Entrepreneurship in the Creative Industries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Songs by Title

Songs by Title Title Artist Title Artist #1 Goldfrapp (Medley) Can't Help Falling Elvis Presley John Legend In Love Nelly (Medley) It's Now Or Never Elvis Presley Pharrell Ft Kanye West (Medley) One Night Elvis Presley Skye Sweetnam (Medley) Rock & Roll Mike Denver Skye Sweetnam Christmas Tinchy Stryder Ft N Dubz (Medley) Such A Night Elvis Presley #1 Crush Garbage (Medley) Surrender Elvis Presley #1 Enemy Chipmunks Ft Daisy Dares (Medley) Suspicion Elvis Presley You (Medley) Teddy Bear Elvis Presley Daisy Dares You & (Olivia) Lost And Turned Whispers Chipmunk Out #1 Spot (TH) Ludacris (You Gotta) Fight For Your Richard Cheese #9 Dream John Lennon Right (To Party) & All That Jazz Catherine Zeta Jones +1 (Workout Mix) Martin Solveig & Sam White & Get Away Esquires 007 (Shanty Town) Desmond Dekker & I Ciara 03 Bonnie & Clyde Jay Z Ft Beyonce & I Am Telling You Im Not Jennifer Hudson Going 1 3 Dog Night & I Love Her Beatles Backstreet Boys & I Love You So Elvis Presley Chorus Line Hirley Bassey Creed Perry Como Faith Hill & If I Had Teddy Pendergrass HearSay & It Stoned Me Van Morrison Mary J Blige Ft U2 & Our Feelings Babyface Metallica & She Said Lucas Prata Tammy Wynette Ft George Jones & She Was Talking Heads Tyrese & So It Goes Billy Joel U2 & Still Reba McEntire U2 Ft Mary J Blige & The Angels Sing Barry Manilow 1 & 1 Robert Miles & The Beat Goes On Whispers 1 000 Times A Day Patty Loveless & The Cradle Will Rock Van Halen 1 2 I Love You Clay Walker & The Crowd Goes Wild Mark Wills 1 2 Step Ciara Ft Missy Elliott & The Grass Wont Pay -

Karaoke Mietsystem Songlist

Karaoke Mietsystem Songlist Ein Karaokesystem der Firma Showtronic Solutions AG in Zusammenarbeit mit Karafun. Karaoke-Katalog Update vom: 13/10/2020 Singen Sie online auf www.karafun.de Gesamter Katalog TOP 50 Shallow - A Star is Born Take Me Home, Country Roads - John Denver Skandal im Sperrbezirk - Spider Murphy Gang Griechischer Wein - Udo Jürgens Verdammt, Ich Lieb' Dich - Matthias Reim Dancing Queen - ABBA Dance Monkey - Tones and I Breaking Free - High School Musical In The Ghetto - Elvis Presley Angels - Robbie Williams Hulapalu - Andreas Gabalier Someone Like You - Adele 99 Luftballons - Nena Tage wie diese - Die Toten Hosen Ring of Fire - Johnny Cash Lemon Tree - Fool's Garden Ohne Dich (schlaf' ich heut' nacht nicht ein) - You Are the Reason - Calum Scott Perfect - Ed Sheeran Münchener Freiheit Stand by Me - Ben E. King Im Wagen Vor Mir - Henry Valentino And Uschi Let It Go - Idina Menzel Can You Feel The Love Tonight - The Lion King Atemlos durch die Nacht - Helene Fischer Roller - Apache 207 Someone You Loved - Lewis Capaldi I Want It That Way - Backstreet Boys Über Sieben Brücken Musst Du Gehn - Peter Maffay Summer Of '69 - Bryan Adams Cordula grün - Die Draufgänger Tequila - The Champs ...Baby One More Time - Britney Spears All of Me - John Legend Barbie Girl - Aqua Chasing Cars - Snow Patrol My Way - Frank Sinatra Hallelujah - Alexandra Burke Aber Bitte Mit Sahne - Udo Jürgens Bohemian Rhapsody - Queen Wannabe - Spice Girls Schrei nach Liebe - Die Ärzte Can't Help Falling In Love - Elvis Presley Country Roads - Hermes House Band Westerland - Die Ärzte Warum hast du nicht nein gesagt - Roland Kaiser Ich war noch niemals in New York - Ich War Noch Marmor, Stein Und Eisen Bricht - Drafi Deutscher Zombie - The Cranberries Niemals In New York Ich wollte nie erwachsen sein (Nessajas Lied) - Don't Stop Believing - Journey EXPLICIT Kann Texte enthalten, die nicht für Kinder und Jugendliche geeignet sind. -

Karaoke Catalog Updated On: 09/04/2018 Sing Online on Entire Catalog

Karaoke catalog Updated on: 09/04/2018 Sing online on www.karafun.com Entire catalog TOP 50 Tennessee Whiskey - Chris Stapleton My Way - Frank Sinatra Wannabe - Spice Girls Perfect - Ed Sheeran Take Me Home, Country Roads - John Denver Broken Halos - Chris Stapleton Sweet Caroline - Neil Diamond All Of Me - John Legend Sweet Child O'Mine - Guns N' Roses Don't Stop Believing - Journey Jackson - Johnny Cash Thinking Out Loud - Ed Sheeran Uptown Funk - Bruno Mars Wagon Wheel - Darius Rucker Neon Moon - Brooks & Dunn Friends In Low Places - Garth Brooks Fly Me To The Moon - Frank Sinatra Always On My Mind - Willie Nelson Girl Crush - Little Big Town Zombie - The Cranberries Ice Ice Baby - Vanilla Ice Folsom Prison Blues - Johnny Cash Piano Man - Billy Joel (Sittin' On) The Dock Of The Bay - Otis Redding Bohemian Rhapsody - Queen Turn The Page - Bob Seger Total Eclipse Of The Heart - Bonnie Tyler Ring Of Fire - Johnny Cash Me And Bobby McGee - Janis Joplin Man! I Feel Like A Woman! - Shania Twain Summer Nights - Grease House Of The Rising Sun - The Animals Strawberry Wine - Deana Carter Can't Help Falling In Love - Elvis Presley At Last - Etta James I Will Survive - Gloria Gaynor My Girl - The Temptations Killing Me Softly - The Fugees Jolene - Dolly Parton Before He Cheats - Carrie Underwood Amarillo By Morning - George Strait Love Shack - The B-52's Crazy - Patsy Cline I Want It That Way - Backstreet Boys In Case You Didn't Know - Brett Young Let It Go - Idina Menzel These Boots Are Made For Walkin' - Nancy Sinatra Livin' On A Prayer - Bon -

Northern Cool Produces Hot Hits

NORDIC SPOTLIGHT Northern cool produces hot hits A number of acts from the The home market in the Nordic countries-Denmark, Finland, Nordic area have burst onto Iceland, Norway and theinternational music Sweden-is growing at an scene in the past twenty or average of 5 percent annually, and last year 61 million albums were so years. Abba were the sold throughout the region. That's first-and perhaps still the still some way short of the European "big three"-Germany, Britain and biggest-Scandinavian France-but ahead of other major success story, but names markets such as Italy and Spain. The suchasRoxette,Bjork, Nordic market was worth $1,047 mil- lion in 1997, more than eight percent Michael Learns To Rock and of the total European figure. A -Ha have had their indi- In Sweden, pop exports are at last in the beingofficiallyrecognised as an vidualtriumphs importantcontributiontostate European charts and else- income, with the government intro- where. Now, in the '90$, the ducing a special "Grammy" award for services to exports. Sweden is also the sum of those parts is creat- only Nordic nation with a body specif- ing a greater whole. Nordic ically set up by the industry to aid the export trade. Export Music Sweden artists are featuring in-and organises the Swedish presence at topping-charts across Midem (Sweden will host the opening Europe and in the U.S.A. at Cannes next year), at Popkomm and at other important international Keith Foster analyses the events, and provides information on Nordic music phenomenon. Swedish product in book form and on the Internet. -

Låtlista Från DJ Uthyrning 1

DJ Uthyrning Tel nr. 0761 - 122 123 E-post [email protected] Låtlista från DJ uthyrning 1. Engelbert Humperdinck - My World 2. Dean martin - that`s amore 3. Beatles - I Saw Her Standing There 4. Unforgettable - Nat king cole 5. Toto - Rosanna 6. Maxi Priest - Wild world 7. Engelbert Humperdinck - How To Win Your Love 8. Elton John - Nikita 9. Christina Aguilera - Candyman 10. Engelbert humperdinck - Release me 11. E.Humperdink - Quando Quando Quando 12. Nine de angel - Guardian angel 13. Lutricia McNeal - Stranded 14. Tom Jones - Help Yourself 15. The art company - Susanna 16. T.Jones - It's not unusual 17. Simply Red - It's only love 18. Toto - Africa 19. Frank Sinatra - Stranger in the nigth 20. Cher - Dov'e Lamore 21. M.Gaye - Sexual Healing Ultimix 22. Hanne Boel - I Wanna Make Love To You 23. tom jones - Delilah 24. Toto - Hold the line 25. Michel Teló Feat Magnate y Valentino - Ai Se Eu Te Pego (Remix) 26. Tina Turner - What's Love Got To Do With It (Special Extended Mix) 27. Tina Turner - We Don't Need Another Hero 28. DJ.bobo - Everybody 29. Enrique Iglesias - Bailamos 30. Mendez - Carnaval 31. MR President - Coco jamboo 32. Madonna - La isla bonita 33. Culture club - Do you really want to hurt me 34. Carl douglas - Kung fu fighting 35. Tina Turner & Jimmy Barnes - The Best (Extended Version) [Capitol Records] 36. ENGELBERT HUMPERDINK - SPANISH EYES 37. The four seasons - December 1963 38. Tom Jones - Love Me Tonight 39. L.Armostrong - What a wonderful world 40. Elton John - Sad song 41. -

Musikutbudet I Svenska Etermedier Eller ”Avgörande För Musikutbudet Är Vad Man Spelar”

Musikutbudet i svenska etermedier eller ”Avgörande för musikutbudet är vad man spelar” Ett examensarbete vid avdelningen för Medieteknik och Grafisk Produktion, KTH, Stockholm Författare: Anders Edström, KTH Leopold Landström, SU Examinator: Prof. Nils Enlund, KTH Handledare: Roger Wallis, KTH Stockholm 2000-07-06 ”Musikutbudet i svenska etermedier” – ett examensarbete vid avdelningen för Medieteknik och Grafisk Produktion, KTH, Stockholm Av Anders Edström, KTH och Leopold Landström, Stockholms universitet - 2000-07-06 ”Oops?! I played it again”1 1 Denna rapport påvisar en tydlig trend att musikläggare på svenska radiostationer tenderar att spela ett minskande antal titlar (verk) fler gånger, samtidigt som musikmängden i radio generellt sett är konstant eller ökar. Trenden gäller både Mix Megapol (som här får representera kommersiell radio) och radiokanaler inom public service, även om utvecklingen inte är lika dramatisk inom den senare. 2 (190) ”Musikutbudet i svenska etermedier” – ett examensarbete vid avdelningen för Medieteknik och Grafisk Produktion, KTH, Stockholm Av Anders Edström, KTH och Leopold Landström, Stockholms universitet - 2000-07-06 Förord Denna rapport är resultatet av ett samarbete mellan två studenter vid KTH och Stockholms universitet. Vår förhoppning är att detta arbete ska öka förståelsen för vilken musik som spelas i etermedia – och då i synnerhet i radio – hur mycket, men framförallt varför. Vi önskar tacka alla som bidragit till denna rapports framställande. Speciellt vill vi tacka Peter Liljander för alla övertidstimmar i sällskap med databasen på STIM, samt Katja Simonson, STIM, som gjorde kompletterande databaskörningar. Victoria van Loan för att vi fick köpa listor från Music Control fast vi bara var studenter. Pia Kalischer för siffrorna bakom topplistan på P3. -

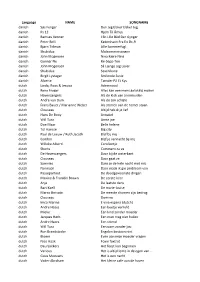

Language NAME SONGNAME Danish Søs Fenger Den Jeg

Language NAME SONGNAME danish Søs Fenger Den Jeg Elsker Elsker Jeg danish Ps 12 Hjem Til Århus danish Bamses Venner I En Lille Båd Der Gynger danish Peter Belli København Fra En Dc-9 danish Bjørn Tidman Lille Sommerfugl danish Shubidua Midsommersangen danish John Mogensen Nina Kære Nina danish Gunnar Nu Re-Sepp-Ten danish John Mogensen Så Længe Jeg Lever danish Shubidua Sexchikane danish Birgit Lystager Smilende Susie danish Alberte Tænder På Et Kys dutch Linda, Roos & Jessica Ademnood dutch Rene Froger Alles kan een mens gelukkig maken dutch Havenzangers Als de klok van arnemuiden dutch Andre van Duin Als de zon schijnt dutch Frans Bauer / Marianne Weber Als sterren aan de hemel staan dutch Clouseau Altijd heb ik je lief dutch Hans De Booy Annabel dutch Will Tura Arme joe dutch Doe Maar Belle helene dutch Tol Hansse Big city dutch Paul de Leeuw / Ruth Jacoth Blijf bij mij dutch Gordon Blijf je vannacht bij mij dutch Willeke Alberti Carolientje dutch Shorts Comment ca va dutch De Havenzangers Daar bij de waterkant dutch Clouseau Daar gaat ze dutch Sjonnies Dans je de hele nacht met mij dutch Normaal Daor maak ik gin probleem van dutch Passepartout De doodgewoonste dingen dutch Maxine & Franklin Brown De eerste keer dutch Anja De laatste dans dutch Bart Kaell De marie-louise dutch Marco Borsato De meeste dromen zijn bedrog dutch Clouseau Domino dutch Imca Marina E viva espana (dutch) dutch Andre Hazes Een beetje verliefd dutch Mieke Een kind zonder moeder dutch Jacques Herb Een man mag niet huilen dutch Andre Hazes Een vriend dutch Will Tura Eenzaam zonder jou dutch Ron Brandsteder Engelen bestaan niet dutch Bloem Even aan mijn moeder vragen dutch Nico Haak Foxie foxtrot dutch Deurzakkers Het feest kan beginnen dutch Various Het is altijd lente in de ogen van .. -

Amadin Fonky Mp3, Flac, Wma

Amadin Fonky mp3, flac, wma DOWNLOAD LINKS (Clickable) Genre: Electronic Album: Fonky Country: Sweden Released: 1995 Style: House MP3 version RAR size: 1639 mb FLAC version RAR size: 1862 mb WMA version RAR size: 1371 mb Rating: 4.8 Votes: 252 Other Formats: AA DTS FLAC VOC AIFF AC3 MOD Tracklist A01 Fonky (Extended) 5:17 B01 Fonky (Captain Fonks Club) 5:16 B02 Fonky (Radio) 3:59 Companies, etc. Published By – Cheiron Songs Published By – Mega Songs Phonographic Copyright (p) – Cheiron Songs Copyright (c) – Tempo Records Recorded At – Cheiron Studios Manufactured By – Next Stop Distribution Distributed By – Next Stop Distribution Credits Producer – John Amatiello, Kristian Lundin Vocals [Additional] – Jessica Folcker Written-By – Herbie Chrichlow*, John Amatiello, Kristian Lundin Notes Written by John Amatiello, Kristian Lundin & Herbie Chrichlow. Produced by John Amatiello & Kristian Lundin. Recorded at Cheiron Studios. Additional vocals by Jessica Folcker. Published by Cheiron Songs / Mega Songs. ℗ 1995 Cheiron Songs. © 1995 Tempo Records. Manufactured & distributed by Next Stop Distribution. Other versions Category Artist Title (Format) Label Category Country Year Amadin & Amadin & Captain Funk - TEMP43CD Tempo Records TEMP43CD Sweden 1995 Captain Funk Fonky (CD, Single) TEMP43T Amadin Fonky (12", Maxi, W/Lbl) Tempo Records TEMP43T Sweden 1995 Related Music albums to Fonky by Amadin Its Alive - Earthquake Visions Rock Herbie - Pick It Up Remixes Electronic Herbie - Pick It Up Electronic da Fonky Headz - Fonky Lover Electronic Pascal D Mann - I Need You More Electronic Santos Suarez, Stefan Vilijn, Jason Cheiron - Ritmo Dancer Electronic Dr. Alban - The Very Best Of 1990 - 1997 Electronic / Reggae / Pop Dr. Alban - Let The Beat Go On Electronic Backstreet Boys - Quit Playing Games (With My Heart) Pop E-Type - You Will Always Be A Part Of Me Electronic / Pop. -

Karaoke Catalog Updated On: 17/12/2016 Sing Online on in English Karaoke Songs

Karaoke catalog Updated on: 17/12/2016 Sing online on www.karafun.com In English Karaoke Songs (H?D) Planet Earth My One And Only Hawaiian Hula Eyes Blackout I Love My Baby (My Baby Loves Me) On The Beach At Waikiki Other Side I'll Build A Stairway To Paradise Deep In The Heart Of Texas 10 Years My Blue Heaven What Are You Doing New Year's Eve Through The Iris What Can I Say After I Say I'm Sorry Long Ago And Far Away 10,000 Maniacs When You're Smiling (The Whole World Smiles With Bésame mucho (English Vocal) Because The Night 'S Wonderful For Me And My Gal 10CC 1930s Standards 'Til Then Dreadlock Holiday Let's Call The Whole Thing Off Daddy's Little Girl I'm Not In Love Heartaches The Old Lamplighter The Things We Do For Love Cheek To Cheek Someday You'll Want Me To Want You Rubber Bullets Love Is Sweeping The Country That Old Black Magic (Woman Voice) Life Is A Minestrone My Romance That Old Black Magic (Man Voice) 112 It's Time To Say Aloha I Know Why (And So Do You) DUET Cupid We Gather Together Aren't You Glad You're You Peaches And Cream Kumbaya (I've Got A Gal In) Kalamazoo 12 Gauge The Last Time I Saw Paris My One And Only Highland Fling Dunkie Butt All The Things You Are No Love No Nothin' 12 Stones Smoke Gets In Your Eyes Personality Far Away Begin The Beguine Sunday, Monday Or Always Crash I Love A Parade This Heart Of Mine 1800s Standards I Love A Parade (short version) Mister Meadowlark Home Sweet Home I'm Gonna Sit Right Down And Write Myself A Letter 1950s Standards Home On The Range Body And Soul Get Me To The Church On -

Catalogue Karaoké Mis À Jour Le: 29/07/2021 Chantez En Ligne Sur Catalogue Entier

Catalogue Karaoké Mis à jour le: 29/07/2021 Chantez en ligne sur www.karafun.fr Catalogue entier TOP 50 J'irai où tu iras - Céline Dion Femme Like U - K. Maro La java de Broadway - Michel Sardou Sous le vent - Garou Je te donne - Jean-Jacques Goldman Avant toi - Slimane Les lacs du Connemara - Michel Sardou Les Champs-Élysées - Joe Dassin La grenade - Clara Luciani Les démons de minuit - Images L'aventurier - Indochine Il jouait du piano debout - France Gall Shallow - A Star is Born Bohemian Rhapsody - Queen La bohème - Charles Aznavour A nos souvenirs - Trois Cafés Gourmands Mistral gagnant - Renaud L'envie - Johnny Hallyday Confessions nocturnes - Diam's EXPLICIT Beau-papa - Vianney La boulette (génération nan nan) - Diam's EXPLICIT On va s'aimer - Gilbert Montagné Place des grands hommes - Patrick Bruel Alexandrie Alexandra - Claude François Libérée, délivrée - Frozen Je l'aime à mourir - Francis Cabrel La corrida - Francis Cabrel Pour que tu m'aimes encore - Céline Dion Les sunlights des tropiques - Gilbert Montagné Le reste - Clara Luciani Je te promets - Johnny Hallyday Sensualité - Axelle Red Anissa - Wejdene Manhattan-Kaboul - Renaud Hakuna Matata (Version française) - The Lion King Les yeux de la mama - Kendji Girac La tribu de Dana - Manau (1994 film) Partenaire Particulier - Partenaire Particulier Allumer le feu - Johnny Hallyday Ce rêve bleu - Aladdin (1992 film) Wannabe - Spice Girls Ma philosophie - Amel Bent L'envie d'aimer - Les Dix Commandements Barbie Girl - Aqua Vivo per lei - Andrea Bocelli Tu m'oublieras - Larusso -

Qui Est Denniz Pop ?

Qui est Denniz Pop ? Denniz Pop, de son vrai nom suédois Dag Krister Volle (dite Dagge), a commencé sa carrière comme DJ dans les environs de Stockholm dans les années 1980. Durant les années 1980 à 1990 Denniz Pop était l’un des DJs les plus convoités des discothèques suédoises grâce à ses remixes appréciés du public. Vers le milieu des années 1980, c’est lors de la sortie de ses remixes « Love to love you baby » du tube disco de Donna Summer et « Billie jean » de Michael Jackson, qu’il s’est fait connaître d’abord en Scandinavie, puis en Europe, et enfin aux Etats-Unis. Dans les années 1990, il arrête sa carrière de DJ pour aller de l’avant dans le milieu de la musique. En désertant les boites de nuit, il remarque les Ace of Base. A l’époque ces derniers étaient adolescents et faisaient des reprises de chansons célèbres dans les cafés et les bars. C’est en les rencontrant, qu’il décida de devenir producteur de musique et parolier. En 1993, il écrit pour ces quatre jeunes suédois « All that she wants » (véritable tube planétaire de 1993 à 1996) et produit leur premier album Happy Nation, dont sont inclus d’autres succès ayant fait le tour des ondes internationales comme « Happy Nation », « Don’t turn around » et le fameux « The sign ». Notons que cet album s’est vendu à plus de 22 millions d’exemplaires : du jamais-vu pour la sortie d’un premier album. Mais Denniz Pop ne s’arrêta pas au succès des Ace of base. -

Eurochart Hot 1000 Singles

SALES week 12/99 Eurochart Hot 1000 Singles ©BPI Communications Inc A TITLE countries TITLE countries 1 TITLE countries ! "8 ARTIST charted `8 ARTIST charted t ARTIST charted 4 original label (publisher) os 4 original label (publisher) 4 original label (publisher) ...Baby One More Time A.B.DIC.D.GRE.IRE.LIVL.NS.CH.UK Would You...? AD.LCH CDCharlie Big Potato D.NLUK 0 16 Britney Spears- Jive (Grantsville 1 Zomba) 3427 20 Touch & Go- Oval /V2 (Oval) 1-41i Skunk Anansie - Virgin (Chrysalis) Pretty Fly (For A White Guy) A.BDEFINF.D.GRE.IREININ.SCILUK I Wish A.D.CH How Deep Is Your Love B.DKEIVLS 3620 8 03 10 The Offspring- Columbia (Underachiver I Wixen) Oli P. - Hansa (EMI1BMG Ufa) 77 21 Dru Hill - Island (EMI 'Various) Big Big World A.B.F.D.GRE.IRE.LNL.CH.HUN Tarzan & Jane ADKD.N.L.N.S * The Launch NL 32 23 Emilia- Rodeo! Universal (EMI) " Toy -Box - Spin I Edel (Spin Off Songs) 87 2 DJ Jean- Digidance (Not Listed) A.B.DKERGRE.IRE.LNL.NE.S.CH.UK B.DK.IFIENL.N.S.UK Believe Chocolate Salty Balls I Want TiiomarethSpzindonMyyolLumibfiaet6simonye Loaivornein&Yondouo:NL 61 19 44 21 Cher -WEA (Rive-Droite /Warner Chappell) Ti)29 13 Chef-American/Columbia (Hilarity Music) 71 . Strong Enough A.B.FDV.F.D.GRE.IRE.NL.E.S.CH.UK Wish I Could Fly A.B.D.NL.E.S.CH.HUN I Want You Back IRE.S.UK ®63 Cher - WEA (Rive-Droite 'Warner Chappell) 3822 5 Roxette - Roxette Recordings /EMI (Hip Happy /EMI) 7255 3 'N Sync - Ariola I Northwestside (Cheiron I BMG) EDChanges B.D.IRKIVL.S.CH.UIC How Will I Know (Who You Are) ADKONL.N.SRUN To The Moon And Back F 7 52Pac - Jive / Amaru (Joshua's Dream I MCA I Zappo /Warner Chappell) 45 7 Jessica Folcker - Jive (BMG Ufa I Grantsville I Zomba) 7350 7 Savage Garden - Columbia (EMI) When The Going Gets Tough IRE.