Ministry of Labour and Employment [Exempted

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Standing Committee on Labour (2017-18) (Sixteenth

30 STANDING COMMITTEE ON LABOUR (2017-18) (SIXTEENTH LOK SABHA) MINISTRY OF TEXTILES [LAND ASSETS MANAGEMENT IN NATIONAL TEXTILE CORPORATION (NTC)] THIRTIETH REPORT LOK SABHA SECRETARIAT NEW DELHI December, 2017/Agrahayana, 1939 (Saka) i THIRTIETH REPORT STANDING COMMITTEE ON LABOUR (2017-18) (SIXTEENTH LOK SABHA) MINISTRY OF TEXTILES [LAND ASSETS MANAGEMENT IN NATIONAL TEXTILE CORPORATION (NTC)] Presented to Lok Sabha on 28th December, 2017 Laid in Rajya Sabha on 28th December, 2017 LOK SABHA SECRETARIAT NEW DELHI December, 2017/Agrahayana, 1939 (Saka) ii CONTENTS PAGE No. COMPOSITION OF THE COMMITTEE (iv) INTRODUCTION (v) REPORT GIST OF OBSERVATIONS/RECOMMENDATIONS 1 CHAPTER - I I. INTRODUCTORY 3 CHAPTER - II I. LAND POLICY 11 II. FREEHOLD LAND 15 III. LEASEHOLD LAND 19 IV. LAND UNDER DISPUTE/ENCROACHMENT 25 V. PENDING COURT CASES 35 VI. MADHUSUDAN MILLS 38 VII. UDAIPUR UNIT 44 VIII. SHOWROOMS OF NTC 47 ANNEXURES Annexure I- State-wise details of land 54 Annexure II- Mill-wise rates, on which the leasehold land was sold 58 Annexure III- Leasehold land lying idle 59 Annexure IV- Details of expenditure of maintenance/security etc. of 62 Mills/Land in all regions by NTC Annexure V- Disputed land - Mill-wise 63 Annexure VI- Status of disputes 67 Annexure VII- Details of land under encroachment 97 Annexure VIII- Details of cases and the orders passed by various courts 103 viz.-a-viz. appeal filed APPENDICES Appendix I- Minutes of the 2nd Sitting of the Committee (2016-17) 109 held on 3rd October, 2016. Appendix II- Minutes of the 19th Sitting of the Committee (2016-17) 112 held on 31st May, 2017. -

Standing Committee on Labour

33 STANDING COMMITTEE ON LABOUR (2017-18) (SIXTEENTH LOK SABHA) MINISTRY OF SKILL DEVELOPMENT & ENTREPRENEURSHIP [INDUSTRIAL TRAINING INSTITUTES (ITIs) AND SKILL DEVELOPMENT INITIATIVE SCHEME] THIRTY-THIRD REPORT LOK SABHA SECRETARIAT NEW DELHI January, 2018/Pausha, 1939 (Saka) i THIRTY-THIRD REPORT STANDING COMMITTEE ON LABOUR (2017-18) (SIXTEENTH LOK SABHA) MINISTRY OF SKILL DEVELOPMENT & ENTREPRENEURSHIP [INDUSTRIAL TRAINING INSTITUTES (ITIs) AND SKILL DEVELOPMENT INITIATIVE SCHEME] Presented to Lok Sabha on 4th January, 2018 Laid in Rajya Sabha on 4th January, 2018 LOK SABHA SECRETARIAT NEW DELHI January, 2018/Pausha, 1939 (Saka) ii CONTENTS PAGE No. COMPOSITION OF THE COMMITTEE (iv) INTRODUCTION (v) REPORT GIST OF OBSERVATIONS/RECOMMENDATIONS 1 INTRODUCTORY 5 STRUCTURE OF CRAFTSMEN TRAINING SCHEME 6 DEFICIENCIES FOUND IN THE FUNCTIONING OF QCI 14 FUTURE ACTION PROPOSED BY THE MINISTRY 32 GRADING/STAR RATING OF ITIS 33 IMPACT OF TRAINING PROVIDED BY ITIS ON EMPLOYABILITY 47 ADMISSION IN ITIs 48 APPRENTICESHIP TRAINING SCHEME AND NATIONAL APPRENTICESHIP 53 PROMOTION SCHEME CURRENT STATUS 55 CRAFTS INSTRUCTOR TRAINING SCHEME 55 UPGRADATION OF ITI'S THROUGH PUBLIC PRIVATE PARTNERSHIP 63 UPGRADATION OF EXISTING GOVERNMENT ITIS INTO MODEL ITIS 66 APPENDICES Appendix I- Minutes of the 20th Sitting of the Committee (2016-17) 69 held on 9th June, 2017. Appendix II- Minutes of the 22nd Sitting of the Committee (2016-17) 72 held on 30th June, 2017. Appendix III- Minutes of the 5th Sitting of the Committee (2017-18) 75 held on 21st November, 2017. Appendix IV- Minutes of the 7th Sitting of the Committee (2017-18) 78 held on 3rd January, 2018. iii COMPOSITION OF THE STANDING COMMITTEE ON LABOUR (2017-18) DR. -

Parliamentary Bulletin

RAJYA SABHA Parliamentary Bulletin PART-II Nos.:54546-54548] MONDAY, AUGUST 31, 2015 No.54546 M.A. Section Local address of Shri Amar Shankar Sable, MP Local address of Shri Amar Shankar Sable, M.P. would be as follows:- Flat no. 4, Meena Bagh, New Delhi - 110011. Members may kindly note for information. ____________ No.54547 Committee Section (Subordinate Legislation) Statutory Orders laid on the Table of the Rajya Sabha during the period August 10 - 13, 2015 (236th Session) The following Statutory Rules and Orders made under the delegated powers of legislation and published in the Gazette were laid on the Table of the Rajya Sabha during the period August 10 - 13, 2015. The Orders will be laid on the Table for a period of 30 days, which may be comprised in one session or in two or more successive sessions. Members can move a motion for modification/annulment before the expiry of the session, immediately, following the session in which the laying period of 30 days is completed. 3 Sl. Number and date Brief Subject Date on Provision of the Statute under No. of Rule/Order which laid which laid 1 2 3 4 5 MINISTRY OF CORPORATE AFFAIRS 1 G.S.R. 438 (E), The Companies (Registration Offices 11.08.2015 Section 469 (4) of the dated the 30th May, and Fees) Second Amendment Rules, Companies Act, 2013. 2015. 2015. 2 G.S.R. 440 (E), The Companies (Registration of -do- -do- dated the 30th May, Charges) Amendment Rules, 2015. 2015. 3 G.S.R. 441 (E), The Companies (Declaration and -do- -do- dated the 30th May, Payment of Dividend) Second 2015. -

Case Filing Status Marking

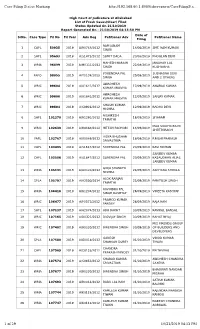

Case Filing Status Marking http://192.168.60.1:8080/ahcrepnew/CaseFilingSta... High Court of Judicature at Allahabad List of Fresh Cases(Clear) Filed Status Updated On 21/10/2019 Report Generated On - 21/10/2019 04:13:50 PM Date of SrNo. Case Type Fil No Fil Year Adv Reg Petitioner Adv Petitioner Name Filing RAM JANAM 1 CAPL 50935 2019 A/R0768/2012 18/06/2019 SMT. RAM KUMARI SINGH 2 SAPL 95693 2019 A/S1473/2012 SUMIT DAGA 20/08/2019 PHOOLAN DEVI MAHESH NARAIN JAWAHAR LAL 3 WRIA 96899 2019 A/M0111/2012 22/08/2019 SINGH KUSHWAHA YOGENDRA PAL SUBHADRA DEVI 4 FAFO 98055 2019 A/Y0108/2013 29/08/2019 SINGH AND 2 OTHERS AWADHESH 5 WRIC 99604 2019 A/A1641/2012 12/09/2019 ANURAG KUMAR KUMAR MALVIYA AWADHESH 6 WRIC 99606 2019 A/A1641/2012 12/09/2019 SANJAY KUMAR KUMAR MALVIYA SHASHI KUMAR 7 WRIC 99894 2019 A/S0926/2012 12/09/2019 RADHA DEVI MISHRA RISHIKESH 8 SAPL 101270 2019 A/R1292/2012 16/09/2019 SIYARAM TRIPATHI MAA SIDDHIDRATRI 9 WRIC 102639 2019 A/H0168/2012 HITESH PACHORI 18/09/2019 SHEETGRAGH VIDYA BHUSHAN 10 FAPL 102767 2019 A/V0089/2012 19/09/2019 P.RISHI PRAKASH SRIVASTAVA 11 CAPL 103495 2019 A/S1647/2012 SURENDRA PAL 20/09/2019 RAVI MOHAN SANJEEV KUMAR 12 CAPL 103506 2019 A/S1647/2012 SURENDRA PAL 20/09/2019 KASAUDHAN ALIAS SANJEEV KUMAR GIRJA SHANKER 13 WRIA 105131 2019 A/G0124/2012 24/09/2019 ARCHANA SHUKLA MISHRA ALOK RANJAN 14 SPLA 105797 2019 A/A2500/2014 25/09/2019 PARITOSH SINGH TRIPATHI RAVINDRA PAL 15 WRIA 106418 2019 A/R1206/2012 26/09/2019 VINEETA KASHYAP SINGH KASHYAP PRAMOD KUMAR 16 WRIC 106477 2019 A/P0371/2012 26/09/2019 -

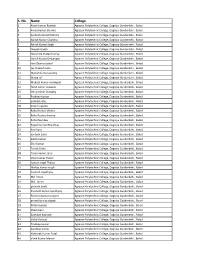

S. No. Name College

S. No. Name College 1 Akash kumar Ramtek Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 2 Aman kumar Sharma Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 3 Amitesh Anand Rathore Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 4 Ashish Kumar Chandra Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 5 Ashish Kumar Singh Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 6 Deepak Gupta Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 7 Devendra Pratap Kurrey Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 8 Harish Kumar Dewangan Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 9 Hari Shankar patel Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 10 Jay Prakash sahu Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 11 Manish kumar pandey Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 12 Mewa lal Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 13 Mukesh kumar manikpuri Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 14 Nand kumar sonwani Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 15 Om prakash Choubey Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 16 Pradeep kumar Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 17 prahlad sahu Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 18 pranshu gupta Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 19 Rahul kumar Mishra Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 20 Rahul kumar sharma Agrasen Polytechnic College, Dagniya Gunderdehi , Balod 21 Rahul -

Standing Committee on Labour

34 STANDING COMMITTEE ON LABOUR (2017-18) (SIXTEENTH LOK SABHA) MINISTRY OF LABOUR AND EMPLOYMENT DEMANDS FOR GRANTS (2018-19) THIRTY-FOURTH REPORT LOK SABHA SECRETARIAT NEW DELHI March, 2018/Phalguna, 1939 (Saka) i THIRTY-FOURTH REPORT STANDING COMMITTEE ON LABOUR (2017-18) (SIXTEENTH LOK SABHA) MINISTRY OF LABOUR AND EMPLOYMENT DEMANDS FOR GRANTS (2018-19) Presented to Lok Sabha on 13.03.2018 Laid in Rajya Sabha on 13.03.2018 LOK SABHA SECRETARIAT NEW DELHI March, 2017/Phalguna, 1938 (Saka) ii CONTENTS PAGE No. COMPOSITION OF THE COMMITTEE (iv) INTRODUCTION (v) REPORT I. INTRODUCTORY 1 II. NEW INITIATIVES 4 III. FINANCIAL AND PHYSICAL PERFORMANCE 5 IV. POOR PERFORMANCE OF SOME SCHEMES 9 V. BUDGET & CASH MANAGEMENT SCHEME (B&CM) 18 VI. REHABILITATION OF BONDED LABOUR 20 VII. INDUSTRIAL RELATIONS 26 VIII. PRADHAN MANTRI ROJGAR PROTSAHAN YOJANA (PMRPY) 32 IX. EMPLOYEES' PROVIDENT FUND ORGANISATION (EPFO) 39 X. EMPLOYEES' PENSION SCHEME, 1995 44 ANNEXURES ANNUEXURE I - Physical Targets and Achievements 48 ANNUEXURE II - Incumbency Position of Presiding Officers at CGIT-Labour 113 Courts as on 01.02.2018 APPENDICES Appendix I- Minutes of the Eleventh Sitting of the Committee held on 115 22nd February, 2018 Appendix II-Minutes of the Fourteenth Sitting of the Committee held 118 on 12th March, 2018 iii COMPOSITION OF THE STANDING COMMITTEE ON LABOUR (2016-17) DR. KIRIT SOMAIYA - CHAIRPERSON MEMBERS Lok Sabha 2. Shri Udayanraje Pratapsingh Bhonsle 3. Shri Rajesh Diwakar 4. Shri Ashok Kumar Dohrey 5. Shri Satish Chandra Dubey 6. Shri Devajibhai Fatepara 7. Shri Satish Kumar Gautam 8. Dr. Boora Narsaiah Goud 9. -

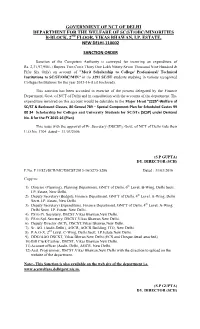

Government of Nct of Delhi Department for the Welfare of Sc/St/Obc/Minorities B-Block, 2Nd Floor, Vikas Bhawan, I.P

GOVERNMENT OF NCT OF DELHI DEPARTMENT FOR THE WELFARE OF SC/ST/OBC/MINORITIES B-BLOCK, 2ND FLOOR, VIKAS BHAWAN, I.P. ESTATE, NEW DELHI-110002 SANCTION ORDER Sanction of the Competent Authority is conveyed for incurring an expenditure of Rs. 2,31,97,956/- (Rupees Two Crore Thirty One Lakh Ninety Seven Thousand Nine Hundred & Fifty Six Only) on account of "Merit Scholarship to College/ Professional/ Technical Institutions to SC/ST/OBC/MIN” in r/o 3291 SC/ST students studying in various recognized Colleges/Institutions for the year 2015-16 (List Enclosed). This sanction has been accorded in exercise of the powers delegated by the Finance Department, Govt. of NCT of Delhi and in consultation with the accounts of the department. The expenditure involved on this account would be debitable to the Major Head “2225”-Welfare of SC/ST & Backward Classes, 80 Geneal 789 – Special Component Plan for Scheduled Castes 99 00 34 Scholarship for Colleges and University Students for SC/STs (SCSP) under Demand No. 8 for the FY 2015-16 (Plan) This issue with the approval of Pr. Secretary (DSCST), Govt. of NCT of Delhi vide their U.O.No. 1704 dated – 31/03/2006. (S.P GUPTA) DY. DIRECTOR (SCH) F.No. F11(82)/SCH/MC/DSCST2015-16/5275-5286 Dated : 31/03/2016 Copy to: 1) Director (Planning), Planning Department, GNCT of Delhi, 6th Level, B-Wing, Delhi Sectt. I.P. Estate, New Delhi. 2) Deputy Secretary (Budget), Finance Department, GNCT of Delhi, 4th Level, A-Wing, Delhi Sectt. I.P. Estate, New Delhi. -

Admission 2014-15 Form No's of Applicants to Download Admit Card

Ad mission 2014-15 Form No’s of Applicants To Download Admit Card Form No. First Name Last Name Father's City F14000006 MONIKA KAKRAN SHEMPAL KAKRAN JANSATH F14000007 CHETAN PRAKASH GUPTA RAM PRATAP GUPTA BHOPAL F14000008 KM SHAILI RAJVIR SINGH JANSATH F14000011 ABHISHEK DUBEY MAYA SHANKAR DUBEY SILVASSA F14000013 SUYASH BHATT PRAMOD BHATT BHOPAL F14000016 ANKLESH VISHWAKARMA ROSHAN LAL MULTAI F14000019 SHALINI AGRAWAL GOVIND AGRAWAL BHOPAL F14000020 VIVEK SINGH RANA AMAR SINGH RANA KEOLARI F14000025 GIRJESH THAKUR VISHWANATH SINGH MORAR F14000026 SUHRID TIWARI RAJMANI TIWARI RAGHURAJ NAGAR F14000035 TARUN PRATAP SINGH VIPUL KUMAR SINGH KADIPUR F14000043 RAKESH KUMAR BHANWAR LAL PINDWARA F14000044 PRADEEP CHANDRA YATISH KUMAR CHANDRA JAIJAIPUR F14000047 VIKAS KUMAR GUPTA LATE RADHA MOHAN GUPTA LUCKNOW F14000049 MOHIT SHARMA BASANT KUMAR SHARMA VIDISHA F14000050 PUNIT RAJPUT JAGASHWAR FARRUKHABAD F14000052 RAVI PRAKASH GUPTA RAJENDRA PRASAD GUPTA GIDDI F14000053 MOHD FARMAN MOHD ANSAAR FARRUKHABAD F14000054 AAKANKSHA YADAV ANIL KUMAR YADAV TADONG GANGTOK F14000055 Nagendra Singh Ravindra Singh Sambhal F14000061 SHUBHAM RATHORE JAGDISH PRASAD RATHORE DAMOH F14000062 SHUBHAM RATHORE JAGDISH PRASAD RATHORE DAMOH F14000065 VIPIN SINGH RAM SAGARE SINGH MAHRAJGANJ F14000066 MAHENDRA KUMAR RAM DHAN PATTI LATE SHRI BHOMRIK DAS F14000070 NIRLESH KHAMBRA KHAMBRA BHOPAL F14000071 ANUKRITI Pandey DR AJAY KUMAR PANDEY Varanasi F14000074 MANISH MISHRA SHATRUGHAN MISHRA ROHINI F14000076 AKASH SINGH DHARMENDRA SINGH BALRAMPUR F14000052 RAVI PRAKASH GUPTA -

Standing Committee on Labour (2017-18)

36 STANDING COMMITTEE ON LABOUR (2017-18) (SIXTEENTH LOK SABHA) MINISTRY OF SKILL DEVELOPMENT & ENTREPRENEURSHIP DEMANDS FOR GRANTS (2018-19) THIRTY SIXTH REPORT LOK SABHA SECRETARIAT NEW DELHI March, 2018/Phalguna, 1939 (Saka) i THIRTY SIXTH REPORT STANDING COMMITTEE ON LABOUR (2017-18) (SIXTEENTH LOK SABHA) MINISTRY OF SKILL DEVELOPMENT & ENTREPRENEURSHIP DEMANDS FOR GRANTS (2018-19) Presented to Lok Sabha on 13.03.2018 Laid in Rajya Sabha on 13.03.2018 LOK SABHA SECRETARIAT NEW DELHI March, 2018/Phalguna, 1939 (Saka) ii CONTENTS PAGE No. COMPOSITION OF THE COMMITTEE (iv) INTRODUCTION (v) REPORT I. INTRODUCTORY 1 II. PROPOSED AND APPROVED ALLOCATIONS FOR 2018-19 2 III. BUDGETARY ALLOCATION & UTILISATION DURING 2016-17 & 11 2017-18 IV. PHYSICAL TARGETS AND ACHIEVEMENTS 17 (i) Pradhan Mantri Kaushal Vikas Yojna (PMKVY) 18 (ii) Centrally Sponsored Centrally Managed (CSCM) 20 (iii) Centrally Sponsored State Managed (CSSM) 21 (iv) Mechanism for Continuous Monitoring 27 (v) Pradhan Mantri Kaushal Kendra (PMKK) 40 V. NATIONAL APPRENTICESHIP PROMOTION SCHEME 44 (NAPS) VI. JAN SHIKSHAN SANSTHAN SCHEME 47 APPENDICES Appendix I- Minutes of the Twelfth Sitting of the Committee held on 22nd February, 51 2018 Appendix II- Minutes of the Fourteen Sitting of the Committee held on 12th March, 54 2018 iii COMPOSITION OF THE STANDING COMMITTEE ON LABOUR (2017-18) DR. KIRIT SOMAIYA - CHAIRPERSON MEMBERS Lok Sabha 2. Shri Udayanraje Pratapsingh Bhonsle 3. Shri Rajesh Diwakar 4. Shri Ashok Kumar Dohrey 5. Shri Satish Chandra Dubey 6. Shri Devajibhai Fatepara 7. Shri Satish Kumar Gautam 8. Dr. Boora Narsaiah Goud 9. Shri Rama Chandra Hansdah 10. Shri C. -

Dk;Kzy; Ftyk ,Oa L= U;K;K/Kh'k] Mttsu ¼E-Iz-½

dk;kZy; ftyk ,oa l= U;k;k/kh'k] mTtSu ¼e-iz-½ vkdfLedrk fuf/k ls osru ikus okys Hk`R;@pkSdhnkj@okVjesu@ekyh ¼dysDVj jsV½ ds in gsrq izkIr vkosnuksa ds p;u lfefr }kjk ijh{k.k mijkUr vik=@=qfViw.kZ gksus ls vU; fiNM+k oxZ ds fujLr vkosndksa dh lwph dkj.k lfgrA Catego Sr. No. Application No. Name Father Name Interview Date fujLrh dk dkj.k ry ANIL MOHAN LAL vkosnu i= ds lkFk nLrkost 1 MPPDS16104493 OBC 10-Dec-16 PAPONDIYA PAPONDIYA layXu ughaA PRADEEP SURESH CHANDRA 'kS{kf.kd ;ksX;rk laca/kh 2 MPPDS16105941 OBC 10-Dec-16 PATIDAR PATIDAR nLrkost layXu ugha gSaA e-iz- dk ewy fuoklh vkosnd 3 MPPDS16110926 AKASH PATEL SIVRAM PATEL OBC 10-Dec-16 dk Loa; dk ugha gSaA MOHAMMAD ewy fuoklh l{ke vf/kdkjh 4 MPPDS16116285 MOHAMMAD AYYUB OBC 10-Dec-16 AMIN }kjk iznRr ugha gSa MOHAN LAL MANOHAR LAL vkosnu i= ds lkFk nLrkost 5 MPPDS16117243 OBC 10-Dec-16 PADIHAR PADIHAR layXu ughaA RUDRA KUMAR e-iz- dk ewy fuoklh layXu 6 MPPDS16117703 BASANT LAL VERMA OBC 10-Dec-16 VERMA ugha gSaA ewy fuoklh vkosnd dk Loa; 7 MPPDS16121444 MO JAID MO SHAFIQ OBC 10-Dec-16 dk layXu ugha gSaA ewy fuoklh l{ke vf/kdkjh 8 MPPDS16124502 KAMAL SINGH BHERU SINGH OBC 10-Dec-16 }kjk iznRr ugha gSa e-iz- dk ewy fuoklh vkosnd 9 MPPDS16130130 DEEPAK KUMAR KISHOR SINGH OBC 10-Dec-16 dk Loa; dk ugha gSaA e-iz- dk ewy fuoklh layXu 10 MPPDS16130152 ANAND PARMANAND OBC 10-Dec-16 ugha gSaA ewy fuoklh vkosnd dk Loa; 11 MPPDS16130986 NILESH SOLANKI RAJENDRA KUMAR OBC 10-Dec-16 dk layXu ugha gSaA BABULAL 12 MPPDS16131908 GOPAL GAWALA OBC 10-Dec-16 GAWALA 'kS{kf.kd ;ksX;rk viw.kZ gSaA RAHUL vkosnd -

Standing Committee on Labour (2017-18) (Sixteenth

35 STANDING COMMITTEE ON LABOUR (2017-18) (SIXTEENTH LOK SABHA) MINISTRY OF TEXTILES DEMANDS FOR GRANTS (2018-19) THIRTY FIFTH REPORT LOK SABHA SECRETARIAT NEW DELHI March, 2018/Phalguna, 1939 (Saka) i THIRTY FIFTH REPORT STANDING COMMITTEE ON LABOUR (2018-19) (SIXTEENTH LOK SABHA) MINISTRY OF TEXTILES DEMANDS FOR GRANTS (2018-19) Presented to Lok Sabha on 13.03.2018 Laid in Rajya Sabha on 13.03.2018 LOK SABHA SECRETARIAT NEW DELHI March, 2018/Phalguna, 1939 (Saka) ii CONTENTS PAGE (S) COMPOSITION OF THE COMMITTEE (iv) INTRODUCTION (v) REPORT I INTRODUCTORY 1 II XII PLAN OUTLAY AND UTILISATION 3 III ALLOCATION AND UTLISATION OF FUNDS DURING 2017-18 8 AND ANNUAL PLAN 2018-19 Supplementary Demands For Grants (2018-19) 15 Shortfall in Scheme 18 Annual Plan 2018-19 19 IV PHYSICAL TARGETS AND ACHIEVEMENTS 28 Handloom Weaver Comprehensive Welfare Scheme 30 V SOME MAJOR ONGOING AND NEW SCHEMES 33 VI REBATE ON STATE LEVIES (RoSL) 42 VII AMENDED TECHNOLOGICAL UPGRADATION FUND SCHEME 44 (ATUFS) VIII SERICULTURE 49 IX INTEGRATED SKILL DEVELOPMENT SCHEME 55 (ISDS) X IMPACT OF GST ON TEXTILE INDUSTRY 62 XI SCHEME FOR INTEGRATED TEXTILE PARKS 67 (SITP) XII WOOL DEVELOPMENT PROGRAMME 72 ANNEXURE 74 Annexure-I Scheme-wise financial/physical targets and achievements during 2017-18. 83 Annexure-II Textiles Parks approved in last 4 years. Annexure-III Details of Textile Parks in Jammu & Kashmir and 85 North-Eastern States. Annexure-IV Model Textile Parks under SITP 86 APPENDICES Appendix-I Minutes of the Tenth sitting of the Standing Committee on 88 Labour held on 16.02.2018. -

Sl No Registration Id Name Fathersname Marks Obtained Aggregate Percentage 1 159241 Animesh Singh Vivek Singh 299 300 99.667 2

Maths_UR SL_NO REGISTRATION_ID NAME FATHERSNAME MARKS_OBTAINED AGGREGATE PERCENTAGE 1 159241 ANIMESH SINGH VIVEK SINGH 299 300 99.667 2 63549 RAJ SINGH RAKESH SINGH 497 500 99.400 3 61248 SIDDHARTH SHARMA SUNIL KUMAR SHARMA 396 400 99.000 4 192595 YASH JHA SHAILESH KUMAR JHA 790 800 98.750 5 62013 CHIRAG PAL RADHE SHYAM 641 650 98.615 6 127960 SHUBHENDU GUPTA RAJ BAHOR GUPTA 394 400 98.500 7 66863 ASHUTOSH PANDEY SANTOSH KUMAR PANDEY 394 400 98.500 8 43485 UTKARSH PANDEY DHARMENDRA KUMAR PANDEY 590 600 98.333 9 52894 ANISH KUMAR MISHRA RAMESH MISHRA 295 300 98.333 10 193008 NARAYAN PRASAD PANDEY KRISHNA KUMAR PANDEY 393 400 98.250 11 50916 ABHISHEK VISHWAKARMA RAJARAM VISHWAKARMA 393 400 98.250 12 13035 ADARSH KUMAR ASHOK KUMAR YADAV 491 500 98.200 13 12355 PRABHAS CHANDRA RAI SANJAY KUMAR RAI 490 500 98.000 14 151829 AKSHAT TRIPATHI PRAMOD TRIPATHI 392 400 98.000 15 51747 AVINASH RAJ ARBIND KUMAR ROY 490 500 98.000 16 18544 SHUBHAM KUMAR GUPTA RAJKUMAR GUPTA 587 600 97.833 17 192322 AKASH DEEP VIJAY KUMAR SINGH 489 500 97.800 18 174269 SHREYANSH TRIPATHI AJAY KUMAR TRIPATHI 586 600 97.667 19 4304 MONIR AKHTAR SAFI AKHTAR 586 600 97.667 20 28380 RISHIKESH JHABINDRA BAHADUR NEPALI 488 500 97.600 21 164528 ARYAN CHATURVEDI SANJEEV KUMAR CHATURVEDI 585 600 97.500 22 182404 SIDDHARTH GAUTAM DHIRAJ YADAV 585 600 97.500 23 51999 RINEET PANDEY LAXMI KANT PANDEY 585 600 97.500 24 8386 SHREYAS GUPTA RAVINDRA KUMAR GUPTA 585 600 97.500 25 103128 YOGESH KUMAR VINOD KUMAR 487 500 97.400 26 78274 SIDDHARTH GUPTA SHIVAJEE PRASAD GUPTA 584 600 97.333