India Daily, February 27, 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tobacco Labelling -.:: GEOCITIES.Ws

Council Directive 89/622/EC concerning the labelling of tobacco products, as amended TAR AND NICOTINE CONTENTS OF THE CIGARETTES SOLD ON THE EUROPEAN MARKET AUSTRIA Brand Tar Yield Nicotine Yield Mg. Mg. List 1 A3 14.0 0.8 A3 Filter 11.0 0.6 Belvedere 11.0 0.8 Camel Filters 14.0 1.1 Camel Filters 100 13.0 1.1 Camel Lights 8.0 0.7 Casablanca 6.0 0.6 Casablanca Ultra 2.0 0.2 Corso 4.0 0.4 Da Capo 9.0 0.4 Dames 9.0 0.6 Dames Filter Box 9.0 0.6 Ernte 23 13.0 0.8 Falk 5.0 0.4 Flirt 14.0 0.9 Flirt Filter 11.0 0.6 Golden Smart 12.0 0.8 HB 13.0 0.9 HB 100 14.0 1.0 Hobby 11.0 0.8 Hobby Box 11.0 0.8 Hobby Extra 11.0 0.8 Johnny Filter 11.0 0.9 Jonny 14.0 1.0 Kent 10.0 0.8 Kim 8.0 0.6 Kim Superlights 4.0 0.4 Lord Extra 8.0 0.6 Lucky Strike 13.0 1.0 Lucky Strike Lights 9.0 0.7 Marlboro 13.0 0.9 Marlboro 100 14.0 1.0 Marlboro Lights 7.0 0.6 Malboro Medium 9.0 0.7 Maverick 11.0 0.8 Memphis Classic 11.0 0.8 Memphis Blue 12.0 0.8 Memphis International 13.0 1.0 Memphis International 100 14.0 1.0 Memphis Lights 7.0 0.6 Memphis Lights 100 9.0 0.7 Memphis Medium 9.0 0.6 Memphis Menthol 7.0 0.5 Men 11.0 0.9 Men Light 5.0 0.5 Milde Sorte 8.0 0.5 Milde Sorte 1 1.0 0.1 Milde Sorte 100 9.0 0.5 Milde Sorte Super 6.0 0.3 Milde Sorte Ultra 4.0 0.4 Parisienne Mild 8.0 0.7 Parisienne Super 11.0 0.9 Peter Stuyvesant 12.0 0.8 Philip Morris Super Lights 4.0 0.4 Ronson 13.0 1.1 Smart Export 10.0 0.8 Treff 14.0 0.9 Trend 5.0 0.2 Trussardi Light 100 6.0 0.5 United E 12.0 0.9 Winston 13.0 0.9 York 9.0 0.7 List 2 Auslese de luxe 1.0 0.1 Benson & Hedges 12.0 1.0 Camel 15.0 1.0 -

Tobacco Tax Administration

WHO TECHNICAL MANUAL ON Tobacco Tax Administration WHO TECHNICAL MANUAL ON Tobacco Tax Administration WHO Library Cataloging-in-Publication Data WHO technical manual on tobacco tax administration 1. Taxes. 2. Tobacco industry – legislation. 3.Tobacco – economics. 4. Smoking – prevention and control. I. World Health Organization. ISBN 978 92 4 156399 4 (NLM classification: WM 290) Reprinted with executive summary, 2011 © World Health Organization 2010 All rights reserved. Publications of the World Health Organization can be obtained from WHO Press, World Health Organization, 20 Avenue Appia, 1211 Geneva 27, Switzerland (tel.: +41 22 791 3264; fax: +41 22 791 4857; e-mail: [email protected]). Requests for permission to reproduce or translate WHO publications – whether for sale or for noncommercial distribution – should be addressed to WHO Press, at the above address (fax: +41 22 791 4806; e-mail: [email protected]). The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of the World Health Organization concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. Dotted lines on maps represent approximate border lines for which there may not yet be full agreement. The mention of specific companies or of certain manufacturers’ products does not imply that they are endorsed or recommended by the World Health Organization in preference to others of a similar nature that are not mentioned. Errors and omissions excepted, the names of proprietary products are distinguished by initial capital letters. -

1 CO-OPERATION AGREEMENT Dated As of 27 September 2010

CO-OPERATION AGREEMENT dated as of 27 September 2010 among IMPERIAL TOBACCO LIMITED AND THE EUROPEAN UNION REPRESENTED BY THE EUROPEAN COMMISSION AND EACH MEMBER STATE LISTED ON THE SIGNATURE PAGES HERETO 1 ARTICLE 1 DEFINITIONS Section 1.1. Definitions........................................................................................... 7 ARTICLE 2 ITL’S SALES AND DISTRIBUTION COMPLIANCE PRACTICES Section 2.1. ITL Policies and Code of Conduct.................................................... 12 Section 2.2. Certification of Compliance.............................................................. 12 Section 2.3 Acquisition of Other Tobacco Companies and New Manufacturing Facilities. .......................................................................................... 14 Section 2.4 Subsequent changes to Affiliates of ITL............................................ 14 ARTICLE 3 ANTI-CONTRABAND AND ANTI-COUNTERFEIT INITIATIVES Section 3.1. Anti-Contraband and Anti-Counterfeit Initiatives............................ 14 Section 3.2. Support for Anti-Contraband and Anti-Counterfeit Initiatives......... 14 ARTICLE 4 PAYMENTS TO SUPPORT THE ANTI-CONTRABAND AND ANTI-COUNTERFEIT COOPERATION ARTICLE 5 NOTIFICATION AND INSPECTION OF CONTRABAND AND COUNTERFEIT SEIZURES Section 5.1. Notice of Seizure. .............................................................................. 15 Section 5.2. Inspection of Seizures. ...................................................................... 16 Section 5.3. Determination of Seizures................................................................ -

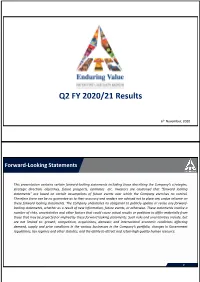

Q2 FY 2020/21 Results

Q2 FY 2020/21 Results 6th November, 2020 Forward‐Looking Statements This presentation contains certain forward‐looking statements including those describing the Company’s strategies, strategic direction, objectives, future prospects, estimates etc. Investors are cautioned that “forward looking statements” are based on certain assumptions of future events over which the Company exercises no control. Therefore there can be no guarantee as to their accuracy and readers are advised not to place any undue reliance on these forward looking statements. The Company undertakes no obligation to publicly update or revise any forward‐ looking statements, whether as a result of new information, future events, or otherwise. These statements involve a number of risks, uncertainties and other factors that could cause actual results or positions to differ materially from those that may be projected or implied by these forward looking statements. Such risks and uncertainties include, but are not limited to: growth, competition, acquisitions, domestic and international economic conditions affecting demand, supply and price conditions in the various businesses in the Company’s portfolio, changes in Government regulations, tax regimes and other statutes, and the ability to attract and retain high quality human resource. 2 Daily Covid cases rose sharply in Aug & Second Wave in Europe & USA Sep’20; sharp fall in Oct’20 India : New Cases – Moving 7‐day Average (‘000s) Global : New Cases – Moving 7‐day Average (‘000s) 100 17 Sep’20 160 90 Daily New Cases – 97,894 -

ITC Sustainability Award for India's Million Smoking Deaths by John R

WhyQuit Law of Addiction Joel's Library Freedom Turkeyville How to Quit FOR IMMEDIATE FREE RELEASE Contact: John R. Polito Saturday, April 20, 2014 [email protected] PDF of this article 01 (843) 797-3234 ITC sustainability award for India's million smoking deaths by John R. Polito India is home to 12% of the world's smokers (120 million), nearly one million annual smoking related deaths, and arguably the world's most brazen tobacco company, ITC Limited. ITC Ltd was originally known as Imperial Tobacco Company and then India Tobacco Company. But name changes cannot hide the fact that 82 percent of 2012-13 ITC profits came Question: How many millions of lives did ITC from cigarette sales. Nor can it hide corporate greed kill during 100 "inspiring" years? Why is it permitted inside India's schools? Click British American Tobacco's 30% image for higher resolution. ownership of ITC. ITC's website boasts, "ITC is the market leader in cigarettes in India. With its wide range of invaluable brands, ITC has a leadership position in every segment of the market. ITC's highly popular portfolio of brands includes Insignia, India Kings, Lucky Strike, Classic, Gold Flake, Navy Cut, Players, Scissors, Capstan, Berkeley, Bristol, Flake, Silk Cut, Duke & Royal." "Invaluable" brands? "Highly popular"? What ITC website visitors are not told is that smoking nicotine is highly addictive, that 80-90 percent of all lung cancers are attributable to smoking, or that 40-50 percent of ITC's nicotine addicts smoke themselves to death, with up to one-quarter dying during middle-age. -

38 2000 Tobacco Industry Projects—A Listing (173 Pp.) Project “A”: American Tobacco Co. Plan from 1959 to Enlist Professor

38 2000 Tobacco Industry Projects—a Listing (173 pp.) Project “A”: American Tobacco Co. plan from 1959 to enlist Professors Hirsch and Shapiro of NYU’s Institute of Mathematical Science to evaluate “statistical material purporting to show association between smoking and lung cancer.” Hirsch and Shapiro concluded that “such analysis is not feasible because the studies did not employ the methods of mathematical science but represent merely a collection of random data, or counting noses as it were.” Statistical studies of the lung cancer- smoking relation were “utterly meaningless from the mathematical point of view” and that it was “impossible to proceed with a mathematical analysis of the proposition that cigarette smoking is a cause of lung cancer.” AT management concluded that this result was “not surprising” given the “utter paucity of any direct evidence linking smoking with lung canner.”112 Project A: Tobacco Institute plan from 1967 to air three television spots on smoking & health. Continued goal of the Institute to test its ability “to alter public opinion and knowledge of the asserted health hazards of cigarette smoking by using paid print media space.” CEOs in the fall of 1967 had approved the plan, which was supposed to involve “before-and-after opinion surveys on elements of the smoking and health controversy” to measure the impact of TI propaganda on this issue.”113 Spots were apparently refused by the networks in 1970, so plan shifted to Project B. Project A-040: Brown and Williamson effort from 1972 to 114 Project AA: Secret RJR effort from 1982-84 to find out how to improve “the RJR share of market among young adult women.” Appeal would 112 Janet C. -

ITC Ltd (ITC) | 243 Target : | 277 Target Period : 12 Months Potential Upside : 14% Cigarette Volumes Back on Track

Result Update October 28, 2016 Rating matrix Rating : Buy ITC Ltd (ITC) | 243 Target : | 277 Target Period : 12 months Potential Upside : 14% Cigarette volumes back on track... • ITC reported 7.8% YoY growth in revenue for Q2FY17 to | 13491.4 What’s changed? crore (I-direct estimate: | 14,288.7 crore). The company witnessed Target Unchanged EPS FY17E Changed from | 8.8 to | 8.7 7.1% YoY growth in cigarette business. FMCG segment grew EPS FY18E Changed from | 10.0 to | 9.7 strongly by 13.3% YoY largely driven by volumes supported by Rating Unchanged brand building and consumer/trade promotion activities. Hotels & agri business grew moderately by 2.5% and 2.0%, respectively; Quarterly performance however, paperboard remained flat | crore Q2FY17 Q2FY16 YoY (%) Q1FY17 QoQ (%) • Our estimates suggest cigarette volume growth in the quarter was Sales 13491.4 12511.8 7.8 13156.7 2.5 ~3-4% YoY and cigarette price hike was ~3%, which was lower than EBITDA 3630.0 3382.7 7.3 3526.2 2.9 our annual estimate of 10%. The company is consciously increasing EBITDA (%) 26.7 26.8 -16 bps 26.6 5 bps PAT 2500.0 2262.5 10.5 2384.7 4.8 the contribution 64 mm cigarettes due to lower tax incidence. • EBITDA margin remained largely flat on YoY basis to 26.7%. Other Key financials income grew substantially by 21.1% YoY leading to a 10.5% YoY | Crore FY15 FY16 FY17E FY18E growth in profit to | 2500.0 crore (I-direct estimate: | 2737.6 crore) Revenue 36,083.2 51,582.5 55,862.9 62,711.6 Cigarette volume growth bounced back in FY17E EBITDA 13,473.6 13,717.9 15,134.2 17,064.0 Net Profit 9,607.7 9,311.3 10,501.2 11,746.7 ITC, the undisputed leader in cigarettes (~75% volume share), has been EPS (|) 8.0 7.7 8.7 9.7 witnessing moderation in volume growth since FY14. -

Télécharger Le Journal Au Format PDF 2,46 MB

CENT QUATORZI6113 ANNÉE - N° 5.911 Le Numéro 0,65 F VENDREDI 8 JANVIER 1911 JOURNAL DE MONACO Bulletin Officiel de la Principauté JOURNAL HEBDOMADAIRE PARAISSANT LE VENDREDI ABONNEMENTS: UN AN DIRECTION - RÉDACTION MONACO - FRANCE ET COMMUNAUTÉ 25.00 F ADMINISTRATION Annexe de la «Propriété Industrielle» seule 10.00 F HOTEL DU GOUVERNEMENT ÉTRANGER: 32.00 F Changement d'adresse: 0.50 F Téléphone 30.19.21 Les Abonnements parlent du le' de chaque année . Compte Chèque Postal: 3019.4/ - Marseille INSERTIONS LÉGALES : 2.30 F . la ligne SOMMAIRE Ordonnance Souveraine n° 4.642 du 4 janler 1971 portant nomination d'un Secrétaire aux Œuvre Sociales de la Mairie (p. 23). MAISON SOUVERAINE Ordonnance Souveraine n° 4.643 du 4 janvier 1971 portant nomination d'un archiviste à la Mairie (p. 24). Ordonnance Souveraine n° 4.644 du 4 janvier 1971 portant nomi- Viner au Palais Princier (p. 17). nation d'une dactylographe-comptable à la Trésorerie Générale Déjeuna- au Palais Princier (p. 18). des Finances (p. 24). ORDONNANCES SOUVERAINES ARRÊTÉS MINISTÉRIELS Ordonnance Souveraine n° 4.630 du 2 janvier 1971 portant Arrêté Ministériel n° 70-419 du 14 décembre 1970 convoquant réduction du taux d'intérêt des obligations cautionnées (p. 19). le Collège Electoral (p. 25). usance Souveraine n° 4.631 du 2 janvier 1971 eonvogriant Arrêté Ministériel no 70-434 du 31 décembre 1970 fixant le le Conseil National en session extraordinaire (p. 19). prix de vente des tabacs (p. 25), Ordonnance Souveraine n° 4.632 du 4 janvier 1971 fixant les Arrêté Ministériel n° 70-435 du 31 décembre 1970 portant modi- porPons saisissables et cessibles des rémunérations, traite- fication du taux de remise aux débitants de tabacs (p. -

India the Tax Treatment of Bidis

P r o f e s s o r S i r J o h n C r o f t o n Dear Colleague: Tobacco is the world’s leading single agent of death, and India is the world’s second- largest consumer of tobacco. In India, bidis account for the great majority of smoked tobacco, and they are no less harmful than cigarettes. Having worked at intervals in India and with many Indian colleagues for more than 50 years, I remain deeply concerned about the current and growing epidemic of illness and death from tobacco, including from bidis. The attached report from Emil Sunley, one of the world’s leading experts on tobacco taxation, shows not only that taxes on bidis should increase, but also lays out a rational, detailed plan for how to do so. Sunley’s conclusions are clear: • On a per-stick basis, bidis are at least as harmful as cigarettes, but the excise on bidis is only 8% that of the most similar type of cigarettes, and less than 1% that of standard cigarettes. • Excise duty accounts for only 9% of the retail price of bidis; the recommended international benchmark for taxation from a health point of view is 70% or higher. • Between half and three quarters of all bidis are completely untaxed, either because of exemptions or tax evasion. Sunley’s recommendations are equally clear. To rationalize taxation and protect health, policymakers should: • In the immediate term, increase the excise rate on bidis from Rs 14 to at least Rs 168 per 1,000 sticks – resulting in a tax rate identical to that of the most similar type of cigarette. -

Février 2020

Bulletin fficiel Numéro 301 O FÉVRIER 2020 MINISTÈRE DE LA CULTURE Bulletin officiel Février 2020 Bulletin officiel 301 Directrice de la publication : Marie Villette Rédacteur en chef : Hugues Ghenassia-de Ferran Secrétaire de rédaction : Éric Rouard Contact : Véronique Van Temsche Ministère de la Culture Secrétariat général Service de la coordination des politiques culturelles et de l'innovation Mission de la politique documentaire 182, rue Saint-Honoré, 75033 Paris Cedex 1. Tél : 01 40 15 38 29 ISSN : 2556-0883 2 Bulletin officiel 301 SOMMAIRE Mesures de publication et de signalisation Administration générale Lignes directrices de gestion « mobilité » (janvier 2020). Page 7 Arrêté du 6 février 2020 portant nomination d’un haut fonctionnaire en charge du handicap Page 12 et de l’inclusion. Décision du 26 février 2020 modifiant la décision du 21 décembre 2018 fixant la composition Page 12 du comité technique d’administration centrale. Arrêté du 28 février 2020 portant désignation de la personne responsable de l’accès aux Page 12 documents administratifs et des questions relatives à la réutilisation des informations publiques. Centre national d’art et de culture Georges-Pompidou Décision du 25 février 2020 portant délégation de signature au Centre national d’art et de Page 13 culture-Georges-Pompidou. Création artistique - Administration générale Arrêté du 11 février 2020 désignant les experts pouvant être sollicités par les membres du jury Page 32 chargé de la sélection des pensionnaires de l’Académie de France à Rome pour l’année 2020. Arrêté du 11 février 2020 modifiant l’arrêté du 17 décembre 2019 nommant les membres Page 33 du jury chargé de la sélection des pensionnaires de l’Académie de France à Rome pour l’année 2020. -

WHO Report on the Global Tobacco Epidemic, 2017 Country Profile: India

WHO report on the global tobacco epidemic, 2017 Country profile India WHO Framework Convention on Tobacco Control (WHO FCTC) status Date of signature 10 September 2003 Date of ratification (or legal equivalent) 5 February 2004 Socioeconomic context Population 1 326 801 576 Income group Middle -income National tobacco control programme as at 31 December 2016 Specific national government objectives in tobacco control Yes National agency or technical unit for tobacco control Yes Number of full-time equivalent staff 400 Government’s expenditures on tobacco control, latest available year INR (2015), in currency reported by country 400 000 000 Summary of MPOWER measures M P O W E R MONITORING SMOKE -FREE CESSATION HEALTH MASS ADVERTISING TAXATION CIGARETTES POLICIES PROGRAMMES WARNINGS MEDIA BANS LESS AFFORDABLE SINCE 2008 YES The legend explaining the colours in this table appears at the end of this document. The methods used to derive all data in this profile are described in the technical notes of the WHO report on the global tobacco epidemic, 2017. WHO report on the global tobacco epidemic, 2017 Country Profile: India Prevalence of tobacco use Tobacco use data from the latest survey results as at 31 December 2016 Youth tobacco use Adult tobacco smoking Adult cigarette smoking Current Prevalence Current cigarette Current Daily Current Daily (%) tobacco use smoking Male 19.0 5.8 24.3 18.3 10.3 6.3 Female 8.3 2.4 2.9 2.4 0.8 0.6 Total 14.6 4.4 14.0 10.7 5.7 3.6 Youth: Global Youth Tobacco Survey, 2009; National, ages 13-15 Adult: Global Adult -

Imperial Tobacco Comments on the Proposal for a Directive of the European Parliament and the Council on the Approximation Of

Imperial Tobacco comments on the Proposal for a Directive of the European Parliament and the Council on the approximation of the laws, regulation and administrative provisions of Member States concerning the manufacture, presentation and sale of tobacco and related products. COM(2012) 788 final (EU Scrutiny Committee reference 34587) 21 February 2013 Proposal for a Directive of the European Parliament and the Council on the approximation of the laws, regulation and administrative provisions of Member States concerning the manufacture, presentation and sale of tobacco and related products. COM(2012) 788 final (EU Scrutiny Committee reference 34587) 2 Page 5 February 2013 Proposal for a Directive of the European Parliament and the Council on the approximation of the laws, regulation and administrative provisions of Member States concerning the manufacture, presentation and sale of tobacco and related products. COM(2012) 788 final (EU Scrutiny Committee reference 34587) Introduction Imperial Tobacco is a FTSE 30 Company based in Bristol UK representing approximately 46% of the UK tobacco market. Imperial Tobacco submits these comments for consideration due to our serious concerns with regards to the Proposal for a Directive of the European Parliament and the Council on the approximation of the laws, regulation and administrative provisions of Member States concerning the manufacture, presentation and sale of tobacco and related products. COM(2012) 788 final (‘the Proposal’). Background: The Tobacco Products Directive The Tobacco Products Directive 2001/37/EC as amended currently govern the “manufacture, presentation and sale of tobacco products”. It covers, for example, the size and content of written warnings, the listing of ingredients and the banning of descriptions such as “mild” or “light”.