Beef Industry Study Released February 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Teaching of a Basic Meats Course

173 fZACHlNG A BASIC NEATS COURSZ BY OEWORSTRATlOW TECHNIQUES 0 A, We HULLINS .*...--..-*.-..*.*...*...........-.*-...UNIVERSITY OF MISSOURI I find myself in a very awkward situation. In the first place I am following a very noted person, Mr. Ken Warner on the program, who is an authority on teaching methods, and secondly, I am talking to a group of very competent teachers with much more experience in the teaching profession than I have had. However, I would like to present to you our method of teaching a basic meats course at Missouri. Later, we would welcome any comments or questions in the way of constructive criticism or otherwise that any of you might have. First, I would libe to give you an idea of the amount of class hours involved in our basic course and the objectives we have outlined. Our basic meat classes meet 3-2 hour periods per week. These periods are arranged for either a laboratory period or a lecture period, Bowever, in the past it has evolved around one lecture period and two laboratory periods. Our ob- jectives in the course are to familiarize the student with the livestock and meat industry relationships, i.e. live animal carcass comparison, slaughter- ing, cutting, curing and smoking? identification, selection, processing, dis- tribution, utilization of meat and meat products. As more and more subJect material became available in these areas, we found we did not have time to present the students with the subject matter and still do the amount of slaughtering and processing that had been done in the past. -

Beef Showmanship Parts of a Steer

Beef Showmanship Parts of a Steer Wholesale Cuts of a Market Steer Common Cattle Breeds Angus (English) Maine Anjou Charolaise Short Horn Hereford (English) Simmental Showmanship Terms/Questions Bull: an intact adult male Steer: a male castrated prior to development of secondary sexual characteristics Stag: a male castrated after development of secondary sexual characteristics Cow: a female that has given birth Heifer: a young female that has not yet given birth Calf: a young bovine animal Polled: a beef animal that naturally lacks horns 1. What is the feed conversion ratio for cattle? a. 7 lbs. feed/1 lb. gain 2. About what % of water will a calf drink of its body weight in cold weather? a. 8% …and in hot weather? a. 19% 2. What is the average daily weight gain of a market steer? a. 2.0 – 4 lbs./day 3. What is the approximate percent crude protein that growing cattle should be fed? a. 12 – 16% 4. What is the most common concentrate in beef rations? a. Corn 5. What are three examples of feed ingredients used as a protein source in a ration? a. Cottonseed meal, soybean meal, distillers grain brewers grain, corn gluten meal 6. Name two forage products used in a beef cattle ration: a. Alfalfa, hay, ground alfalfa, leaf meal, ground grass 7. What is the normal temperature of a cow? a. 101.0°F 8. The gestation period for a cow is…? a. 285 days (9 months, 7 days) 9. How many stomachs does a steer have? Name them. a. 4: Rumen, Omasum, Abomasum, and Reticulum 10. -

Meat: a Novel

University of New Hampshire University of New Hampshire Scholars' Repository Faculty Publications 2019 Meat: A Novel Sergey Belyaev Boris Pilnyak Ronald D. LeBlanc University of New Hampshire, [email protected] Follow this and additional works at: https://scholars.unh.edu/faculty_pubs Recommended Citation Belyaev, Sergey; Pilnyak, Boris; and LeBlanc, Ronald D., "Meat: A Novel" (2019). Faculty Publications. 650. https://scholars.unh.edu/faculty_pubs/650 This Book is brought to you for free and open access by University of New Hampshire Scholars' Repository. It has been accepted for inclusion in Faculty Publications by an authorized administrator of University of New Hampshire Scholars' Repository. For more information, please contact [email protected]. Sergey Belyaev and Boris Pilnyak Meat: A Novel Translated by Ronald D. LeBlanc Table of Contents Acknowledgments . III Note on Translation & Transliteration . IV Meat: A Novel: Text and Context . V Meat: A Novel: Part I . 1 Meat: A Novel: Part II . 56 Meat: A Novel: Part III . 98 Memorandum from the Authors . 157 II Acknowledgments I wish to thank the several friends and colleagues who provided me with assistance, advice, and support during the course of my work on this translation project, especially those who helped me to identify some of the exotic culinary items that are mentioned in the opening section of Part I. They include Lynn Visson, Darra Goldstein, Joyce Toomre, and Viktor Konstantinovich Lanchikov. Valuable translation help with tricky grammatical constructions and idiomatic expressions was provided by Dwight and Liya Roesch, both while they were in Moscow serving as interpreters for the State Department and since their return stateside. -

Our Product List Our Product List at a Glance at a Glance

385352 Product List v8_Layout 1 7/10/13 3:20 PM Page 1 385352 Product List v8_Layout 1 7/10/13 3:20 PM Page 1 OUR PRODUCT LIST OUR PRODUCT LIST AT A GLANCE AT A GLANCE FRESH CUT BEEF Pork Loin Chops BACON FRESH CUT BEEF Pork Loin Chops BACON Beef Tenderloin Thick Cut Pork Loin Chops *Hickory Smoked Bacon Beef Tenderloin Thick Cut Pork Loin Chops *Hickory Smoked Bacon Ribeye Steak Center Cut Pork Loin Chops *Pepper Bacon Ribeye Steak Center Cut Pork Loin Chops *Pepper Bacon Porterhouse Steak Boneless Pork Chops *Beef Bacon Porterhouse Steak Boneless Pork Chops *Beef Bacon Chuckeye Steak Pork Loin Back Ribs *Homestyle Cottage Bacon Chuckeye Steak Pork Loin Back Ribs *Homestyle Cottage Bacon T-Bone Steak Pork Liver *Thick Sliced Bacon T-Bone Steak Pork Liver *Thick Sliced Bacon New York Strip Steak Lard *Apple Cinnamon Bacon New York Strip Steak Lard *Apple Cinnamon Bacon Sirloin Steak Boneless Boston Butts *Raspberry Chipotle Bacon Sirloin Steak Boneless Boston Butts *Raspberry Chipotle Bacon Beef Brisket Fresh Bone-In Ham Roast *Honey Glazed Bacon Beef Brisket Fresh Bone-In Ham Roast *Honey Glazed Bacon Boneless Prime Rib Roast Country-Style Pork Ribs *Maple Bacon Boneless Prime Rib Roast Country-Style Pork Ribs *Maple Bacon Flank Steak *Pulled Pork w/Sauce Flank Steak *Pulled Pork w/Sauce Boneless Beef Roast *Stuffed Pork Chops SMOKED SAUSAGES Boneless Beef Roast *Stuffed Pork Chops SMOKED SAUSAGES Oxtail *Smoked Center Cut Chops **Grand Champion Bratwurst Oxtail *Smoked Center Cut Chops **Grand Champion Bratwurst Soup Bones Smokehouse -

Report Name: Livestock and Products Semi-Annual

Required Report: Required - Public Distribution Date: March 06,2020 Report Number: AR2020-0007 Report Name: Livestock and Products Semi-annual Country: Argentina Post: Buenos Aires Report Category: Livestock and Products Prepared By: Kenneth Joseph Approved By: Melinda Meador Report Highlights: Argentine beef exports in 2020 are projected down at 640,000 tons carcass weight equivalent as lower prices and animal and human health issues generate negative trade dynamics. Lower exports will be reflected in marginal growth expansion of the domestic market in 2020. FAS/USDA has changed the conversion rates for Argentine beef exports. THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Conversion Rates: Due to continuing efforts to improve data reliability, the “New Post” trade forecasts reflect new conversion rates. Historical data revisions (from 2005 onward) will be published on April 9th in the Production, Supply and Demand (PSD) database (http://www.fas.usda.gov/psdonline). Beef and Veal Conversion Factors Code Description Conversion Rate* 020110 Bovine carcasses and half carcasses, fresh or chilled 1.0 020120 Bovine cuts bone in, fresh or chilled 1.0 020130 Bovine cuts boneless, fresh or chilled 1.36 020210 Bovine carcasses and half carcasses, frozen 1.0 020220 Bovine cuts bone in, frozen 1.0 020230 Bovine cuts boneless, frozen 1.36 021020 Bovine meat salted, dried or smoked 1.74 160250 Bovine meat, offal nes, not livers, prepared/preserve 1.79 -

Plant-Based Meat Mind Maps

PLANT-BASED MEAT MIND MAPS: AN EXPLORATION OF OPTIONS, IDEAS, AND INDUSTRY Christie Lagally Senior Scientist, The Good Food Institute Erin Rees Clayton, Ph.D. Scientifc Foundations Liaison, The Good Food Institute Liz Specht, Ph.D. Senior Scientist, The Good Food Institute SEPTEMBER 25, 2017 GFI is a 501(c)(3) nonproft working to create a healthy, humane, and sustainable food supply. GFI is committed to democratizing scientifc information that will help move our food system away from factory farming and toward better alternatives. I. AN INTRODUCTION TO MIND MAPS: CONCEPTUALIZING GROWTH OPPORTUNITIES A mind map provides a visual representation of critical technologies in an emerging industry to identify gaps in research and development as well as opportunities for strategic industry partnerships. This paper presents established, emerging, and speculative opportunities for plant-based meat sourcing, creation, processing, and distribution through two schematics: the plant-based meat product mind map, which surveys the types of meat analogues that have the potential to replace meat; and the plant-based meat technology mind map, which outlines areas of research and innovation that will accelerate the sector’s ability to compete for market share of the meat industry. The end goal of producing more and better plant-based meat products is to decrease consumption of animal meat products at all levels of quality and price, from steaks to processed meat. Therefore, some of the opportunities and recommendations presented here may apply to only certain types of products or manufacturing methods. For replacement to be successful, in addition to the scientifc and technological opportunities discussed below, we must consider the nutritional profles of various types of plant-based meat and their comparability to the animal products they are designed to replace. -

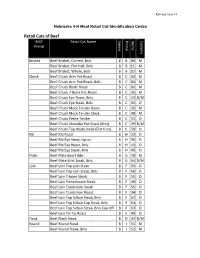

Retail Cuts of Beef BEEF Retail Cut Name Specie Primal Name Cookery Primal

Revised June 14 Nebraska 4-H Meat Retail Cut Identification Codes Retail Cuts of Beef BEEF Retail Cut Name Specie Primal Name Cookery Primal Brisket Beef Brisket, Corned, Bnls B B 89 M Beef Brisket, Flat Half, Bnls B B 15 M Beef Brisket, Whole, Bnls B B 10 M Chuck Beef Chuck Arm Pot-Roast B C 03 M Beef Chuck Arm Pot-Roast, Bnls B C 04 M Beef Chuck Blade Roast B C 06 M Beef Chuck 7-Bone Pot-Roast B C 26 M Beef Chuck Eye Roast, Bnls B C 13 D/M Beef Chuck Eye Steak, Bnls B C 45 D Beef Chuck Mock Tender Roast B C 20 M Beef Chuck Mock Tender Steak B C 48 M Beef Chuck Petite Tender B C 21 D Beef Chuck Shoulder Pot Roast (Bnls) B C 29 D/M Beef Chuck Top Blade Steak (Flat Iron) B C 58 D Rib Beef Rib Roast B H 22 D Beef Rib Eye Steak, Lip-on B H 50 D Beef Rib Eye Roast, Bnls B H 13 D Beef Rib Eye Steak, Bnls B H 45 D Plate Beef Plate Short Ribs B G 28 M Beef Plate Skirt Steak, Bnls B G 54 D/M Loin Beef Loin Top Loin Steak B F 59 D Beef Loin Top Loin Steak, Bnls B F 60 D Beef Loin T-bone Steak B F 55 D Beef Loin Porterhouse Steak B F 49 D Beef Loin Tenderloin Steak B F 56 D Beef Loin Tenderloin Roast B F 34 D Beef Loin Top Sirloin Steak, Bnls B F 62 D Beef Loin Top Sirloin Cap Steak, Bnls B F 64 D Beef Loin Top Sirloin Steak, Bnls Cap Off B F 63 D Beef Loin Tri-Tip Roast B F 40 D Flank Beef Flank Steak B D 47 D/M Round Beef Round Steak B I 51 M Beef Round Steak, Bnls B I 52 M BEEF Retail Cut Name Specie Primal Name Cookery Primal Beef Bottom Round Rump Roast B I 09 D/M Beef Round Top Round Steak B I 61 D Beef Round Top Round Roast B I 39 D Beef -

The New U.S. Meat Industry

Barkema/Drabenstott.qxd 6/21/01 1:37 PM Page 33 The New U.S. Meat Industry By Alan Barkema, Mark Drabenstott, and Nancy Novack new meat industry is rapidly emerging in the United States, as food retailers, meat processors, and farms and ranches coalesce Ainto fewer and larger businesses. The industry’s rapid consolida- tion in recent years has triggered alarms that the industry’s new giants in retailing and processing could drive up food prices for consumers and drive down livestock prices for producers. How should public policy respond to the industry’s consolidation? And how can all participants in the industry—producers, processors, retailers, and consumers—benefit from its new structure? This article studies the striking changes in the meat industry in three steps. First it describes how the industry is changing. Then it examines the forces driving the industry’s consolidation. Finally, it con- siders how consumers and industry participants are affected. While cur- rent evidence is scant that market power has hurt either consumers or producers, the industry’s rapid consolidation nevertheless warrants vigi- lance. At the same time, public policy might also play a role in ensuring that all participants in the market benefit from its new structure. All three authors are members of the bank’s Center for the Study of Rural America. Alan Barkema is vice president and economist, Mark Drabenstott is vice president and director, and Nancy Novack is a research associate. Kate Sheaff, a research associate in the Center, helped prepare the article. The article is on the bank’s web site at www.kc.frb.org. -

Meat Packing, an Industry on the Deck

University of Mississippi eGrove Touche Ross Publications Deloitte Collection 1964 Meat Packing, an industry on the deck Maurice McGill Iowa Beef Packers Follow this and additional works at: https://egrove.olemiss.edu/dl_tr Part of the Accounting Commons, and the Taxation Commons Recommended Citation Quarterly, Vol. 10, no. 3 (1964, September), p. 17-21 This Article is brought to you for free and open access by the Deloitte Collection at eGrove. It has been accepted for inclusion in Touche Ross Publications by an authorized administrator of eGrove. For more information, please contact [email protected]. by Maurice McGill MEAT PACKIN6 The author wishes to express his appreciation to Iowa Beef Packers, Inc., for their cooperation in preparing this article. An Industry nn the Deck "Gentlemen, this industry is on the deck. It has hit the cheaper to transport the cattle to feed supplies, primarily bottom and has only one way to go — up." This statement corn, than it was to transport feed to the cattle, particu was made recently to a group of financial analysts by larly in view of the fact that in doing so, the cattle were A. D. Anderson, president of Iowa Beef Packers, Inc., as moved closer to the larger Eastern population centers he discussed one of the largest, most important industries where they would ultimately be consumed. Inadequate of the United States — meat packing. These comments, refrigeration and transportation facilities made it impera coming from the president of the newest member in the tive that meat slaughter plants be located close to the family of major meat packers, were greeted with some consumer. -

1 2 3 4 5 6 7 8 9 10 11 12 13 14 Appetizers

1 Steamed or Pan Fried Dumplings …………………….. 5.95 (Choice of: Chicken, Vegetable or Pork) 2 Crystal Watercress Shrimp Dumplings………………... 6.95 3 Crab Meat Sui Mai…………………………………….. 6.95 4 Little Juicy Pork Buns…………………………………. 8.95 5 Scallion Pancake………………………………………. 5.50 6 Edamame ……………………………………………… 4.50 7 B-B-Q Spare Ribs……………………………………… 9.95 8 Cantonese Roast Duck…………………………………. 9.95 9 Cantonese Roast Pork………………………………….. 8.95 10 Rock Shrimp…………………………………………… 6.95 11 Fried Calamari…………………………………………. 6.95 12 Fried Cheese Wonton………………………………….. 4.95 13 Shrimp Wonton in Red Sesame Oil…………………… 6.95 14 Sesame Cold Noodle (not Spicy)……………………… 5.50 APPETIZERS (CHEN-DU) 15* Dan Dan Noodles Chen-Du Style……………………… 5.50 16* Pork Dumplings in Chili Oil…………………………... 6.95 17 Leaf-wrapped Glutinous Rice Cake…………………… 5.95 18 Glutinous Rice Balls…………………………………… 6.95 19 Wonton in Light Soups………………………………… 6.95 20* Northern Sichuan Style Bean Jelly…………………….. 6.95 21* Spicy Sichuan Cold Noodle…………………………… 5.50 22** Sour & Hot Sweet Potato Noodles……………………. 6.95 23** Tears in Eyes (Very Spicy Mung Bean Noodle)………. 6.95 24* Pork Wonton in Red Sesame Oil………………………. 5.95 SOUP 25* Hot & Sour Soup Small: 2.95 Large: 5.95 26 Egg Drop Soup Small: 2.95 Large: 5.95 27 Wonton Soup Small: 2.95 Large: 5.95 28 Miso Soup Small: 2.95 Large: 5.95 29 Velvet Chicken Corn Soup…………………………….. 6.95 30 Vegetable Soup………………………………………… 7.95 31 Bamboo Fungus and Chicken (on bone) Soup………… 13.95 32 Duck (on bone ) Soup w/ Preserved Reddish………….. 13.95 33 Slice Fish w/ Pickled Vegetable Soup…………………. 9.95 34 Loofah & Scramble Egg Soup…………………………. -

Insights of Innovation and Competitiveness in Meat Supply Chains

OPEN ACCESS International Food and Agribusiness Management Review Please citeVolume this article 19 Issue as 'in 4, press'; 2016; DOI: 10.22434/IFAMR2018.0031 Received: 24 February 2018 / Accepted: 30 November 2018 Insights of innovation and competitiveness in meat supply chains REVIEW ARTICLE Alice Munz Fernandes a, Odilene de Souza Teixeirab, Heitor Vieira Riosa, Maria Eugênia Andrighetto Canozzic, Glauco Schultzd and Júlio Otávio Jardim Barcellose a Researcher, Center of Agribusiness Studies – CEPAN, Universidade Federal do Rio Grande do Sul, Porto Alegre (UFRGS), Avenue Bento Gonçalves 7712, CEP 91540-000, Porto Alegre, RS, Brazil b Researcher, Department of Animal Science (Zootecnia), Universidade Federal do Rio Grande do Sul (UFRGS), Porto Alegre, Avenue Bento Gonçalves 7712, CEP 91540-000, Porto Alegre, RS, Brazil c Researcher, Instituto Nacional de Investigación Agropecuaria (INIA). Programa Producción de Carne y Lana. Estación Experimental INIA La Estanzuela. Ruta 50 km 11, 39173, Colonia, Uruguay d Professor, Department of Economic Science and Center of Agribusinnes Studies – CEPAN, Universidade Federal do Rio Grande do Sul, Porto Alegre (UFRGS), Avenue João Pessoa 52, CEP 90040-000, Porto Alegre, RS, Brazil e Professor, Department of Animal Science (Zootecnia) and Center of Agribusinnes Studies – CEPAN, Universidade Federal do Rio Grande do Sul (UFRGS), Porto Alegre, Avenue Bento Gonçalves 7712, CEP 91540-000, Porto Alegre, RS, Brazil Abstract The world demand for food in parallel with environmental concerns is a paradigm for the competitiveness of agro-industrial production chains. The present study intended to propose insights on the contribution of innovation and competitiveness in meat production chains. A systematic review of the literature was carried out, considering manuscripts published in the Scopus, Web of Science and Science Direct databases. -

Industrial Agriculture, Livestock Farming and Climate Change

Industrial Agriculture, Livestock Farming and Climate Change Global Social, Cultural, Ecological, and Ethical Impacts of an Unsustainable Industry Prepared by Brighter Green and the Global Forest Coalition (GFC) with inputs from Biofuelwatch Photo: Brighter Green 1. Modern Livestock Production: Factory Farming and Climate Change For many, the image of a farmer tending his or her crops and cattle, with a backdrop of rolling fields and a weathered but sturdy barn in the distance, is still what comes to mind when considering a question that is not asked nearly as often as it should be: Where does our food come from? However, this picture can no longer be relied upon to depict the modern, industrial food system, which has already dominated food production in the Global North, and is expanding in the Global South as well. Due to the corporate take-over of food production, the small farmer running a family farm is rapidly giving way to the large-scale, factory farm model. This is particularly prevalent in the livestock industry, where thousands, sometimes millions, of animals are raised in inhumane, unsanitary conditions. These operations, along with the resources needed to grow the grain and oil meals (principally soybeans and 1 corn) to feed these animals place intense pressure on the environment. This is affecting some of the world’s most vulnerable ecosystems and human communities. The burdens created by the spread of industrialized animal agriculture are wide and varied—crossing ecological, social, and ethical spheres. These are compounded by a lack of public awareness and policy makers’ resistance to seek sustainable solutions, particularly given the influence of the global corporations that are steadily exerting greater control over the world’s food systems and what ends up on people’s plates.