2019 & 2017 Texas Legislative Issues

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

August 1, 2019 Texas Windstorm Insurance

August 1, 2019 Texas Windstorm Insurance Association, Board of Directors c/o John Polak, General Manager P.O. Box 99090 Austin, Texas 78709 Dear TWIA Board of Directors: We, the undersigned coastal members of the 86th Texas Legislature, respectfully request the Texas Windstorm Insurance Association (TWIA) board to postpone or reject consideration of any proposed rate increase on residential and commercial policyholders for the reasons outlined below. In early October, 2018, prior to the 86th Legislature convening, Governor Greg Abbott utilized his executive power in the aftermath of Hurricane Harvey to protect coastal homeowners and business owners from any unnecessary barrier that would impede recovery efforts post-disaster. He wrote a letter to the Texas Department of Insurance (TDI) Commissioner, Kent Sullivan, directing him to "delay any decision to approve or disapprove the proposed rate increase, and any deemed approval of the proposed rate increase, until the Legislature has had a full opportunity to address the matter." The Governor's order to suspend windstorm rates remained in effect until June 16, 2019. On May 24, 2019, the TWIA Board of Directors voted unanimously to withdraw the Association's annual rate filing made in August 2018. The Governor also emphasized the statutory timeframe within which the TWIA board and Commissioner of Insurance were required to consider rate adequacy: "strict compliance with this time frame would deprive the Legislature of the opportunity to address any actuarial deficiency in TWIA during the upcoming legislative session…". The 86th Legislature followed suit by passing significant legislation, Senate Bill 615 and House Bill 1900, addressing rate adequacy transparency and requiring two interim legislative committees, appointed by state leadership, to thoroughly inspect and review the current funding structure. -

2014 Texas State Voter Guide

2014 Texas State Voter Guide 2014 Texas Voter Guide Table of Contents • Importance in getting civically engaged • Important dates • Who is your representative The Texas chapter of the Council on American-Islamic Relations (CAIR-TX) has compiled some resources to help inform community members when they vote in the November 2014 elections. Enclosed are Texas School of Education, State Representatives, State Senators, Lt. Governor race, Governor’s race, and Congressional representatives. Policy information gathered on candidates is strictly from the respective candidates official websites. Where such a website was not available, information was taken from interviews directly with candidates, or the candidates’ respective political party official websites (i.e. Democrat, Republican and Libertarian). The amount of information listed on candidates’ profiles is based strictly on the information provided on their official websites, or (where necessary), interviews/party websites. No opinion pieces, news articles, opinion polls or opponent sited facts/opinions were used on the candidates’ profiles. No candidate profiles were made for unopposed positions. CAIR’s aim is to provide unbiased, bipartisan information on key candidates running in the November 2014 election cycle. While CAIR’s aim is to assist the voter with non-bias information, we encourage everyone to do his or her own research and to not rely solely on this brochure. If any information in our Election Voter Guide is found to be false or inaccurate, please contact us at (713) 838-2247 and we will make it our priority to correct any mistakes. The Council on American-Islamic Relations is the largest American Muslim civil rights and advocacy organization in the United States. -

IDEOLOGY and PARTISANSHIP in the 87Th (2021) REGULAR SESSION of the TEXAS LEGISLATURE

IDEOLOGY AND PARTISANSHIP IN THE 87th (2021) REGULAR SESSION OF THE TEXAS LEGISLATURE Mark P. Jones, Ph.D. Fellow in Political Science, Rice University’s Baker Institute for Public Policy July 2021 © 2021 Rice University’s Baker Institute for Public Policy This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and the Baker Institute for Public Policy. Wherever feasible, papers are reviewed by outside experts before they are released. However, the research and views expressed in this paper are those of the individual researcher(s) and do not necessarily represent the views of the Baker Institute. Mark P. Jones, Ph.D. “Ideology and Partisanship in the 87th (2021) Regular Session of the Texas Legislature” https://doi.org/10.25613/HP57-BF70 Ideology and Partisanship in the 87th (2021) Regular Session of the Texas Legislature Executive Summary This report utilizes roll call vote data to improve our understanding of the ideological and partisan dynamics of the Texas Legislature’s 87th regular session. The first section examines the location of the members of the Texas Senate and of the Texas House on the liberal-conservative dimension along which legislative politics takes place in Austin. In both chambers, every Republican is more conservative than every Democrat and every Democrat is more liberal than every Republican. There does, however, exist substantial ideological diversity within the respective Democratic and Republican delegations in each chamber. The second section explores the extent to which each senator and each representative was on the winning side of the non-lopsided final passage votes (FPVs) on which they voted. -

Sunday, May 26, 2013 — 82Nd

HOUSE JOURNAL EIGHTY-THIRD LEGISLATURE, REGULAR SESSION PROCEEDINGS EIGHTY-SECOND DAY Ð SUNDAY, MAY 26, 2013 The house met at 2 p.m. and was called to order by the speaker. The roll of the house was called and a quorum was announced present (Recordi1286). Present Ð Mr. Speaker; Alonzo; Anderson; Ashby; Aycock; Bell; Bonnen, G.; Branch; Burkett; Burnam; Button; Callegari; Canales; Capriglione; Carter; Clardy; Collier; Cook; Cortez; Craddick; Creighton; Dale; Darby; Davis, J.; Davis, S.; Deshotel; Dukes; Dutton; Elkins; Fallon; Farias; Farney; Fletcher; Flynn; Frank; Frullo; Geren; Goldman; Gonzales; GonzaÂlez, M.; Gonzalez, N.; Gooden; Guerra; Gutierrez; Harper-Brown; Hilderbran; Howard; Huberty; Hughes; Hunter; Isaac; Johnson; Kacal; Keffer; King, K.; King, P.; King, S.; King, T.; Kleinschmidt; Klick; Kolkhorst; Krause; Kuempel; Larson; Lavender; Leach; Lewis; Lozano; MaÂrquez; Martinez; Martinez Fischer; McClendon; Miller, D.; Miller, R.; Morrison; Murphy; Naishtat; NevaÂrez; Oliveira; Orr; Otto; Paddie; Parker; Patrick; Perez; Perry; Phillips; Pickett; Pitts; Price; Raney; Ratliff; Raymond; Riddle; Ritter; Rodriguez, E.; Rose; Sanford; Schaefer; Sheffield, J.; Sheffield, R.; Simmons; Simpson; Smith; Springer; Stephenson; Stickland; Taylor; Thompson, E.; Thompson, S.; Toth; Turner, C.; Turner, E.S.; Turner, S.; Villalba; Villarreal; Vo; White; Workman; Wu; Zedler; Zerwas. Absent Ð Allen; Alvarado; Anchia; Bohac; Bonnen, D.; Coleman; Crownover; Davis, Y.; Eiland; Farrar; Giddings; Guillen; Harless; Hernandez Luna; Herrero; Laubenberg; -

Amicus Brief of Former Speakers of the House

No. 21-0538 In the Supreme Court of Texas IN RE CHRIS TURNER, IN HIS CAPACITY AS A MEMBER OF THE TEXAS HOUSE OF REPRESENTATIVES AND HIS CAPACITY AS CHAIR OF THE HOUSE DEMOCRATIC CAUCUS; TEXAS AFL-CIO; HOUSE DEMOCRATIC CAUCUS; MEXICAN AMERICAN LEGISLATIVE CAUCUS; TEXAS LEGISLATIVE BLACK CAUCUS; LEGISLATIVE STUDY GROUP; THE FOLLOWING IN THEIR CAPACITIES AS MEMBERS OF THE TEXAS HOUSE OF REPRESENTATIVES: ALMA ALLEN, RAFAEL ANCHÍA, MICHELLE BECKLEY, DIEGO BERNAL, RHETTA BOWERS, JOHN BUCY, ELIZABETH CAMPOS, TERRY CANALES, SHERYL COLE, GARNET COLEMAN, NICOLE COLLIER, PHILIP CORTEZ, JASMINE CROCKETT, YVONNE DAVIS, JOE DESHOTEL, ALEX DOMINGUEZ, HAROLD DUTTON, JR., ART FIERRO, BARBARA GERVIN-HAWKINS, JESSICA GONZÁLEZ, MARY GONZÁLEZ, VIKKI GOODWIN, BOBBY GUERRA, RYAN GUILLEN, ANA HERNANDEZ, GINA HINOJOSA, DONNA HOWARD, CELIA ISRAEL, ANN JOHNSON, JARVIS JOHNSON, JULIE JOHNSON, TRACY KING, OSCAR LONGORIA, RAY LOPEZ, EDDIE LUCIO III, ARMANDO MARTINEZ, TREY MARTINEZ FISCHER, TERRY MEZA, INA MINJAREZ, JOE MOODY, CHRISTINA MORALES, EDDIE MORALES, PENNY MORALES SHAW, SERGIO MUÑOZ, JR., VICTORIA NEAVE, CLAUDIA ORDAZ PEREZ, EVELINA ORTEGA, LEO PACHECO, MARY ANN PEREZ, ANA-MARIA RAMOS, RICHARD RAYMOND, RON REYNOLDS, EDDIE RODRIGUEZ, RAMON ROMERO, JR., TONI ROSE, JON ROSENTHAL, CARL SHERMAN, SR., JAMES TALARICO, SHAWN THIERRY, SENFRONIA THOMPSON, JOHN TURNER, HUBERT VO, ARMANDO WALLE, GENE WU, AND ERIN ZWIENER; AND THE FOLLOWING IN THEIR CAPACITIES AS LEGISLATIVE EMPLOYEES: KIMBERLY PAIGE BUFKIN, MICHELLE CASTILLO, RACHEL PIOTRZKOWSKI, AND DONOVON RODRIGUEZ, Relators. Brief of Amici Curiae Former Speakers of the Texas House of Representatives and former Lieutenant Governor of the State of Texas in Support of Petition for Writ of Mandamus Jessica L. Ellsworth Blayne Thompson (pro hac vice application forthcoming) State Bar No. -

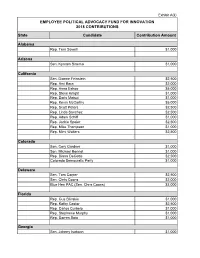

2018 BMS PAC Contributions

Exhibit A(ii) EMPLOYEE POLITICAL ADVOCACY FUND FOR INNOVATION 2018 CONTRIBUTIONS State Candidate Contribution Amount Alabama Rep. Terri Sewell $1,000 Arizona Sen. Kyrsten Sinema $1,000 California Sen. Dianne Feinstein $2,500 Rep. Ami Bera $2,000 Rep. Anna Eshoo $5,000 Rep. Steve Knight $1,000 Rep. Doris Matsui $1,000 Rep. Kevin McCarthy $5,000 Rep. Scott Peters $2,500 Rep. Linda Sanchez $2,500 Rep. Adam Schiff $1,000 Rep. Jackie Speier $2,500 Rep. Mike Thompson $1,000 Rep. Mimi Walters $2,500 Colorado Sen. Cory Gardner $1,000 Sen. Michael Bennet $1,000 Rep. Diana DeGette $2,500 Colorado Democratic Party $1,000 Delaware Sen. Tom Carper $2,500 Sen. Chris Coons $2,000 Blue Hen PAC (Sen. Chris Coons) $3,000 Florida Rep. Gus Bilirakis $1,000 Rep. Kathy Castor $2,500 Rep. Carlos Curbelo $1,000 Rep. Stephanie Murphy $1,000 Rep. Darren Soto $1,000 Georgia Sen. Johnny Isakson $1,000 Sen. David Perdue $2,000 Rep. Buddy Carter $2,500 Iowa Gov. Kim Reynolds $2,000 Sen. Chuck Grassley $2,500 State Sen. Charles Schneider $2,000 State Sen. Tom Shipley $500 Idaho Sen. Mike Crapo $5,000 Illinois Rep. Cheri Bustos $1,000 Rep. Bill Foster $1,000 Rep. Robin Kelly $1,000 Rep. Darin LaHood $1,000 Rep. Pete Roskam $1,000 Rep. Brad Schneider $1,000 Rep. John Shimkus $2,500 Indiana Sen. Mike Braun $1,000 Sen. Joe Donnelly $2,500 Rep. Larry Bucshon $2,500 Rep. Susan Brooks $2,000 Rep. Andre Carson $1,000 Rep. -

Environmental Assessment for Programmatic Safe Harbor Agreement for the Houston Toad in Texas

ENVIRONMENTAL ASSESSMENT FOR PROGRAMMATIC SAFE HARBOR AGREEMENT FOR THE HOUSTON TOAD IN TEXAS Between Texas Parks and Wildlife Department and U.S. Fish and Wildlife Service Prepared by: U.S. Fish and Wildlife Service 10711 Burnet Road, Suite 200 Austin, Texas 78758 TABLE OF CONTENTS 1.0 PURPOSE AND NEED FOR ACTION ……………………………………….. 1 1.1 INTRODUCTION ……………………………………………………………….. 1 1.2 PURPOSE OF THE PROPOSED ACTION …………………………………….. 1 1.3 NEED FOR TAKING THE PROPOSED ACTION …………………………….. 1 2.0 ALTERNATIVES ………………………………………………………………. 2 2.1 ALTERNATIVE 1: NO ACTION ………………………………………………. 2 2.2 ALTERNATIVE 2: ISSUANCE OF A SECTION 10(a)(1)(A) ENHANCEMENT OF SURVIVAL PERMIT AND APPROVAL OF A RANGEWIDE PROGRAMMATIC AGREEMENT (PROPOSED ACTION)........... 3 2.3 ALTERNATIVES CONSIDERED BUT ELIMINATED FROM DETAILED ANALYSIS ……………………………………………………………………… 5 3.0 AFFECTED ENVIRONMENT ……………………………………………….. 5 3.1 VEGETATION …………………………………………………………………... 6 3.2 WILDLIFE ………………………………………………………………………. 7 3.3 LISTED, PROPOSED, AND CANDIDATE SPECIES ………………………… 8 3.4 CULTURAL RESOURCES …………………………………………………….. 12 3.5 SOCIOECONOMIC ENVIRONMENT ………………………………………… 13 Austin County ……………………………………………………………………. 13 Bastrop County …………………………………………………………………... 13 Burleson County …………………………………………………………………. 13 Colorado County …………………………………………………………………. 14 Lavaca County …………………………………………………………………… 14 Lee County ……………………………………………………………………….. 14 Leon County ……………………………………………………………………… 14 Milam County ……………………………………………………………………. 15 Robertson County ………………………………………………………………... 15 3.6 WETLANDS -

TSTA-PAC 2018 Endorsements Primary Winners / Runoffs / Friendly Incumbents

TSTA-PAC 2018 Endorsements Primary Winners / Runoffs / Friendly Incumbents Ryan Guillen - Rio Grande City HD 31** Republican Texas Senate Eric Johnson - Dallas HD 100** Kel Seliger - Amarillo SD 31** Jarvis Johnson - Houston HD 139 Julie Johnson - Dallas HD 115 Texas House of Representatives Ina Minjarez -San Antonio HD 124 Steve Allison – San Antonio HD 121* René O. Oliveira - Brownsville HD 37* Ernest Bailes - Shepherd HD 18 Ron Reynolds - Missouri City HD 27** Keith Bell - Forney HD 4 Shawn Thierry - Houston HD 146** Travis Clardy - Nacogdoches HD 11 John Turner - Dallas HD 114 Scott Cosper - Killeen HD 54* Dan Flynn - Van HD 2 State Board of Education Charlie Geren - Fort Worth HD 99 Ruben Cortez, Jr. - Brownsville SBOE 2 Cody Harris - Palestine HD 8 Marisa B. Perez - San Antonio SBOE 3 Dan Huberty - Houston HD 127** Ken King - Canadian HD 88 General Election Early Endorsement Chris Paddie - Marshall HD 9** Texas Senate Four Price - Amarillo HD 87** Democratic John Raney - Bryan HD 14 Kirk Watson - Austin SD 14 J.D. Sheffield - Gatesville HD 59** Royce West - Dallas SD 23 Hugh Shine - Temple HD 55** Reggie Smith - Sherman HD 62 Texas House of Representatives Lynn Stucky - Sanger HD 64 Democratic Alma Allen - Houston HD 131 Rafael Anchia - Dallas HD 103 Democratic Lt. Governor Nicole Collier - Fort Worth HD 95 Mike Collier - Houston Jessica Farrar - Houston HD 148 Abel Herrero - Robstown HD 34 Texas Senate Gina Hinojosa - Austin HD 49 Beverly Powell - Tarrant SD 10 Donna Howard - Austin HD 48 Nathan Johnson - Dallas SD 16 Victoria Neave - Dallas HD 107 John Whitmire - Houston SD 15 Mary Ann Perez - Houston HD 144 Joseph C. -

Hearing Committee on Oversight and Government

OBAMACARE IMPLEMENTATION: WHO ARE THE NAVIGATORS? HEARING BEFORE THE COMMITTEE ON OVERSIGHT AND GOVERNMENT REFORM HOUSE OF REPRESENTATIVES ONE HUNDRED THIRTEENTH CONGRESS FIRST SESSION DECEMBER 16, 2013 Serial No. 113–82 Printed for the use of the Committee on Oversight and Government Reform ( Available via the World Wide Web: http://www.fdsys.gov http://www.house.gov/reform U.S. GOVERNMENT PRINTING OFFICE 87–014 PDF WASHINGTON : 2014 For sale by the Superintendent of Documents, U.S. Government Printing Office Internet: bookstore.gpo.gov Phone: toll free (866) 512–1800; DC area (202) 512–1800 Fax: (202) 512–2104 Mail: Stop IDCC, Washington, DC 20402–0001 VerDate Aug 31 2005 10:56 Mar 19, 2014 Jkt 000000 PO 00000 Frm 00001 Fmt 5011 Sfmt 5011 C:\DOCS\87014.TXT APRIL COMMITTEE ON OVERSIGHT AND GOVERNMENT REFORM DARRELL E. ISSA, California, Chairman JOHN L. MICA, Florida ELIJAH E. CUMMINGS, Maryland, Ranking MICHAEL R. TURNER, Ohio Minority Member JOHN J. DUNCAN, JR., Tennessee CAROLYN B. MALONEY, New York PATRICK T. MCHENRY, North Carolina ELEANOR HOLMES NORTON, District of JIM JORDAN, Ohio Columbia JASON CHAFFETZ, Utah JOHN F. TIERNEY, Massachusetts TIM WALBERG, Michigan WM. LACY CLAY, Missouri JAMES LANKFORD, Oklahoma STEPHEN F. LYNCH, Massachusetts JUSTIN AMASH, Michigan JIM COOPER, Tennessee PAUL A. GOSAR, Arizona GERALD E. CONNOLLY, Virginia PATRICK MEEHAN, Pennsylvania JACKIE SPEIER, California SCOTT DESJARLAIS, Tennessee MATTHEW A. CARTWRIGHT, Pennsylvania TREY GOWDY, South Carolina TAMMY DUCKWORTH, Illinois BLAKE FARENTHOLD, Texas ROBIN L. KELLY, Illinois DOC HASTINGS, Washington DANNY K. DAVIS, Illinois CYNTHIA M. LUMMIS, Wyoming PETER WELCH, Vermont ROB WOODALL, Georgia TONY CARDENAS, California THOMAS MASSIE, Kentucky STEVEN A. -

BE a UTRGV LEGISLATIVE INTERN at the TEXAS CAPITOL! Live

BE A UTRGV LEGISLATIVE INTERN AT THE TEXAS CAPITOL! Live & Work in Austin While Earning College Credit Earn SIX Credit Hours in Political Science or Academic Credit in certain Masters Programs. Gain ‘Real-World’ Experience – Receive an $8,000 Stipend!* Where will I Intern? Internships are available in the offices of State Legislators at the Texas Capitol in Austin, Texas. When? The 86th Texas Legislative Session begins Jan. 8, 2019. You will report to your Capitol office a few days before. An orientation at UTRGV will be provided prior to your report date. What Will I Do? You will put your academic knowledge into practice as you assist legislators & staff in administration, engage in research and writing assignments, steward legislation, participate in event organization and perform tasks at the Texas Capitol. How will I Benefit? You will acquire a greater understanding of the legislative process, receive training in a learning environment and increase professional skills while earning six upper-level credit hours in political science or Master’s program credit. Students selected for the Austin Legislative Internships will receive $8,000* each to help cover their expenses of living in Austin. How Do I Qualify? You must be currently enrolled at UTRGV, have completed 60 undergraduate hours, including 12 semester credit hours in political science, a 3.0 GPA in political science courses and a 2.5 cumulative GPA. Master’s students must have a minimum 3.0 GPA and enroll in the appropriate course(s) in the academic departments. Who Do I Contact? Contact Dr. Ruth Ann Ragland at [email protected] or Richard Sanchez at [email protected] Apply at: www.utrgv.edu/careercenter/_files/documents/vlip-internship-application.pdf Deadline to Apply: NOVEMBER 15, 2018 Legislative Internships at the Texas Capitol Spring 2019 State Legislative Offices Rio Grande Valley Texas House & Senate Members** TEXAS SENATORS TEXAS REPRESENTATIVES Senator Juan “Chuy” Hinojosa Representative Terry Canales Senator Eddie Lucio Jr. -

Future of Austin Avenue Bridges Comes Into Focus Transportation Experts Address Issue New Report Recommends ‘Destination’ Fix

Barber Kay McConaughey hangs up shares her story his She relished raising three sons, including clippers award-winning actor Page 1B Page 3B Vol. 40 No. 32 GEORGETOWN, TEXAS n JANUARY 11, 2015 One Dollar Future of Austin Avenue bridges comes into focus Transportation experts address issue New report recommends ‘destination’ fix By MATT LOESCHMAN session that precedes their 3 p.m. workshop. An independent Austin Av- the importance of increased assets,” said the report, which The workshop session will include rec- enue bridges assessment pre- pedestrian connectivity with was prepared by Cheney Bostic Two nationally prominent transporta- ommendations from the city’s Road Bond pared by Winter & Company, a the city’s award-winning San of Winter & Company. tion experts will talk about the future of the Committee, which has listed the Austin Av- Colorado urban design studio Gabriel River trails system, The plan would also: 75-year-old Austin Avenue bridges over the enue bridges as its top priority. with an international reputa- making the bridges safer for n Minimize construction north and south forks of the San Gabriel tion, offers clear recommenda- pedestrians and cyclists, using time to four to six months while River in a special meeting Tuesday. Public Q&A tions — and a very different ap- the bridge repair to turn the maintaining traffic on two The public is invited to the meeting, set Council members in attendance will not proach from a previous bridges historic downtown into a desti- lanes of the bridges, lessening for 2 p.m. in council chambers, 101 East Sev- ask questions following the presentation, study — to the city council re- nation attraction and maintain- the negative impact on down- enth Street. -

The Shafi Controversy: Context and Preliminary Takeaways

THE SHAFI CONTROVERSY: CONTEXT AND PRELIMINARY TAKEAWAYS David R. Brockman, Ph.D. Nonresident Scholar, Religion and Public Policy April 2019 © 2019 by Rice University’s Baker Institute for Public Policy This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. Wherever feasible, papers are reviewed by outside experts before they are released. However, the research and views expressed in this paper are those of the individual researcher(s) and do not necessarily represent the views of the Baker Institute. David R. Brockman, Ph.D. “The Shafi Controversy: Context and Preliminary Takeaways” https://doi.org/10.25613/jryw-jq08 The Shafi Controversy Introduction In late 2018 and early 2019, a faction within the Tarrant County Republican Party (TCGOP) attempted to force the removal of the organization’s newly appointed vice chair, Dr. Shahid Shafi, because he is Muslim. The controversy drew national and international media attention,1 and pitted anti-Muslim activists against party luminaries such as U.S. Senator Ted Cruz and Texas Governor Greg Abbott, who voiced support for Shafi. Though anti-Muslim rhetoric has become common in the GOP, party leaders now condemned religious bigotry and discrimination as contrary to Republican principles. While the effort to oust Shafi ultimately failed, the episode offers a case study in the ways religion and politics intersect in a Texas that is steadily growing more ethnically and religiously diverse. Shafi’s appointment to party leadership is itself an indicator of the growth of the Muslim community, both demographically and in political influence, in the Dallas-Fort Worth (DFW) area as well as statewide and nationally.