Some Remarks About Financial Market Modelling Using a Minority Game Approach

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Introduction to Game Theory

Introduction to Game Theory June 8, 2021 In this chapter, we review some of the central concepts of Game Theory. These include the celebrated theorem of John Nash which gives us an insight into equilibrium behaviour of interactions between multiple individuals. We will also develop some of the mathematical machinery which will prove useful in our understanding of learning algorithms. Finally, we will discuss why learning is a useful concept and the real world successes that multi-agent learning has achieved in the past few years. We provide many of the important proofs in the Appendix for those readers who are interested. However, these are by no means required to understand the subsequent chapters. 1 What is a Game? What is the first image that comes to mind when you think of a game? For most people, it would be something like chess, hide and seek or perhaps even a video game. In fact, all of these can be studied under Game Theoretical terms, but we can extend our domain of interest much further. We do this by understanding what all of our above examples have in common I There are multiple players II All players want to win the game III There are rules which dictate who wins the game IV Each player's behaviour will depend on the behaviour of the others With these in place, we can extend our analysis to almost any interaction between mul- tiple players. Let us look at some examples, noticing in each, that components of a game that we discussed above show up in each of the following. -

Exact Solution of a Modified El Farol's Bar Problem: Efficiency and the Role

Exact solution of a modified El Farol’s bar problem: Efficiency and the role of market impact Matteo Marsili Istituto Nazionale per la Fisica della Materia (INFM), Trieste-SISSA Unit, V. Beirut 2-4, Trieste I-34014 Damien Challet Institut de Physique Th´eorique, Universit´ede Fribourg, CH-1700 and Riccardo Zecchina The Abdus Salam International Centre for Theoretical Physics Strada Costiera 11, P.O. Box 586, I-34014 Trieste Abstract We discuss a model of heterogeneous, inductive rational agents inspired by the El Farol Bar problem and the Minority Game. As in markets, agents interact through a collective aggregate variable – which plays a role similar to price – whose value is fixed by all of them. Agents follow a simple reinforcement-learning dynamics where the reinforcement, for each of their available strategies, is related to the payoff delivered by that strategy. We derive the exact solution of the model in the “thermodynamic” limit of infinitely many agents using tools of statistical physics of disordered systems. Our results show that the impact of agents on the market price plays a key role: even though price has a weak dependence on the behavior of each individual agent, the collective behavior crucially depends on whether agents account for such dependence or not. Remarkably, if the adaptive behavior of agents accounts even “infinitesimally” for this dependence they can, in a whole range of parameters, reduce global fluctuations by a finite amount. Both global efficiency and individual utility improve with respect to a “price taker” behavior if agents arXiv:cond-mat/9908480v3 [cond-mat.stat-mech] 8 Dec 1999 account for their market impact. -

Living in a Natural World"

DISSERTATION Titel der Dissertation "Living in a Natural World" or "Keeping it Real" Verfasser Mag. iur. Bakk. techn. Günther Greindl angestrebter akademischer Grad Doktor der Philosophie Wien, 2010 Department of Philosophy University of Vienna A-1010 Austria [email protected] Studienkennzahl lt. A 092 296 Studienblatt: Dissertationsgebiet lt. Philosophy Studienblatt: Betreuer: Prof. Franz Martin Wimmer and Prof. Karl Svozil This Page Intentionally Left Blank When superior students hear of the Way They strive to practice it. When middling students hear of the Way They sometimes keep it and sometimes lose it. When inferior students hear of the Way They have a big laugh. But "not laughing" in itself is not sufficient to be called the Way, and therefore it is said: The sparkling Way seems dark Advancing in the Way seems like regression. Settling into the Way seems rough. True virtue is like a valley. The immaculate seems humble. Extensive virtue seems insufficient. Established virtue seems deceptive. The face of reality seems to change. The great square has no corners. Great ability takes a long time to perfect. Great sound is hard to hear. The great form has no shape. The Way is hidden and nameless. This is exactly why the Way is good at developing and perfecting. – Daode Jing, Verse 41i i Translated by Charles Muller (LaoziMuller 2004) This Page Intentionally Left Blank Table of Contents 1 Introduction..................................................................................................................................1 -

Finding Core Members of Cooperative Games Using Agent- Based Modeling

Vernon-Bido and Collins December 2019 FINDING CORE MEMBERS OF COOPERATIVE GAMES USING AGENT- BASED MODELING Daniele Vernon-Bido, and Andrew J. Collins Old Dominion Unversity Norfolk, Virginia, USA [email protected] ABSTRACT Agent-based modeling (ABM) is a powerful paradigm to gain insight into social phenomena. One area that ABM has rarely been applied is coalition formation. Traditionally, coalition formation is modelled using cooperative game theory. In this paper, a heuristic algorithm is developed that can be embedded into an ABM to allow the agents to find coalition. The resultant coalition structures are comparable to those found by cooperative game theory solution approaches, specifically, the core. A heuristic approach is required due to the computational complexity of finding a cooperative game theory solution which limits its application to about only a score of agents. The ABM paradigm provides a platform in which simple rules and interactions between agents can produce a macro-level effect without the large computational requirements. As such, it can be an effective means for approximating cooperative game solutions for large numbers of agents. Our heuristic algorithm combines agent-based modeling and cooperative game theory to help find agent partitions that are members of a games’ core solution. The accuracy of our heuristic algorithm can be determined by comparing its outcomes to the actual core solutions. This comparison achieved by developing an experiment that uses a specific example of a cooperative game called the glove game. The glove game is a type of exchange economy game. Finding the traditional cooperative game theory solutions is computationally intensive for large numbers of players because each possible partition must be compared to each possible coalition to determine the core set; hence our experiment only considers games of up to nine players. -

A Game Theoretic Framework for Distributed Self-Coexistence Among IEEE 802.22 Networks

A game theoretic framework for distributed self-coexistence among IEEE 802.22 networks S. Sengupta and R. Chandramouli S. Brahma and M. Chatterjee Electrical and Computer Engineering Electrical Engineering and Computer Science Stevens Institute of Technology University of Central Florida Hoboken, NJ 07030 Orlando, FL 32816 Email: fShamik.Sengupta, [email protected] Email: fsbrahma,[email protected] Abstract—The cognitive radio based IEEE 802.22 wireless coexistence issues are only considered after the specification regional area network (WRAN) is designed to operate in the essentially is finalized, it is required for IEEE 802.22 to take under–utilized TV bands by detecting and avoiding primary TV the proactive approach and mandate to include self-coexistence transmission bands in a timely manner. Such networks, deployed by competing wireless service providers, would have to self- protocols and algorithms for enhanced MAC as revision of the coexist by accessing different parts of the available spectrum initial standard conception and definition [8]. in a distributed manner. Obviously, the goal of every network is In this paper, we focus on the self–coexistence of IEEE to acquire a clear spectrum chunk free of interference from other 802.22 networks from a game theoretic perspective. We use the IEEE 802.22 networks so as to satisfy the QoS of the services tools from minority game theory [5] and model the competitive delivered to the end–users. In this paper, we study the distributed WRAN self–coexistence problem from a minority game theoretic environment as a distributed Modified Minority Game (MMG). perspective. We model the spectrum band switching game where We consider the system of multiple overlapping IEEE 802.22 the networks try to minimize their cost in finding a clear band. -

A Survey of Collective Intelligence

A SURVEY OF COLLECTIVE INTELLIGENCE David H. Wolpert Kagan Turner NASA Ames Research Center NASA Ames Research Center Moffett Field, CA 94035 Caelum Research dhw@ptolemy, arc. nasa.gov Moffett Field, CA 94035 [email protected] April 1, 1999 Abstract This chapter presents the science of "COllective INtelligence" (COIN). A COIN is a large multi-agent systems where: i) the agents each run reinforcement learning (RL) algorithms; ii) there is little to no centralized communication or control; iii) there is a provided worht utility fimction that rates the possible histories of the full system. The conventional approach to designing large distributed systems to optimize a world utility dots not use agents running RL algorithms. Rather that approach begins with explicit modeling of the overall system's dynamics, followed by detailed hand-tuning of the interactions between the components to ensure that they "cooperate" as far as the world utility is concerned. This approach is labor-intensive, often results in highly non-robust systems, and usually results in design techniques that have limited applicability. In contrast, with COINs We wish to s})lve the system design problems implicitly, via the 'adaptive' character of the IlL algorithms of each of the agents. This COIN approach introduces an entirely new, profound design problem: Assuming the RL algorithms are able to achieve high rewards, what reward functions for the individual agents will, when pursued by those agents, result in high world utility? In other words, what reward fimctions will best ensure that we do not have phenomena like the tragedy of the commons, or Braess's paradox? Although still very young, the science of COINs has already resulted in successes in artificial domains, in particular in packet-routing, the leader-follower problem, and in variants of Arthur's "El Farol bar problem". -

'El Farol Bar Problem' in Netlogo

Modeling the ‘El Farol Bar Problem’ in NetLogo ∗ PRELIMINARY DRAFT Mark Garofalo† Dexia Bank Belgium Boulevard Pach´eco 44 B-1000 Brussels, Belgium http://www.markgarofalo.com Abstract believe most will go, nobody will go’ (Arthur (1994)). Resource limitation is characteristic to many other areas Arthur’s ‘El Farol Bar Problem’ (Arthur (1994)) is a such as road traffic, computer networks like internet or finan- metaphor of a complex economic systems’ model based on cial markets. These systems are complex in the sense that interaction and it is perfectly suited for the multi-agent sim- they composed by a large variety of elements and that the ulation framework. It is a limited resource model in which interaction in between these elements are non-linear and not agents are boundedly rational and where no solution can be completely captured (LeMoigne (1990), Kauffman (1993)). deduced a priori. In this paper we discuss in particular the Paraphrasing Casti (1996), in the EFBP the agents are in a implementation of the model in NetLogo, a multi-agent universe in which their ‘forecasts (...) act to create the world platform introduced by Wilensky (1999). Our aim is to they are trying to forecast’1. Arthur’s simple scenario pro- translate Arthur’s model described in natural language into vides useful insights into complex systems and this is why a workable computational agent-based tool. Throughout the it is viewed as paradigmatic. process of setting up the tool we discuss the necessary as- Modeling in mainstream economics is generally equation sumptions made for it’s implementation. We also conduct based. -

Coordination in the El Farol Bar Problem: the Role of Social Preferences and Social Networks

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Chen, Shu-Heng; Gostoli, Umberto Working Paper Coordination in the El Farol Bar problem: The role of social preferences and social networks Economics Discussion Papers, No. 2013-20 Provided in Cooperation with: Kiel Institute for the World Economy (IfW) Suggested Citation: Chen, Shu-Heng; Gostoli, Umberto (2013) : Coordination in the El Farol Bar problem: The role of social preferences and social networks, Economics Discussion Papers, No. 2013-20, Kiel Institute for the World Economy (IfW), Kiel This Version is available at: http://hdl.handle.net/10419/70481 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. http://creativecommons.org/licenses/by/3.0/ www.econstor.eu Discussion Paper No. -

When the El Farol Bar Problem Is Not a Problem? the Role of Social Preferences and Social Networks

When the El Farol Bar Problem Is Not a Problem? The Role of Social Preferences and Social Networks Shu-Heng Chen and Umberto Gostoli ? AI-ECON Research Center - National ChengChi University Abstract. In this paper, we study the self-coordination problem as demonstrated by the well-known El Farol Bar problem (Arthur, 1994), which later becomes what is known as the Minority Game in the econo- physics community. While the El Farol problem or the minority game has been studied for almost two decades, existing studies are most con- cerned with efficiency only. The equality issue, however, has been largely neglected. In this paper, we build an agent-based model to study both efficiency and equality and ask whether a decentralized society can ever possibly self-coordinate a result with highest efficiency while also main- taining a highest degree of equality. Our agent-based model shows the possibility of achieving this social optimum. The two key determinants to make this happen are social preferences and social networks. Hence, not only does institution (network) matters, but individual characteris- tics (preferences) also matters. The latter part is open for human-subject experiments for further examination. 1 Introduction The El Farol Bar problem, introduced by Arthur (1994) has become over the years the prototypical model of a system in which agents, competing for scarce resources, adapt inductively their belief-models (or hypotheses) to the aggre- gate environment they jointly create. The numerous works that have analyzed and extended along different lines this problem show that perfect coordination, that is, the steady state where the aggregate bar's attendance is always equal to the bar's maximum capacity, is very hard, not to say impossible, to reach, at least under the common knowledge assumption (Fogel, Chellapilla, and Ange- line (1999); Edmonds (1999), to name just a few). -

Statistical Modelling of Games

Statistical modelling of games by Yu Gao, MSci. Thesis submitted to the University of Nottingham for the degree of Doctor of Philosophy July 2016 Abstract This thesis mainly focuses on the statistical modelling of a selection of games, namely, the minority game, the urn model and the Hawk-Dove game. Chapters 1 and 2 give a brief introduction and survey of the field. In Chapter 3, the key characteristics of the minority game are reproduced. In addition, the minority game is extended to include wealth distribution and leverage effect. By assuming that each player has initial wealth which rises and falls according to profit and loss, with the potential of borrowing and bankruptcy, we find that modelled wealth distribution may be power law distributed and leverage increases the instability of the system. In Chapter 4, to explore the effects of memory, we construct a model where agents with memories of different lengths compete for finite resources. Using analytical and numerical approaches, our research demonstrates that an instability exists at a critical memory length; and players with different memory lengths are able to compete with each other and achieve a state of co-existence. The analytical solution is found to be connected to the well-known urn model. Additionally, our findings reveal that the temperature is related to the agent's memory. Due to its general nature, this memory model could potentially be relevant for a variety of other game models. In Chapter 5, our main finding is extended to the Hawk-Dove game, by introducing the memory parameter to each agent playing the game. -

Download Presentation Slides

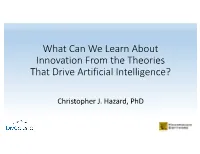

What Can We Learn About Innovation From the Theories That Drive Artificial Intelligence? Christopher J. Hazard, PhD Exploration (Discover New Things) Reinforcement Learning Unsupervised Learning Goal Oriented Accuracy Oriented (Measure Goodness) (Measure Accuracy) Optimization Supervised Learning Exploitation (Utilizing Existing Information) Example Domain: Food Awesomeness Nutrition Density Supervised Learning Given the other data, Unknown Figure out if this is Meal or Snack Meal Snack Awesomeness Nutrition Density Supervised Learning: Universal Function Approximators Model A Low Variance Model C Data Good Model Model B Low Bias Unsupervised Learning Given food, come up with categories Awesomeness Find anomalies Nutrition Unsupervised Learning: Clustering and Anomaly Detection Outlier Group 2 Outlier Group 1 Group 3 Reinforcement Learning Objective: eat a highly nutritious meal Unknown Meal Snack After getting the first guess right, it gets two wrong, 1 is corrected, learns from its mistakes, and decides how to learn next Awesomeness 2 3 4 Nutrition Density Reinforcement Learning: Seeking Rewards, filling in Unknowns Maximize Awesomeness & Nutrition Savory? Salty? Sweet? 50% Nutritious 70% Nutritious 10% Nutritious 40% Awesome 70% Awesome 90% Awesome Green? Yellow? Sour? 90% Nutritious 50% Nutritious ??? ??? 40% Nutritious ??? 5% Awesome 50% Awesome 50% Awesome Orange Tart Candy ??? ??? 100% Nutritious 0% Nutritious ??? 70% Awesome 90% Awesome Optimization Find the “best” meal Unknown Meal Snack Found the best meal Awesomeness Nutrition -

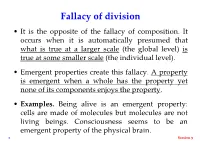

Fallacy of Division • It Is the Opposite of the Fallacy of Composition

Fallacy of division • It is the opposite of the fallacy of composition. It occurs when it is automatically presumed that what is true at a larger scale (the global level) is true at some smaller scale (the individual level). • Emergent properties create this fallacy. A property is emergent when a whole has the property yet none of its components enjoys the property. • Examples. Being alive is an emergent property: cells are made of molecules but molecules are not living beings. Consciousness seems to be an emergent property of the physical brain. 1 Session 3 “Because the coordinated macroeconomy is an emergent characteristic of uncoordinated micro behaviour, macro outcomes that are unexpected can emerge (in the sense that the outcomes are not consistent with the objectives of individuals). The most obvious example emphasized by classical and neoclassical economists is that the unconstrained pursuit of maximal profits by individuals operating in a competitive setting ends up reducing their profits to zero. The tragedy of the commons is another example well known to economists.” RG Lipsey, KI Carlaw, CT Bekar (2006): Economic Transformations: General Purpose Technologies and Long- Term Economic Growth, Oxford University Press, p. 37. 2 Session 3 Simpson’s paradox (or reversal paradox) • Related to the fallacy of division, it occurs when something true for different groups is false for the combined group. • Example. There are three groups, two periods, and the tax rate (taxes paid in relation to income) of each group. The tax rate of each group diminishes from t = 1 to t = 2, but, in the aggregate, the tax rate increases from t = 1 to t = 2.