2016 TOC.Indd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

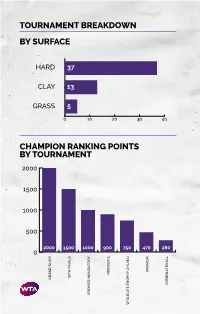

Tournament Breakdown by Surface Champion Ranking Points By

TOURNAMENT BREAKDOWN BY SURFACE HAR 37 CLAY 13 GRASS 5 0 10 20 30 40 CHAMPION RANKING POINTS BY TOURNAMENT 2000 1500 1000 500 2000 1500 1000 900 750 470 280 0 PREMIER PREMIER TA FINALS TA GRAN SLAM INTERNATIONAL PREMIER MANATORY TA ELITE TROPHY HUHAI TROPHY ELITE TA 55 WTA TOURNAMENTS BY REGION BY COUNTRY 8 CHINA 2 SPAIN 1 MOROCCO UNITED STATES 2 SWITZERLAND 7 OF AMERICA 1 NETHERLANDS 3 AUSTRALIA 1 AUSTRIA 1 NEW ZEALAND 3 GREAT BRITAIN 1 COLOMBIA 1 QATAR 3 RUSSIA 1 CZECH REPUBLIC 1 ROMANIA 2 CANADA 1 FRANCE 1 THAILAND 2 GERMANY 1 HONG KONG 1 TURKEY UNITED ARAB 2 ITALY 1 HUNGARY 1 EMIRATES 2 JAPAN 1 SOUTH KOREA 1 UZBEKISTAN 2 MEXICO 1 LUXEMBOURG TOURNAMENTS TOURNAMENTS International Tennis Federation As the world governing body of tennis, the Davis Cup by BNP Paribas and women’s Fed Cup by International Tennis Federation (ITF) is responsible for BNP Paribas are the largest annual international team every level of the sport including the regulation of competitions in sport and most prized in the ITF’s rules and the future development of the game. Based event portfolio. Both have a rich history and have in London, the ITF currently has 210 member nations consistently attracted the best players from each and six regional associations, which administer the passing generation. Further information is available at game in their respective areas, in close consultation www.daviscup.com and www.fedcup.com. with the ITF. The Olympic and Paralympic Tennis Events are also an The ITF is committed to promoting tennis around the important part of the ITF’s responsibilities, with the world and encouraging as many people as possible to 2020 events being held in Tokyo. -

Fsj-2016-12-December.Pdf

PUBLISHED BY THE AMERICAN FOREIGN SERVICE ASSOCIATION DECEMBER 2016 THE NEW RUSSIA AT 25 DIPLOMACY LESSONS AN INTERVIEW WITH GEORGE SHULTZ FINDING MONEY FOR COLLEGE EDUCATION SUPPLEMENT FOREIGN SERVICE December 2016 Volume 93, No. 10 Focus On Russia 21 Understanding Russian Foreign Policy Today U.S.-Russia relations are in disarray, with talk of a new Cold War pervasive. Fortunately, framing the conflicts in terms of national interests points to a way forward. By Raymond Smith 27 The Rise of the New Russia This tour d’horizon from the fall of 21 the Soviet Union to today—including hopes, disappointment and missed opportunities—puts U.S.-Russia relations into perspective. 48 Communications Education By Louis D. Sell Behind the Iron Curtain This firsthand account of a fire in Supplement 32 the secure area of Embassy Moscow Something Happened on March 28, 1991, conveys the on the Way to the Market: importance and drama of Diplomatic Telecommunications Service work 76 The Economic State of during the last days of the USSR. Finding Money the Former USSR By Timothy C. Lawson for College: A Guide When it comes to the Soviet successor to Scholarships nations, economic and commercial Scholarships can lighten the financial diplomacy is a particularly important 52 burden of a college education. Here part of the U.S. foreign policy playbook. Groundbreaking are some tips on finding them. By Michael A. Lally Diplomacy: An Interview By Francesca Kelly with George Shultz 37 George Shultz reflects on his tenure Four Centuries and as Secretary of State in the Reagan 86, 88, 90 administration and the process of Schools at a Glance Three Decades of making foreign policy and conducting Russian Thinking diplomacy during the decade leading Conversations in Moscow with up to the fall of the Soviet Union. -

2021 Media Guide 2021 Women’S Tennis Association Media Guide

Ashleigh barty WTA WORLD NO.1 SINGLES PLAYER 2021 media guide 2021 Women’s Tennis Association Media Guide © Copyright WTA 2021 All Rights Reserved. No portion of this book may be reproduced - electronically, mechanically or by any other means, including photocopying- without the written permission of the Women’s Tennis Association (WTA). Compiled by the Women’s Tennis Association (WTA) Communications Department WTA CEO: Steve Simon Editor-in-Chief: Kevin Fischer Assistant Editors: Chase Altieri, Amy Binder, Jessica Culbreath, Ellie Emerson, Katie Gardner, Estelle LaPorte, Adam Lincoln, Alex Prior, Teyva Sammet, Catherine Sneddon, Bryan Shapiro, Chris Whitmore, Yanyan Xu Cover Design: Henrique Ruiz, Tim Smith, Michael Taylor, Allison Biggs Contributors: Mike Anders, Danny Champagne, Evan Charles, Crystal Christian, Grace Dowling, Sophia Eden, Ellie Emerson,Kelly Frey, Anne Hartman, Jill Hausler, Pete Holtermann, Ashley Keber, Peachy Kellmeyer, Christopher Kronk, Courtney McBride, Courtney Nguyen, Joan Pennello, Neil Robinson, Sue Stanley- Green, Kathleen Stroia Photography: Getty Images (AFP, Bongarts), Action Images, GEPA Pictures, Ron Angle, Michael Baz, Matt May, Pascal Ratthe, Art Seitz, Chris Smith, Red Photographic, adidas, WTA WTA Corporate Headquarters 100 Second Avenue South Suite 1100-S St. Petersburg, FL 33701 +1.727.895.5000 2 Table of Contents GENERAL INFORMATION Women’s Tennis Association Story . 4-5 WTA Organizational Structure . 6 Steve Simon - WTA CEO & Chairman . 7 WTA Executive Team & Senior Management . 8 WTA Media Information . 9 WTA Performance & Health . 10-11 WTA Coach Initiatives . 12 WTA Player Development . 13 CALENDAR & TOURNAMENTS 2021 WTA Calendar . 16-17 WTA Premier Mandatory Profiles . 18 WTA Premier 5 Profiles . 19 WTA Finals & WTA Elite Trophy . -

PLAYERS GUIDE — Trump National Golf Club | Bedminster, N.J

72ND U.S. WOMEN’S OPEN CHAMPIONSHIP PLAYERS GUIDE — Trump National Golf Club | Bedminster, N.J. — July 13-16, 2017 conducted by the 2017 U.S. WOMEN'S OPEN PLAYERS' GUIDE — 1 2017 U.S. Women’s Open Exemption List TY AKABANE (a) Marina Alex 11 Stacy Lewis 6, 10, 11, 16 Beth Allen 14 Xiyu Lin 11 Birth Date: November 06, 2000 Aditi Ashok 14 Brittany Lincicome 7, 11, 13, 16 Seon Woo Bae 14, 16 Pernilla Lindberg 11 Birthplace: Walnut Creek, Calif. Isabelle Boineau 14 Gaby Lopez 11 Katie Burnett 11 Leona Maguire 4 Age: 16 Ht.: 5’5 Virginia Elena Carta 2 Mo Martin 6, 11, 16 Chella Choi 11 Caroline Masson 11, 13, 16 Home: Danville, Calif. Na Yeon Choi 1, 11 Catriona Matthew 11 In Gee Chun 1, 8, 11, 12, 16 Ai Miyazato 11 Carlota Ciganda 11, 13, 16 Mika Miyazato 11 Player Notes: ELIGIBILITY: She shot 148 at Lake Merced Golf Jacqui Concolino 11 Azahara Munoz 11 Paula Creamer 1, 11 Haru Nomura 11, 13, 16 Club in Daly City, Calif., to earn one of two spots. Austin Ernst 11, 16 Anna Nordqvist 10, 11, 13, 16 Jodi Ewart Shadoff 10, 11, 16 Ryann O’Toole 11 Ty Akabane started playing golf at age six with a set of Snoopy Shanshan Feng 11, 13, 16 Su-Hyun Oh 11 Sandra Gal 11 Lee-Anne Pace 11 golf clubs. She would hit golf balls up the giant hill across from Georgia Hall 14 Hee Young Park 11 her house, marking her progress by how far the ball went up the Brooke Henderson 5, 11, 13, 16 Inbee Park 1, 5, 6, 7, 9, 11, 12, 13, 16 Charley Hull 11, 13, 16 Sung Hyun Park 10, 14, 16 hill. -

Women's Tennis Association Media Guide

2017 Women’s Tennis Association Media Guide © Copyright WTA 2017 All Rights Reserved. No portion of this book may be reproduced —electronically, mechanically or by any other means, including photocopying— without the written permission of the Women’s Tennis Association (WTA). Printed in Canada Compiled by the Women’s Tennis Association (WTA) Communications Department WTA CEO & Chairman: Steve Simon Editors-in-Chief: Kevin Fischer & Adam Lincoln Assistant Editors: Amy Binder, Heather Bowler, Kate Goff, Estelle LaPorte, Alex Prior, Catherine Sneddon, Bryan Shapiro, Eloise Tyson, Jeff Watson, Yanyan Xu Cover Design: Jack Anton, Henrique Ruiz, Tim Smith Graphic Design: Provations Group, Nicholasville, KY, USA Contributors: Mike Anders, Crystal Christian, Sloan Floyd, Kelly Frey, Anne Hartman, Jill Hausler, Jamie Holley, Pete Holtermann, Kico Jiang, David Kane, Ashley Keber, Peachy Kellmeyer, Cindy Lupkey, Courtney McBride, Sean O’Malley, Joan Pennello, Neil Robinson, Kathleen Stroia, Chris Whitmore Photography: Getty Images (AFP, Bongarts), Action Images, GEPA Pictures, Ron Angle, Michael Baz, Matt May, Pascal Ratthe, Art Seitz, Chris Smith, Red Photographic, adidas, WTA www.wtatennis.com (English) facebook.com/WTA www.wta.cn (Chinese) twitter.com/WTA www.es.wtatennis.com (Spanish) youtube.com/WTA Snapchat.com/WTA Instagram.com/WTA WTA WTA WTA WTA Corporate European Asia-Pacific Finals Headquarters Headquarters Headquarters Headquarters 100 Second Avenue South, Palliser House, Palliser Road Vantone Center Tower C, Suite 601 6 Stadium Walk Suite 1100-S London W14 9EB, England 6A Chaowai Avenue #01-05 Sports Information & St Petersburg, Florida 33701 USA Tel: +44.20.7386.4100 Chaoyang District, Resource Centrer Tel: +1.727.895.5000 Beijing 100020, China Singapore, 397698 Tel: +86.10.5910.2700 Tel: +65.6653.9450 2 Table of Contents GENERAL INFORMATION Women’s Tennis Association (WTA) Story. -

2016 Rulebook 13Oct1149.Indd

The 2016 ATP® Offi cial Rulebook Copyright © 2016 by ATP Tour, Inc. All Rights Reserved. Reproduction of this work in whole or in part without the written per- mission of the ATP Tour, Inc., is prohibited. Printed in the United States of America. 2 TABLE OF CONTENTS I. ATP CIRCUIT REGULATIONS ...............................7 1.01 Categories of Tournaments ...................................................................... 7 1.02 Tournament Week ..................................................................................... 7 1.03 Match Schedule Plan ............................................................................... 8 1.04 Finals Options ........................................................................................... 8 1.05 Change of Tournament Site ....................................................................... 9 1.06 Commitment to Rules ................................................................................ 9 1.07 Commitment, Membership Obligations and Bonus Pool ........................... 9 1.08 Reduction of ATP World Tour Masters 1000 Commitment ...................... 12 1.09 Unsatisfi ed Player Commitment Penalties .............................................. 13 1.10 Mandatory Player Meeting ...................................................................... 13 1.11 Player Eligibility/Player University/Physical Exam ................................... 14 1.12 Waiver of Claims ..................................................................................... 14 1.13 Waiver/Player -

2016 Sponsorship Opportunities Tournament At-A-Glance

2016 SPONSORSHIP OPPORTUNITIES TOURNAMENT AT-A-GLANCE The Connecticut Open is a world-class WTA (women’s) tennis event that benefits the community and statewide charities. Long considered the tune-up to the US Open, the tournament is the only event of its kind in the Northeast and also the culmination of the summer long Emirates Airline US Open Series. Legacy event with a rich history; Tournament Director Anne Worcester is former CEO of the Women’s Tennis Association (WTA) with relationships that result in World Top 10 players competing in Connecticut each year – alongside the rising stars of tomorrow. Former champions read like a “Who’s Who” of women’s tennis: Steffi Graf, Venus Williams, Jennifer Capriati, Lindsay Davenport, Justine Henin, Caroline Wozniacki, and Petra Kvitova. To the delight of men’s tennis fans, in 2014 Connecticut Open added an annual Men’s Legends event. 2015’s event is headlined by John McEnroe alongside Andy Roddick, James Blake and Jim Courier. 2 2015 TOURNAMENT RESULTS LOCATION: Connecticut Tennis Center at Yale New Haven, Connecticut PRIZE MONEY: $754,163 PLAYER FIELD:* Including five World Top 10 and more than half of the top 30 from over 25 countries. DEFENDING SINGLES CHAMPION:* World #4 Petra Kvitova (CZE) ATTENDANCE: 52,000 TV COVERAGE:** Domestic: ESPN2 holds the domestic TV rights - 3.7M viewers Global: 7.8M viewers worldwide in over 160 countries Digital Coverage:** An additional 1.7M watched via mobile, web, and over- the top digital services such as Apple TV, Roku, and other Petra Kvitova (CZE) World #4 digital devices. -

20 16 Wta Official Rulebook

2016 WTA OFFICIAL RULEBOOK WTA 2016 WTA - Women’s Tennis Association 100 Second Avenue South, Suite 1100-S St. Petersburg, Florida, USA 33701 TEL: +1.727.895.5000 FAX: +1.727.894.1982 www.wtatennis.com Printed in the United States of America 1-124-Intro-Players.qxp_Layout 1 12/11/15 9:54 AM Page 1 2016 Official Rulebook Copyright 2016 WTA Tour, Inc. All Rights Reserved WTA and WTA Tour are registered trademarks of WTA Tour, Inc. Printed in the United States of America 1-124-Intro-Players.qxp_Layout 1 12/11/15 9:54 AM Page 1 TABLE OF CONTENTS THE WTA I. INTRODUCTION 7 A. DESCRIPTION 7 B. ADMINISTRATION 7 C. RULES 7 D. TOURNAMENT ACCEPTANCES 8 E. TOUR YEARS 8 F. WORLD CHAMPION 8 G. WTA BOARD OF DIRECTORS 9 II. TOP 10 PLAYER LIST 11 A. COMPOSITION AND ORDER 11 B. MINIMUM COMMITMENT REQUIREMENTS 12 C. COMPENSATION 13 D. COMMITMENT DEADLINES AND RULES 13 E. INCENTIVE PAYMENTS 16 F. SUSPENSION RULE 17 G. CALCULATION AND PAYMENT 20 H. ADDITIONAL RULES FOR TOP 10 PLAYERS 21 I. YEARS OF SERVICE 21 J. FUNDING OF BONUS POOL 22 III. ENTRIES/WITHDRAWALS/DRAWS/SCHEDULING 23 A. ENTRIES AND ACCEPTANCES 23 B. WITHDRAWING FROM A TOURNAMENT 34 C. DRAWS 45 D. SCHEDULING 82 IV. PLAYER RESPONSIBILITIES/ON-COURT RULES 91 AND PROCEDURES A. DIAMOND ACES POLICY 91 B. MEDIA/SPONSOR/PUBLIC RELATIONS 100 RESPONSIBILITIES C. CLOTHING AND EQUIPMENT 112 D. TOILET/CHANGE OF ATTIRE BREAKS 120 E. WTA MEDICAL RULE 122 F. CODE OF CONDUCT 122 G. DELAY OF PLAY 122 H. -

Dominika C Porn

Dominika c porn Continue Mostly from the I've watched, there seems to be a whole three categories of vulva:1. Incision type - external labia form a single slit or furrow without the clitorial hood visible or internal labia protruding. Looks tiny and tidy. Very small microscopic clitoris, very tiny inner labia. Open type - the outer labia naturally parted revealing the inner labia of the chick between them. May or may not have a prominent hood or a larger clitoris. The most common.3. Huge - the large, flappy labia that dangle behind the main lips is usually tightly folded and extruding down/outward noticeably from her mound. Can have a huge prominent hood or an unusually large clitoris. What is the most exciting/sexy arousal for you? Guys, what type of do you prefer/find the most stimulating? The process of stretching the labia involves pulling or weighing down the inner labia, or labia minora, in order to lengthen them. It began as a cultural tradition in parts of ancient Africa, Asia and the South Sea, but has since been adopted by some Western cultures, albeit on a much smaller scale. This is primarily done for appearance and sexual enhancement. Labia stretching is usually approached with the aim of permanently increasing the length of the labia minora. The stretching process should be done on a regular basis for a long period of time to achieve long-term results. Regular stretching also constantly increases the size of the labia. Lips can only spread outside the labia major or stretch down as far as a woman's knees. -

London 10-26 June 2016 Contents

PRESS PACK London 10-26 June 2016 Contents Key contacts & resources 1 Welcome message from FIH President Leandro Negre 2 About the Hockey Champions Trophies 3 About London and the Lee Valley Hockey and Tennis Centre 9 Competitions format 11 Men’s Competition Teams 13 Match schedule 21 Tournament Officials 22 Women’s Competition Teams 23 Match schedule 32 Tournament Officials 33 Useful information Event logos for download 34 Event photography 35 Following the competitions 36 Key facts 37 Rules and Tournament regulations 38 FIH World Rankings 40 Rio 2016 Olympic Games preview 42 The Hockey Revolution 45 The Future of International Hockey 46 CNT Key contacts & resources FIH Media Contacts: For all media queries relating to the event, please contact [email protected] FIH Event Media Manager Richard Stainthorpe Email: [email protected] Tel: +44 (0) 7733 322910 FIH Communications and Digital Manager Daniel Parker Email: [email protected] Tel: +41 (79) 619 7724 Great Britain Hockey Media Contacts: GB Hockey Communications Manager Craig Mortimer-Zhika Email: [email protected] Tel: +44 (0)7988 620992 Resources: Event Websites: Men: http://www.fih.ch/events/champions-trophy/2016-mens-champions-trophy Women: http://www.fih.ch/events/champions-trophy/2016-womens-champions-trophy Social media: The FIH will provide comprehensive coverage of the event via our social media channels, including Facebook, Instagram, Twitter and Snapchat. Facebook: facebook.com/fihockey Instagram: instagram.com/fihockey Twitter: twitter.com/fih_hockey Snapchat: fihockey Hashtags: #HCT2016 #BestOfTheBest In-Event Stats and Historical data: The FIH has created a dedicated website which provides a fascinating overview of the men’s and women’s Hockey Champions Trophy events. -

Connecticut Open – Semifinals (Friday)

DAILY MATCH NOTES: CONNECTICUT OPEN NEW HAVEN, CT, USA | AUGUST 19-25, 2018 | USD $799,000 PREMIER WTA Website: www.wtatennis.com | @WTA | facebook.com/wta Tournament Website: www.ctopen.org | @ConnecticutOpen | facebook.com/ConnecticutOpen WTA Communications: Bryan Shapiro ([email protected]) SAP Tennis Analytics for Media is an online portal that provides real-time data and insights to media during every WTA event and across all devices. Please email [email protected] to request your individual login to grant access to SAP Tennis Analytics for Media. CONNECTICUT OPEN – SEMIFINALS (FRIDAY) ARYNA SABALENKA (BLR #25) vs. [5] JULIA GOERGES (GER #9) Sabalenka leads 1-0 Sabalenka has now reached back-to-back SF, having reached final four at Cincinnati last week… Goerges, the sole seed left standing, is bidding to become the first German to reach the final at New Haven since Stefanie Graf defeated Jana Novotna for the title in 1998… Since the pair last played at Eastbourne at the end of June, Sabalenka has slashed her ranking from No.45 to No.25 CARLA SUAREZ NAVARRO (ESP #30) vs. [Q] MONICA PUIG (PUR #72) Suarez Navarro leads 4-1 Suarez Navarro, playing her first SF of the season, is the only player remaining yet to drop a set this week – indeed, she has needed to win just three sets to reach the last four… At No.72, Puig would become the lowest-ranked player to reach the final here, should she advance today… No player from Spain or Puerto Rico has won this title since the event moved to New Haven in 1998 POTENTIAL FINAL HEAD‐TO‐HEADS SUAREZ NAVARRO PUIG SABALENKA First meeting First meeting GOERGES Goerges leads 3‐2 Puig leads 3‐2 (2‐1 at tour level) WTA TV – LIVE ACTION FROM NEW HAVEN Every main draw match from New Haven is LIVE and ON DEMAND on wtatv.com. -

PLAYERS GUIDE — Shoal Creek | Birmingham, Ala

73RD U.S. WOMEN’S OPEN CHAMPIONSHIP PLAYERS GUIDE — Shoal Creek | Birmingham, Ala. — May 31-June 3, 2018 conducted by the 2018 U.S. WOMEN'S OPEN PLAYERS' GUIDE — 1 2018 U.S. Women’s Open Exemption List MARINAhttp://www.golfstats.com/gs_scripts/golfstats/golfstats.php?guide=2018wopen&style=&tour=LPGA&name=Marina+Alex&year=&tournament= ALEX &in=Search Marina Alex (9) Megan Khang (9) Azahara Munoz (9,12) Brittany Altomare (9) Hyo Joo Kim (7,9) Haru Nomura (9) Birth Date: August 02, 1990 Ashleigh Buhai (9) I.K. Kim (5,9,11) Anna Nordqvist (7,9) Pei-Yun Chien (9) Ji-Hyun Kim (12) Su-Hyun Oh (9) Birthplace: Wayne, N.J. Chella Choi (9) Sei Young Kim (8,9) Ryann O’Toole (9) Hye Jin Choi (8) Katherine Kirk (9) Inbee Park (1,4,5,9) Age: 27 Ht.: 5’3 Na Yeon Choi (1) Jin Young Ko (11,12) Jane Park (9) Kelsey Chugg (2) Lydia Ko (6,7,9) Sung Hyun Park (1,8,9,11) Home: Jupiter, Fl. In Gee Chun (1,7,9) Jessica Korda (9) Pornanong Phatlum (9) Carlota Ciganda (8,9,12) Nelly Korda (9) So Yeon Ryu (1,6,8,9) Cydney Clanton (9) Olafia Kristinsdottir (9) Madelene Sagstrom (9) College: Vanderbilt Jacqui Concolino (9) Candie Kung (9) Lizette Salas (9) Paula Creamer (1) Brittany Lang (1,9) Supamas Sangchan (13) Turned Professional: 2012 Austin Ernst (9) Saranporn Langkul Sophie Schubert (2) Jodi Ewart Shadoff (9) gasettrin (13) Alena Sharp (9) Joined LPGA Tour: 2014 Shanshan Feng (8,9,11) Nicole Broch Larsen (9) Erica Shepherd (2) Sandra Gal (9) JeongEun Lee (9) Jenny Shin (9) Laura Gonzalez Escallon Jeongeun6 Lee (8,12) Sarah Jane Smith (9) Player Notes: [ELIGIBILITY: 9] (9) Mihyang Lee (9,11) Jennifer Song (9) Georgia Hall (12) Min Young Lee (12) Klara Spilkova (12) Alex comes from a golf family.