Urban Development Program

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Investigation of Low Density Residential and Farming Zone Land

Investigation of Low Density Residential and Farming Zone Land 1 Contents Introduction ....................................................................................................................... 5 Map of the Study Area ....................................................................................................... 6 Summary of Recommendations......................................................................................... 8 Sites to be investigated further ........................................................................................ 12 Site 1: Simpsons Road ................................................................................................. 12 East Bendigo ................................................................................................................... 15 Site 2: South of Heinz Street, East of Murphy Street, West of the Airport ..................... 15 Epsom ............................................................................................................................. 20 Site 3: Allen Street to Jones Road................................................................................ 20 Site 4: Area bounded by Jones Road, Station Street, Sargeants Road and Midland Hwy .................................................................................................................................... 23 Site 5: Area bounded by Sargeants Road, Station Street, Midland Highway and Ligar Street .......................................................................................................................... -

Northern Victorian Cluster - Municipal Heatwave Plan

Northern Victorian Cluster - Municipal Heatwave Plan Sub Plan prepared February 2018 Template Prepared by Central Victorian Greenhouse Alliance for Buloke, Central Goldfields, Gannawarra, Loddon, Macedon Ranges and Mount Alexander shire councils who participated in the Resilient Community Assets Heat Health project and City of Greater Bendigo who was involved in the early stages of the project. The Resilient Community Assets Project — a partnership between the Victorian Government and six local councils. Version Control Date Version Details Officer April 2016 2 New Municipal Heatwave Plan Central Victorian Greenhouse template developed Alliance July 2016 2.1 Draft Municipal Heatwave Plan Mount Alexander Shire - developed for Heatwave Working Emergency Management Group Coordinator October 2016 2.2 Further devp. Mount Alexander Shire - Climate Change Coordinator November 2016 2.3 Municipal Heatwave Workshop Mount Alexander Shire - held – further development Climate Change Coordinator and Emergency Management Team November 2016 3.0 Final Version Mount Alexander Shire - Emergency Management Coordinator May 2017 3.1 Additional developments and Mount Alexander Shire - transition to Northern Victorian Emergency Management Cluster Sub Plan Coordinator June 2017 3.2 Campaspe Shire information Mount Alexander Shire - added Emergency Management Coordinator Abbreviations ABS Australian Bureau of Statistics AV Ambulance Victoria BOM Bureau of Meteorology CDCH Castlemaine District Community Health CH Castlemaine Health CSU Councils “Customer Service -

P L a C I N G S Bendigo Competitions Society Inc

P L A C I N G S Bendigo Competitions Society Inc. 2/06/2018 Morning Commences at 10:00 AM MODERN VOCAL COMPETITION SECTION: MV336 19 years and under MODERN BALLAD SOLO 1st Charlotte Plum (Ormond) 1st Sebastian-Jon Mathieson (Bunbartha) 2nd Liv Brereton (Epsom) 2nd Monique Heath (Donvale) 3rd Jemma Patullo (Ascot) HM Charli Patullo (Ascot) HM Lily O'Shea (Alfredton) SECTION: MV334 19 years and under COUNTRY MUSIC SOLO 1st Monique Heath (Donvale) 2nd Charli Patullo (Ascot) 3rd Amelie Ryan (Ascot) SECTION: MV338 19 years and under OWN CHOICE DUET or TRIO 1st Charli Patullo and Jemma Patullo (Ascot) 2nd Kandice Joye & Rhiannon Taylor (Montmorency) 3rd Amelie Ryan & Lauren MacKenzie (Spring Gully) 2/06/2018 Afternoon Commences at 1:00 PM MODERN VOCAL COMPETITION SECTION: MV332 19 years and under SONG FROM A STAGE MUSICAL SOLO 1st Monique Heath (Donvale) 2nd Jemma Patullo (Ascot) 3rd Charlotte Plum (Ormond) 3rd Liv Brereton (Epsom) HM Charli Patullo (Ascot) HM Rhiannon Taylor (Montmorency) Page 1 of 9 SECTION: MV330 19 years and under CONTEMPORARY UP TEMPO SOLO 1st Liv Brereton (Epsom) 2nd Charlotte Plum (Ormond) 2nd Jemma Patullo (Ascot) 3rd Charlie Clark (Strathdale) 3rd Monique Heath (Donvale) HM Kaitlin Ryan (Strathfieldsaye) SECTION: MV339 19 years and under PERFORMANCE SHOWCASE SOLO RECITAL 1st Monique Heath (Donvale) 2nd Charlotte Plum (Ormond) 3rd Jemma Patullo (Ascot) 3rd Liv Brereton (Epsom) HM Kaitlin Ryan (Strathfieldsaye) HM Sebastian-Jon Mathieson (Bunbartha) 2/06/2018 Evening Commences at 7:00 PM MODERN VOCAL COMPETITION SECTION: -

Demographic Profile of Young People in Greater Bendigo

Attachment 4 DEMOGRAPHIC PROFILE OF YOUNG PEOPLE IN GREATER BENDIGO 2017 1 Acknowledgement of Country The City of Greater Bendigo is on both Dja Dja Wurrung and Taungurung Country, whose ancestors and their descendants are the traditional owners of this Country. We acknowledge that they have been custodians for many centuries and continue to perform age old ceremonies of celebration, initiation and renewal. We acknowledge their living culture and their unique role in the life of this region. Contact: City of Greater Bendigo 195 Lyttleton Terrace Bendigo Vic 3550 Telephone: (03) 5434 6000 Website: www.yobendigo.com.au 2 CONTENTS CONTENTS .................................................................................................................................... 3 TABLES .......................................................................................................................................... 6 INTRODUCTION ............................................................................................................................ 8 DEMOGRAPHIC SNAPSHOT OF YOUNG PEOPLE IN GREATER BENDIGO .............................. 9 CITY OF GREATER BENDIGO POPULATION SUMMARY AND FORECASTS ........................... 11 Population ................................................................................................................................. 11 Population Forecasts ................................................................................................................. 11 Analysis .................................................................................................................................... -

List of Parishes in the State of Victoria

List of Parishes in the State of Victoria Showing the County, the Land District, and the Municipality in which each is situated. (extracted from Township and Parish Guide, Department of Crown Lands and Survey, 1955) Parish County Land District Municipality (Shire Unless Otherwise Stated) Acheron Anglesey Alexandra Alexandra Addington Talbot Ballaarat Ballaarat Adjie Benambra Beechworth Upper Murray Adzar Villiers Hamilton Mount Rouse Aire Polwarth Geelong Otway Albacutya Karkarooc; Mallee Dimboola Weeah Alberton East Buln Buln Melbourne Alberton Alberton West Buln Buln Melbourne Alberton Alexandra Anglesey Alexandra Alexandra Allambee East Buln Buln Melbourne Korumburra, Narracan, Woorayl Amherst Talbot St. Arnaud Talbot, Tullaroop Amphitheatre Gladstone; Ararat Lexton Kara Kara; Ripon Anakie Grant Geelong Corio Angahook Polwarth Geelong Corio Angora Dargo Omeo Omeo Annuello Karkarooc Mallee Swan Hill Annya Normanby Hamilton Portland Arapiles Lowan Horsham (P.M.) Arapiles Ararat Borung; Ararat Ararat (City); Ararat, Stawell Ripon Arcadia Moira Benalla Euroa, Goulburn, Shepparton Archdale Gladstone St. Arnaud Bet Bet Ardno Follett Hamilton Glenelg Ardonachie Normanby Hamilton Minhamite Areegra Borug Horsham (P.M.) Warracknabeal Argyle Grenville Ballaarat Grenville, Ripon Ascot Ripon; Ballaarat Ballaarat Talbot Ashens Borung Horsham Dunmunkle Audley Normanby Hamilton Dundas, Portland Avenel Anglesey; Seymour Goulburn, Seymour Delatite; Moira Avoca Gladstone; St. Arnaud Avoca Kara Kara Awonga Lowan Horsham Kowree Axedale Bendigo; Bendigo -

East Bendigo Local Structure Plan Final Report

East Bendigo Local Structure Plan Final Report ADOPTED – 19 JULY 2006 Maunsell Australia Pty Ltd Level 9, 161 Collins Street Melbourne Vic 3000 Australia Tel: +61 3 9653 1234 Fax: +61 3 9654 7117 Our Reference: 30018502 East Bendigo Local Structure Plan Final Report © Maunsell Australia Proprietary Limited 2003 The information contained in this document produced by Maunsell Australia Pty Ltd is solely for the use of the Client identified on the cover sheet for the purpose for which it has been prepared and Maunsell Australia Pty Ltd undertakes no duty to or accepts any responsibility to any third party who may rely upon this document. All rights reserved. No section or element of this document may be removed from this document, reproduced, electronically stored or transmitted in any form without the written permission of Maunsell Australia Pty Ltd. East Bendigo Local Structure Plan Adopted Final Report 19 July 2006 U:\Strategy\Landuse & Transport\Industrial Land Strategy 1\Local Structure Plan\Final Report\EBLSP Final Report- Adopted 19 July 2006.doc Page 2 of 97 Table of Contents Executive Summary 5 1 Introduction 8 1.1 Background and Impetus for Study 9 1.2 Aim of the Study 10 1.3 Study Area 11 2 Stakeholder Consultation 13 2.1 City of Greater Bendigo 14 2.2 State Government Agencies 14 2.3 Servicing Authorities 16 2.4 Business Owners, Operators and Real Estate Agencies 16 2.5 Other 17 3 Strategic Planning Context 18 3.1 Land Use Planning 19 3.1.1 State Planning Policy 19 3.1.2 Regional and Local Planning Polices 21 3.2 Transport Planning -

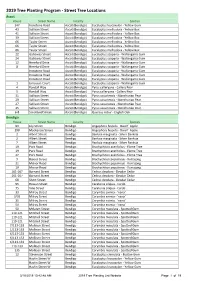

2019 Tree Planting List Website

2019 Tree Planting Program ‐ Street Tree Locations Ascot House Street Name Locality Species 147 Ironstone Road Ascot (Bendigo) Eucalyptus leucoxylon ‐ Yellow Gum 43 Sullivan Street Ascot (Bendigo) Eucalyptus melliodora ‐ Yellow Box 41 Sullivan Street Ascot (Bendigo) Eucalyptus melliodora ‐ Yellow Box 39 Sullivan Street Ascot (Bendigo) Eucalyptus melliodora ‐ Yellow Box 66 Taylor Street Ascot (Bendigo) Eucalyptus melliodora ‐ Yellow Box 66 Taylor Street Ascot (Bendigo) Eucalyptus melliodora ‐ Yellow Box 66 Taylor Street Ascot (Bendigo) Eucalyptus melliodora ‐ Yellow Box 22 Galloway Street Ascot (Bendigo) Eucalyptus scoparia ‐ Wallangarra Gum 24 Galloway Street Ascot (Bendigo) Eucalyptus scoparia ‐ Wallangarra Gum 12 Hereford Drive Ascot (Bendigo) Eucalyptus scoparia ‐ Wallangarra Gum 8 Hereford Drive Ascot (Bendigo) Eucalyptus scoparia ‐ Wallangarra Gum Ironstone Road Ascot (Bendigo) Eucalyptus scoparia ‐ Wallangarra Gum Ironstone Road Ascot (Bendigo) Eucalyptus scoparia ‐ Wallangarra Gum Ironstone Road Ascot (Bendigo) Eucalyptus scoparia ‐ Wallangarra Gum 1 Limousin Court Ascot (Bendigo) Eucalyptus scoparia ‐ Wallangarra Gum 4 Randall Way Ascot (Bendigo) Pyrus calleryana ‐ Callery Pear 5 Randall Way Ascot (Bendigo) Pyrus calleryana ‐ Callery Pear 31 Sullivan Street Ascot (Bendigo) Pyrus ussuriensis ‐ Manchurian Pear 29 Sullivan Street Ascot (Bendigo) Pyrus ussuriensis ‐ Manchurian Pear 27 Sullivan Street Ascot (Bendigo) Pyrus ussuriensis ‐ Manchurian Pear 25 Sullivan Street Ascot (Bendigo) Pyrus ussuriensis ‐ Manchurian Pear 6‐8 Strickland -

WHITE HILLS and EAST BENDIGO HERITAGE STUDY 2016 Vol

WHITE HILLS AND EAST BENDIGO HERITAGE STUDY 2016 Vol. 2: Place and precinct citations Adopted by Council 15 November 2017 Prepared for City of Greater Bendigo WHITE HILLS AND EAST BENDIGO HERITAGE STUDY 2016 ii CITY OF GREATER BENDIGO Context Pty Ltd 2015 Project Team: Louise Honman, Director Ian Travers, Senior Heritage Consultant Catherine McLay, Heritage Consultant Jessie Briggs Report Register This report register documents the development and issue of the report entitled 1962 undertaken by Context Pty Ltd in accordance with our internal quality management system. Project Issue Notes/description Issue Issued to No. No. Date 1962 1 Draft citations 31/08/2015 Dannielle Orr 1962 2 Final draft citations 03/11/2015 Dannielle Orr 1962 3 Final citations 12/2/2016 Dannielle Orr 1962 4 Final citations 27/4/2016 Dannielle Orr 1962 5 Final citations adopted by City of 21/12/2017 Morgan James Greater Bendigo Context Pty Ltd 22 Merri Street, Brunswick VIC 3056 Phone 03 9380 6933 Facsimile 03 9380 4066 Email [email protected] Web www.contextpl.com.au 3 WHITE HILLS AND EAST BENDIGO HERITAGE STUDY 2016 4 CITY OF GREATER BENDIGO CONTENTS BRIDGE STREET NORTH PRECINCT 6 BULLER STREET PRECINCT 15 GLEESON STREET PRECINCT 22 NORFOLK STREET PRECINCT 29 WHITE HILLS PRECINCT 36 BAXTER STREET PRECINCT EXTENSION 45 TOMLINS STREET PRECINCT EXTENSION 53 8 BAKEWELL STREET, BENDIGO NORTH 60 105 BAXTER STREET, BENDIGO 63 80 NOLAN STREET, BENDIGO 66 POTTERS’ ARMS, 48-56 TAYLOR STREET, ASCOT 68 147 BARNARD STREET, BENDIGO 71 FORMER NORFOLK BREWERY, 3 BAYNE -

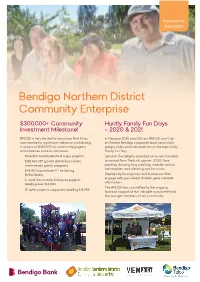

2020-21 Newsletter

Newsletter 2020/2021 Bendigo Northern District Community Enterprise $300,000+ Community Huntly Family Fun Days Investment Milestone! – 2020 & 2021 BNDCE is very excited to announce that it has In February 2020 and 2021 our BNDCE and City now reached a significant milestone contributing of Greater Bendigo supported local community in excess of $300,000 to community projects groups, clubs and individuals to run the free Huntly and initiatives since its formation. Family Fun Day. • $104,200 contributed to 8 major projects Some of the delights provided at no cost included • $138,565 (127 grants) distributed via the an animal farm, firetruck, games, LEGO, face twice-yearly grants programs painting, dancing, bug catching, wooden animal construction, rock climbing and live music. • $43,150 to purchase 21 Life Saving Defibrillators Displays by local groups and businesses that engage with pre-school children gave valuable • 6 Joint Community Enterprise projects information. totalling over $14,000 The BNDCE has committed to the ongoing • 27 other projects supported totalling $12,059. financial support of this valuable annual event for the younger members of our community. Community Investment Grants More shady days for Huntly North Epsom Cricket Club Funds for the community investment grants Juniors program are generated through customers The junior cricket club had purchased club apparel and linking their banking and phone business equipment for junior teams. The balance of the grant (held with Bendigo Bank and Bendigo Telco) was used to purchase a new SunSmart shade marquee to protect juniors on game days. The total funds to the community enterprise and the Bank granted was $2,500. -

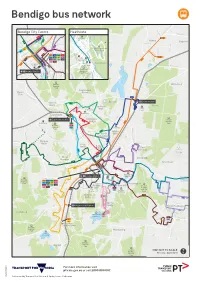

Bendigo-Bus-Network-Map.Pdf

Bendigo bus network d R n o s y n n B e o -T © r o o ig n d Bendigo City Centre Heathcote i n Greater Bendigo a e Mid R B land Hw H y National Park d C e V y o a d o i R t e t w n s w h o t M S H t Golf Course M c e S t e s o S d r t n le c g f y t l a r Iv i B k d l C e r a e W ea i d o Huntly r i h a B r l N Bagshot a n l d B M C H d t d o t w Sa t i S w R wmi d l g Lan e r ll Rd e o rd se d t ll S y l R S - a Woodvalet l h n C S d t aPr h t I B y a © o ronb r t p o ark a S e d m ll l N Heathcote-Graytown w M r a M S c t R Rd id Ivo o S t r e l M u Rd rt y t R National Park W h al n h e s d d t e c a a S P y r n r Whipstick S E a t S n u t a t S M t Bendigo City Centre - H h a ie t e w t h z t C i n it S o y R c P e c rs th Rd d cK h e ea n a e y H eto n M ll M yn W K t t Cemetery § k S S ac h t rr S a E ig Primary School B n a H M e L g e y e n Rd ® ans Rd u l r e t Q S eto l W h e t yn Heathcote Heathcote a S Shopping il K t l ck w ia Ba Hospital Huntly-F Centre k o m M sterville s - Rd c m o © N n I v S C e t o t o i n Rushworth l N r S d b o t o n t o i n Heathcote r AD S r l S S t Bendigo Station o t t h C © r v t e u a S State Forest e r e l S e l R g r t t H i e u e n Bendigo S n l h n v d k e s i r a t s e R n R H e r y o e e wRegional p s t l d u l r y s N d m w S r d a C i Park a t o H l Heathcote to Bendigo C H G S d © n a l d © Rushworth i Bendigo Heathcote M Wellsford Regional State Forest d R Park n w t o d S a Eaglehawk n n r a o Myers i B Lo North t - d a m Flat do t so n S p Va E lle -

Parish and Township Plan Numbers

Parish and Township plan numbers This is a complete list of Victorian parishes and townships, together with plan numbers assigned by the Victorian Department of Crown Lands and Survey at some point between 1950 and 1970. The list has been reproduced from the Vicmap Reference Tables on the Department of Sustainability and Environment's land information website. Browse the list or use a keyword search to identify the plan number/s for a location. The plans are listed alphabetically. Townships and parishes are inter-sorted on the list. Some entries refer to locations within parishes or townships; these entries may be duplicated. The plan number can be used to locate copies of plans that PROV holds in the series VPRS 16171 Regional Land Office Plans Digitised Reference Set. For example, using the Search within a Series page on the PROV online catalogue with series number '16171' and the text '5030' will return the specific plans relating to the township of Ballarat. In this case, searching for 'Ballaarat' by name will return al the plans in the Ballarat land district, covering much of central and western Victoria. PROV does not hold copies of plans for the locations highlighted in pale yellow below. In most cases this is because parish-level plans were not created for areas such as national parks, where there were few land transactions to record. Plans showing these locations can be downloaded from the landata website under the section 'Central Plan Office Records'. 5001 Township of Aberfeldy 2016 Parish of Angora 2001 Parish of Acheron 2017 -

Serviced Properties 2019-2020

Notice of Declaration of Serviced Property Pursuant to section 144 of the Water Act 1989 (Vic), Coliban Water intends to declare the following land as serviced property for the services listed below. This land will become serviced property on the date that Coliban Water issues ‘Practical Completion’ for the reticulation asset works. WATER & SEWERAGE Development/Address Suburb/Town Lot Nos. PS No. Brangus Court & Galloway St ASCOT 1301-1306 824340F V02 Triplett Avenue ASCOT 1-2 812478R V1 Axe Creek Road Axe Creek 1-5 839464C V01 Axe Creek Road Axe Creek 1-2 837075A V02 Emu Creek Road Axe Creek 1-2 831392U V01 Gleesons Road Axe Creek 1-2 831356Y V02 Peatlings Road BAGSHOT 1-2 837074C V01 Sherwood Road BAGSHOT 101 - 130 815341E V3 Carrs Rd BARKERS CREEK 1-2 829316A V2 Midland Hwy BARKERS CREEK 838385D V1 1 & 6 Barry Street BENDIGO 1-2 824236A V1 314 Lyttleton Terrace & 25 Queen Street BENDIGO 1-2 831844K V02 93 Rowan Street and 71 Vine Street BENDIGO 1-2 828559C V02 Barnard Street BENDIGO 1-2 807937P V01 Forest Street BENDIGO 1-3 815358L V01 Hargreaves Street BENDIGO 1-2 824345U V02 Hargreaves Street BENDIGO 1 - 2 810194S V1 MacKenzie Street BENDIGO 1 & 2 815344X V3 McCrae Street BENDIGO 1-2 834207B V04 Mill Street BENDIGO 1 & 2 824234E V2 Milroy Street BENDIGO 1 & 2 815343A V1 Camp Street BRIDGEWATER 1-2 830956D V01 Park Street BRIDGEWATER 1-5 743229W V1 Brown Street CALIFORNIA GULLY 1-2 812504T V1 Christian Street CALIFORNIA GULLY 1-2 814340M V1 Dowding Street CALIFORNIA GULLY 1 & 2 831383V V2 Evans Street CALIFORNIA GULLY 1-2 822817P