FEB 2021 Wonder Home Finance Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Industries for Which CPCB Has Checked Remote Zero and Span

List of industries for which CPCB has checked Remote Zero and Span Check facility installed for Online Continuous Emission Monitoring Systems and deviation was found less than 10% w.r.t reference Gas Concentration - as on 3rd April, 2019 1) Remote Calibration facility is mandatory for applicable emission parameters (except PM) in 17 category industries and GPIs. 2) CPCB/SPCPs/PCCs may conduct zero & Span check remotely from time to time as per requirement. S. Industry Details Category State No. Hindalco Industries Limited, Mahan, NH-75E, SINGRAULI -SIDHI 1 Aluminium Madhya Pradesh ROAD, P.O-BARGAWAN, DISTT- SINGRAULI 486886 Birla Corporation Limited, Unit- Satna Cement Works, P.O. - Birla Vikas, 2 Cement Madhya Pradesh Distt. - Satna (M.P.) Pin- 485005 M/s Shree Cement Limited-Village-Ras, Tehsil-Jaitran,Distt.-Pali, 3 Cement Rajasthan Rajasthan 4 Tamilnadu Newsprint And Papaers Limited(Mini Cement), Karur Cement Tamilnadu 5 Rain Cements Limited, Ramapuram Cement Telangana 6 Zuari Cement Limited, Yerraguntla Cement Andhra Pradesh 7 J K Cement Works, Nimbahera Plant Cement Rajasthan 8 NCL Industries Ltd Cement Telangana 9 J. K Cements Limited, Mangrol Cement Rajasthan 10 India cements Limited, Vishnupuram Works, Wadapally Cement Telangana Sri Jayajothi Cements Pvt. Ltd., Yanakandla Village, Banaganapalle 11 Cement Andhra Pradesh Mandal, Kurnool Dist The India Cements Limited, Malkapur Works, Malkapura (V), Tandur 12 Cement Telangana (M),Rangareddy District, Rangareddy, Telangana 13 Reliance Cement ltd., Maihar, Madhya Pradesh Cement Madhya Pradesh Zuari Cement Limited, Sithapuram, Dondapadu (V), Mellacheruvu (M). 14 Cement Telangana Nalgonda District NUVOCO vistas corp. ltd. (Formerly LAFARGE CEMENT-Chittorgarh), 15 cement Rajasthan Bhawalia, Nimbahera, Rajasthan S. -

Csr Company Related Letter 17.07.2019

CSR Companies Contact Details S.No. District Company Name Concerned Name Mobile/Email 1 Ajmer R.K.Marble Pvt. Ltd., Makrana Road, Sh. Subhash C. Agarwal [email protected] Madanganj- Kishangarh- Mr. Suresh Patni 305801Ajmer 9829071401 2 Ajmer Shree Cement Ltd, Bangur Nagar, Sh. Bhawani Singh 9251037546 Beawar, Ajmer [email protected] 3 Ajmer Property Ventures (India) Pvt. Ltd., Sh. Vikas Patni [email protected] Makrana Road, Madanganj- Sh. Hemant Rathi, [email protected] Kishangarh, Ajmer Director [email protected] Sh. Namita Jain, CS 9829071401 4 Alwar Vintage Distillers Ltd., 117, M.I.A. Sh. Saurabh Jain 7665779000 Alwar-301030 Sh. Prakash Narang, 7073709112 Manager Personnel 7073709111 [email protected] [email protected] 5 Alwar United Breweries Ltd., UB Tower, Ms. Tushara Shankar (91-80) 39855000, Direct 39855 Level 3-5, UB City, #24 Vittal Maliya [email protected] Road, Bengaluru-560001 6 Alwar Eicher Engines ( A unit of TAFE Sh. R.N.Sahai [email protected] Motors and Tractors Limited), Sr. DGM 9414017928 Itarana Road, Alwar- 301001 Sh. Nageshwar Dutt [email protected] Lakhawat 7 Alwar Carlsberg India Pvt. Ltd., Plot No. SP- Sh. Ananad Shrivastava [email protected] 1-4& 5-8, Agro Food Park, MIA Ext. [email protected] Alwar 9785107507 8 Alwar Ashok Leyland Ltd., SPL-298, MIA, Sh. Gopinath [email protected] Alwar- 301 030 Asst. Manager-HR 9414020361 9 Alwar Metso India Pvt. Ltd., SP 1-1 to 1-13, Sh. Sanjay Sehgal [email protected] MIA Industrial Area, South East Sr. Manager 8094019207 Zone, Alwar- 301030 10 Alwar Havells India Ltd. -

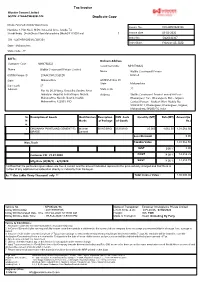

Tax Invoice Duplicate Copy 1

Tax Invoice Wonder Cement Limited GSTIN:-27AAACW6009L1Z4 Duplicate Copy Dhule-Finished Goods Warehouse Invoice No.: DHL20INV020106 Nardana-1, Plot No.4, MIDC Industrial Area, Jatoda, Tal- ShindKheda, DhuleDhule PlantMaharashtra DhuleDP111001 ind 1 Invoice date 08-02-2020 Order No : SO20342367 CIN : U26943RJ2005PLC021205 Order Date : February 08, 2020 State : Maharashtra State Code : 27 Bill To: Delivery Address Customer Code : MHN790322 Customer Code : MHN790322 Name Wallfix Construwell Private Limited Name Wallfix Construwell Private GSTIN/Unique ID 27AACCW1215E1ZR Limited State Maharashtra GSTIN/Unique ID State Maharashtra State code 27 Address State code 27 Flat No 09, B Wing, Shraddha Garden, Near Jankalyan Hospital, Indira Nagar, Nashik, Address Wallfix Construwell Private Limited At Post - Maharashtra, Nashik, Nashik, Nashik, Dharangaon Tal - Dharangaon, Dist - Jalgaon Maharashtra, 422009, IND Contact Person - Mahesh Wani Mobile No - 9922929911, Dharangaon, Dharangaon, Jalgaon, Maharashtra, DP038276, India Sr. Description of Goods Identification Description HSN Code Quantity (MT) Rate(MT) Amount(in N Marks of Package of Goods Rs.) o. 1 ORDINARY PORTLAND CEMENT 53 Wonder 50 KG BAG 25232910 25.000 4,062.50 1,01,562.50 GRADE Cement Less Discount 0.00 Non_Trade Taxable Value 1,01,562.50 IGST 0.00 % 0.00 Customer PO : 27.01.2020 CGST 14.00 % 14,218.75 Mfg Date (W/M/Y) - 6/2/2020 SGST 14.00 % 14,218.75 Certified that the particulars given above are true & correct and the amount indicated represents the price actually charged and that there is no flow of any additional consideration directly or indirectly from the buyer. Rs. ** One Lakhs Thirty Thousand only ** Total Invoice Value : 1,30,000.00 Vehicle No. -

Power Plant Engineering HOLTEC

Power Plant Engineering HOLTEC A. WASTE HEAT RECOVERY BASED CAPTIVE POWER PLANT Capacity Client Name Project Location MW 1. Yanbu Cement Company $ Yanabu, Saudi Arabia 36.0 2. Najan Cement Company $ Najran, Saudi Arabia 27.0 3. J K Cement Limited Mangrol, Rajasthan 27.0 4. Prism Cement Limited Satna, Madhya Pradesh 22.0 5. Eastern Province Cement Company $ Saudi Arabia 21.0 6. Chettinard Cement Private Limited Dachapalli, Andhra Pradesh 19.0 7. Wonder Cement Limited Nimbahera, Rajasthan 18.0 8. Al Ain Cement Factory $ Abu Dhabi, UAE 18.0 9. UltraTech Cement Limited Awarpur, Maharashtra 13.22 10. Heidelberg Cement India Limited Damoh, Madhya Pradesh 12.7 11. Fujairah Cement Industries $ Fujairah, UAE 12.5 12. Emami Cement Limited Rishda, Chattisgarh 12.5 13. UltraTech Cement Limited (Rajashree) Malkhed, Karnataka 10.7 14. UltraTech Cement Limited Hirmi, Rajasthan 10.0 15. Nageri Sembilan Cement Industries SDN BHD $ Perlis, Malaysia 10.0 16. Adani Cementation Limited Lakhpat, Gujarat 9.0 17. Dalmia Cement Bharat Limited Kadapa Andhra Pradesh 9.0 18. Calcom Cement India Limited Umrangshu, Assam 8.0 19. Chettinad Cement Corporation Limited Kallur, India 7.5 20. Nuvoco Vistas Corporation Limited Chittorgarh, Rajasthan 7.0 21. Nuvoco Vistas Corporation Limited Arasmeta, Chhattisgarh 7.0 22. UltraTech Cement Limited Aditya Line 2 Shambhupura, Rajasthan 6.3 23. E.ON Masdar Integrated Carbon Limited $ Turkey 6.3 24. Oman Cement Company (SAOG) $ Daqm, Oman 6.0 25. Ambuja Cement Limited Rabriyawas, Rajasthan 6.0 26. Gujarat Sidhee Cement Limited Sidheegram, Gujarat 5.5 27. Ras Al Khaimah Cement Company $ Ras Al Khaimah, UAE 5.0 28. -

Press Release Wonder Home Finance Limited

Press Release Wonder Home Finance Limited December 31, 2020 Ratings Amount Facilities Ratings1 Rating Action (Rs. crore) Provisional CARE A- (CE) Placed on Credit 10.00 @ (Under Credit watch with Developing Implications) watch with (Reduced from 40.00) [Provisional Single A Minus (Credit Enhancement); Developing Under credit watch with developing implications] Implications CARE A- (CE) Placed on Credit 78.00 (Under Credit watch with Developing Implications) watch with Long Term bank (Enhanced from 50.00) [Single A Minus (Credit Enhancement)] (Under Developing facilities Credit watch with Developing Implications) Implications CARE A- (CE) (Under Credit watch with Developing Implications) 12.00 Assigned [Single A Minus (Credit Enhancement)] (Under Credit watch with Developing Implications) 150.00 CARE BBB+; Stable Reaffirmed (Enhanced from 10.00) [Triple B Plus; Outlook: Stable] 250.00 Total Facilities (Rupees Two Hundred and Fifty Crore only) @- The above rating is provisional and shall be confirmed once company furnishes evidence supporting execution of unconditional and irrevocable corporate guarantee by R. K. Marble Private Limited (RKMPL; rated CARE A- /CARE A2+; under credit watch with developing implications) and confirms the final repayment terms of the loan. Details of facilities in Annexure-1 Unsupported Rating 2 Withdrawn Detailed Rationale & Key Rating Drivers For CE Rating: The rating assigned to the bank facilities of Wonder Home Finance Limited (WHFL) continue to be based on the credit enhancement in the form of unconditional and irrevocable corporate guarantee extended by RKMPL. Detailed rationale and description of the key rating drivers of corporate guarantee provider i.e., RKMPL is available on our website www.careratings.com. -

Indian Minerals Yearbook 2017 (Part- III : Mineral Reviews)

CEMENT Indian Minerals Yearbook 2017 (Part- III : Mineral Reviews) 56th Edition CEMENT (ADVANCE RELEASE) GOVERNMENT OF INDIA MINISTRY OF MINES INDIAN BUREAU OF MINES Indira Bhavan, Civil Lines, NAGPUR – 440 001 PHONE/FAX NO. (0712) 2565471 PBX : (0712) 2562649, 2560544, 2560648 E-MAIL : [email protected] Website: www.ibm.gov.in March, 2018 5-1 CEMENT 5 Cement he Cement Industry in India is among the core IBM captures data from mineral consuming T Industries that is vital for economic growth industries as per provisions made under Rule 45, and development. Ever since the Industry was MCDR-2017 in Form 'M' (Erstwhile Form 'O'). delicensed in 1991, there has been remarkable As per the returns received from various cement growth that metamorphosed it to a globally plants and Survey of Cement Industry & Directory, competitive Market, making India the second 2017 the total installed capacity and the total largest producer of cement after China in the production of these plants have been arrived at 502.03 world. Cement is the basic building material and million tonnes and 153.64 millione tonnes, is used extensively in urban housing, industrial respectively. sector and infrastructure development. It has become synonymous with construction The Department of Industrial Policy and activity and the per capita consumption of cement Promotion (DIPP), Ministry of Commerce, Govt. of is accepted as an important indicator of the India publishes data on production and capacity of country's economic growth. cement in its Annual Report. As per Annual Report 2015-16, the total installed capacity of cement plants In terms of quality, technology, productivity have been placed at 421.10 million tonnes and the and efficiency, India compares well with the production of cement during 2015-16 was 283.45 best in the world. -

Rajasthan Chapter, Udaipur July, 2018 Bi-Monthly Vol

Rajasthan Chapter, Udaipur July, 2018 Bi-Monthly Vol. 18 No. 2 EXECUTIVE COMMITTEE National President MEAI : Shri A.K. Kothari SUPREME COURT Mob. : 9414155413 Email : [email protected] 1. The Supreme Court had stopped sand mining till scientific sand replenishment report is Patron : Shri R. P. Gupta prepared and evaluated in State of Rajasthan. Further direction is still awaited. Patron : Shri Akhilesh Joshi 2. Aravalli matter came up for hearing on dt. 26.7.18. State of Raj. have been given one month's Chairman : Prof. (Dr.) S. S. Rathore time by the Court to file reply of the report submitted by CEC. The State was not satisfied with Mob : 98290 41632 the report of Empowered Committee as the committee did not agree to 40 degree slope and E mail : [email protected] showed Aravalli range by dots. The range should have been regular and follow contours. Vice‐Chairman : Shri L.S. Shekhawat MINISTRY OF MINES Mob : 9001294907 1. PRIVATE CA FIRM HIRED TO AUDIT NATIONAL MINERAL EXPLORATION TRUST‐ E mail : [email protected] NMET is a state‐run non‐profit body with the primary objective of promoting regional and Secretary : Shri M.S. Paliwal detailed mineral exploration in the country. Faridabad‐based AKGS & Associates won the bid in Mob : 9414264334 February this year when it quoted the lowest fees of Rs 82,010. Three other CA firms ‐ two Delhi‐ E mail : [email protected] based and one Hissar based ‐ had also put in bids. However, AKGS has not submitted its audit Joint Secretary : Dr. S.C. -

Pre-Feasibility Report

Expansion of Integrated Cement Project - Clinker (9.5 to 13 MTPA), Cement (12 MTPA to 16 MTPA), & WHRB (30 to 45 MW) At Villages: Sangaria, Borakheri, Peerkhera and Rasulpura, Tehsil: Nimbahera, District: Chittorgarh (Rajasthan) Pre – Feasibility Report PRE-FEASIBILITY REPORT 1.0 EXECUTIVE SUMMARY M/s. Wonder Cement Limited is proposing for Expansion of Integrated Cement Project - Clinker (9.5 MTPA to 13 MTPA), Cement (12 MTPA to 16 MTPA), & WHRB (30 MW to 45 MW) near Villages: Sangaria, Borakheri, Peerkhera and Rasulpura, Tehsil: Nimbahera, District: Chittorgarh (Rajasthan) Salient Features of the Project S. NO. PARTICULARS DETAILS 1. Nature & Size of the Project Expansion of Integrated Cement Project - Clinker (9.5 MTPA to 13 MTPA), Cement (12 MTPA to 16 MTPA), & WHRB (30 MW to 45 MW) near Villages: Sangaria, Borakheri, Peerkhera and Rasulpura, Tehsil: Nimbahera, District: Chittorgarh (Rajasthan) 2. Category of the Project As per EIA Notification dated 14th September, 2006, as amended on 1st December, 2009; the project falls under Category “A”, Project or Activity ‘3(b)’. 3. Location details Villages Sangaria, Borakheri, Peerkhera and Rasulpura, Tehsil Nimbahera District Chittorgarh State Rajasthan 4. Latitude 24°39‘12.47” N & 24°40’ 14.8” N Longitude 74°37’ 43.26” E & 74°38‘48.56” E Toposheet No. 45 L-9 & 45 L-10 5. Plant Area 191.064 ha 6. Water Requirement Water requirement for the expansion project will be about 845 KLD. Source: Ground Water, Mine Sump Water & Gambhiri Reservoir 7. Power Requirement Power requirement for proposed expansion project is 48 MW out of which around 44 MW will be for cement plant and 4 MW for WHRB, colony and others. -

Brief Industrial Profile of Chittorgarh District

lR;eso t;rs Government of India Ministry of MSME Brief Industrial Profile of Chittorgarh District MSME - Development Institute (Ministry of MSME, Govt. of India) 22- Godown Industrial Estate, Jaipur - 302006 Phone 0141-2212098, 2213099, Fax: 0141-2210553 e-mail: dcdi-jaipur.dcmsme.gov.in Web site- www.msmedijaipur.gov.in 0 1 Contents S.No. Topic Page No. 1. General Characteristics of the District 3 1.1 Location & Geographical Area 3 1.2 Topography 3 1.3 Availability of Minerals 4-5 1.4 Forest 5 1.5 Administrative set up 5-6 2. District at a glance 7-9 2.1 Existing Status of Industrial Area in the District 9-10 Chittorgarh 3. Industrial Scenario of Chittorgarh 3.1 Industry at a Glance 10 3.2 Year Wise Trend of Units Registered 10-11 3.3 Details o Existing Micro & Small Enterprises & Artisan 11 Units in the District 3.4 Medium & Large Scale Industries 12 3.4.1 Public Sector Undertakings 12 3.5 Major Exportable Item 13 3.6 Growth Trend 13 3.7 Vendorisation/Ancillarisation of the Industry 13 3.8 Service Enterprises 3.8.1 Potentials areas for service Industry 13-14 3.8.2 Potential for new MSMEs 14 4 Existing Clusters of Micro & Small Enterprise 4.1 Detail of Major Clusters 15 4.1.1 Manufacturing Sector 15 4.2 Details for Indentified Cluster 15 4.2.1 Wooden toys cluster 15 4.2.2 Dyeing & Printing Cluster 16-17 5. Steps to set up MSMEs 18 6. Important contact nos. District Chittorgarh 19 7. -

Government of India Ministry of Commerce & Industry Department for Promotion of Industry and Internal Trade Lok Sabha Unstar

GOVERNMENT OF INDIA MINISTRY OF COMMERCE & INDUSTRY DEPARTMENT FOR PROMOTION OF INDUSTRY AND INTERNAL TRADE LOK SABHA UNSTARRED QUESTION NO. 3700. TO BE ANSWERED ON WEDNESDAY, THE 11TH DECEMBER, 2019. FUNCTIONING OF CEMENT FACTORIES 3700. SHRI VISHNU DAYAL RAM: SHRI SHANTANU THAKUR: Will the Minister of COMMERCE AND INDUSTRY be pleased to state: वाणि煍य एवं उ饍योग मंत्री (a) the State/UT-wise details of the cement factories functioning in the country; (b) the details of the productivity and quality improvement in cement industry that are proposed by the National Council for Cement and Building Materials (NCCBM); and (c) the State/UT-wise details of the number of sick cement factories and funds sanctioned/utilized and steps taken by the Government for the revival and development of infrastructure in the country including West Bengal during each of the last five years? ANSWER वाणिज्य एवं उ饍योग मंत्री (श्री पीयूष गोयल) THE MINISTER OF COMMERCE & INDUSTRY (SHRI PIYUSH GOYAL) (a): The State/UT-wise details of the cement factories functioning in the country as per information available with the Department are placed at Annexure ‘A’. (b): National Council for Cement and Building Materials (NCCBM) provides scientific, technological and industrial support services to the cement, related building materials and construction industries. (c): Cement Industry had been de-controlled in year 1989 and de-licensed in year 1991. Details of sick cement factories are not maintained by the Department for Promotion of Industry and Internal Trade. ******** ANNEXURE –A ANNEXURE REFERRED TO IN REPLY TO PART (a) OF THE LOK SABHA UNSTARRED QUESTION NO. -

Reliable and Energy Efficient Pumps for Cement Industry

Pioneering for You Reliable and Energy Efficient Pumps For Cement Industry SB_Metal_Industry_02_A4_200618_E Pioneering for You 01 Introduction Introduction 02 Who we are Founded in 1872 as Kupfer- und Messingwarenfabrik in Dortmund, Wilo has evolved from being a local specialist to a global player. As the majority shareholder with a stake of approximately 90 percent, the Caspar Ludwig Opländer Founded ensures the company’s continuity and independence. An uncompromising customer-driven mind-set, immediate market proximity and, in particular, our culture of innovation have made us who we are: one of the worldwide leading manufactures of high-tech pumps and pump systems. What we are Wilo is a premium supplier in the field of building services, water management and industry. This leading position drives us to maintain our superiority. For our customers, we make complex technologies user-friendly, simple to operate energy-efficient and powerful. The main focus of our activities is therefore on the people. We offer them outstanding products, system solutions and services. In this spirit, our brand promise “Pioneering for You” stands for maximum quality of life. Chinchwad, Pune Plant WILO Mather and Platt Pumps Pvt. Ltd. Mather and Platt started its Indian operations in 1913 from Kolkata, and has been fulfilling the need of water supply for more than 100 years in India for segments like building services, water management and industries. We started our operation at Chinchwad works in Pune, Maharashtra in year 1959. Mather and Platt Pump Ltd became part of WILO SE in the year 2005 And in year 2014, WILO Mather and Platt Pumps Ltd. -

Government of India Ministry of Heavy Industries and Public Enterprises Department of Heavy Industry

GOVERNMENT OF INDIA MINISTRY OF HEAVY INDUSTRIES AND PUBLIC ENTERPRISES DEPARTMENT OF HEAVY INDUSTRY LOKSABHA UNSTARRED QUESTION NO.2581 TO BE ANSWERED ON 15.12.2015 Revival of Japla Cement Factory 2581. SHRI VISHNU DAYAL RAM: Will the Minister of HEAVY INDUSTRIES AND PUBLIC ENTERPRISES be pleased to state: (a) the details of the cement factories functioning in the country, State-wise and location-wise; (b) the number of sick cement factories and the measures taken by the Government to revive them; (c) whether the Government has any proposal to revive the closed Japla Cement factory in Jharkhand and (d) if so, the details thereof? ANSWER MINISTER OF STATE IN THE MINISTRY OF HEAVY INDUSTRIES AND PUBLIC ENTERPRISES (SHRI G.M. SIDDESHWARA) (a): Details ofcement plants/factories presently functional in the countries as provided by Department of Industrial Policy and Promotion (DIPP) is enclosed as Annexure-I. (b): Department of Industrial Policy and Promotion has intimated that cement industries has been decontrolled in 1989 and de-licensed in 1991under the policy of liberalization and, hence, the Department does not take any action to revive sick cement industries. Further, Ministry of Finance/Department of Financial Services has informed that certain measures like financial re- construction, change in management of sick company, amalgamation with other company, sale or lease of part of or whole of sick company etc. are recommended by Board for Industrial and Financial Reconstruction (BIFR). A list of sick cement plants registered and pending with BIFR with their current status (State-wise) is attached as per Annexure-II. So far as Cement Corporation of India(CCI), a Central Public Sector Enterprise under Department of Heavy Industry is concerned, it is a BIFR referred sick company having Corporate office in Delhi.