Miami Office Market Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Brickell Retail/Restaurant Spaces Available Contact Us

Brickell Retail/Restaurant Spaces Available Contact us: BRICKELL ARCH | 1395 BRICKELL AVENUE | MIAMI, FL 33131 Jonathan Carter Executive Managing Director Colliers International is pleased to offer the opportunity to lease retail/ +1 786 517 4971 restaurant spaces on the ground floor of Brickell Arch, a 36-story [email protected] mixed-use project that features over 268,000 SF of class “A” office space and the 203-room Conrad Hotel. Jenny Gefen Director +1 786 517 4974 FEATURES [email protected] • Adjacent to JW Marriott Hotels and The Four Seasons Kirk Fetter • 980 car attached parking garage with on-site valet +1 786 999 8003 • Large outdoor seating area and lobby courtyard access [email protected] AVAILABILITY SPACE 1 SPACE 2 SPACE 3 Colliers International ± ± ± South Florida, LLC 4,538 SF 758 SF 2,594 SF 801 Brickell Avenue, Suite 850 Miami, FL 33131 GROUND FLOOR SPACE 1 ±4,538 SF SW 14TH STREET Jonathan Carter Jenny Gefen Kirk Fetter Executive Managing Director Director +1 786 999 8003 +1 786 517 4971 +1 786 517 4974 [email protected] [email protected] [email protected] Outdoor Patio Small Brickell Retail/Restaurant Spaces Available GROUND FLOOR VALET Space 1: ± 758 SF Space 2: ± 2,594 SF Lobby Total: 3,352 SF Brickell Avenue ± BRICKELL AVENUE BRICKELL Situated on the ground floor of Brickell Arch and supported by the Conrad Hotel, a 36 story mixed-use tower with over 268,000 SF of class “A” office space and 203 hotel rooms SPACE 3 SPACE 2 ±2,594 SF 980 car attached parking garage with on- ±±758 -

Macy's Redevelopment Site Investment Opportunity

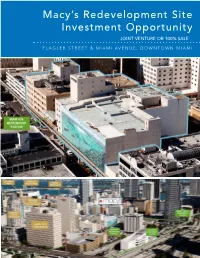

Macy’s Redevelopment Site Investment Opportunity JOINT VENTURE OR 100% SALE FLAGLER STREET & MIAMI AVENUE, DOWNTOWN MIAMI CLAUDE PEPPER FEDERAL BUILDING TABLE OF CONTENTS EXECUTIVE SUMMARY 3 PROPERTY DESCRIPTION 13 CENTRAL BUSINESS DISTRICT OVERVIEW 24 MARKET OVERVIEW 42 ZONING AND DEVELOPMENT 57 DEVELOPMENT SCENARIO 64 FINANCIAL OVERVIEW 68 LEASE ABSTRACT 71 FOR MORE INFORMATION, CONTACT: PRIMARY CONTACT: ADDITIONAL CONTACT: JOHN F. BELL MARIANO PEREZ Managing Director Senior Associate [email protected] [email protected] Direct: 305.808.7820 Direct: 305.808.7314 Cell: 305.798.7438 Cell: 305.542.2700 100 SE 2ND STREET, SUITE 3100 MIAMI, FLORIDA 33131 305.961.2223 www.transwestern.com/miami NO WARRANTY OR REPRESENTATION, EXPRESS OR IMPLIED, IS MADE AS TO THE ACCURACY OF THE INFORMATION CONTAINED HEREIN, AND SAME IS SUBMITTED SUBJECT TO OMISSIONS, CHANGE OF PRICE, RENTAL OR OTHER CONDITION, WITHOUT NOTICE, AND TO ANY LISTING CONDITIONS, IMPOSED BY THE OWNER. EXECUTIVE SUMMARY MACY’S SITE MIAMI, FLORIDA EXECUTIVE SUMMARY Downtown Miami CBD Redevelopment Opportunity - JV or 100% Sale Residential/Office/Hotel /Retail Development Allowed POTENTIAL FOR UNIT SALES IN EXCESS OF $985 MILLION The Macy’s Site represents 1.79 acres of prime development MACY’S PROJECT land situated on two parcels located at the Main and Main Price Unpriced center of Downtown Miami, the intersection of Flagler Street 22 E. Flagler St. 332,920 SF and Miami Avenue. Macy’s currently has a store on the site, Size encompassing 522,965 square feet of commercial space at 8 W. Flagler St. 189,945 SF 8 West Flagler Street (“West Building”) and 22 East Flagler Total Project 522,865 SF Street (“Store Building”) that are collectively referred to as the 22 E. -

Miami Office Space Can Be Found by Those Who Search February 7, 2017 By: Carla Vianna

Miami Office Space Can Be Found by Those Who Search February 7, 2017 By: Carla Vianna Businesses searching for space in Miami's urban core have more options than they might think. While vacancy rates are down across the board, significant chunks of space are available in several Class A buildings in downtown and the Brickell Avenue financial district. "There are more alternatives available for those companies that take the time to appropriately investigate the market," said Chris Lovell, a senior managing director with Savills Studley in Miami. Leasing space on an upper floor with a view may be difficult since only six buildings on Brickell have a full floor above the 20th story available for lease. For tenants that can live without the view, there is plenty of open space to choose from. Four downtown Class A buildings have at least 75,000 square feet of contiguous space available, one Class A building on Brickell has a 65,000- square-foot block — "and we don't have tenants of that size standing in line to the claim the space," Lovell said. Savills Studley has found many of the large available blocks are in older downtown buildings. "You're always going to have buildings that are going to have certain pockets available," said Tere Blanca, founder of Miami-based Blanca Commercial Real Estate Inc. She said the market is responding well to the new Miami Central project, which is under construction with 60 percent of its office component pre- leased. The mixed-use development will serve as Brightline's downtown train station and will add 286,000 square feet of office space in two buildings. -

OFFERING MEMORANDUM Miami, FL 33131 235 SE 1St Street Themiamiplaza.Com

THE P LA ZA themiamiplaza.com MEMORANDUM 235 SE 1st Street Miami, FL 33131 OFFERING THE P LA ZA THE P LA ZA 235 SE 1st Street THE OFFERING Miami, FL 33131 he Plaza is a 81,000 SF office building Ton a 20,000 SF corner lot located in the heart of Downtown Miami and its most prominent corner. The site benefits from the most liberal mixed-use zoning in all of South Florida, T6-80-O, allowing up to 489,600 SF of development and 470 residential units. The Plaza is an amazing add value office building with tremendous future uses for development. Developers will benefit from the ability to receive temporary cash flow while waiting on the next cycle or plan approval. THE CORNER OF DOWNTOWN MIAMI THE P LA ZA PROPERTY SUMMARY + + Address: Lot Size: Building Size: Zoning: FLR Allowable FLR Allowable +Bonus Building Height: Building Height +Bonus: Allowable Units: Folio: 235 SE 1st St. 20,400/ 81,382 SF T6-80-O 489,600 SF Unlimited 80 Unlimited 470 01-0112-000-1020 Miami, FL 33131 0.47 Acres 6 7 FOUR SEASONS BRICKELL CITY INVESTMENT CENTRE ICON BRICKELL HIGHLIGHTS SOUTHEAST FINANCIAL CENTER WELLS FARGO CENTER MIAMI TOWER ASTON MARTIN JAMES L. KNIGHT RESIDENCES CENTER MET SQUARE CINEPLEX WHOLE FOODS CENTRO Covered Land with In-Place Income he Plaza is a prime opportunity to repurpose or add value to an existing Tclass C office building located in Downtown’s most highly trafficked corridor. The property is positioned to capture an already active-large tenant base with over 175,000 employees existing within Downtown’s LA EPOCA Central Business District. -

Miami Cbd Large Blocks of Office Space

RESEARCH MIAMI CBD AUGUST 2019 LARGE BLOCKS OF OFFICE SPACE 836 MACARTHUR CAUSEWAY 100,000+ SF Blocks 395 Southeast Financial Center Four Seasons Tower 200 S Biscayne Boulevard 1441 Brickell Avenue Ponte Gadea USA 9 Millennium Partners Management 1 1,225,000 RBA – 67.8% Leased 258,767 RBA – 98.1% Leased 133,120 SF Max Contig. 28,763 SF Max Contig. $53.25/RSF FS $60.00/RSF FS Citigroup Center 1221 Brickell 201 S Biscayne Boulevard 1221 Brickell Avenue Crocker Partners Rockpoint Group 2 809,594 RBA – 74.0% Leased 10 408,649 RBA – 86.1% Leased 95 127,634 SF Max Contig. 26,761 SF Max Contig. $48.00-$52.00/RSF FS $52.50/RSF FS Freedom PORT BLVD A1A Tower Wells Fargo Center 50,000 - 99,999 SF Blocks 333 SE 2nd Avenue AVE MetLife Real Estate Investments AVE 11 ND 752,845 RBA – 85.9% Leased ND SunTrust International Center 26,000 SF Max Contig. 1 SE 3rd Avenue BISCAYNE BLVD BISCAYNE $48.00/RSF FS N MIAMI AVE MIAMI N 2 NE NW 2 NW MiaMarina Pacific Coast Capital Partners MIAMI RIVER 3 440,299 RBA – 66.4% Leased 90,255 SF Max Contig. $38.00-$40.00/RSF FS 15,000 - 24,999 SF Blocks Brickell Office Plaza Brickell World Plaza Downtown 777 Brickell Avenue 600 Brickell Avenue 8 Padua Realty Company Elm Spring, Inc. 4 288,457 RBA – 74.8% Leased 12 631,866 RBA – 92.5% Leased 3 6 68,386 SF Max Contig. CLASS 24,138 SF Max Contig. -

Echo Brickell

ECHO BRICKELL ECHO BRICKELL Call: +1.786.383.1553 Call: +1.786.383.1553 ORAL REPRESENTATIONS CANNOT BE RELIED UPON AS CORRECTLY STATING REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. OBTAIN THE PROPERTY REPORT REQUIRED BY FEDERAL LAW AND READ IT BEFORE SIGNING ANYTHING. NO FEDERAL AGENCY HAS JUDGED THE MERITS OR VALUE , IF ANY, OF THIS PROPERTY . EAST/SOUTHEAST VIEW VIEWS ACTUAL VIEWS MAY VARY AND CANNOT BE GUARANTEED. VIEWS SHOWN CANNOT BE RELIED UPON AS THE ACTUAL VIEW FROM ANY PARTICULAR UNIT WITHIN THE CONDOMINIUM. ORAL REPRESENTATIONS CAN- NOT BE RELIED UPON AS CORRECTLY STATING REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. OBTAIN THE PROPERTY REPORT REQUIRED BY FEDERAL LAW AND READ IT BEFORE SIGNING ANYTHING. NO FEDERAL AGENCY HAS JUDGED THE MERITS OR VALUE, IF ANY, OF THIS PROPERTY. OVERVIEW ECHO Brickell is a boutique residential high-rise in the epicenter of Miami’s fastest growing metropolitan neighborhood, located on the coveted East side of Brickell Avenue. Echo Brickell’s 157 state-of-the-art residences redefine opulent living in Miami’s most exciting locale. With conceptual design from mastermind Carlos Ott, ECHO Brickell is a host of privilege at every turn. Echo Brickell’s interiors introduce an exciting new concept to the world - fusing world renowned architect, Carlos Ott and yoo design studio, in a first time collaboration to create a limited edition collection: Carlos Ott + yoo . -

Vice 300 Biscayne Boulevard

DOWNTOWN MIAMI FL VICE 300 BISCAYNE BOULEVARD CONCEPTUAL RENDERING SPACE DETAILS LOCATION GROUND FLOOR West block of Biscayne Boulevard between NE 3rd and NE 4th Streets NE 4TH STREET 38 FT SPACE Ground Floor 1,082 SF FRONTAGE 38 FT on NE 4th Street 1,082 SF TERM Negotiable (COMING SOON) POSSESION LEASE OUT Summer 2018 SITE STATUS New construction LEASE OUT CO-TENANTS Caffe Fiorino (coming soon), GOGO Fresh Foods (coming soon) and OXXO Care Cleaners (coming soon) NEIGHBORS Area 31, Fratelli Milano, CVI.CHE 105, Gap, Il Gabbiano, Juan Valdez Coffee, NIU Kitchen, Pollos & Jarras, Segafredo, Skechers, Starbucks, STK Miami, Subway, Ten Fruits, Toro Toro, Tuyo Restaurant, Victoria’s Secret, Wolfgang’s Steakhouse and Zuma COMMENTS VICE is a 464-unit apartment tower under construction in the heart of Downtown Miami Directly across from Bayside Marketplace and neighboring Miami Dade College, two blocks from American Airlines Arena, and adjacent to the College-Bayside Metromover Station Miami-Dade College has over 25,000 students on campus daily (COMING SOON) (COMING SOON) ADDITIONAL RENDERINGS CONCEPTUAL RENDERING CONCEPTUAL RENDERING CONCEPTUAL RENDERING Downtown Miami & Brickell Miami, FL AREASeptember 2017 RETAIL NW 8TH STREET NE 8TH STREET VICE AVENUE 300 BISCAYNE NE 7TH STREET NE 2ND HEAT BOULEVARD BOULEVARD MIAMI FL FREEDOM TOWER NW 6TH STREET PORT BOULEVARD MIAMI-DADE COLLEGE FACULTY Downtown Miami PARKING Movers NW 5TH STREET NE 5TH STREET 300 BISCAYNE BOULEVARDP MIAMI-DADE COLLEGE FEDERAL NE 4TH STREET NE -

Miami DDA Area Offices

NE 28th St NE 27th Te NW 28th St NE 27th St NW 27th St NE 26th Te No. Class Name Address Year RBA 1 A 10 Museum Park 1040 Biscayne Blvd 2007 24,000 \ NW 26th St NE 26th St 2 A 900 Biscayne Bay 900 Biscayne Blvd 2008 95,000 3 A Marina Blue 888 Biscayne Blvd 2008 750,000 4 B NAP of the Americas 50 NE 9th ST 2001 750,000 NW 25th St NE 25th St 5 A 2 MiamiCentral 601 NW 1st Ave 2018 190,000 NE 24th St 6 A 3 MiamiCentral 161 NW 6th ST 2018 95,000 NW 24th St NW 24th St NE 24th St 7 B The Citadel 49 NW 5th ST 1950 50,000 8 B Courthouse Center 40 NW 3rd ST 2009 40,300 NW 23rd St NW 23rd St 9 B 36 NE 2nd ST 36 NE 2nd ST 1925 205,172 10 B Chase Bank Building 150 SE 2nd Ave 1966 125,388 NE 23rd St NE 22nd Te 11 B Bayside Office Center 141 NE 3rd Ave 1923 57,093 12 B 261 Office Lofts 261 NE 1st ST 1982 34,741 NE 22nd St 13 B New World Tower 100 N Biscayne Blvd 1966 285,000 NW 22nd St Ave 2nd NE 14 C Capital Building 117 NE 1st Ave 1926 85,000 15 C Congress Building 111 NE 2nd Ave 1922 242,294 NE 21st St Dade Commonwealth 16 B Building 139 NE 1st ST 1927 43,265 17 B One Bayfront Plaza 100 S Biscayne Blvd 1959 312,896 BISCAYNE BOULEVARD BISCAYNE Flagler Federal NE 20th St 18 B Building 101-111 NE 1st ST 1961 64,470 N MIAMI AVE MIAMI N NW Miami Ct Miami NW NW 1st Ave 1st NW NW 2nd Ave 2nd NW NE 19th Te NW 1st Ct 1st NW NW 20th St Pl 1st NW 19 B Historic Post Office 100 NE 1st Ave 1912 37,600 20 B Metromall Building 1 Ne 1st ST 1926 156,000 NE 19th St 21 C 219-223 E Flagler ST 219-223 E Flagler ST 1984 42,000 22 B A.I. -

MIAMI TOWER | CLASS A, CORE OFFICE TOWER 100 SE 2Nd Street, Miami, Florida 33131

MIAMI TOWER | CLASS A, CORE OFFICE TOWER 100 SE 2nd Street, Miami, Florida 33131 Transwestern is pleased to exclusively offer the opportunity to lease office space within Miami Tower, a landmark on the Miami skyline and one of the nation’s most iconic office towers. PENTHOUSE Consisting of 15,418 square feet on the 46th and 47th floors. This space offers the most discerning tenant the privacy and exclusivity of penthouse space on a low square footage floorplate. PANORAMIC WATER & CITY VIEWS Miami Tower is one of the tallest skyscrapers in Downtown Miami. Tenants enjoy unparalleled water and city views that are enhanced by the building’s curvilinear architectural design, which provides abundant natural light and maximizes the window line. FLOOR SIZES The building was designed with three distinct tiers, each one slightly set back from the one below. The FACTS & STATS low-rise offers 22,000 square foot floorplates, the 47 stories (625’ tall), consisting of 37 floors of mid-rise offers 18,000 square foot floorplates and office space constructed above 10 floors of the high-rise offers 14,000 square foot floorplates. parking, street level retail pedestal, and an 11th floor Sky Lobby and expansive Sky Terrace. 619,093 SF of Class A office & retail space. CEILING HEIGHTS Finished ceiling heights are 8 feet 6 inches with floor-to-floor ceiling heights of 12 feet. The Sky RESPONSIBLE Lobby has a height of 20 feet 4 inches, and the Miami Tower is LEED® Silver certified as well ground floor lobby has a height of 12 feet 2 inches. -

2020: the New Miami

MIAMI REPORT AN IN-DEPTH ANALYSIS OF SOUTH FLORIDA’S NEW CONDOMINIUM MARKET 2020 NEWTHE MIAMI “MIAMI IS ENTERING A NEW GOLDEN AGE OF GROWTH.” - ISG PRINCIPALS PHOTOGRAPH BY GLEASON WAITE ROMER MIAMI, FL | CIRCA 1950 WEALTH REPORT THE CITIES THAT MATTER TO HNWI’S - GLOBAL SURVEY MOST IMPORTANT NOW AS SEEN IN London 1New York 2 THE WEALTH REPORT REPORT THE WEALTH 3 Singapore Hong Kong A GLOBAL PERSPECTIVE ON PRIME PROPERTY AND WEALTH AND WEALTH ON PRIME PROPERTY PERSPECTIVE A GLOBAL 4 Geneva 5 Shanghai6 7 Dubai Miami THE GLoBAL PERSPECTIVE oN PRIME PRoPERTy AND WEALTH 8 Paris WWW.THEWEALTHREPORT.NET 9 Beijing10 HNWI – High Net Worth Individuals US $30 MIL + NEW CONSTRUCTION PIPELINE AS OF FEBRUARY 2014 BRICKELL TOTAL NEW CONSTRUCTION CONDO UNITS AVAILABLE FOR SALE SINCE JAN. 2012 DeveloperDEVELOPER Units UNITSSold SOLD DEVELOPER UNITSDeveloper UNSOLD Units Unsold 1010 Brickell 50% SOLD 900 BRICKELL 352 UNITS Bond 60% SOLD BRICKELL 323 UNITS Brickell CityCentre I & II 820 UNITS BRICKELL (release date TBD) 50% SOLD *Brickell Heights 358 UNITS BRICKELL Brickell House 100% SOLD 374 UNITS BRICKELL Echo Brickell 70% SOLD 180 UNITS BRICKELL 128 UNITS Le Parc 62% SOLD BRICKELL 390 UNITS Nine at Mary Brickell 55% SOLD BRICKELL 382 UNITS Millecento 100% SOLD BRICKELL 192 UNITS 100% SOLD MyBrickell BRICKELL 450 UNITS SLS Brickell 100% SOLD BRICKELL *Tower 1 only (other tower currently unavailable) 3,949 UNITS TOTAL • 2,367 UNITS SOLD • 1,581 UNSOLD AVG ABSORPTION : 1,900 UNITS ANNUALLY OVER THE LAST 10 YEARS BISCAYNE CORRIDOR DOWNTOWN MIAMI, EDGEWATER, MIDTOWN & DESIGN DISTRICT TOTAL NEW CONSTRUCTION CONDO UNITS AVAILABLE FOR SALE SINCE JAN. -

Location 400 S.E Second Ave Miami, Florida 33131 305.416.5970

Location 400 S.E Second Ave Miami, Florida 33131 305.416.5970 www.jlkc.com The complex is situated overlooking the Miami River at Brickell Avenue, just seven miles from Miami International Airport and two miles from the Port of Miami. Interstate 95 provides both north and southbound exits directly into the facility and the Hyatt Regency, as does the adjacent Knight Center Station that provides direct access to both the Downtown Metro Mover and Miami-Dade County's Metro rail rapid transit system. METRORAIL & METROMOVER Take Metrorail ($2) to Government Center station. Proceed to the Metromover (FREE), Inner Loop for the most direct route. Take the Omni line and get off at Knight Center. Down escalators take you to the Tower lobby. Turn right off the escalator and proceed to the Knight Center/Hyatt Regency via the air-conditioned, covered walkway. DRIVING DIRECTIONS Directions from North and South of Miami • Take I-95 North or South • Continue on I-95 (N or S) until EXIT 2-A (Biscayne Blvd.) • At the end of the exit ramp, there is a traffic light. • At traffic light, make a right hand turn onto South East 2nd Ave. • After making the right hand turn, make another quick right and the Hyatt Regency Miami will be on your left along with the James L Knight Center. Once on the hotel drive valet parking will be on your left. For self-parking, bear to the right and take the next right into the Knight Center/ Miami Tower garage. Parking elevators will take you to the Miami Tower lobby that is connected to the Knight Center/Hyatt Hotel by an air- conditioned, covered walkway. -

Downtown Miami Fully Approved Hotel Development Site

Downtown Miami Fully approved hotel development site NE 1st Street Confidential offering memorandum Downtown Miami | Hotel Development Site | 139 NE 1st Street, Miami, Florida Table of contents 01. Executive summary 3 02. Property overview 8 03. Market overview 25 04. Area overview 29 2 01. Executive summary Introduction Investment highlights Downtown Miami | Hotel Development Site 01. Introduction 139 NE 1st Street Miami, FL 33132 Avison Young is pleased to exclusively offer for sale the historic Dade Commonwealth Building (“the Property”), an existing office building and fully site plan approved hotel development site located in the heart of Downtown Miami, Florida. Permits have been approved to demolish the existing structure (with the exception of the façade for the first 3 stories), and permits for the construction of a17-story, 163-key hotel are pending approval, with approval expected in July of 2021. A hotel on the site would benefit from the excellent location of the Property, within short walking distance to some of Downtown Miami’s major office buildings, dining and nightlife spots and cultural attractions, offering the ability to cater to both business- and leisure-oriented travelers. The Property is located just 400 feet from the First Street MetroMover Station, which offers rail access throughout Downtown Miami and Brickell, and a short walk from the Government Center MetroRail Station, which offers rail access throughout Miami-Dade County. It is also located near some of Downtown Miami’s top-performing luxury hotels, including the Hyatt Regency, the Kimpton EPIC, the InterContinental Miami, the JW Marriott Marquis, and the Hotel Beaux Arts.