Mortgage Terminology Defined

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

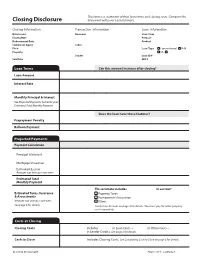

Closing Disclosure Document with Your Loan Estimate

This form is a statement of final loan terms and closing costs. Compare this Closing Disclosure document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued Borrower Loan Term Closing Date Purpose Disbursement Date Product Settlement Agent Seller File # Loan Type Conventional FHA Property VA _____________ Lender Loan ID # Sale Price MIC # Loan Terms Can this amount increase after closing? Loan Amount Interest Rate Monthly Principal & Interest See Projected Payments below for your Estimated Total Monthly Payment Does the loan have these features? Prepayment Penalty Balloon Payment Projected Payments Payment Calculation Principal & Interest Mortgage Insurance Estimated Escrow Amount can increase over time Estimated Total Monthly Payment This estimate includes In escrow? Estimated Taxes, Insurance Property Taxes & Assessments Homeowner’s Insurance Amount can increase over time Other: See page 4 for details See Escrow Account on page 4 for details. You must pay for other property costs separately. Costs at Closing Closing Costs Includes $5,877.00 in Loan Costs + $7,642.43 in Other Costs – $0 in Lender Credits. See page 2 for details. Cash to Close Includes Closing Costs. See Calculating Cash to Close on page 3 for details. CLOSING DISCLOSURE PAGE 1 OF 5 • LOAN ID # 0000000000 This form is a statement of final loan terms and closing costs. Compare this Closing Disclosure document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued Borrower Loan Term -

5/1 MOP Loan Program

GENERAL GUIDELINES 5/1 Maximum Loan-to-Value Ratio: Same as Standard MOP LTV Thresholds Fixed Rate Period: 5 Years ORTGAGE M Maximum Loan Term: 30 Years RIGINATION Qualifying Interest Rate: Initial 5/1 MOP Interest Rate O Minimum Interest Rate: 3.25% ROGRAM P Maximum Payment-to-Income Ratio: 40% Maximum Overall Debt-to-Income Ratio: 48% PROGRAM OVERVIEW 5/1 MOP Initial Interest Rate The 5/1 Mortgage Origination Program (5/1 MOP) loan is a fully-amortizing mortgage loan The initial fixed interest rate* in effect during the Fixed Rate that offers an initial fixed interest rate and payment for the first 5 years of the loan, after which Period of the loan is comprised of the following three (3) the loan converts to a 1-year adjustable rate mortgage (“Standard MOP”) for the remaining components: loan term. The maximum overall loan term is 30 years. All or any portion of the principal Index: 5-year Treasury Bond Yield balance may be prepaid without penalty at any time and there is no negative amortization associated with 5/1 MOP loans. For eligibility requirements, refer to the MOP Brochure. Spread: J.P. Morgan U.S. Liquid Index (JULI) Index Service Fee: .25% IMPORTANT CONSIDERATIONS: *The minimum 5/1 MOP Initial Interest Rate is 3.25% • The 5/1 MOP Initial Interest Rate may be higher or lower than the current Standard Rate offered for a Standard MOP loan. The current interest rate for each of these loan products is available at www.ucop.edu/loan-programs. QUESTIONS? • Fixed rate payments during the first 5 years of the loan provide a stable monthly payment Contact the local Campus Housing Programs to borrowers; however, there is potential for increased monthly payments when the Fixed Representative or the University of California Home Loan Rate Period ends. -

Homeowners and Reverse Mortgages

MLA :: 1-color logo :: PMS 1807c Maryland Legal Aid Offices Anne Arundel County Montgomery County 229 Hanover Street 600 Jefferson Plaza Annapolis, MD 21401 Suite 430 Reverse (410) 972-2700 Rockville, MD 20852 Maryland Legal Aid: Who We Are (800) 666-8330 (240) 314-0373 Mortgages Baltimore City (855) 880-9487 Maryland Legal Aid is a non-profi t law fi rm You should not take out a reverse mortgage if: 500 E. Lexington Street Northeastern Maryland Baltimore, MD 21202 Cecil, Harford 1911 since Maryland in All for Justice and Rights Human Advancing dedicated to providing high-quality legal • You feel rushed or pressured to take out a Telephone Intake Lines: 103 S. Hickory Avenue advocacy to protect and advance human rights reverse mortgage by someone, or do not (410) 951-7750 Bel Air, MD 21014 (866) MD LAW 4U (410) 836-8202 for Maryland’s most vulnerable low-income understand the loan. For example, some reverse (or 866-635-2948) (800) 444-9529 mortgage sellers promise to complete home individuals, families and communities. Business Line: Southern Maryland repairs, but then they do not complete the repairs. (410) 951-7777 Calvert, Charles, St. Mary’s You should talk to a lawyer if that has happened to (800) 999-8904 15045 Burnt Store Road Homeowners Baltimore County P.O. Box 249 What is a Reverse Mortgage? you. You can also fi le a complaint with the Maryland Hughesville, MD 20637 215 Washington Avenue Offi ce of the Attorney General (301) 932-6661 Suite 305 A reverse mortgage is a type of home loan for (877) 310-1810 (1-888-743-0023), the Consumer Financial Towson, MD 21204 and Reverse homeowners who are 62 years of age or older. -

Agency Guideline Revisions Note: Suntrust Mortgage Specific Overlays Are Underlined

Agency Guideline Revisions Note: SunTrust Mortgage specific overlays are underlined. Impacted Revised Guidelines Topic Impacted Products Current Guidelines Document Effective Immediately for NEW AND EXISTING Loan Applications ON OR After May 26, 2017 Appraisal Correspondent HomeReady® Appraisal Analysis: Agency Loan Programs / Improvements Section of the Appraisal Report Appraisal Analysis: Agency Loan Programs / Improvements Section of the Appraisal Report Requirements Section 1.07 Mortgage / Accessory Appraisal- (non-AUS & Non-AUS Non-AUS Units Guideline DU) Note: Below is an EXCERPT only of the guidance from the above referenced section. All other currently published Note: Below is an EXCERPT only of the guidance from the above referenced section. All other currently published Home guidelines from this section remain the same. guidelines from this section remain the same. Possible® Accessory Units Accessory Units Mortgage Fannie Mae will purchase a one-unit property with an accessory unit. An accessory unit is typically an Fannie Mae will purchase a one-unit property with an accessory unit. An accessory unit is typically an (LPA) additional living area independent of the primary dwelling unit, and includes a fully functioning additional living area independent of the primary dwelling unit, and includes a fully functioning kitchen and bathroom. Some examples may include a living area over a garage and basement units. kitchen and bathroom. Some examples may include a living area over a garage and basement units. Whether a property is defined as a one-unit property with an accessory unit or a two-unit property Whether a property is defined as a one-unit property with an accessory unit or a two-unit property will be based on the characteristics of the property, which may include, but are not limited to, the will be based on the characteristics of the property, which may include, but are not limited to, the existence of separate utilities, a unique postal address, and whether the unit is rented. -

Quiz 38:Financing

Quiz 38:Financing 1. An FHA-insured mortgage loan would be obtained from which of the following? a. The Federal Housing Administration b. The Department of Housing and Urban Development c. Any FHA-approved lending institution d. Any FHA-approved insuring institution 2. Fannie Mae a. makes FHA loans. c. services FHA loans. b. buys FHA loans. d. insures FHA loans. 3. The grantor becomes the lessee and the grantee becomes the lessor under which of the following financing arrangements? a. Partial sale c. Sale and leaseback b. Wraparound mortgage d. Assumption of mortgage 4. Members of which of the following pairs of terms are synonyms? a. Interim financing and construction loan b. Construction loan and passthrough loan c. Pass-through loan and takeout loan d. Takeout loan and construction loan 5. The type of real estate loan that allows the lender to increase the outstanding balance of a loan up to the original sum in the note while advancing additional funds is the a. wraparound mortgage. c. growing-equity mortgage. b. open-end mortgage. d. graduated-payment mortgage. 6. Richie has been making regular principal and interest payments on his mortgage, but the final payment will be larger than the others. This is a (n) a. balloon payment loan c. FHA loan b. fully amortized loan d. straight loan. 7. A mortgage broker generally offers which of the following services? a. Handling the escrow procedures b. Bringing the borrower and the lender together c. Providing credit qualification and evaluation reports d. Granting real estate loans using investor funds 8. -

The Tax Consequences of Wraparound Mortgages

Journal of Civil Rights and Economic Development Volume 2 Issue 2 Volume 2, 1987, Issue 2 Article 4 The Tax Consequences of Wraparound Mortgages Robert Liquerman Diane Di Franco Follow this and additional works at: https://scholarship.law.stjohns.edu/jcred This Comment is brought to you for free and open access by the Journals at St. John's Law Scholarship Repository. It has been accepted for inclusion in Journal of Civil Rights and Economic Development by an authorized editor of St. John's Law Scholarship Repository. For more information, please contact [email protected]. THE TAX CONSEQUENCES OF WRAPAROUND MORTGAGES Often in a sale of real property, the seller may elect to receive payment in installments, thereby providing the buyer with con- venient financing while securing for himself desirable tax advan- tages.1 The installment method of reporting allows a taxpayer who is to receive at least one payment after the year of a disposi- ' See I.R.C. § 453 (1982 & Supp. 1984). This section, which contains rules for reporting income under the installment method, provides in pertinent part: (b) Installment sale defined. - For purposes of this section- (1) In general. - The term "installment sale" means a disposition of property where at least I payment is to be received after the close of the taxable year in which the dispo- sition occurs. (c) Installment method defined. - For purposes of this section, the term "installment method" means a method under which the income recognized for any taxable year from a disposition is that proportion of the payments received in that year which the gross profit (realized or to be realized when payment is completed) bears to the total con- tract price. -

Adjustable-Rate Mortgage (ARM) Is a Loan with an Interest Rate That Changes

The Federal Reserve Board Consumer Handbook on Adjustable-Rate Mortgages Board of Governors of the Federal Reserve System www.federalreserve.gov 0412 Consumer Handbook on Adjustable-Rate Mortgages | i Table of contents Mortgage shopping worksheet ...................................................... 2 What is an ARM? .................................................................................... 4 How ARMs work: the basic features .......................................... 6 Initial rate and payment ...................................................................... 6 The adjustment period ........................................................................ 6 The index ............................................................................................... 7 The margin ............................................................................................ 8 Interest-rate caps .................................................................................. 10 Payment caps ........................................................................................ 13 Types of ARMs ........................................................................................ 15 Hybrid ARMs ....................................................................................... 15 Interest-only ARMs .............................................................................. 15 Payment-option ARMs ........................................................................ 16 Consumer cautions ............................................................................. -

Get a Glossary of Terms Used in the Title Industry

GLOSSARY A Abstract Plant – A geographically arranged abstract plant, currently kept to date, that is adequate for use in insuring titles, so as to provide for the safety and protection of the policyholders. An abstract plant as further defined in Rule P-12 and as further provided for in the Insurance Code, Chapter 2501.003 and Chapter 2502, must include an abstract plant for each county in which a title insurance agent or direct operation maintains an office. Abstract of Title - A compilation of all the recorded documents relating to a parcel of land. Usually kept by the land owner and used as the basis for an attorney as to the condition of title. Still in use in some states, and in some areas of Texas, but mostly replaced by issuance of title insurance. Abstract of Judgment – A lien created by a statutory filing of a court judgment in the real property records. This lien, commonly referred to as an AJ (in Texas), attaches to all non- exempt real property of the person or entity that the judgment was against. Acceleration Clause (in a mortgage) – Specifies conditions under which the lender may advance the time when the entire debt which is secured by the mortgage becomes due. For example, most mortgages contain provisions that the note shall become due immediately upon the sale of the securing land without the lender's consent or upon failure of the landowner to pay an installment when due. Access – The right to enter and leave a tract of land from a public way. Can include the right to enter and leave over the lands of another. -

Reverse Mortgage Servicing & Foreclosure: Emerging Issues

Reverse Mortgage Servicing & Foreclosure: Emerging Issues ISSUE BRIEF • APRIL 2017 Odette Williamson, Attorney, National Consumer Law Center The National Consumer Law Center The National Consumer Law Center uses its expertise in consumer law and energy policy to work for consumer justice and economic security for low-income and other disadvantaged people, including older adults and people of color. NCLC works with nonprofit and legal services organizations, private attorneys, policymakers, and federal and state government and courts across the nation to stop exploitive practices, help financially stressed families build and retain wealth, and advance economic fairness. Introduction Reverse mortgages allow older homeowners to convert equity in their homes into cash without having to move out and without having to make monthly mortgage payments. The mortgages allow older homeowners to age in place by supplementing income, providing funding for repairs or modifications to the home, or funds to meet other necessary expenses. Cashing out the equity in the home does come with some risks and costs. Recently there has been an uptick in reverse mortgage foreclosures due to default on property-related charges (e.g., taxes and insurance) and other issues despite options to cure these types of default and reinstate the mortgage. The challenges homeowners face in fulfilling the requirements of the mortgage have been exacerbated by poor or inadequate loan servicing. Poor servicing leads to quick foreclosure and ejectment of the elder from the home. Ms. Brown filed for bankruptcy after her loan servicer repeatedly refused to allow her to enter into a repayment plan to cure her property charge default and scheduled her home for sale. -

Reverse Mortgages a Discussion Guide

Reverse mortgages A discussion guide Consumer Financial Protection Bureau About this discussion guide This guide gives an overview of many key concepts of reverse mortgages. A qualified reverse mortgage counselor can help you learn more. If you’re interested in considering a reverse mortgage, but haven’t spoken with a counselor yet, call (800) 569-4287 to find a U.S. Department of Housing and Urban Development (HUD), hud.gov approved reverse mortgage counselor today. A detailed discussion with a counselor will give you important information to help you decide whether a reverse mortgage is right for you. HUD- approved reverse mortgage counselors have the latest information on reverse mortgages. In order to get the most out of your counseling session, come prepared to talk about: § Your financial needs and goals § Your spouse or partner’s future housing and financial needs § Other family members or dependents living with you and their future housing needs § The reasons you’re considering a reverse mortgage § The alternatives to a reverse mortgage you may have considered Alert Most reverse mortgages today are called Home Equity Conversion Mortgages (HECMs). HECMs are federally insured by the Federal Housing Administration (FHA). This guide covers typical features and requirements for HECM reverse mortgages. Non-HECM reverse mortgages may have different requirements and features. 1 How is a reverse mortgage different from a traditional mortgage? Traditional mortgages With a traditional mortgage, you usually borrow money to pay for the home at the time of the purchase, and pay it back over time. With each payment, you build your equity and your loan balance goes down. -

Reverse Mortgages: Forwards and Backwards

REVERSE MORTGAGES: FORWARDS AND BACKWARDS Bruce Levitt, Esq. Levitt & Slafkes (Maplewood) Victor Medina, Esq. Medina Law Group (Pennington) WRPP03136 © 2016 New Jersey State Bar Association. All rights reserved. Any copying of material herein, in whole or in part, and by any means without written permission is prohibited. Requests for such permission should be sent to NJICLE, a Division of the New Jersey State Bar Association, New Jersey Law Center, One Constitution Square, New Brunswick, New Jersey 08901-1520. Thank you for logging in – the webinar will begin shortly. WHAT EVERY ATTORNEY NEEDS TO KNOW ABOUT REVERSE MORTGAGES Using The Online Classroom 1. All Attendee phone lines are muted. 2. Questions may be submitted Via Chat on the right hand side of your screen. Questions will be answered periodically during the presentation Note: Attendees with dial up connections will see a slower response. Asking Questions – Easy as 1,2,3 3. See your messages here 1. Type your question here. 2. Send SEMINAR MATERIALS AND CLE FORMS • TO ACCESS SEMINAR MATERIALS, ATTENDANCE VERIFICATION AND CLE FORMS PLEASE GO TO: WWW.NJICLE.COM/WEBINAR ATTENDANCE VERIFICATION • PLEASE FAX OR E-MAIL YOUR ATTENDANCE VERIFICATION FORM TO NJ ICLE • FAX: 732-249-1428 • E-MAIL: [email protected] REVERSE MORTGAGES Reverse Mortgages - Two Parts • What Is It and How Does It Get Set-Up? • How Do They Go Wrong Reverse Mortgages - What Are They • Bank loan for people 62 and older against their home equity. • Repayment is deferred until you sell or die, or some other trigger of default. • Amount available depends on equity, age, prevailing interest rates. -

World Bank Document

Policy Research Working Paper 9134 Public Disclosure Authorized Reverse Mortgages, Financial Inclusion, and Economic Development Public Disclosure Authorized Potential Benefit and Risks Peter Knaack Margaret Miller Fiona Stewart Public Disclosure Authorized Public Disclosure Authorized Finance, Competitiveness and Innovation Global Practice January 2020 Policy Research Working Paper 9134 Abstract This paper examines the state of reverse mortgage markets constraints are equally relevant, in particular high non-in- in selected countries around the world and considers the terest costs, abuse concerns, and the inability of reverse potential benefits and risks of these products from a financial mortgages to cover key risks facing the elderly, particularly inclusion and economic benefit standpoint. Despite poten- health and elder care. In developing countries, constraints tially increasing demand from aging societies—combined are likely to be even higher than in advanced economies, due with limited pension income—a series of market failures to high transaction costs and lack of consumer knowledge constrain supply and demand. The paper discusses a series and protection. The enabling conditions for such markets of market failures on the supply side, such as adverse selec- to develop are outlined, along with examples of regulatory tion, moral hazard, and the costly regulation established oversight. The paper concludes that these still seem to be to address these problems, leading to only a small number largely products of last resort rather than well-considered of providers, even in developed markets. Demand-side purchases as part of good retirement planning. This paper is a product of the Finance, Competitiveness and Innovation Global Practice. It is part of a larger effort by the World Bank to provide open access to its research and make a contribution to development policy discussions around the world.