Local Planning Strategy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cultural Plan

APPENDIX 12 ATTACHMENT 1 Cultural Plan 2021 - 2025 This plan is available upon request in alternative languages and formats upon request. joondalup.wa.gov.au ii City of Joondalup – Cultural Plan 2021 City of Joondalup – Cultural Plan 2021 iii Contents Executive Summary ............ iv Context .............................. 4 Culture in the City of Joondalup .............. 8 Developing the Plan ............ 14 The Plan ............................ 17 Reviewing the Plan and Monitoring Progress ........... 23 The City acknowledges the custodians of this land, the Whadjuk Noongar and their Elders past, present and emerging. The City acknowledges and respects their continuing culture and the contribution they make to the life of this city and this region. iv City of Joondalup – Cultural Plan 2021 Executive Summary Since its early days, the City has developed a The resulting Cultural Plan has been developed to reputation for managing high quality cultural respond to these community sentiments, increasing destinations, assets and events, many of which access to the arts, and embedding cultural moments appeal to visitors from the wider Perth metropolitan in everyday life. The Plan provides strategic direction area. In doing so the City has successfully for the City of Joondalup’s activities for the period of demonstrated how culture plays a significant 2021 - 2025, ensuring investment is directed towards role in visitor and resident attraction, community the programming and infrastructure most valued cohesiveness and quality of life. by the community. This includes strategic initiatives which grow the City’s cultural capacity and audience, From its inception as a newly formed local in consideration of future plans for signficant cultural government in the late 1990s, the City of Joondalup infrastructure including the proposed Joondalup has successfully implemented cultural events such as Performing Arts Facility. -

Metropolitan Area Recreation Advisory Group Minutes

Metropolitan Area Recreation Advisory Group Minutes Department of Local Government, Sport and Cultural Industries 264 Vincent Street, Leederville Thursday 4 July 2019 – 11am 1.0 WELCOME, ATTENDANCE AND APOLOGIES 1.1 Welcome Patrick Quigley welcomed attendees to the inaugural meeting of the Metropolitan Area Recreation Advisory Group (MARAG). Patrick advised that the aim of MARAG was to provide leadership, coordination, advocacy and strategic direction relevant to the development and operation of metropolitan sport and recreation facilities, programs, services and projects. 1.2 Attending Patrick Quigley - City of South Perth David Bruce - City of Bayswater Marissa MacDonald - WALGA Jonelle Morley – DLGSC Alyce Atkinson – DLGSC Clayton White - DLGSC Leith Fradd – PLAWA Colby Halpin – City of Armadale Courtney Amlett – Town of Cambridge Dean Burton – City of Cockburn Tim Dayman – Town of Bassendean Salvatore Siciliano – Town of Bassendean Dan Barber – City of Bayswater Rachael Rowcroft – City of Gosnells Shane Fraser – City of Joondalup Stewart Winfield – Shire of Mundaring Amanda Cronin - City of Nedlands Sam Hegney – City of Rockingham Jason Parker- Shire of Serpentine-Jarrahdale Jess Fordham – City of South Perth Julie Rechichi – City of Subiaco Amy Fuller – City of Subiaco Michael Hayes – City of Subiaco Sarah Perkins – City of Swan Sarah Kitis – Town of Victoria Park Wayne Grimes – City of Vincent Sandra Watson – City of Vincent Samantha Culliver – City of Wanneroo Craig Bartlett – City of Wanneroo Wayne Stuart – City of Wanneroo Dan -

10.1.1 Local Government Reform - Update

COUNCIL MEETING 15 December 2014 10.1.1 LOCAL GOVERNMENT REFORM - UPDATE ATTACHMENTS 1. Letter Local Government Advisory Board 2. Media Statement Funding Package for Reforming Local Government 3. Media Statements Landmark Reports Sets Out New Look for Metro Perth 4. Local Government Advisory Board Notice Right to Request A Poll 5. Information Sheet Proposed City of Riversea Landmark report sets out new look for metro Perth Wednesday, 22 October 2014 Release of the Local Government Advisory Board report on metropolitan local government reform Board recommends Perth’s 30 councils be reduced to 16 Minister accepts all but two of the report’s boundary recommendations in the biggest shake-up of local government in 100 years Government to introduce City of Perth Act to reflect capital’s status New local governments will have increased financial sustainability and capacity to cope with Perth’s population growth The State Government today released the Local Government Advisory Board report, which provides the framework for the most significant reform of metropolitan local government in 100 years. Of the report's boundary recommendations for metropolitan Perth, Local Government Minister Tony Simpson has accepted all but two, those for the City of Perth/City of Vincent and the proposed City of Riversea, which includes five western suburbs councils. The Minister has rejected the Board’s recommendation for the City of Perth, on the basis that key icons such as The University of Western Australia (UWA) and the Queen Elizabeth II Medical Centre (QEII), were not included. As a result of the flow-on effects from City of Perth changes, he has also rejected the recommendation for the proposed City of Riversea, which includes five western suburbs councils. -

City of Melville Health and Wellbeing Profile 2019

City of Melville Health and Wellbeing Profile 2019 South Metropolitan Health Service Health Promotion Page 1 of 23 Acknowledgment The South Metropolitan Health Service (SMHS) respectfully acknowledges the Aboriginal Noongar people both past and present, the traditional owners of the land on which we work. Notes In this report: The terms ‘City of Melville’ and ‘Melville LGA’ are used interchangeably. The use of the term ‘Aboriginal’ within this document refers to Australians of both Aboriginal and Torres Strait Islander people. Important disclaimer All information and content in this material is provided in good faith by the WA Department of Health, and is based on sources believed to be reliable and accurate at the time of development. The State of Western Australia, the WA Department of Health and their respective officers, employees and agents, do not accept legal liability or responsibility for the material, or any consequences arising from its use. Abbreviations ABS Australian Bureau of Statistics AIHW Australian Institute of Health and Welfare BMI Body mass index CI Confidence interval DoH Department of Health, Western Australia ERP Estimated resident population HWSS Health and Wellbeing Surveillance System LGA Local government area NHPA National Health Priority Areas RSE Relative standard error SMHS South Metropolitan Health Service SMHS- HP South Metropolitan Health Service – Health Promotion WA Western Australia City of Melville Health and Wellbeing Profile 2019 Page 2 of 23 Contents Acknowledgment 2 Abbreviations 2 About this -

Eric Street Local Centre Additional

TOWN OF COTTESLOE TOWN OF COTTESLOE LOCAL PLANNING SCHEME NO. 3 AMENDMENT NO. 7 PLANNING AND DEVELOPMENT ACT 2005 RESOLUTION DECIDING TO AMEND A LOCAL PLANNING SCHEME TOWN OF COTTESLOE LOCAL PLANNING SCHEME NO. 3 AMENDMENT NO. 7 RESOLVED that the Council, in pursuance of Section 75 of the Planning and Development Act 2005, amend the above local planning scheme by: a) Amending Schedule 2 - Additional Uses of the Town of Cottesloe Local Planning Scheme No. 3 as follows: No. Description of land Additional use Conditions A10 Lot 50 (RN 36) Eric Medical Centre. Use and/or development of the site for Street, Cottesloe. Additional Uses shall be subject to planning approval. b) Modifying the Scheme Maps accordingly to reflect the Additional Use No. A10 over Lot 50 Eric Street, Cottesloe as provided for on the attached Scheme Amendment Map. The Amendment is standard under the provisions of the Planning and Development (Local Planning Schemes) Regulations 2015 (the Regulations) for the following reasons: 1. Pursuant to Regulation 34(a) of the Regulations, the amendment relates to a zone that is consistent with the objectives identified in the scheme for that zone or reserve; 2. Pursuant to Regulation 34(e) of the Regulations, it is considered that the amendment would have minimal impact on land in the scheme area that is not the subject of the amendment; and 3. Pursuant to Regulation 34(f) of the Regulations, it is considered that the amendment does not result in any significant environmental, social, economic or governance impact on land in the scheme area. -

Wildlife Enhancement Plan 2014–2019 Aims to Support Increased Biodiversity and the Conservation of Native Fauna and Fauna Habitat Within the Local Environment

Wildlife Enhancement Plan 2014 – 2019 www.subiaco.wa.gov.au Goal statement The Wildlife Enhancement Plan 2014–2019 aims to support increased biodiversity and the conservation of native fauna and fauna habitat within the local environment. Acknowledgements The city would like to thank Danielle Bowler from the City of Joondalup, Tamara Kabat from Bird Life Australia, Mathew Swan from the Department of Parks and Wildlife and Jake Tanner from the City of Fremantle for assisting with the development of this plan. The City of Subiaco is committed to protecting the global environment through local action. By printing this publication on Australian made 100 per cent recycled paper, the city aims to conserve the resources of the city. The document is available via the Internet at www.subiaco.wa.gov.au TABLE OF CONTENTS Table of contents Executive summary 4 Key definitions 5 Introduction 6 Wildlife conservation and enhancement 7 Parks, reserves and street trees 7 Wetlands 7 Greenways and remnant bushland areas 8 Aboriginal cultural significance 8 Community education 8 Management of identified risks 10 Climate change 10 Feral animals 10 Domestic animals 10 Plant pathogens 10 Resources and useful links 11 References 12 Appendix A: Fauna list 13 Photo courtesy of Margaret Owen CITY OF SUBIACO 2014 –2019 WILDLIFE ENHANCEMENT PLAN | 3 EXECUTIVE SUMMARY Executive summary The Wildlife Enhancement Plan 2014–2019 aims to support increased biodiversity and the conservation of native fauna and fauna habitat within the city’s local environment. The plan includes actions to enhance wildlife conservation, as well as provide education and participation opportunities for the community. -

Planning for Better Noise and Health Outcomes in the City of Cockburn

Planning for Better Noise and Health Outcomes in the City of Cockburn cockburn.wa.gov.au City of Cockburn’s Noise Attenuation Policy Policy and Guidelines describe: • When to engage an Acoustic Consultant • Reporting processes for Planning, Building • Clarifies requirements for the City of Cockburn in accordance with: o Environmental Protection (Noise) Regs (EPNRs) o SPP 4.1 – State Industrial Buffer o EPA Guidance No. 3 Separation Distances Between Industrial & Sensitive Land Uses o SPP 5.3 – Jandakot Airport Vicinity o SPP 5.4 - Road & Rail Transport Noise • Clarifies that amenity considerations are required for planning applications Where is the City of Cockburn? City of Fremantle City of Melville City of Canning City of Gosnells 8km south of Fremantle 24 km City of south of Armadale Perth Shire of City of Kwinana Serpentine Jarrahdale Mixed Use Development Areas ‘Intensive Mixed Use Community Areas’ • Transport Noise (SPP5.3 and SPP5.4) • What about other intrusive noise?? o Industrial and/or Commercial Noise Sources (EPNRs and SPP4.1) o Ambient Noise . ‘Vibrant’ Town Centre Notification on Title? Cockburn Central West 8.5.2 Road Noise 8.5.1 Land Use Generated Noise… Cockburn Central West Midgegooroo Road Cockburn Central West • Land Use Generated Noise?? o Pre-Existing Industrial and New Commercial Noise Sources Midgegooroo Road Midgegooroo (EPNRs/SPP4.1) Industrial Area o Noise Emissions from Proposed Development (EPNRs) o Future Ambient Noise?? o What about the ARC?? . Isn’t exempt noise still intrusive? Cockburn Aquatic and Recreation -

CITY of MELVILLE Ephemera PR14522/MEL L CALL NO

CITY OF MELVILLE Ephemera PR14522/MELL To view items in the Ephemera collection, contact the State Library of Western Australia CALL NO. DESCRIPTION PR14522/MEL/1 Melville public libraries. Hours of opening. Pamphlet. 15 February 1968 PR14522/MEL/2 Official celebration dinner. Toast list and banquet menu and quotations. 2 May 1968 PR14522/MEL/3 A portrait of your city. Pamphlet. August 1974 PR14522/MEL/4 Canning Bridge Public Library. An introduction to the library service. Pamphlet. 1974 PR14522/MEL/5 Invitation to meet WA author Gerald Glaskin. 9 June 1976 PR14522/MEL/6 Melville public libraries. Writer's evening. WA author Gerald Glaskin. Pamphlet. 1977 PR14522/MEL/7 Town of Melville public libraries readers ticket & bookcard. 1977 PR14522/MEL/8 Melville public libraries. Members card. 1977 PR14522/MEL/9 Melville public libraries. New books request slip. 1968 PR14522/MEL/10 Melville public libraries. Date return card. 1968 PR14522/MEL/11 The occasion to mark the Grant of Armorial Bearings to the Municipality of City of Melville. 26 July 1981 D PR14522/MEL/12 Wireless Hill Park and Telecommunications Museum. Pamphlet. October 1981 PR14522/MEL/13 Wireless Hill Park and Telecommunications Museum. Pamphlet. February 1984 PR14522/MEL/14 Social Welfare Service. Pamphlet. 1985 PR14522/MEL/15 Southern Districts Community Recreation Centre. Second term programme. 4 May 1987 PR14522/MEL/16 Residents' and Ratepayers' Association Inc. Sub‐Committee to amend Melville Town Planning Scheme No 3. 4 December 1985 PR14522/MEL/17 Residents' and Ratepayers' Association Inc. Re Melville Town Planning Scheme No 3. 3 December 1985 PR14522/MEL/18 What is happening to Alfred Cove. -

Recreational Waters Bacterial Quality Monitoring Program Swan and Canning Rivers - Global Positioning System - Reference Points

Recreational Waters Bacterial Quality Monitoring Program Swan and Canning Rivers - Global Positioning System - Reference Points GPS Deci GPS Deci Water Site Code Site Name LGA District Managing Authority Degs_S Degs_E body EV3/522 Sandy Beach Reserve -31.92215 115.95087 BASSENDEAN Town of Bassendean River EV3/548 Point Reserve (Nth Jetty) -31.9041 115.962726 BASSENDEAN Town of Bassendean River EV3/523 Hind Reserve (Garratt Rd - Jetty) -31.93125 115.91724 BAYSWATER City of Bayswater River EV3/541 East St Maylands Yacht Club -31.93723 115.89096 BAYSWATER City of Bayswater River EV3/517 Garvey Park (Fauntleroy Ave) -31.92121 115.94295 BELMONT City of Belmont River Belmont Park Beach (End Beach - EV3/538 -31.95349 115.89873 BELMONT City of Belmont River Goodwood Pd) EV3/539 Cracknell Park (Riversdale Rd) -31.95391 115.90326 BELMONT City of Belmont River EV3/542 Shelly Beach (Near Drain) -32.02762 115.88249 CANNING City of Canning River EV3/547 Clontarf Bay (Cadets) -32.02088 115.89865 CANNING City of Canning River EV3/545 Preston Point - John Tonkin Park -32.02903 115.76196 EAST FREMANTLE Town of East Fremantle River EV3/505 Bicton Baths -32.0276 115.77819 MELVILLE City of Melville River EV3/507 Cunningham St (Applecross) -32.02252 115.82608 MELVILLE City of Melville River EV3/532 Point Walter (Kiosk) -32.01294 115.79115 MELVILLE City of Melville River EV3/533 Point Walter (Boat Ramps) -32.0121 115.78834 MELVILLE City of Melville River EV3/534 Waylen Bay (Scout Hall) -32.00445 115.84057 MELVILLE City of Melville River EV3/540 Deep Water Point -

Town of East Fremantle News JULY 2015

Town of East Fremantle News JULY 2015 TOWN OF EAST FREMANTLE UPCOMING EVENTS Art Exhibition Army Art – Strategic Community 7-9 August at Leeuwin Barracks Council Meetings - Plan - Biennial Review 21 July 2015, 18 August 2015 With amalgamation well behind us, the Town of East Garage Sale Trail – Fremantle elected members and staff recently embarked 26 October 2015 on the two year (biennial) review of the Town’s Strategic Community Plan 2013-2023 (the Plan). The Plan was initially developed and was a key factor in deciding whether the the consultation and engagement process adopted by Council in 2013 and sets out direction of the Plan was still relevant. will be widely advertised to ensure there the vision, aspirations and objectives for is an opportunity for stakeholders and There has been some rewording of the Town over the next 10 years. And, to community members to get involved. the Plan to include Governance and ensure that what is planned for can be Leadership and Council is confident that A copy of the (revised) Strategic achieved, consideration is given to the the strategic direction outlined in the Community Plan 2013-2023 will be financial, asset and workforce constraints updated Plan will in turn shape actions available late July - please go to our that we work within. that will deliver realistic benefits for the website www.eastfremantle.wa.gov.au or With that in mind the review process community. email [email protected] to involved a number of workshops with the obtain a copy. The Council is looking forward to the Mayor, Councillors and senior staff who set major review of the Plan, which will involve about reconsidering the stated objectives a comprehensive community consultation in the Plan. -

Parklets Guidelines

HomelessnessParklets Strategy 2020-2022Guidelines Welcome and acknowledgement of Country City of Stirling kaadatj Nyoongar moort Nyoongar boodja-k Wadjak boodja-k, Mooro boodja-k. Ngalak kaadatj Nyoongar nedingar wer birdiya, baalap barn boodja-k wer kaaratj boodja-k koora koora wer yeyi. Ngalak kaadatj baalabang malayin wer nakolak baalap yang ngalany-al City of Stirling dandjoo Nyoongar moort-al kolbang koorliny. The City of Stirling acknowledges the Wadjak People of the Nyoongar Nation as the traditional custodians of Mooro Country. We pay our respects to Aboriginal and Torres Strait Islander Elders past and present for they hold the memories, the traditions, the culture and hopes for Aboriginal Australia. “ There is no single Background cause or solution to homelessness.” What is homelessness? How do people become homeless? The Australian Bureau of Statistics (ABS) The causes of homelessness are numerous and definition states that when a person does not complex. Contributing factors that increase the have suitable accommodation alternatives, they risk of homelessness are classified as ‘causal are considered homeless if their current living factors’ and these include: arrangement: • Financial stressors, including poverty, lack • Is in a dwelling that is inadequate or of affordable housing and available rental housing, lack of superannuation in retirement , • Has no tenure, or if their initial tenure and cost of living pressures is short and not extendable or • Vulnerability of people exiting facilities such • Does not allow them to have control of, as prison, care facilities, hospitals, and drug and access to space for social relations. and alcohol treatment • Health including physical, mental, and disability • System failures and structural factors • Individual circumstances , including family Being homeless and domestic violence, discrimination, Mayor’s Message addictions, and traumatic events and is not a crime. -

Tabled Paper [I

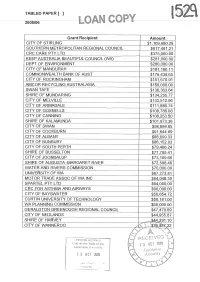

TABLED PAPER [I 2005/06 Grant Recipient Amount CITY OF STIRLING 1,109,680.28 SOUTHERN METROPOLITAN REGIONAL COUNCIL $617,461.21 CRC CARE PTY LTD $375,000.00 KEEP AUSTRALIA BEAUTIFUL COUNCIL (WA) $281,000.00 DEPT OF ENVIRONMENT $280,000.00 ITY OF MANDURAH $181,160.11 COMMONWEALTH BANK OF AUST $176,438.65 CITY OF ROCKINGHAM $151,670.91 AMCOR RECYCLING AUSTRALASIA 50,000.00 SWAN TAFE $136,363.64 SHIRE OF MUNDARING $134,255.77 CITY OF MELVILLE $133,512.96 CITY OF ARMADALE $111,880.74 CITY OF GOSNE LS $108,786.08 CITY OF CANNING $108,253.50 SHIRE OF KALAMUNDA $101,973.36 CITY OF SWAN $98,684.85 CITY OF COCKBURN $91,644.69 CITY OF ALBANY $88,699.33 CITY OF BUNBURY $86,152.03 CITY OF SOUTH PERTH $79,466.24 SHIRE OF BUSSELTON $77,795.41 CITY OF JOONDALUP $73,109.66 SHIRE OF AUGUSTA -MARGARET RIVER $72,598.46 WATER AND RIVERS COMMISSION $70,000.00 UNIVERSITY OF WA $67,272.81 MOTOR TRADE ASSOC OF WA INC $64,048.30 SPARTEL PTY LTD $64,000.00 CRC FOR ASTHMA AND AIRWAYS $60,000.00 CITY OF BAYSWATER $50,654.72 CURTIN UNIVERSITY OF TECHNOLOGY $50,181.00 WA PLANNING COMMISSION $50.000.00 GERALDTON GREENOUGH REGIONAL COUN $47,470.69 CITY OF NEDLANDS $44,955.87_ SHIRE OF HARVEY $44,291 10 CITY OF WANNEROO 1392527_ 22 I Il 2 Grant Recisien Amount SHIRE OF MURRAY $35,837.78 MURDOCH UNIVERSITY $35,629.83 TOWN OF KWINANA $35,475.52 PRINTING INDUSTRIES ASSOCIATION $34,090.91 HOUSING INDUSTRY ASSOCIATION $33,986.00 GERALDTON-GREENOUGH REGIONAL COUNCIL $32,844.67 CITY OF FREMANTLE $32,766.43 SHIRE OF MANJIMUP $32,646.00 TOWN OF CAMBRIDGE $32,414.72 WA LOCAL GOVERNMENT