Stewardship Activity Report: Q2 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Representative Financial Services M&A Transactions

Representative Financial Services M&A Transactions Asset Management • Hellman & Friedman. Representing Hellman & Friedman in connection with its acquisition of Allfunds Bank S.A., a Spanish bank that offers intermediation and investment services to commercial banks, private banking institutions, fund managers, insurance companies and fund supermarkets. • Ramius, LLC. Represented Ramius, LLC, in its sale of Ramius Alternative Solutions to AllianceBernstein. • Landmark Partners. Represented Landmark Partners in the $465 million sale to OM Asset Management, a privately owned asset management holding company. • State Street Bank and Trust Company. Represented State Street Bank and Trust Company in the acquisition of GE Asset Management (GEAM), a privately owned investment manager. • Mitsubishi UFJ Investor Services. Represented Mitsubishi UFJ Investors Services in its acquisition of UBS Global Asset Management’s Alternative Fund Services Business, a company that offers professional services for hedge funds, funds of hedge funds, private equity, and real estate structures. • Mitsubishi UFJ Fund Services Holdings Ltd. Represented Mitsubishi UFJ Fund Services Holdings Ltd., an asset administration company, in its acquisition of Meridian Fund Services Group. • Bain Capital. Represented the global credit affiliate of Bain Capital in its $1.6 billion acquisition of four portfolios of collateralized loan obligations (CLOs) from Regiment Capital. • Wellington Management Company. Represented Wellington Management Company, a privately owned investment manager, in its $85 million PIPE investment in ChinaCache International Holdings Ltd., a provider of content and application delivery services in the People’s Republic of China. • 3i Group. Represented 3i Group in its strategic transaction with Fraser Sullivan, a privately owned investment manager. • Special Committee of Cole Credit Property Trust II Inc. -

Fact Sheet:State Street Aggregate Bond Index Fund, Jun2021

State Street Aggregate Bond Index Fund - Class K Fixed Income 30 June 2021 Fund Objective Total Return The State Street Aggregate Bond Index Fund (the "Fund") seeks to provide Bloomberg Barclays investment results that, before fees and expenses, correspond generally U.S. Aggregate to the price and yield performance of an index that tracks the U.S. dollar Cumulative Fund at NAV Bond Index denominated investment grade bond market over the long term. QTD 1.80% 1.83% Process YTD -1.77 -1.60 The Fund seeks to achieve its investment objective by investing Annualized substantially all of its investable assets in the Aggregate Bond Index 1 Year -0.56 -0.33 Portfolio, which has substantially similar investment policies to the Fund 3 Year 5.31 5.34 when the Fund invests in this “master-feeder” structure, the Fund’s only 5 Year 2.88 3.03 investments are shares of the Portfolio and it participates in the investment returns achieved by the Portfolio. Under normal circumstances, at least Since Fund Inception 3.27 3.40 80% of the Fund's net assets will be invested (either on its own or as a part of a master/feeder structure) in securities comprising the Bloomberg Barclays U.S. Aggregate Bond Index (the "Index") or in securities that Gross Expense Ratio 0.215% SSGA Funds Management, Inc. (the “Adviser”) determines have economic Net Expense Ratio^ 0.025% characteristics that are comparable to the economic characteristics of 30 Day SEC Yield 2.04% securities that comprise the Index. The Fund is not managed according 30 Day SEC Yield (Unsubsidized) 1.94% to traditional methods of "active" investment management, which involve the buying and selling of securities based upon economic, financial Maximum Sales Charge - and market analysis and investment judgment. -

Fall Forum 2018 September 16 – 18 Four Seasons Hotel Baltimore, MD

Fall Forum 2018 September 16 – 18 Four Seasons Hotel Baltimore, MD AGENDA AT A GLANCE DRESS CODE FOR SUNDAY IS CASUAL AND MONDAY AND TUESDAY IS BUSINESS CASUAL. ALL TIMES AND SESSIONS ARE TENTATIVE AND SUBJECT TO CHANGE. Sunday, September 16, 2018 Time Meeting Room Floor 2:00 – 5:00 PM Board of Directors Meeting Azure 2nd Limited to Board of Directors only. 3:45 – 4:45 PM Co-Chair Meeting Grand Ballroom B 2nd Limited to Co-Chairs only. 5:00 – 6:00 PM Board of Directors & Co-Chair Meeting Grand Ballroom B 2nd Limited to Board of Directors and Co-Chairs only. 6:00 – 7:00 PM Cocktail Reception Splash Terrace – 4th weather permitting Grand Ballroom A – 2nd alternate Monday, September 17, 2018 Time Meeting Room Floor 8:00 – 9:00 AM Breakfast & New Member/First Time Attendee Grand Ballroom B 2nd Orientation 9:00 – 11:00 AM General Session Grand Ballroom A 2nd • Update from the Chair Erica Borghi, Brown Brothers Harriman & Co. • Security Aspects for Digital Currencies: ISO Standards Edward Scheidt, ANSI X9 Financial Standards Today, many use digital platforms for payments and transactions. Standards offer an international compromise and acceptance. As the International Standards Organization (ISO) advance digital use cases with currencies, security becomes the differentiation among the world bodies. Security technologies, policies, and innovations are needed to ensure Trust. • Modernizing the U.S. Equity Post-Trade Infrastructure & Settlement Optimization John Abel, DTCC John Abel, Executive Director DTCC Settlement Services, will discuss how DTCC is exploring several ways to further shorten the trade settlement cycle beyond T+2 and introduce new operational and capital efficiencies to the NSCC and DTC transactional workflows. -

Gold: the Original Liquid Alternative

Gold: The Original Liquid Alternative In today’s market environment, it is increasingly important to balance the need for diversification with risk-adjusted performance. Interest in alternatives (private equity, hedge funds, real estate, and commodities) has significantly grown over the past decade for two main reasons: 1) investors seek positive risk-adjusted returns and 2) they want to improve the diversification of traditional stock/bond portfolios while mitigating risk. Gold has historically shown that it may improve both. GOLD AS AN ALTERNATIVE TO ENHANCE ALTERNATIVES promote buying (investing in) gold as a store of value.1 In turn, One of the foundations of modern asset allocation is this creates a balance that drives gold’s lack of correlation to that, over the long run, a well-balanced portfolio increases other assets.2 risk-adjusted returns. Hedge funds, private equity, real estate, liquid alternatives (managed futures, long/short equity) and GOLD: METAL BY DESIGN, CURRENCY BY NATURE even commodities can potentially help investors achieve While we believe that commodities are an important portfolio higher risk-adjusted returns when compared to stocks and diversifier that can help hedge against inflation, gold’s unique bonds alone. But gold may offer benefits that cannot be solely characteristics make it stand out. Gold has low correlation obtained by investing in bonds, stocks or other alternative to commodities (Figure 3) and, in general, we believe that strategies. In other words, whether an investor is considering investors should see gold as more than a line-item in a generic adding alternatives to their asset allocation, has already commodities basket allocation. -

FX Factors and Media

FX Factors and Media Media information can improve the performance of FX carry, momentum and valuation Currency management styles or factors are now firmly part of the active currency management Figure 1: G10 Value & Media, returns and information ratios landscape. Rule-based active currency factors such 35% Value + Media IR = 0.7 as Momentum, Valuation and Carry have been shown 30% to generate positive risk-adjusted returns over the 25% long term, though their performance can be sensitive 20% through time. 15% Value IR = 0.2 10% 5% Cumulative return Cumulative measures of media sentiment, intensity and 0% disagreement, which capture the tone, volume and -5% returns correlation = 0.7 dispersion of media coverage drawn from hundreds -10% of thousands of curated, unstructured online Mar'13 Mar'14 Mar'15 Mar'16 Mar'17 Mar'18 Mar'19 sources. Over the past six years, we have found that Value Value+Media this data can generate timely insights into the Source: State Street Global Markets. Notes: Results span 13 to . We performance of foreign currencies. These near real- measure factor performance from 2013 onwards to span the period for which we have media data. G10 currencies: AUD, CAD, CHF, EUR, GBP, JPY, NOK, NZD, time pulses of broad media coverage enable investors SEK, USD to evaluate the impact of online chatter and control for systematic biases. Combinining these measures of media with traditional FX factors such as Momentum, Valuation and Carry can help enhance returns, reduce risk, and improve risk-adjusted performance. Figure 1 shows the historical performance of the media-enhanced value factor (Value+Media) applied to the major G10 currencies. -

Fact Sheet:SPDR® Bloomberg Barclays Global Aggregate Bond

EMEA_ETFEQFI 31 July 2021 31 August 2021 SPDR® Bloomberg Barclays Global Aggregate Bond USD Hdg UCITS ETF (Dist) ISIN IE00BF1QPH33 Index Description The Bloomberg Barclays Global Aggregate Bond Index (USD Fund Objective Hedged) represents a close estimation of the performance that can The objective of the Fund is to track the performance of global be achieved by hedging the currency exposure of its parent index, markets for investment grade (high quality) fixed-rate debt the Bloomberg Barclays Global Aggregate Bond Index, to USD. The securities. index is 100% hedged to the USD by selling the forwards of all the currencies in the parent index at the one-month Forward rate. The parent index is composed of government, government-related and corporate bonds, as well as asset-backed, mortgage-backed and commercial mortgage-backed securities from both developed and emerging markets issuers. Index Ticker LEGATRUH Index Type Total Return Number of Constituents 27,340 Key Facts Inception Date Income Treatment Domicile ISA Eligible Currency Hedging 14-Feb-2018 Semi-Annually Distribution Ireland Yes Monthly Share Class Currency Replication Method Investment Manager SIPP Eligible USD Stratified Sampling State Street Global Advisors Yes Europe Limited Fund - Base Currency UCITS Compliant PEA Eligible USD Yes Fund Umbrella No SSGA SPDR ETFs Europe I plc TER Sub-Investment Man- 0.10% Share Class Assets (millions) ager US$994.03 State Street Global Advisors Limited Total Fund Assets (millions) US$2,012.08 TAX STATUS As standard, SSGA aims to meet all applicable tax reporting requirements for all of the SPDR ETFs in the following countries. -

Fourth Quarter & Full Year 2017 Financial Highlights

Fourth Quarter & Full Year 2017 Financial Highlights January 23, 2018 (NYSE: STT) Preface and forward-looking statements This presentation includes certain highlights of, and also material supplemental to, State Street Corporation’s news release announcing its fourth quarter and full year 2017 financial results. That news release contains a more detailed discussion of many of the matters described in this presentation and is accompanied by detailed financial tables. This presentation is designed to be reviewed together with that news release, which is available on State Street’s website, at www.statestreet.com/stockholder, and is incorporated herein by reference. This presentation (and the conference call accompanying it) contains forward-looking statements as defined by United States securities laws. These statements are not guarantees of future performance, are inherently uncertain, are based on assumptions that are difficult to predict and have a number of risks and uncertainties. The forward-looking statements in this presentation speak only as of January 23, 2018, and State Street does not undertake efforts to revise forward-looking statements. See “Forward-Looking Statements” in the Appendix for more information, including a description of certain factors that could affect future results and outcomes. Financial information in this presentation includes presentation on both an “operating” or otherwise adjusted basis, which represent non-GAAP presentations. Refer to the Appendix for explanations of our non-GAAP financial measures, -

INVESTED in DISRUPTION IQ Redefining Investment Performance

Q3 & 4 2017 INVESTED IN DISRUPTION IQ Redefining Investment Performance The New Alternatives Paradigm Disruption in Action Demography and Destiny Q3&4 2017 IQ magazine provides the most relevant thought IQ leadership from State Street Global Advisors. We live in an age of disruption, in which business models, industries and even our daily lives are being transformed. As the pace of disruption accelerates, we look at game-changing shifts that are redefining ideas around investment performance and value and how investors can navigate this new landscape. State Street Global Advisors 2 4 ALL CHANGE While macroeconomic conditions might suggest a return to “normal,” disruptions on all sides require investors to embrace change and look for the opportunities. 8 CHANGE THE GOAL, CHANGE THE GAME In our latest investment roundtable, we look at how institutional investors are redefining ideas of performance and value beyond traditional metrics. 14 THE NEW ALTERNATIVES PARADIGM Alternatives remain an important portfolio component, but liquidity lessons and factor approaches are transforming how investors build their exposures. 20 DISRUPTION IN ACTION Automobiles, healthcare and retail are in the front lines of creative destruction: we look at what those disruptions mean for investors. 32 DEMOGRAPHIC DISRUPTION Ageing populations around the world are challenging assumptions about saving and investing. State Street Global Advisors 3 RICK LACAILLE Global Chief Investment Officer ALL State Street Global Advisors CHANGEAs we move into the final stretch of 2017, the global economy continues to grind higher, with overall growth for the year slated to improve for the first time in three years. While the stimulus expected from the new Trump administration has languished, the equity bull market in the US nonetheless is charging into its ninth year. -

2003 - 2019 Top 200 Employers for CPT Students**

2003 - 2019 Top 200 Employers for CPT Students** **If a student is employed at the same Employer while in a different program, he/she will be counted multiple times for that employer. Top 200 Employer Names Number of Students Participating in CPT in 2003-2019 Amazon 9,302 Intel Corporation 6,453 Microsoft Corporation 6,340 Google 6,132 IBM 4,721 Deloitte 3,870 Facebook 3,810 Qualcomm Technologies, Inc 3,371 Ernst & Young 2,929 Goldman Sachs 2,867 Cummins 2,729 JP Morgan Chase 2,474 PricewaterhouseCoopers 2,295 Bank of America 2,241 Apple, Inc 2,229 Cisco System, Inc 2,133 Disney 2,041 Morgan Stanley 1,970 World Bank 1,956 Citigroup 1,904 Merrill Lynch 1,850 KPMG 1,464 Dell, Inc 1,448 Yahoo 1,403 Motorola 1,357 Tesla, Inc 1,314 eBay or PayPal 1,268 Kelly Services 1,195 EMC Corporation 1,119 NVIDIA Corporation 1,110 Walmart 1,108 Samsung Research America 1,102 Ericsson, Inc 1,100 Adobe Systems Incorporated 1,085 PRO Unlimited 1,042 Texas Instruments 1,022 Credit Suisse 1017 Barclays 970 Randstad 942 Sony 930 Schlumberger 928 McKinsey & Company 883 2003 - 2019 Top 200 Employers for CPT Students** **If a student is employed at the same Employer while in a different program, he/she will be counted multiple times for that employer. VMWare 868 Adecco 845 Philips 829 Deutsche Bank 797 Broadcom Corporation 791 HP, Inc 789 Oracle 789 Advanced Micro Devices, Inc 782 Micron Technology, Inc 775 Boston Consulting Group 755 CVS Pharmacy 741 Robert Bosch LLC 723 Bloomberg 711 State Street 705 Hewlett-Packard 702 Alcatel-Lucent 666 Oak Ridge Institute for Science and Education 662 Genentech 657 Symantec Corporation 657 Nokia 642 Aerotek, Inc 638 Los Alamos National Laboratory 638 LinkedIn 635 Tekmark Global Solutions LLC 634 Populus Group 624 Salesforce 623 SAP America, Inc 619 Juniper Network 609 Atrium 584 The Mathworks, Inc 582 Monsanto 581 Wayfair 580 Autodesk 571 Intuit 562 Wells Fargo 559 Synopsys, Inc 546 NEC Laboratories America, Inc. -

State Street Corporation

03/25/2020 STATE STREET CORPORATION Annual Report of Holding Companies- FR Y-6 For the Fiscal Year Ending December 31, 2019 Contents: Signature Page Reference Index 2019 State Street Corporation Form 10-K 2019 State Street Corporation Organizational Chart 2019 State Street Corporation Domestic Branch Listing of Directors and Executive Officers STATE STREET CORPORATION ANNUAL REPORT OF HOLDING COMPANIES-FR Y-6 For the fiscal year ending December 31, 2019 REPORT ITEM 1a: Form 10-K filed with the Securities and Exchange Commission. State Street Corporation files its 2019 Form 10-K with the SEC via EDGAR transmission. A hard copy of that transmission is enclosed as Required Exhibit I. REPORT ITEM 1b: Not applicable, see 1a. REPORT ITEM 2a: Organizational Chart: This chart is as of December 31, 2019 and appears as Exhibit II. REPORT ITEM 2b: Domestic Branch Listing: This listing is as of December 31, 2019 and appears as Exhibit III. REPORT ITEM 3: Securities Holders: This information is as of December 31, 2019 and appears as Exhibit IV. REPORT ITEM 4: Insiders: The list of Directors and Executive Officers appears as Exhibit V. REPORT ITEM 1a: Form 10-K filed with the Securities and Exchange Commission EXHIBIT I Section 1: 10-K (10-K) UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 Form 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2019 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File No. -

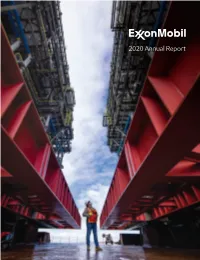

2020 Annual Report

2020 Annual Report CONTENTS II To our shareholders IV Positioning for a lower-carbon energy future VI Energy for a growing population Scalable technology solutions VIII Providing energy and products for modern life IX Progressing advantaged investments X Creating value through our integrated businesses XII Upstream XIV Downstream XV Chemical XVI Board of Directors 1 Form 10-K 124 Stock performance graphs 125 Frequently used terms 126 Footnotes 127 Investor information ABOUT THE COVER Delivery of two modules to the Corpus Christi Chemical Project site in 2020. Each module weighed more than 17 million pounds, reached the height of a 17-story building, and was transported more than 5 miles over land. Cautionary Statement • Statements of future events or conditions in this report are forward-looking statements. Actual future results, including financial and operating performance; demand growth and mix; planned capital and cash operating expense reductions and efficiency improvements, and ability to meet or exceed announced reduction objectives; future reductions in emissions intensity and resulting reductions in absolute emissions; carbon capture results; resource recoveries; production rates; project plans, timing, costs, and capacities; drilling programs and improvements; and product sales and mix differ materially due to a number of factors including global or regional changes in oil, gas, or petrochemicals prices or other market or economic conditions affecting the oil, gas, and petrochemical industries; the severity, length and ultimate -

Large Bank Capital Requirements August 2021

Large Bank Capital Requirements August 2021 Board of Governors of the Federal Reserve System www.federalreserve.gov Under the Federal Reserve Board’s capital framework for bank holding companies and U.S. intermediate holding companies with $100 billion or more in total consolidated assets, capital requirements are in part determined by the supervisory stress test results. Table 1 shows the total common equity tier 1 (CET1) capital requirement for each large bank, which is made up of several components, including • a minimum CET1 capital requirement of 4.5 percent, which is the same for each bank; • the stress capital buffer (SCB) requirement, which is determined from the supervisory stress test results and is at least 2.5 percent;1 and • if applicable, a capital surcharge for global systemically important banks (G-SIBs), which is at least 1.0 percent. 1 See 12 C.F.R. § 225.8(f) for rules on the SCB requirement calculation and Dodd-Frank Act Stress Test 2021: Super- visory Stress Test Results, https://www.federalreserve.gov/publications/files/2021-dfast-results-20210624.pdf, for details on which large banks participated in the Dodd-Frank Act Stress Test (DFAST) 2021 cycle. The firms that did not participate in DFAST 2021 have SCB requirements based on DFAST 2020 results and that have been adjusted by the Federal Reserve Board pursuant to 12 C.F.R. § 225.8(f)(4). 2 Large Bank Capital Requirements Table 1. Large bank capital requirements, effective October 1, 2021 Percent Minimum CET1 Stress capital buffer CET1 capital Bank G-SIB surcharge* capital ratio requirement requirement Ally Financial Inc.† 4.5 3.5 n/a 8.0 American Express Company† 4.5 2.5 n/a 7.0 Bank of America Corporation 4.5 2.5 2.5 9.5 The Bank of New York Mellon Corporation 4.5 2.5 1.5 8.5 Barclays US LLC 4.5 3.6 n/a 8.1 BMO Financial Corp.