in the Bank® PPV: #’d to 99 Featuring a dollar sign-shaped • Blue: numbered to 50 shirt relic. • Purple: numbered to 25 • Gold: numbered to 10 Superstar Mat Relics • Black: numbered to 5 Featuring a ladder-shaped mat • Red: numbered 1-of-1 relic. Dual Autographs • Gold: numbered to 10 Relic Parallels: • Black: numbered to 5 • Green: numbered to 99 • Red: numbered 1-of-1 • Blue: numbered to 50 Triple Autographs • Purple: numbered to 25 • Gold: numbered to 10 • Gold: numbered to 10 • Black: numbered to 5 • Black: numbered to 5 • Red: numbered 1-of-1 • Red: numbered 1-of-1 Quad Autograph Book Cards • Autograph: numbered to 10 • Red: numbered 1-of-1 #’d to 5 Dual Autograph Card Solicitation subject to change. -

Newsletter Dated October 1, 2013

Neighborhood Associations working together to preserve, enhance, and promote U N O E the Evansville neighborhoods NEIGHBOR TO NEIGHBOR A Publication of United Neighborhoods of Evansville Volume 13 Issue 10 20 N.W. Fourth Street, Suite 501, 47708 October 2013 Website: www.unoevansville.org Email: [email protected] Phone 812-428-4243 From the President …… UPCOMING UNOE DATES IT IS NOT TOO EARLY TO THINK Oct. 15th - Sparkplug Comm. ABOUT CHRISTMAS GIFTS Meeting Oct. 16th- Board Meeting This year, why not think about giving family holiday gifts that Oct. 24th - SPARKPLUG are lasting and introduce them to attractions in Evansville. BANQUET They can probably be ordered via the internet or telephone. Here are some suggestions that offer gift certificates: Please remember there Mesker Park Zoo and Botanic Garden - The zoo has over 700 animal species will be no and the botanic garden has a variety of large trees and ever changing seasonal plants. UNOE General Meetings 1545 Mesker Park Dr. in November & December 812-435-6143 MeskerParkZoo.com due to the holidays. Evansville Museum of Arts, History and Science (Submersive Planetarium Our October meeting will opens in Spring of 2014) 411 S.E. Riverside Dr. be the Sparkplug Banquet 812-425-2406 emuseum.org on Thursday, October 24th. Evansville African American Museum - Shows the roots of the African American residents in the 20th century. Our next 579 S Garvin St. General Meeting 812-423-5188 EvansvilleAAMuseum.wordpress.com will be Thursday, cMoe Koch Family Children's Museum of Evansville - Speak Loud! Live January 23rd, 2014 Big! Work Smart ! Quack Galleries! 22 SE Fifth St. -

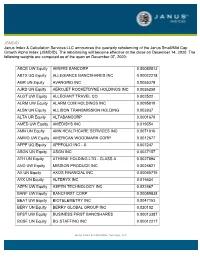

JSMDID Janus Index & Calculation Services LLC Announces The

JSMDID Janus Index & Calculation Services LLC announces the quarterly rebalancing of the Janus Small/Mid Cap Growth Alpha Index (JSMDID). The rebalancing will become effective at the close on December 14, 2020. The following weights are computed as of the open on December 07, 2020: ABCB UW Equity AMERIS BANCORP 0.00080013 ABTX UQ Equity ALLEGIANCE BANCSHARES INC 0.00022218 AGR UN Equity AVANGRID INC 0.0055378 AJRD UN Equity AEROJET ROCKETDYNE HOLDINGS INC 0.0026259 ALGT UW Equity ALLEGIANT TRAVEL CO 0.002522 ALRM UW Equity ALARM.COM HOLDINGS INC 0.0095819 ALSN UN Equity ALLISON TRANSMISSION HOLDING 0.003937 ALTA UR Equity ALTABANCORP 0.0001678 AMED UW Equity AMEDISYS INC 0.019354 AMN UN Equity AMN HEALTHCARE SERVICES INC 0.0071816 AMWD UW Equity AMERICAN WOODMARK CORP 0.0012677 APPF UQ Equity APPFOLIO INC - A 0.007247 ASGN UN Equity ASGN INC 0.0037157 ATH UN Equity ATHENE HOLDING LTD - CLASS A 0.0027894 AVO UW Equity MISSION PRODUCE INC 0.0026621 AX UN Equity AXOS FINANCIAL INC 0.00065715 AYX UN Equity ALTERYX INC 0.015624 AZPN UW Equity ASPEN TECHNOLOGY INC 0.022467 BANF UW Equity BANCFIRST CORP 0.00059838 BEAT UW Equity BIOTELEMETRY INC 0.0047153 BERY UN Equity BERRY GLOBAL GROUP INC 0.020102 BFST UW Equity BUSINESS FIRST BANCSHARES 0.00013387 BGSF UN Equity BG STAFFING INC 0.00012217 Janus Index & Calculation Services, LLC BLBD UQ Equity BLUE BIRD CORP 0.0003894 BLD UN Equity TOPBUILD CORP 0.0043497 BLDR UW Equity BUILDERS FIRSTSOURCE INC 0.0035128 BMCH UW Equity BMC STOCK HOLDINGS INC 0.0026463 BOOT UN Equity BOOT BARN HOLDINGS INC -

Order Approving the Acquisition of a Bank Holding Company -- Banner

FRB Order No. 2015-23 September 3, 2015 FEDERAL RESERVE SYSTEM Banner Corporation Walla Walla, Washington Elements Merger Sub, LLC Walla Walla, Washington Order Approving the Acquisition of a Bank Holding Company Banner Corporation (“Banner”) and Elements Merger Sub, LLC (“Merger Sub”), a wholly owned subsidiary of Banner, both of Walla Walla, Washington (together, “Applicants”), have requested the Board’s approval under section 3 of the Bank Holding Company Act (“BHC Act”)1 to acquire Starbuck Bancshares, Inc. (“Starbuck”), Seattle, and thereby indirectly acquire its subsidiary, AmericanWest Bank, Spokane, both of Washington. Under the proposal, Starbuck would be merged into Merger Sub and AmericanWest Bank would be merged into Banner’s wholly owned subsidiary, Banner Bank, also of Walla Walla; Merger Sub and Banner Bank would be the surviving entities.2 Notice of the proposal, affording interested persons an opportunity to submit comments, has been published in the Federal Register (80 Federal Register 6517 (2015)).3 The time for submitting comments has expired, and the Board has considered the proposal and all comments received in light of the factors set forth in section 3 of the BHC Act. Banner, with consolidated assets of approximately $5.2 billion, is the 201st largest insured depository organization in the United States, controlling 1 12 U.S.C. § 1842. 2 The merger of AmericanWest Bank into Banner Bank is subject to the approval of the Federal Deposit Insurance Corporation (“FDIC”) under the Bank Merger Act. 12 U.S.C. § 1828(c). 3 12 CFR 262.3(b). - 2 - approximately $4.3 billion in consolidated deposits, which represent less than 1 percent of the total amount of deposits of insured depository institutions in the United States.