\Ryest MORRIS REGIONAL HIGH SCHOOL DISTRICT

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

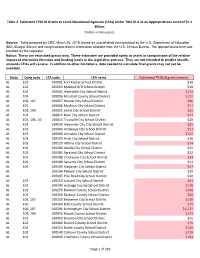

Page 1 of 283 State Cong Code LEA Code LEA Name Estimated FY2018

Table 2. Estimated FY2018 Grants to Local Educational Agencies (LEAs) Under Title IV-A at an Appropriations Level of $1.1 Billion Dollars in thousands Source: Table prepared by CRS, March 26, 2018, based on unpublished data provided by the U.S. Department of Education (ED), Budget Service and congressional district information available from the U.S. Census Bureau. The appropriations level was provided by the requester. Notice: These are estimated grants only. These estimates are provided solely to assist in comparisons of the relative impact of alternative formulas and funding levels in the legislative process. They are not intended to predict specific amounts LEAs will receive. In addition to other limitations, data needed to calculate final grants may not yet be available. State Cong code LEA code LEA name Estimated FY2018 grant amount AL 102 100001 Fort Rucker School District $10 AL 102 100003 Maxwell AFB School District $10 AL 104 100005 Albertville City School District $153 AL 104 100006 Marshall County School District $192 AL 106, 107 100007 Hoover City School District $86 AL 105 100008 Madison City School District $57 AL 103, 106 100011 Leeds City School District $32 AL 104 100012 Boaz City School District $41 AL 103, 106, 107 100013 Trussville City School District $20 AL 103 100030 Alexander City City School District $83 AL 102 100060 Andalusia City School District $51 AL 103 100090 Anniston City School District $122 AL 104 100100 Arab City School District $26 AL 105 100120 Athens City School District $54 AL 104 100180 Attalla -

Download, View and Print the Second Part of the Report As a Pdf File

Universe of Public Elementary and Secondary Education Agencies - Fall 2002 MONTANA / Page 203 Total 2001-02 Name of Agency Mailing Address Telephone Name of County Metro Grade Student Reg HS Spec Ed Teachers Sch's Street or P.O. Box City ZIP Number Status Span Membership Grads IEP Regular School Districts ABSAROKEE ELEM 327 S WOODARD AVE ABSAROKEE 59001 406-328-4583 STILLWATER 3 PK-08 237 † 39 17 2 ABSAROKEE H S 327 S WOODARD AVE ABSAROKEE 59001 406-328-4583 STILLWATER 3 09-12 121 33 8 11 1 ALBERTON K-12 SCHOOLS PO BOX 330 ALBERTON 59820 406-722-4413 MINERAL 3 PK-12 210 20 33 18 3 ALBION ELEM (NON-OP) HC 50 BOX 3 ALZADA 59311 406-828-4598 CARTER 3 N -N † † † † -2 ALDER ELEM PO BOX 110 ALDER 59710 406-842-5285 MADISON 3 PK-06 13 † † 2 1 ALZADA ELEM BOX 8 ALZADA 59311 406-828-4554 CARTER 3 PK-08 10 † 4 1 1 AMSTERDAM ELEM 6360 CAMP CREEK ROAD MANHATTAN 59741 406-282-7216 GALLATIN 3 KG-06 75 † 14 6 1 ANACONDA ELEM PO BOX 1281 ANACONDA 59711 406-563-8277 DEER LODGE 3 PK-08 927 † 162 58 4 ANACONDA H S PO BOX 1281 ANACONDA 59711 406-563-8277 DEER LODGE 3 09-12 476 90 62 26 1 ANDERSON ELEM 10040 COTTONWOOD ROAD BOZEMAN 59718 406-587-1305 GALLATIN 3 PK-08 184 † 15 14 2 ARLEE ELEM PO BOX 37 ARLEE 59821 406-726-3216 LAKE 3 PK-08 324 † 46 28 2 ARLEE H S PO BOX 37 ARLEE 59821 406-726-3216 LAKE 3 09-12 147 21 14 12 1 ARROWHEAD ELEM PO BOX 37 PRAY 59065 406-333-4359 PARK 3 PK-08 121 † 17 11 2 ASHLAND ELEM BOX 17 ASHLAND 59003 406-784-2568 ROSEBUD 3 PK-08 53 † 19 7 2 AUCHARD CREEK ELEM 9605 HWY 287 WOLF CREEK 59648 406-562-3528 LEWIS AND CLARK 3 PK-08 -

Allocations to Leas Under ESSER & GEER

Federal Emergency Aid for Public Education: Allocations to LEAs under ESSER & GEER ESSER Allocations to LEAs in New Jersey Across all three federal laws (CARES, CRRSA, and ARP), SEAs must use at least 90 percent of their grant awards to make subgrants to LEAs in proportion to the amount of funds that each LEA received under Title I, Part A in the most recent fiscal year. minimum DOE distribution to LEAs ESSER I Fund $279,334,092 ESSER II Fund 1,107,874,581 ARP ESSER Fund 2,488,128,933 Total, ESSER $3,875,337,606 GEER Allocations to New Jersey Both the CARES Act and CRRSA Act provided funding to Governors through the Governor’s Emergency Education Relief (GEER) Fund. The U.S. Department of Education is required to allocate 60 percent of the funds based on each state’s relative population of individuals aged 5 through 24, and 40 percent based on each state’s relative number of children counted under the Title I, Part A formula. GEER I Fund $68,864,994 GEER II Fund 29,926,370 Total, GEER $98,791,364 GEER funds may be used by the Governor of New Jersey in support of public elementary and secondary education, institutions of higher education (IHEs), or other education-related entities. A Governor has wide discretion in determining the entities in the State that will receive GEER funds. A Governor can choose to fund only LEAs, only IHEs, only education-related entities, or any combination of eligible entities. New Jersey Department of Education Elementary and Secondary School Emergency Relief (ESSER) Fund Local Education Agency (LEA) Allocations -

All Paths Lead to All Paths Lead To

AALLLL PPATHSATHS LLEADEAD TTOO ChesterChester •• ChesterChester Twp.Twp. HardingHarding Twp.Twp. MendhamMendham MendhamMendham Twp.Twp. Go Online to view this section! WashingtonWashington Twp.Twp. www.newjerseyhills.com Observer-Tribune RECORDER COMMUNITY NEWSPAPERS Informational Directory 2013-2014 THE INNOVATORS OF COMFORT™ There are recliners you sit in. Then there are those you escape to. Place a Stressless® recliner in any space and the room transforms into a haven of perfect comfort. Where tension gives way to relaxation. And the mind settles as placidly as the body. At the heart of the Stressless® experience are unique comfort systems that provide rejuvenating support across the entire body. Available in up to three sizes to create the perfect fit. www.ekornes.com Stressless® is proudly endorsed by the American Chiropractic Association. 151 ROUTE 31 FLEMINGTON, NJ • (908) 782-7662 • www.flemingtondepartmentstore.com ON LEFT 2 MILES NORTH OF THE FLEMINGTON CIRCLE • Store Hours: Mon.-Fri. 9am-8pm • Sat. 9am-6pm; Sun. 11am-5pm Deborah Herridge Call us TODAY for a consultation! REALTOR ® Direct: 201.400.2980 • Office: 973.539.1120 55 Madison Avenue • Morristown, NJ 07960 REALTOR ® www.TheHerridgeGroup.com Hesco has the keys to unlock Giorgios Pappas Furrier the beauty of your home with light. www.giorgiospappasfurrier.com • Indoor and Outdoor Lighting • Attic Cooling Fans (973) 425-1111 • Bath Cabinets • Landscape Lighting • Paddle Fans • Central Vacuums • cleaning & glazing • custom designs • cold storage • remodeling • repairs • re-sizing • relining Come See Our Be sure to visit Hesco for any of your household electrical needs, New Line! and ask about our whole-house and volume discounts. -

Form of Local Unit Facility Certificate, 4/11

LOCAL UNIT FACILITY ACCEPTANCE CERTIFCATE On behalf of the [__________________] (the “Local Unit”), and as a duly authorized officer of the Local Unit, I hereby represent, warrant and covenant as follows: 1. The Local Unit understands that it has been preliminarily selected by the Morris County Improvement Authority (the “Authority”) as one of the local government participants in the Authority’s 2011 Renewable Energy Program (the “Program”). The Local Unit further understands that although there is no legal agreement between the Authority and the Local Unit until such parties execute that certain “License and Access Agreement (Morris County Renewable Energy Program, Series 2011)” (a form of which “License Agreement” shall be supplied to the Local Unit by the Authority when the Program is closer to implementation), the information being provided to the Authority in this Certificate enables the Authority to draft the License Agreement, seek the necessary approvals, and otherwise implement the Program. 2. The License Agreement shall refer to the building(s) or ground(s) (each “Local Unit Facility”), location, size and scope (and if applicable, style) of the solar project (the “Renewable Energy Project”) to be implemented on behalf of the Local Unit by the Authority and its various contract parties, including a competitively selected solar developer (the “Company”). Various consultants to the Authority, based on site visits and past information supplied by the Local Unit to the Authority, have identified the Local Unit Facility(ies) and Renewable Energy Project(s) (which include solar overlays prepared by Authority consultants) set forth on Schedule A to this certificate for inclusion in the License Agreement, for selection of the Company, and for financing and implementation under the Authority’s Renewable Energy Program. -

Master FRS Certified Schools with County 6-3-20.Xlsx

FRS - NJ Certified Public Schools Listed in alphabetical order by County, School District, School Name County School District School Name Level Year Bergen Demarest School District Demarest Middle School Bronze 2018 - 2021 Bergen Demarest School District Luther Lee Emerson School Bronze 2018 - 2021 Bergen Hackensack Public Schools Fairmount School Bronze 2019 - 2022 Bergen Hackensack Public Schools Fanny Meyer Hillers Bronze 2018 - 2021 Bergen Hackensack Public Schools Hackensack High School Silver 2019 - 2022 Bergen Hackensack Public Schools Hackensack Middle School Silver 2019 - 2022 Bergen Hackensack Public Schools Nellie K. Parker Bronze 2018 - 2021 Bergen Northern Valley Regional High School District* Northern Valley Regional High School at Demarest Silver 2018 - 2021 Bergen Northern Valley Regional High School District* Northern Valley Regional High School at Old Tappan Silver 2018 - 2021 Bergen Norwood Public School Norwood Public School Bronze 2019 - 2022 Bergen Old Tappan School District Charles DeWolf Middle School Bronze 2017 - 2020 Bergen Park Ridge School District Park Ridge High School Bronze 2018 - 2021 Bergen Pascack Valley Regional High School District Pascack Hills High School Bronze 2017 - 2020 Bergen Pascack Valley Regional High School District Pascack Valley High School Bronze 2017 - 2020 Bergen Ramapo Indian Hills Regional High School District Indian Hills High School Bronze 2019 - 2022 Bergen Ramapo Indian Hills Regional High School District Ramapo High School Bronze 2019 - 2022 Bergen River Vale Public Schools Holdrum -

2020 List of Currently Certified Schools

2020 List of Currently Certified Schools ~ UPDATED 9/4/2020 ~ Certified schools and districts with at least one certified school do not have to provide the requested green team documentation in the grant application and will receive special consideration. 50% of the grant funds in this cycle will be reserved for awards to be given to certified schools and districts with at least one certified school. For those applying for a grant as a school…please review the list of certified schools to see if your school is currently certified in the Sustainable Jersey for Schools program. If your school is on the list, it is currently certified. For those applying for a grant as a district…please review the list of certified schools to see if at least one of the schools in your district are currently certified in the Sustainable Jersey for Schools program. You can also check the certification status of a school using the list view of the Participating Districts and Schools map located here on the Sustainable Jersey for Schools website. A preview of the list is shown below. If you have any questions about your certification status please contact Veronique Lambert, Schools Program Coordinator at 609-771-3427 or at [email protected]. LIST OF CERTIFIED SCHOOLS Current Certification County School Name District Name Level Atlantic Pennsylvania Avenue School Atlantic City Public Schools Bronze Atlantic Alder Avenue Middle School Egg Harbor Township School District Bronze Atlantic Clayton J. Davenport Elementary School Egg Harbor Township School District Bronze Atlantic Dr. Joy Miller Elementary School Egg Harbor Township School District Bronze Atlantic E.H. -

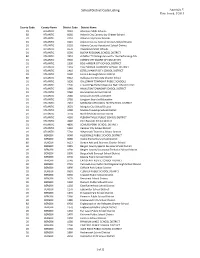

Appendix V Date Issued: 5/2015

School District Code Listing Appendix V Date Issued: 5/2015 County Code County Name District Code District Name 01 ATLANTIC 0010 Absecon Public Schools 80 ATLANTIC 6060 Atlantic City Community Charter School 01 ATLANTIC 0110 Atlantic City Public Schools 01 ATLANTIC 0125 Atlantic County Special Services School District 01 ATLANTIC 0120 Atlantic County Vocational School District 01 ATLANTIC 0570 Brigantine Public Schools 01 ATLANTIC 0590 BUENA REGIONAL SCHOOL DISTRICT 80 ATLANTIC 7410 chARTer~TECH High School for the Performing Arts 01 ATLANTIC 0960 CORBIN CITY BOARD OF EDUCATION 01 ATLANTIC 1300 EGG HARBOR CITY SCHOOL DISTRICT 01 ATLANTIC 1310 EGG HARBOR TOWNSHIP SCHOOL DISTRICT 01 ATLANTIC 1410 ESTELL MANOR CITY SCHOOL DISTRICT 01 ATLANTIC 1540 Folsom Borough School District 80 ATLANTIC 6612 Galloway Community Charter School 01 ATLANTIC 1690 GALLOWAY TOWNSHIP PUBLIC SCHOOLS 01 ATLANTIC 1790 Greater Egg Harbor Regional High School District 01 ATLANTIC 1940 HAMILTON TOWNSHIP SCHOOL DISTRICT 01 ATLANTIC 1960 Hammonton School District 01 ATLANTIC 2680 Linwood City School District 01 ATLANTIC 2780 Longport Board of Education 01 ATLANTIC 2910 MAINLAND REGIONAL HIGH SCHOOL DISTRICT 01 ATLANTIC 3020 Margate City School District 01 ATLANTIC 3480 Mullica Township School District 01 ATLANTIC 3720 Northfield City School District 01 ATLANTIC 4180 PLEASANTVILLE PUBLIC SCHOOL DISTRICT 01 ATLANTIC 4240 Port Republic School District 01 ATLANTIC 4800 SOMERS POINT SCHOOL DISTRICT 01 ATLANTIC 5350 Ventnor City School District 01 ATLANTIC 5760 Weymouth Township -

Carahsoft Technology Corp

CARAHSOFT’S RESPONSE TO THE The Cooperative Purchasing Network REQUEST FOR PROPOSAL Software and Related Products and Services SOLICITATION NO. 15-04 Tuesday March 3, 2015 CARAHSOFT TECHNOLOGY CORP. 12369 SUNRISE VALLEY DRIVE RESTON, VA 20191 888.66.CARAH | WWW.CARAHSOFT.COM carahsoft March 3, 2015 TCPN Region 4 ESC Office 7145 West Tidwell Road Houston, TX 77092 Re: Carahsoft’s Response to The Cooperative Purchasing Network’s Request for Proposal for Software and Related Products and Services, Solicitation # 15-04 Dear Mr. Zingelmann, Carahsoft Technology Corporation appreciates the opportunity to respond to The Cooperative Purchasing Network (TCPN)’s Request for Proposal for Software and Related Products and Services. Carahsoft is proposing its entire product line, which fully meets TCPN’s requirements for Software and Related Products and Services. Our team has considered TCPN’s requirements outlined in the Request for Proposal, and has carefully put together a solution that will best meet your needs. Carahsoft is submitting as a current TCPN contract holder (#R5011) and top rated IT reseller and distributor. Carahsoft has utilized the TCPN contract to sell over $3,000,000 in IT products and services to various agencies. Carahsoft has delivered best value solutions to our government and education clients for over ten years, including Region IV and TCPN’s member agencies. In fact, Carahsoft has delivered almost $100,000,000 in sales to Education agencies in 2014, and has completed $15,000,000 of those sales in the State of Texas. Please feel free to contact me directly at 703.230.7545/[email protected] or Robert Moore at 703.871.8504/[email protected] with any questions or communications that will assist TCPN in the evaluation of our response.