The Complexity of Bank Holding Companies: a New Measurement Approach

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Wells Fargo & Company

No. 15-5059 IN THE UNITED STATES COURT OF APPEALS FOR THE FEDERAL CIRCUIT WELLS FARGO & COMPANY, Plaintiff-Appellee v. UNITED STATES, Defendant-Appellant ON APPEAL FROM THE ORDER OF THE UNITED STATES COURT OF FEDERAL CLAIMS No. 11-808-T, Judge Nancy Firestone CORRECTED BRIEF FOR THE APPELLANT CAROLINE D. CIRAOLO Acting Assistant Attorney General DIANA L. ERBSEN Deputy Assistant Attorney General GILBERT S. ROTHENBERG (202) 514-3361 JONATHAN S. COHEN (202) 514-2970 ELLEN PAGE DELSOLE (202) 514-8128 Attorneys, Tax Division Department of Justice Post Office Box 502 Washington, D.C. 20044 May 13, 2015 12695276.1 TABLE OF CONTENTS Page Table of contents ......................................................................................... i Table of authorities .................................................................................. iii Statement of related cases ........................................................................ xi Glossary ...................................................................................................xiii Jurisdictional statement ......................................................................... xiv Statement of the issues .............................................................................. 1 Statement of the case ................................................................................. 2 A. Procedural History ................................................................... 2 B. Factual Background ................................................................ -

The California Numismatist

Numismatic Fall 2008 California State Association of V. 5, No. 3 Numismatic Southern California $5.00 Association The California Numismatist The California Numismatist Offi cial Publication of the California State Numismatic Association and the Numismatic Association of Southern California Fall 2008, Volume 5, Number 3 About the Cover The California Numismatist Staff Images from our three main Editor Greg Burns articles grace our cover against a P.O. Box 1181 backdrop relating to a surprising de- Claremont, CA 91711 velopment in the printing of our little [email protected] journal: color! This is the fi rst issue Club Reports Virginia Bourke with the interior pages printed in color, South 10601 Vista Camino though the cover has been in color Lakeside, CA 92040 since the inception of TCN in 2004 [email protected] (starting in 2002 The NASC Quarterly, one of our predecessor publications, Club Reports Michael S. Turrini also started having color covers). North P.O. Box 4104 Please do write and let us know Vallejo, CA 94590 what you think about the new look. [email protected] While the expense is a bit more, Advertising Lila Anderson there’s such an improvement in aes- P.O. Box 365 thetics we’re inclined to keep it up. Grover Beach, CA 93483 [email protected] Visit Us on the Web The California Numismatist has a Web site at www.CalNumismatist.com. You can fi nd the offi cial scoop there in between issues. Also, both CSNA and NASC main- tain their own Web sites at: www.Calcoin.org www.NASC.net 2 The California Numismatist • Fall 2008 Contents Articles Wells Fargo & Company Jim Hunt ............................................................................................................10 Through the Numismatic Glass: This 19th Century Cent Design Lasted for Only One Year Dr. -

Temple R. Hollcroft Collection

Temple Hollcroft Collection WELLS COLLEGE ARCHIVES AND SPECIAL COLLECTIONS TEMPLE R. HOLLCROFT COLLECTION Quantity: 5 Linear Feet Containers: 5 Archival Boxes Date Processed: Fall 2010 Processed by: Kathryn McNamara Finding Aid: December 12, 2010 / Amended October 22, 2019 By: Kathryn McNamara / Amended by Robyn Fordyce Edited by: Molly Brown / Tiffany Raymond Prepared for Web: By: Access: There is no restriction on access to the Temple Hollcroft Collection for research use. Particularly fragile items may be restricted for preservation purposes. Copyright: Requests for permission to publish material from the Temple Hollcroft Collection should be directed to the Archives and Special Collections. It is the responsibility of the researcher to identify and satisfy the holders of all copyrights. Page 2 Temple Hollcroft Collection INTRODUCTION Biographical Note/Background: Temple Rice Hollcroft was born in Indiana in 1889. He was a Mathematics Professor at Wells College beginning in 1918 and stayed for 36 years. After his tenure as a faculty member, he was named as the Wells College Historian in 1953, and his interest in history served the college well. He was thorough and dedicated to the position, and a series of his short pieces of historical interest appeared in the Alumna News. He was interested in statistics and intent on accuracy and correct presentation. He died in New York, September of 1967. Related Material: Hollcroft, Temple. A History of Wells College. (3 copies) Hollcroft, Temple. Wells Fargo History. Manuscript (ribbon copy), 1968. Hollcroft, Temple. Salem Town: Partial Autobiography and Masonic Biography. New York: American Lodge of Research, Free and Accepted Masons, 1951. Print. -

2001-Annual-Report.Pdf

Connected to our past, focused on our future. Wells Fargo & Company Annual Report 2001 1 Connected to our Past, Wells Fargo & Company (NYSE:WFC) is a Focused on our Future diversified financial services company— From the 1850s to the 2000s, our values providing banking, insurance, investments, are the same. Sixteen of our team members tell you how. mortgage and consumer finance from more than 5,400 stores, the industry’s leading 17 To our Owners Chairman and CEO Dick Kovacevich internet site (wellsfargo.com) and other reports on 2001, and our progress in distribution channels across North America. market share growth and service quality. Our corporate headquarters is in San Francisco 24 Serving our Communities: but we’re decentralized so all Wells Fargo “The Good We May Render” “convenience points”—stores, ATMs, We contribute an average of $175,000 Phone BankSM centers, internet and direct a day to non-profits across the USA. mail —are headquarters for satisfying all our Our goal: help all our communities grow and prosper. customers’financial needs and helping them succeed financially. 29 The Businesses of Wells Fargo We’re one of North America’s largest, Assets: $308 billion most diversified financial services Rank in size among U.S. peers: 5th companies. Here’s how the pieces fit. Market value of stock: $74 billion 31 Board of Directors, Corporate Officers, Rank by value of stock among U.S. peers: 3rd Senior Business Officers Fortune 500 rank: 62 33 Financial Review Team members: 120,000 54 Financial Statements 97 Independent Auditors’ Report 100 Shareholder Information FORWARD-LOOKING STATEMENTS In this report we make forward-looking statements about our company’s financial condition, results of operations, plans, objectives and future performance and business. -

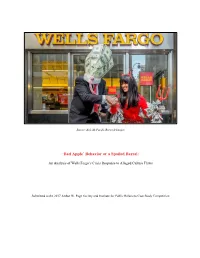

Bad Apple’ Behavior Or a Spoiled Barrel

Source: Erik M./Pacific/Barcroft Images ‘Bad Apple’ Behavior or a Spoiled Barrel: An Analysis of Wells Fargo’s Crisis Response to Alleged Culture Flaws Submitted to the 2017 Arthur W. Page Society and Institute for Public Relations Case Study Competition Abstract Who’s held accountable when deceptive practices are revealed in a company’s operations – those conducting the unethical behavior or company leadership? Wells Fargo continues to publicly grapple with this question as it mitigates damages from a fraudulent account scandal. Initial leadership response seemingly laid blame on a few ‘bad apples,’ but former employees pointed to a cross-sell-driven culture breeding bad behavior. The disparity between these viewpoints resulted in a controversy that gained intense stakeholder attention. This case study examines Wells Fargo’s crisis response to the scandal, as well as impacts to its financials, reputation and character. 1 Table of Contents Overview………………………………………………………………………………………..... 3 Company Background………………………………………………………………………... 3-6 1. Wells Fargo History……………………………………………….………………….... 3-5 2. Corporate Reputation…………………………………………………………………….. 5 3. Corporate Culture……………………………………………………………………… 5-6 Fraudulent Account Activity Timeline (2011 to 2016)…........................................................ 6-7 Wells Fargo’s Actions and Response……………………………………………………….. 7-10 Cultural Disconnect………………………………………………………………………… 10-14 1. Employee Response in the Media…………………………..………………………. 10-12 2. Corporate Values and Character…………………………………………………..... -

Sept.2015 Newsletter

September 2015 Pres Says: PP 2012The County Courthouse is showing signs of moving activity….We will keep you abreast of This year is an exciting year for the Yolo County that project. Historical Society. We have great programs lined up for your enjoyment. October 18th at Now that school is in session, our fall living 2:00 p.m., we will be at the Pollock/Reiff Ranch history program will begin…We owe thanks to and hear about Wells Fargo right by the old the following ladies who came and cleaned for Wells Fargo Building. In November, we will the Fair: Erin and Lea Cliff, Andraya and go on a mini field trip to Sacramento and visit Jannell Tam, Betsy and Anjulee Petersen, Bella the Sacramento Medical Museum where Henneke, and Janene Denis. These ladies are instruments from the past are stored. In from the Church of Later Day Saints in January, we will visit Woodland Fire Station #1 Woodland. Thanks to Connie Crandall, one of and hear about the early efforts to fight fires in our school marms for arranging this. And Woodland and the Spring Lake area. In thanks to Connie for volunteering to teach February, we will be treated to a discussion on adults at the Fair. post cards and their history. All will be encouraged to bring old postcards to this Many of you commented on my article in the discussion. In March, we will look at the last newsletter “To Fix or Not To Fix”…Thank architecture of Woodland in the historic you …We have to be diligent…. -

El Rol Del Sistema Financiero En El Desarrollo Sostenible En Los Años 2002-2016: Economías Emergentes Y

Universidad de Lima Facultad de Ciencias Empresariales y Económicas Carrera de Economía EL ROL DEL SISTEMA FINANCIERO EN EL DESARROLLO SOSTENIBLE EN LOS AÑOS 2002-2016: ECONOMÍAS EMERGENTES Y DESARROLLADAS Tesis para optar el Título Profesional de Economista Kaori Stefania Olulo Taipe Código 20140936 Asesor Yuri Jesús Landa Arroyo Lima – Perú Abril de 2020 ii THE ROLE OF THE FINANCIAL SYSTEM IN SUSTAINABLE DEVELOPMENT IN THE YEARS 2002-2016: EMERGING AND DEVELOPED ECONOMIES iii TABLA DE CONTENIDO RESUMEN .................................................................................................. XI ABSTRACT ................................................................................................ XII INTRODUCCIÓN ...................................................................................... 1 CAPÍTULO I: MARCO TEÓRICO .......................................................... 8 1.1 Principios teóricos ................................................................................. 8 1.2 Sector bancario ...................................................................................... 10 1.2.1. Enfoque y componentes ...................................................................... 10 1.2.2. Inclusión y profundidad financiera ...................................................... 13 1.3 Mercado Bursátil ................................................................................... 15 1.3.1. Concepto y componentes .................................................................... 15 1.4 Revisión de la -

The Real Wells Fargo: Board & Management Failures, Consumer Abuses, and Ineffective Regulatory Oversight

THE REAL WELLS FARGO: BOARD & MANAGEMENT FAILURES, CONSUMER ABUSES, AND INEFFECTIVE REGULATORY OVERSIGHT REPORT PREPARED BY THE MAJORITY STAFF OF THE COMMITTEE ON FINANCIAL SERVICES, U.S. HOUSE OF REPRESENTATIVES THE HONORABLE MAXINE WATERS, CHAIRWOMAN THE HONORABLE AL GREEN, CHAIRMAN, SUBCOMMITTEE ON OVERSIGHT AND INVESTIGATIONS 116TH CONGRESS, SECOND SESSION MARCH 2020 This report has not been officially adopted by the Committee on Financial1 Services and may not necessarily reflect the views of its Members Table of Contents Executive Summary ................................................................................................................. 4 I. Introduction ................................................................................................................... 6 II. Background on Wells Fargo ........................................................................................... 9 III. The Committee Staff’s Investigation ............................................................................14 A. Consent Orders ..........................................................................................................15 1. 2016 Sales Practices Consent Orders. ......................................................................15 2. 2018 Federal Reserve Consent Order. ......................................................................18 3. 2018 Compliance Risk Management Consent Orders. .............................................19 B. Key Wells Fargo Board Members & Senior Executives ...........................................21 -

King of Cross-Sell” and the Race to Eight an Analysis of Wells Fargo’S Cross-Sell Numbers Since 1998

September 29, 2016 www.citizen.org The “King of Cross-Sell” and the Race to Eight An Analysis of Wells Fargo’s Cross-Sell Numbers Since 1998 Acknowledgments This report was written by Michael Tanglis, Senior Researcher for Public Citizen’s Congress Watch division and edited by Congress Watch Research Director Taylor Lincoln. About Public Citizen Public Citizen is a national non-profit organization with more than 400,000 members and supporters. We represent consumer interests through lobbying, litigation, administrative advocacy, research, and public education on a broad range of issues including consumer rights in the marketplace, product safety, financial regulation, worker safety, safe and affordable health care, campaign finance reform and government ethics, fair trade, climate change, and corporate and government accountability. Public Citizen’s Congress Watch 215 Pennsylvania Ave. S.E Washington, D.C. 20003 P: 202-546-4996 F: 202-547-7392 http://www.citizen.org © 2016 Public Citizen. Public Citizen The “King of Cross-Sell” and the Race to Eight Introduction “Cross-sell is the result of serving our customers extraordinarily well, understanding their financial needs and goals over their lifetimes, and ensuring we innovate our products, services, and channels so that we earn more of their business and help them succeed financially.” -John G. Stumpf, Chairman and CEO, Wells Fargo, The Vision & Values of Wells Fargo1 Cross-selling amounts to selling a new product to an existing customer. For example, if a customer only has a savings account with Wells Fargo, an employee may try to “cross-sell” that customer a checking, credit card, or other type of account. -

“Disclosure Update and Simplification,” Proposed Rule File No

October 18, 2016 Mary Jo White Chair Securities and Exchange Commission Re: “Disclosure Update and Simplification,” Proposed Rule File No. S7-15-16 RIN 3235-AL82 Dear Chair, We oppose the proposed rule of the Securities and Exchange Commission’s (SEC, Commission, or Agency) titled “Disclosure Update and Simplification.” This enormously complex tangle of jolting alterations that is speeding through the Agency poses serious dangers. The Commission must withdraw this proposal and approach disclosure from the vantage point of what best serves investors. Disclosure forms the foundation of market integrity, of how investors decide how to allocate their savings, and how the SEC can detect misconduct.1 Changes to this foundation threaten the entire market. Changes cannot be made without extreme care. Yet the SEC proposes a major devaluation of this disclosure framework and couches its proposal in the comforting phrase “disclosure simplification.” On its face, the rulemaking may appear to be a series of innocuous changes. In fact, these proposals portend vast and dangerous consequences for investors and the market generally. The recent revelations that Wells Fargo signed up customers for accounts without their consent serves as an obvious object lesson about the need for more, not less disclosure, and for better enforcement of existing disclosure rules. According to the Consumer Financial Protection Bureau (CFPB), the Office of the Comptroller of the Currency (OCC), and the Los Angeles (LA) City Attorney, Wells Fargo engaged in fraudulent cross-selling practices that were described respectively as “improper, ”2 “unsafe or unsound,”3 and “an ambitious and 1 Joel Seligman, THE TRANSFORMATION OF WALL STREET, Houghton Mifflin (2003) 2 In the matter of: Wells Fargo Bank, N.A., Consent Order, U.S. -

Wachovia Corp 10K 2007

FORM 10-K WACHOVIA CORP NEW - WB Filed: February 28, 2008 (period: December 31, 2007) Annual report which provides a comprehensive overview of the company for the past year Table of Contents 10-K - WACHOVIA CORPORATION PART I ITEM 1. BUSINESS. ITEM 1A. RISK FACTORS. ITEM 1B. UNRESOLVED STAFF COMMENTS. ITEM 2. PROPERTIES. ITEM 3. LEGAL PROCEEDINGS. ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS. PART II ITEM 5. MARKET FOR REGISTRANT S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. ITEM 6. SELECTED FINANCIAL DATA. ITEM 7. MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK. ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA. ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE. ITEM 9A. CONTROLS AND PROCEDURES. ITEM 9B. OTHER INFORMATION. PART III ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE. ITEM 11. EXECUTIVE COMPENSATION. ITEM 12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS. ITEM 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE. ITEM 14. PRINCIPAL ACCOUNTING FEES AND SERVICES. PART IV ITEM 15. EXHIBITS, FINANCIAL STATEMENT SCHEDULES. SIGNATURES EXHIBIT INDEX EX-10.P (EXHIBIT (10)(P)) EX-12.A (EXHIBIT (12)(A)) EX-12.B (EXHIBIT (12)(B)) EX-13 (EXHIBIT (13)) EX-21 (EXHIBIT (21)) EX-23 (EXHIBIT (23)) EX-24 (EXHIBIT (24)) EX-31.A (EXHIBIT (31)(A)) EX-31.B (EXHIBIT (31)(B)) EX-32.A (EXHIBIT (32)(A)) EX-32.B (EXHIBIT (32)(B)) Source: WACHOVIA CORP NEW, 10-K, February 28, 2008 SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. -

For Immediate Release April 13, 1998

For immediate release April 13, 1998 The Federal Reserve Board today conditionally approved the applications and notices of First Union Corporation, Charlotte, North Carolina, to merge with CoreStates Financial Corp, Philadelphia, Pennsylvania, and thereby acquire CoreStates Bank, N.A., Philadelphia, and CoreStates Bank of Delaware, N.A., Wilmington, Delaware, and the nonbanking subsidiaries and foreign branches of CoreStates. The Board's approval is conditioned on the divestiture of 23 branches in the Philadelphia banking market and 9 branches in the Lehigh Valley banking market. First Union must also report any changes in its preliminary plans to close branches in low- and moderate-income census tracts to the Federal Reserve System for a period of two years. Attached is the Board's Order relating to this action. Attachment - 2 - FEDERAL RESERVE SYSTEM First Union Corporation Charlotte, North Carolina Order Approving the Merger of Bank Holding Companies First Union Corporation (“First Union”), a bank holding company within the meaning of the Bank Holding Company Act (“BHC Act”), has requested the Board’s approval under section 3 of the BHC Act (12 U.S.C. § 1842) to merge with CoreStates Financial Corp (“CoreStates”) and thereby acquire CoreStates Bank, N.A., Philadelphia, Pennsylvania (“CoreStates Bank”), and CoreStates Bank of Delaware, N.A., Wilmington, Delaware (“CoreStates Delaware”).1/ First Union also has requested the Board’s approval under section 4(c)(8) of the BHC Act (12 U.S.C. § 1843(c)(8)) to acquire the nonbanking subsidiaries of CoreStates and, under section 25 of the Federal Reserve Act (12 U.S.C. § 601), to acquire CoreStates Bank’s foreign branches.