Odoo 2020: Vision & Strategy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Paper Title (Use Style: Paper Title)

A selection model of ERP system in mobile ERP design science research Case study: mobile ERP usability Khalil Omar Jorge Marx Gómez Department of Computing Science Department of Computing Science University of Oldenburg University of Oldenburg Oldenburg, Germany Oldenburg, Germany [email protected] [email protected] Abstract— Nowadays, mobile apps penetrate in every aspect Two complementary but distinct research paradigms of our daily life, due to the proliferation of mobile devices, the characterize much of the research in IS discipline namely: constant advances in mobile computing, and the enormous leaps behavioural science and design science [9]. The behavioural of mobile HCI. Thus, these factors have increased the demands to science paradigm has its roots in natural science research adopt the mobile ERP as a working model in enterprises. methods; it seeks to develop and verify theories that explain or Regardless of these demands, mobile ERP has several challenges predict human or organizational behaviour [9]. Whereas design and issues that need to be addressed through a problem the science paradigm is considered a problem-solving paradigm, design science research paradigm, since this paradigm is and it has its roots in engineering and the sciences of the considered a problem-solving paradigm and it has its roots in artificial [9]. The latter is accepted as a valid and valuable engineering and the sciences of the artificial. Accordingly, this research methodology by the engineering research culture, due paper aims to propose a model for selecting an appropriate ERP system within the mobile ERP’s design science research domain. -

Measuring Non Monetary Innovation in Software: a Case Study in Floss Firms from Argentina

International Journal of Innovation ISSN: 2318-9975 [email protected] Universidade Nove de Julho Brasil MEASURING NON MONETARY INNOVATION IN SOFTWARE: A CASE STUDY IN FLOSS FIRMS FROM ARGENTINA Motta, Jorge; Morero, Hernán Alejandro; Borrastero, Carina MEASURING NON MONETARY INNOVATION IN SOFTWARE: A CASE STUDY IN FLOSS FIRMS FROM ARGENTINA International Journal of Innovation, vol. 7, no. 1, 2019 Universidade Nove de Julho, Brasil Available in: https://www.redalyc.org/articulo.oa?id=499165584008 DOI: https://doi.org/10.5585/iji.v7i1.319 PDF generated from XML JATS4R by Redalyc Project academic non-profit, developed under the open access initiative MEASURING NON MONETARY INNOVATION IN SOFTWARE: A CASE STUDY IN FLOSS FIRMS FROM ARGENTINA ENSURANDO A INOVAÇÃO NÃO MONETÁRIA EM SOFTWARE: UM ESTUDO DE CASO EM EMPRESAS DE CÓDIGO ABERTO (FLOSS) DA ARGENTINA Jorge Moa [email protected] Universidad Nacional de Córdoba, Argentina hps://orcid.org/0000-0002-1430-7009 Hernán Alejandro Morero [email protected] Universidad Nacional de Córdoba-UNC, Argentina hps://orcid.org/0000-0002-6076-1915 Carina Borrastero [email protected] Universidad Nacional de Córdoba-UNC, Argentina International Journal of Innovation, vol. hps://orcid.org/0000-0002-8754-1381 7, no. 1, 2019 Universidade Nove de Julho, Brasil DOI: https://doi.org/10.5585/ iji.v7i1.319 Abstract: is paper presents a critical review of the design of innovation surveys that follow the Oslo Manual standards, based on a series of case studies in Free/Libre Redalyc: https://www.redalyc.org/ articulo.oa?id=499165584008 Open Source Soware (FLOSS) companies. e main objective of the article is to propose criteria for measuring innovation in soware that consider the specificities of the non-monetized innovation generated in the FLOSS community, helping to overcome relevant limitations of the current sectorial surveys based on the Oslo Manual. -

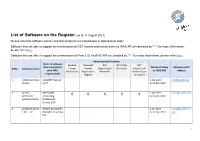

List of Software on the Register (As at 31 August 2021) √ √ √

List of Software on the Register (as at 31 August 2021) Please note that software owners and their products are listed below in alphabetical order. Software that are able to support the transmission of GST returns and transactions via IRAS API are denoted by "*". For more information, please refer here. Software that are able to support the transmission of Form C-S via IRAS API are denoted by “^”. For more information, please refer here. Recommended Features Name of software Reverse Overseas GST GST Filing GST that is compliant Period of Listing Business email S/No. Software owner Charge Vendor Registration Reminder Automated with IRAS' Mechanism Registration Reminder Blocked Input on IRAS ASR address requirements Regime Tax Claims 1. A2000 Solutions A2000ERP Version 1 Jan 2021 [email protected] Pte Ltd 12.X* to 31 Dec 2021 2. AccPro AAP R/4(R) - 1 Jan 2021 [email protected] Computer Accounting √ √ √ √ √ to 31 Dec 2021 Systems Pte Ltd Professional Version 10.0 3. ACMEFOCUS.NE WHIZIT ACCOUNTS 1 Jan 2021 [email protected] T PTE LTD ORGANIZER version to 31 Dec 2021 om PA1 1 Recommended Features Name of software Reverse Overseas GST GST Filing GST that is compliant Period of Listing Business email S/No. Software owner Charge Vendor Registration Reminder Automated with IRAS' on IRAS ASR address Mechanism Registration Reminder Blocked Input requirements Regime Tax Claims 4. AM8ZE Pte Ltd AM8ZE ERP Version 24 May 2021 [email protected] 10-13 to 31 Dec 2021 5. Asian Business (a) ABSS Premier 1 Jan 2021 [email protected] Software for Windows √ √ to 31 Dec 2021 m Solutions Pte Version 23.x Ltd (b) Financio Version 2.x 6. -

Advances in Natural and Applied Sciences 2018 April; 12(4): Pages 16-21 DOI: 10.22587/Anas.2018.12.4.4 Research Article AENSI Publications

Advances In Natural And Applied Sciences 2018 April; 12(4): pages 16-21 DOI: 10.22587/anas.2018.12.4.4 Research Article AENSI Publications Integration Between ERP Software and Business Intelligence in Odoo ERP: Case Study A Distribution Company Yulia Kendengis and Leo Willyanto Santoso Correspondence Author: Yulia Kendengis, Informatics Department, Petra Christian University, Indonesia Received date: 12 January 2018, Accepted date: 10 March 2018, Online date: 2 April 2018 Copyright: © 2018 Yulia Kendengis and Leo Willyanto Santoso. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited. Abstract Odoo is an open-source ERP software. Odoo has advantage in price because it’s free. And from the functional side, Odoo has been equipped with more than 4500 modules, one of them is business intelligence (BI). BI is a solution and technique that helps company to understand about the business situation to make effective business decisions and meet their objectives. A study about the integration between Enterprise Resource Planning and BI in Odoo ERP will be explained in this paper. In the case study, we used sales data from a distribution company. Key words: Business Intelligence, ERP, Odoo INTRODUCTION BI transforms raw data into meaningful metrics reflective upon historical, current and predictive business operations and performance. In the past, the activities of BI were performed through gathering data from multiple sources manually, manipulating data in spreadsheets, with a static report output. The data should be gathered from some functional areas. -

Python 2018, Fulda, Germany Nationaler Akademietag in Fulda 2018

Python 2018, Fulda, Germany Nationaler Akademietag in Fulda 2018 Maciek Wichary, Sławek Wernikowski, OpenEDG Python Institute April 2018 Yes You can find me in this picture! My very first CCNA group back in 2002 All of my students have great jobs now. © 20172016 Cisco and/or its affiliates. All rights reserved. Cisco Confidential 2 Agenda Overview of the How to make your Programming Essentials teaching job easier. 02 In Python course 04 Why Python? Use of Python Overview EDUBE A very important tool to What is Python actually make labs attractive and used for? easy. 01 03 We will do the lab now! © 2017 Cisco and/or its affiliates. All rights reserved. Cisco Confidential 3 Educationjobs.thelocal.comas the process Start Lectures, labs, quizes, chapter assesments What is Python actually used for? They were all written, to Battlefield 2, Battlefield 2142 and Battlefield Heroes a greater or lesser All the games use Python for logic and server controls extent, in Python. Other examples • Internet Applications (BitTorrent, Jogger Publishing Assistant, TheCircle, TwistedMatrix) • 3D CAD/CAM (FreeCAD, Fandango, Blender, Vintech RCAM) • Enterprise Applications (Odoo, Tryton, Picalo, LinOTP 2, RESTx) • Image Applications (Gnofract 4D, Gogh, imgSeek, MayaVi, VPython) • Mobile Applications (Aarlogic C05/3, AppBackup, Pyroute) • Office Applications (calibre, faces, Notalon, pyspread) • Personal Information Managers (BitPim, Narval, Prioritise, Task Coach, WikidPad) Generally, Python is a great choice for: • Web and Internet development (e.g., Django -

Erp Software Vendor Directory

ERP FOCUS ERP SOFTWARE VENDOR DIRECTORY C CONVERTED MEDIA ERP FOCUS M ERP Software Features Billing CRM Customer Service Financials & Accounting Planning & Scheduling 3S ERP Project Management Supply Chain Management 3S ERP is specifically designed for small to medium-sized manufacturing companies. The ERP is a fully-integrated Document Management system with a wide range of management modules that cater for production, manufacturing, and administration. The 3S ERP production module is particularly well-equipped for manufacturers, offering features for quality management, hazardous materials handling, tool management and product planning and configuration. It also VIEW SOFTWARE REVIEWS, interfaces with CAD. As 3S ERP is modular, users can build up from basic financial management with production, SCREENSHOTS & MORE distribution, CRM and much more. 3S ERP is easily customized and does not need any additional programming VIEW COMPLETE PROFILE knowledge. The security of 3S ERP data is managed at three levels – the operating system, the network and at the level to the database and applications. Access can be limited to the user level, meaning you can control access to restricted data across user groups. 3S ERP offers searchable one-time data entry, with advanced analytics features alongside this. It also helps support internal and external financial audits. 3S ERP is installed on-premise, with iOS and web apps available for increased mobility. System installation takes around seven days, and 3S offer user training during implementation. Users can access software updates and upgrades free of charge. ERP Software Features Billing Business Intelligence/Analytics Costing ABAS ERP CRM Financials & Accounting abas ERP is a software system for manufacturers, retailers, distributors and service providers. -

Odoo-Book-By-Cybrosys-Technologies

About The Publisher Cybrosys is a proven and well-established ISO Certified software development company which provides quality services all over the world. We have been providing reliable software services across different sectors of the software industry since 2008. Cybrosys has established its presence around the world within a short span of time. Now we serve our widespread customers around the globe via our offices located in London, Dubai, Bangalore, Kochi and Calicut. Our partnership with technology leaders like Microsoft, Sun, IBM, Symantec, and Odoo assist us to deliver high quality software solutions to our diverse customer base. ERP solutions being our core area of service, we perform Odoo ERP customization, implementation, and allied services. Along with that, we are also into Source code sale, Custom software development, and Employee outsourcing. Earlier with our own proven ERP suite, we hit the market, however, later our focus turned towards more affordable open source solutions. Cybrosys has been a reliable and trusted service provider of Odoo at the beginning itself and our expertise have made Odoo even more user-friendly. Our uncompromised and user oriented services in the field of Odoo implementation and customization keep us distinguished among market players “Never compromise on your needs, when we can assist you” CEO’s Message “Hard work always pays dividend, sooner or later” It’s been a long journey since we established Cybrosys. We have seen tides of growth and decline during the voyage. But we endured everything, and here we are, as one of the fast growing player, constantly striving to be better. -

Data Quadrant Report

April 2020 DATA QUADRANT REPORT Enterprise Resource Planning 1107 22 Reviews Vendors Evaluated Enterprise Resource Planning Data Quadrant Report Table of How to Use the Report Info-Tech’s Data Quadrant Reports provide a comprehensive evaluation of popular products in the Enterprise Resource Planning market. This buyer’s guide is designed to help prospective Contents purchasers make better decisions by leveraging the experiences of real users. The data in this report is collected from real end users, meticulously verified for veracity, Data Quadrant.................................................................................................................. 6 exhaustively analyzed, and visualized in easy to understand charts and graphs. Each product is compared and contrasted with all other vendors in their category to create a holistic, unbiased view Category Overview .......................................................................................................7 of the product landscape. Use this report to determine which product is right for your organization. For highly detailed reports Vendor Capability Summary ................................................................................ 9 on individual products, see Info-Tech’s Product Scorecard. Vendor Capabilities .....................................................................................................13 Product Feature Summary .................................................................................25 Product Features ..........................................................................................................31 -

Comparison of Development Possibilities of Information System: Case Study

Masaryk University Faculty of Informatics Comparison of development possibilities of information system: case study Master’s Thesis Bc. Jan Hrubeš Brno, Fall 2016 Declaration Hereby I declare that this paper is my original authorial work, which I have worked out on my own. All sources, references, and literature used or excerpted during elaboration of this work are properly cited and listed in complete reference to the due source. Bc. Jan Hrubeš Advisor: Ing. Leonard Walletzký, Ph.D. i Acknowledgement First of all, I would like to thank my tutor Professor Ing. Leonard Walletzký, Ph.D. for his support and guidance in curating the topic and content of this study. Also, I would like to thank my family, girlfriend and friends for moral support while writing this thesis. In addition, I am obliged with great appreciation and gratitude to all co-workers from studied company for valuable information. Finally, I must express my immense thanks to all people who share objective resources online and contributed to make this thesis success- ful. iii Abstract The purpose of this thesis is to present and describe information system roles and issues in a specific medium sized e-commerce com- pany as well as identifying the key motivation drivers to look for a replacement or alternative system. Such alternative is proposed taking advantage of open-source ERP systems and evaluated from econom- ical perspective to provide a decision material for studied company. Research is concluded with evaluation of its positive and negative out- comes. Although the implementation resulted to be more expensive than a maintenance of legacy information system, relevant benefits were discovered as well. -

Analisis Perbandingan Free/ Open Source Erp (Fos Erp) Dari Aspek Arsitektur, Fungsio- Nalitas, Dan Komunitas

TUGAS AKHIR – KS141501 ANALISIS PERBANDINGAN FREE/ OPEN SOURCE ERP (FOS ERP) DARI ASPEK ARSITEKTUR, FUNGSIO- NALITAS, DAN KOMUNITAS ANALYSIS OF COMPARISON ON FREE/ OPEN SOURCE ERP (FOS ERP) FROM ASPECT OF ARCHITECTURE, FUNCTIONALITY, AND COMMUNITY TESAR AKRAM PRATAMA NRP 5213 100 097 Dosen Pembimbing Mahendrawathi ER, S.T., M.Sc., Ph.D JURUSAN SISTEM INFORMASI Fakultas Teknologi Informasi Institut Teknologi Sepuluh Nopember Surabaya 2016 i iii TUGAS AKHIR – KS141501 ANALISIS PERBANDINGAN FREE/ OPEN SOURCE ERP (FOS ERP) DARI ASPEK ARSITEKTUR, FUNGSIO- NALITAS, DAN KOMUNITAS TESAR AKRAM PRATAMA NRP 5213 100 097 Dosen Pembimbing Mahendrawathi ER, S.T., M.Sc., Ph.D JURUSAN SISTEM INFORMASI Fakultas Teknologi Informasi Institut Teknologi Sepuluh Nopember Surabaya 2016 iii v FINAL PROJECT – KS141501 ANALYSIS OF COMPARISON ON FREE/ OPEN SOURCE ERP (FOS ERP) FROM ASPECT OF ARCHITECTURE, FUNCTIONALITY, AND COMMUNITY TESAR AKRAM PRATAMA NRP 5213 100 097 Supervisor Mahendrawathi ER, S.T., M.Sc., Ph.D INFORMATION SYSTEMS DEPARTMENT Information Technology Faculty Sepuluh Nopember Institute of Technology Surabaya 2016 v vii LEMBAR PENGESAHAN vii ix LEMBAR PERSETUJUAN ix ANALISIS PERBANDINGAN FREE/ OPEN SOURCE ERP (FOS ERP) DARI ASPEK ARSITEKTUR, FUNGSIONALITAS, DAN KOMUNITAS Nama Mahasiswa : Tesar Akram Pratama NRP : 5213 100 097 Jurusan : Sistem Informasi FTIF-ITS Pembimbing 1 : Mahendrawathi Er., S.T, M.Sc, Ph.D ABSTRAK ERP sebagai bagian dari enterprise system yang mengintegrasikan antar data mempunyai peran penting dalam pertukaran informasi antar departemen dalam organisasi. ERP yang berperan menyediakan sistem informasi terintegrasi dalam organisasi ini, kini tidak hanya dibutuhkan oleh perusahaan-perusahaan besar, tetapi juga perusahaan berskala menengah dan kecil. Namun mahalnya biaya implementasi ERP menjadi masalah utama bagi kebanyakan perusahaan, utamanya mereka yang beroperasi dengan ekonomi terbatas. -

A Study on Open ERP for Start-Up Smes

Volume : 4 | Issue : 6 | June2015 ISSN - 2250-1991 Research Paper Management A Study on Open ERP for Start-Up SMEs Assistant Professor, Nehru School of Management, Nehru College Mr.DINESH.E of Engineering and Research Centre, Pampady, Thiruvilwamala, Thrissur, Kerala. Professor and Head, Department of Management Studies, Velalar Dr.T.VETRIVEL College of Engineering and Technology, Thindal, Erode, Tamil- nadu. Enterprise Resource Planning (ERP) is a software package, where it integrates the functional departments of an organization. In this article, an ERP package called Odoo (formally Open ERP) is a web based application. It supports the business processes of an organization. Odoo meets all the requirements of business processes irrespective of their industry. Start-up companies and small and medium sized companies may use this ERP package for their systematic way. This article focuses about ERP ABSTRACT packages, Technical benefits of Odoo and Functional Benefits of Odoo for the business scenario. KEYWORDS Open ERP, Open Source Software, ERP Systems, SME, Odoo Introduction 4. ERP5 Enterprise Resource Planning (ERP) is a software package, 5. webERP where it integrates the functional departments of an organi- 6. Dolibarr ERP zation. Functional departments of an organization like Human 7. Sugar CRM Resource, Finance, Materials, Sales and Distribution, Logistics, Manufacturing, Operations, etc. There are two types of ERP The above Open Source ERPs are free licensed web based Systems for enterprises. One is to install in the server or a en- softwares available in the internet. They also used Open terprise system and implement. This type is called Stand Alone Source Languages like Javascript, Php, Frappe, etc to develop ERP System. -

Migració D'un Sistema ERP Propietari a Un ERP Open Source

Màster Internacional en Programari Lliure – TFM PAC1–Estudi de viabilitat i anàlisi Data màxima de lliurament: 19/03/2018 Nom i cognoms: EDUARDO HERNANDEZ ASENSIO PAC1 –Estudi de viabilitat i anàlisi Data màxima de lliurament: 19/03/2018 Nom i cognoms: EDUARDO HERNANDEZ ASENSIO MIGRACIO D'UN SISTEMA ERP PROPIETARI A UN ERP Títol del treball: OPEN SOURCE Nom de l'autor: Eduardo Hernández Asensio Nom del consultor/a: Amadeu Albós Raya Nom del PARA: Maria Isabel Guitard Domingo Titulació o programa: Màster en Programari Lliure Àrea del Treball Final Direcció de Sistemes d'Informació de Màster: Idioma del treball: Català Paraules clau: ERP, Propietari, Open Source, Odoo Data de lliurament: 11/6/2018 Resum del Treball: En aquest treball de final de màster es fa un estudi de migració d’una eina de gestió empresarial ERP propietària que s’ha quedat obsoleta, que part d’ella es va desenvolupar amb llenguatges obsolets i que té unes mancances d’accessibilitat remarcables. A partir de la descripció dels components, funcionalitats i procediments associats es fa un anàlisi del mercat de les eines ERP Open Source per triar la que millor s’adapti als processos de producció i negoci de l’empresa. Finalment s’elabora pas per pas un pla de migració valorat amb tots els elements i afectacions que suposa per l’organització Màster Internacional en Programari Lliure – TFM Màster Internacional en Programari Lliure – TFM Índex ............................................................................................. 1 Nom i cognoms: EDUARDO HERNANDEZ ASENSIO