COTY INC [COTY:US] Research Presentation Released in April 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1H2018 M&A Update

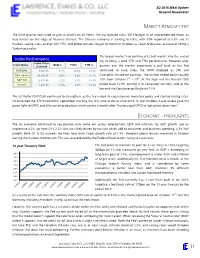

3Q 2018 M&A Update General Newsletter MARKET ATMOSPHERE The third quarter continued to give us drama on all fronts. The EU rejected Italy’s 2019 budget in an unprecedented move, as Italy teeters on the edge of financial distress. The Chinese economy is starting to falter, with GDP reported at 6.5% and its markets seeing a loss of over 20% YTD. And global tensions began to mount in October as Saudi Arabia was accused of killing a Turkish journalist. The broad market had continued its bull market into the end of Index Performance Q3, marking a solid YTD and TTM performance. However after Index Price Index Name QoQ % YTD% TTM % 9/28/2018 quarter end the market experience a pull back as the Fed NASDAQ 8,046.35 7.1% 14.8% 23.9% continued to raise rates, the DOW dropped as 3M, and Dow Jones 26,458.31 9.0% 6.6% 18.1% Caterpillar missed on earnings. The market ended down roughly st th S&P 500 2,913.98 7.2% 8.1% 15.7% 10% from October 1 – 29 . At the high end the Russell 2000 Russell 1,696.57 3.3% 9.5% 13.8% pulled back 12.9%, putting it in correction territory, and at the low end the Dow Jones pulling back 7.6%. The US Dollar (DXY:CUR) continued to strengthen, as the fed ended its expansionary monetary policy and started raising rates. Oil breached the $70 threshold in September marking the first time to do so since 2014. In late October, Saudi Arabia gave the green light to OPEC and allies on oil production, which comes a month after Trump urged OPEC to “get prices down now.” ECONOMIC - HIGHLIGHTS The US economy continued to see positive data come out across employment, GDP and inflation. -

COTY INC. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 Form 10-Q (Mark One) ý QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE QUARTERLY PERIOD ENDED SEPTEMBER 30, 2018 OR ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO COMMISSION FILE NUMBER 001-35964 COTY INC. (Exact name of registrant as specified in its charter) Delaware 13-3823358 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification Number) 350 Fifth Avenue, New York, NY 10118 (Address of principal executive offices) (Zip Code) (212) 389-7300 Registrant’s telephone number, including area code Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨ Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨ Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. -

Keurig to Acquire Dr Pepper Snapple for $18.7Bn in Cash

Find our latest analyses and trade ideas on bsic.it Coffee and Soda: Keurig to acquire Dr Pepper Snapple for $18.7bn in cash Dr Pepper Snapple Group (NYSE:DPS) – market cap as of 17/02/2018: $28.78bn Introduction On January 29, 2018, Keurig Green Mountain, the coffee group owned by JAB Holding, announced the acquisition of soda maker Dr Pepper Snapple Group. Under the terms of the reverse takeover, Keurig will pay $103.75 per share in a special cash dividend to Dr Pepper shareholders, who will also retain 13 percent of the combined company. The deal will pay $18.7bn in cash to shareholders in total and create a massive beverage distribution network in the U.S. About Dr Pepper Snapple Group Incorporated in 2007 and headquartered in Plano (Texas), Dr Pepper Snapple Group, Inc. manufactures and distributes non-alcoholic beverages in the United States, Mexico and the Caribbean, and Canada. The company operates through three segments: Beverage Concentrates, Packaged Beverages, and Latin America Beverages. It offers flavored carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs), including ready-to-drink teas, juices, juice drinks, mineral and coconut water, and mixers, as well as manufactures and sells Mott's apple sauces. The company sells its flavored CSD products primarily under the Dr Pepper, Canada Dry, Peñafiel, Squirt, 7UP, Crush, A&W, Sunkist soda, Schweppes, RC Cola, Big Red, Vernors, Venom, IBC, Diet Rite, and Sun Drop; and NCB products primarily under the Snapple, Hawaiian Punch, Mott's, FIJI, Clamato, Bai, Yoo- Hoo, Deja Blue, ReaLemon, AriZona tea, Vita Coco, BODYARMOR, Mr & Mrs T mixers, Nantucket Nectars, Garden Cocktail, Mistic, and Rose's brand names. -

E C O N O M I C S

ECONOMICS OF MOBILE 2015 EDITION © 2015 SNL Kagan, a division of SNL Financial LC. All rights reserved. One SNL Plaza, Charlottesville, VA 22902 | Phone: 866.296.3743 | www.snlkagan.com Published May 2015 | ISBN: 978-1-939835-437 ECONOMICS OF MOBILE 2015 EDITION © 2015 SNL Kagan, a division of SNL Financial LC. All rights reserved. One SNL Plaza, Charlottesville, VA 22902 | Phone: 866.296.3743 | www.snlkagan.com Published May 2015 | ISBN: 978-1-939835-437 Economics of Mobile Programming SNL Kagan Industry Report Contents Executive Summary........................................................2 Mobile ads vs. video subscription services revenue, U.S. (chart) ................2 Comparing multichannel video subs and subscription OTT subs, Q4 2014 (chart)...3 The Addressable Market: Sizing the U.S. Smartphone and Tablet Audience .............4 Smartphone and tablets in use, U.S., 2008-2014 (chart) .......................4 Carrier Video Subscription Services Are No Competition for OTT/TV Everywhere .......5 Carrier-branded mobile video subs, 2007-2014 (chart)........................5 Carrier-branded mobile video revenue, 2007-2014 (chart) .....................5 OTT and mobile video year-end subs, 2007-2014 (chart) ......................6 Comparing multichannel video subs and subscription OTT subs, Q4 2014 (chart)...6 OTT and carrier-branded mobile video device compatibility ...................7 Price differential between OTT & carrier-based mobile video services, 2015 .......7 Free mobile video content, 2015.........................................7 -

Nnn Investment Opportunity Long Term Corporate Lease Krispy Kreme Doughnut Corporation Nnn Investment Opportunity Long Term Corporate Tenant

KRISPY KREME| 810 CASSAT AVENUE, JACKSONVILLE, FL 32205 NNN INVESTMENT OPPORTUNITY LONG TERM CORPORATE LEASE KRISPY KREME DOUGHNUT CORPORATION NNN INVESTMENT OPPORTUNITY LONG TERM CORPORATE TENANT KRISPY KREME| 810 CASSAT AVENUE,£¤301 JACKSONVILLE FL 32205 £¤17 UVA1A JACKSONVILLE INT'L AIRPORT PROPERTY HIGHLIGHTS • Address: 810 Cassat Ave, Jacksonville FL 32205 • Total SF: 19,820 SF • Total AC: 0.455 AC • Building SF: 2,600 SF • Occupancy :100% • Concept: Krispy Kreme JACKSONVILLE • Year Built: 2012 DOWNTOWN ¨¦§295 £¤90 UVA1A TENANT HIGHLIGHTS £¤17 • Over 1,400 Krispy Kreme locations across 30 countries UNIVERSITY OF NORTH FLORIDA • Founded 82 years ago in Winston-Salem, NC UV202 • Acquired by JAB Holdings in 2016 (S&P “A-“ credit rating) NAVAL AIR STATION JACKSONVILLE • World Famous “Glazed Doughnut” icon £¤17 295 ¨¦§ £¤1 UV21 ¨¦§95 ¨¦§95 For more information, please contact: £¤1 PJ BEHR Vice President, CCIM Investment Sales 407.540.7746 420 South Orange Ave. Suite 950 [email protected] Orlando, FL 32801 Although the information contained herein was provided by sources believed to be reliable, CNL Commercial Real Estate makes foundrycommercial.com no representation, expressed or implied, as to its accuracy and said information is subject to errors, omissions or changes. NNN INVESTMENT OPPORTUNITY LONG TERM CORPORATE TENANT MARKET AERIAL CASSAT AVE - 23,500 VPD AVE CASSAT I - 10 - 103,500 VPD PROPERTY FEATURES The Krispy Kreme is located at 810 Cassat Ave, a major north-south artery in the Riverside submarket of Jacksonville, FL. The property is a .45 ac signalized corner lot with great visibility and access at the SWC of the intersection. -

Deal of the Week: JAB to Buy Pret a Manger for $2B

Deal of the Week: JAB to Buy Pret A Manger for $2B Announcement Date May 29, 2018 Acquirer JAB Holding Company Acquirer Description Privately held German conglomerate that includes investments of companies operating in the arenas of consumer goods, forestry, coffee, luxury fashion, and fast food, among others Already owns Panera, Au Bon Pain, Caribou Coffee, Krispy Kreme, and Keurig Headquartered in Luxembourg Target Company Pret A Manger Target Description International sandwich shop chain commonly referred to simply as "Pret” with approximately 530 locations in nine countries Controlled by the investment firm Bridgepoint Advisers Revenue of 879 million pounds last year Founded in 1983 and headquartered in London Acquirer Advisor HSBC Target Advisor JP Morgan Price / Consideration $2 billion Cash Rationale Since 2012, JAB Holdings, backed by Germany’s wealthy and secretive Reimann family, has spent tens of billions of dollars to assemble a huge portfolio of brands, expanding its coffee and beverage empire It began with coffee, as JAB sought to challenge the industry heavyweight Nestlé. JAB made deals for Peet’s Coffee, Caribou Coffee, Stumptown and more. Then came restaurants like Krispy Kreme and the fast‐casual chain Panera. And this year, JAB helped Keurig Green Mountain, which the conglomerate bought and combined with Mondelez’s former coffee arm, move into soft drinks with an $18.7 billion deal for Dr Pepper Snapple "Management's proven track record and commitment to customer service, investment in innovation and -

JAB to Buy Keurig Green Mountain for $13.9B

Deal of the Week: JAB to Buy Keurig Green Mountain for $13.9B Announcement Date December 7, 2015 Acquirer JAB Holding Company Acquirer Description European consumer products conglomerate Target Keurig Green Mountain, Inc. (NASDAQ: GMCR) Target Description Produces and sells coffeemakers and specialty coffee in the United States, Canada, and internationally Founded in 1981 and headquartered in Waterbury, Vermont Target Financial Mkt Cap: $13.4 billion LTM EBITDA: $1.1 billion Statistics EV: $8.1 billion LTM EV / Revenue: 1.8x LTM Revenue: $4.5 billion LTM EV / EBITDA: 7.6x Target Advisors Bank of America and Credit Suisse provided fairness opinions to Keurig Green Mountain Price / Consideration Price: $13.9 billion Consideration: Cash Rationale Acquiring Keurig Green Mountain is JAB’s latest and biggest move yet to capitalize on consumers’ craving for coffee “Keurig Green Mountain represents a major step forward in the creation of our global coffee platform,” Bart Becht, the chairman of JAB, said in the statement. “Keurig Green Mountain will operate as an independent entity to ensure it will further build on its coffee and technology strength and continue to serve all its partners to the best of its abilities.” “This transaction will deliver significant cash value for our shareholders and offers an exciting new chapter for our customers, partners and employees by combining Keurig Green Mountain with JAB’s global coffee platform,” added Brian Kelley, CEO of Keurig Green Mountain Deal Points JAB will acquire Keurig Green Mountain for $92 a share in cash, a 78% premium over its stock price on Dec. 4 To acquire Keurig, JAB joined with several firms that are already investors in Jacobs Douwe Egberts. -

Iamabroadcaster Delegate Book 2015

P10 AGENDA P14 SPEAKERS Your guide to two days of Who is contributing to this AIB informative sessions outstanding conference Association for International Broadcasting #iamabroadcaster TWO DAYS OF HIGH-LEVEL DISCUSSION AND DEBATE ABOUT THE INTERNATIONAL MEDIA INDUSTRY | LONDON | 18-19 FEBRUARY 2015 Conference agenda AIB Association for International Broadcasting PRACTICAL INFORMATION #iamabroadcaster Twitter Mobile phones Video recording You can tweet about today’s event As a courtesy to your colleagues AIB will record the conference. - we have created the hashtag of at the conference, please ensure By entering the conference premises, you give your #iamabroadcaster for the that your mobile is switched to consent to be filmed. conference. silent when you are in the You also agree not to record or digitise any parts of Follow AIB @aibnews on twitter. conference. the event. Refreshments and lunch Transportation Refreshments will be served in The closest Underground stations are Regent’s Park – on the Bakerloo line – and Oxford the reception area adjacent to the Circus – on the Bakerloo, Central and Victoria lines. Traditional black cabs can be booked in main conference auditorium. advance through Radio Taxis by calling 020 7272 0272. Mini cabs can be booked through Lunch will be served in the Addison Lee by calling 020 7387 8888. We also recommend Uber which offers an efficient Florence Hall on the first floor. service in London. Quote the RIBA postcode when booking your taxi – W1B 1AD Smoking After the conference We would like to make this event non-smoking – and Photographs and speaker presentations - for those who have granted it is important to remember that smoking is not permission - will be available in the week following the event. -

Panera Bread (Houston MSA) 6439 Garth Road Baytown, Texas 77521 Panera Bread | Baytown, TX Table of Contents

Net Lease Investment Offering Panera Bread (Houston MSA) 6439 Garth Road Baytown, Texas 77521 Panera Bread | Baytown, TX Table of Contents TABLE OF CONTENTS Offering Summary Executive Summary ................................................................... 1 Investment Highlights ............................................................. 2 Property Overview ...................................................................... 3 Location Overview Photographs ...................................................................................4 Location Aerial .............................................................................. 5 Site Plan ..............................................................................................6 Location Map ................................................................................. 7 Market Overview Demographics ..............................................................................8 Market Overviews .......................................................................9 Tenant Summary Tenant Profile .................................................................................11 www.bouldergroup.com | Confidential Offering Memorandum Panera Bread | Baytown, TX Executive Summary EXECUTIVE SUMMARY The Boulder Group is pleased to exclusively market for sale a single tenant net leased Panera Bread property located within the Houston MSA in Baytown, Texas. Panera Bread has been in this location since June 2013. There are over 12 years remaining on the primary term of the -

What Millennials Want Fro M Tv

W HAT M ILLENNIALS W ANT F RO M TV Author: Colin Dixon, Founder and Chief Analyst, nScreenMedia | Date: Q3 2014 www.nScreenMedia.com This paper is made possible by the generous contribution of: Introduction After years of growth the pay television industry has Stalwarts of the industry are confident that they will hit a plateau. In the US, while the pundits argue about win the millennial consumer’s business. Jeff Bewkes, small gains and losses, the core number of households Time Warner Inc. CEO, said recently, “Once they with pay television has been stuck at about a hundred <millennials> take the mattress and get it off the floor, million for the last few years. In the UK, it is the same that’s when they subscribe to TV.” 1 Is he right, as story. Sky, the leading pay-TV provider in the UK, has millennials age will they subscribe to pay television, struggled to continue growth beyond 10.5 million just as their parents did? Unfortunately, there is homes. evidence that attracting the young customer is harder than it has ever been before. Though the overall number of subscribers may not be changing, operators must work very hard just to keep This paper will examine the dimensions of the those that they have today. In this daily battle for problems facing operators in attracting millennial customers, one of the most important age groups for consumers. It will look at the increasingly important operators to focus on is the 18 to 29-year-olds, the so- role of social media in the video experience, called millennial generation. -

JAB Holding to Buy Krispy Kreme for $1.35B

Deal of the Week: JAB Holding to Buy Krispy Kreme for $1.35B Announcement Date May 9, 2016 Acquirer JAB Holding Company Acquirer Description Billionaire European family Investment arm of the Reimann family, heirs to the German consumer goods conglomerate, Joh. A. Benckiser Target Company Krispy Kreme Doughnuts, Inc. (NYSE: KKD) Target Description Operates as a branded retailer and wholesaler of doughnuts, coffee and other complementary beverages, and treats and packaged sweets Founded in 1937 and headquartered in Winston‐Salem, North Carolina Target Financial Mkt Cap: $1.3 billion LTM EBITDA: $68.9 million Statistics EV: $1.0 billion LTM EV / Revenue: 2.0x LTM Revenue: $513.7 million LTM EV / EBITDA: 15.1x Acquirer Advisors Barclays and BDT & Company Target Advisor Wells Fargo Price / Consideration $1.35 billion Cash Rationale With the deal, the JAB Holding Company will add to its trove of coffee‐ oriented businesses, including Peet’s Coffee & Tea, Stumptown Coffee Roasters and Caribou Coffee In December, JAB acquired Keurig Green Mountain for $13.9 billion, its biggest bet yet in building its coffee empire “We are thrilled to have such an iconic brand as Krispy Kreme joining the JAB portfolio,” said Peter Harf, senior partner at JAB, in the statement. “This is yet another example of our commitment to investing in extraordinary brands with significant growth prospects.” Deal Points JAB plans to acquire Krispy Kreme for $21 a share in cash, a premium of more than 25% from Friday’s closing price BDT Capital Partners, -

Six Emerging Trends in Media and Communications Occasional Paper

Six emerging trends in media and communications Occasional paper NOVEMBER 2014 Canberra Melbourne Sydney Red Building Level 32 Level 5 Benjamin Offices Melbourne Central Tower The Bay Centre Chan Street 360 Elizabeth Street 65 Pirrama Road Belconnen ACT Melbourne VIC Pyrmont NSW PO Box 78 PO Box 13112 PO Box Q500 Belconnen ACT 2616 Law Courts Queen Victoria Building Melbourne VIC 8010 NSW 1230 T +61 2 6219 5555 T +61 3 9963 6800 T +61 2 9334 7700 F +61 2 6219 5353 F +61 3 9963 6899 1800 226 667 F +61 2 9334 7799 Copyright notice http://creativecommons.org/licenses/by/3.0/au/ With the exception of coats of arms, logos, emblems, images, other third-party material or devices protected by a trademark, this content is licensed under the Creative Commons Australia Attribution 3.0 Licence. We request attribution as: © Commonwealth of Australia (Australian Communications and Media Authority) 2014. All other rights are reserved. The Australian Communications and Media Authority has undertaken reasonable enquiries to identify material owned by third parties and secure permission for its reproduction. Permission may need to be obtained from third parties to re-use their material. Written enquiries may be sent to: Manager, Editorial and Design PO Box 13112 Law Courts Melbourne VIC 8010 Tel: 03 9963 6968 Email: [email protected] Contents Introduction 1 Communication goes OTT 6 Consumers build their own communications links 10 Wearable devices—personalised data arrives 15 ‘Flexible’ TV—online expands viewer options 19 Multi-screening is mainstream 25 TV is still the main news source, even as platforms shift 30 | iii Introduction The ACMA monitors industry and consumer data to identify changes in the media and communications environment and their impact on regulatory settings.