参照文献 Philippine Statistical Yearbook, National Statistical

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Submission of Proposals: Application Form

Submission of Proposals: Application Form. Please read carefully the "Guidelines for the Submission of Proposals" which outline the modalities for application and the criteria for the selection of proposals spelled out in the Cities Alliance Charter. Please ensure that all necessary supporting documentation is attached to this form. Additional information may also be enclosed, but total submission should not exceed 12 pages. DATE: rec’d 15 November 2010 1. TITLE of PROPOSAL: Developing a National Slum Upgrading Strategy for the Philippines 2. PROPOSAL SUBMITTED BY1: Name and Title: Nestor P. Borromeo, Secretary General Organization : Housing and Urban Development Coordinating Council Address: 15F, BDO Plaza, Makati Avenue, Makati City Telephone/Fax/E-mail: (0632) 811-4168, Name and Title: Wendel Avisado, Deputy Secretary General Organization : Housing and Urban Development Coordinating Council Address: 15F, BDO Plaza, Makati Avenue, Makati City Telephone/Fax/E-mail: (0632) 811-4116, [email protected] 3. CITIES ALLIANCE MEMBER(S) SPONSORINGTHE APPLICATION: Name and Title: Christopher T. Pablo, Senior Operations Officer and Task Team Leader Organization : The World Bank Office Manila Address: 20/F, Taipan Place, Emerald Ave., Ortigas Center, Pasig City,Metro Manila, Philippines Telephone/Fax/E-mail: +632-917-3065/632-937-5870/ [email protected] Name and Title: Organization : Address: Telephone/Fax/E-mail: 4. RECIPIENT ORGANISATION: – organization that will receive and execute the grant: Task Manager Name & Title: Wendel Avisado, Deputy Secretary General Organization : Housing and Urban Development Coordinating Council Address: 15F, BDO Plaza, Makati Avenue, Makati City Telephone/Fax/E-mail: (0632) 811-4168 5. OTHER IMPLEMENTING PARTIES (if any): Name & Title: Organization: Address: Contact Person/Title: Telephone/Fax/E-mail: 1 Country-specific proposals typically originate from local authorities, but must be sponsored by at least one member of the Cities Alliance (see Cities Alliance Charter, Section D.14). -

Conference Proceedings

Mobilizing Aid for Trade: Focus Asia and the Pacific 19–20 September 2007, ADB Headquarters, Manila, Philippines Conference Proceedings Mobilizing Aid for Trade: Focus Asia and the Pacific Conference Proceedings Co-hosted by the Asian Development Bank, the Philippine Government, and the World Trade Organization 19–20 September 2007, ADB Headquarters, Manila, Philippines © 2008 Asian Development Bank All rights reserved. Published 2008. Printed in the Philippines. The views expressed in this book are those of the authors and do not necessarily reflect the views and policies of the Asian Development Bank (ADB) or its Board of Governors or the governments they represent. ADB does not guarantee the accuracy of the data included in this publication and accepts no responsibility for any consequence of their use. Use of the term “country” does not imply any judgement by the authors or ADB as to the legal or other status of any territorial entity. Foreword FOREWORD Aid for Trade is important. At this critical juncture for global trade, it promises help for countries still isolated from the emerging global trading system—particularly the least-developed and small states—to meet the adjustment costs of opening up their markets. t will help them build the capacity to trade effectively, with donor support coordinated through partnerships with institutions like the World Trade Organization (WTO) and multilateral development banks. Launched in December 2005 at the WTO’s ministerial conference in Hong Kong, China, Aid for Trade is defined as aid for developing countries to build supply-side capacity and trade-related infrastructure to expand trade. From its outset, it was envisioned as a complement, and not a substitute, to the Doha Development Round of the WTO. -

LSDE September 01, 2020

Leyte-Samar DAILYPOSITIVE EXPRESS l FAIR l FREE VOL. XXXI I NO. 073 TUESDAY, SEPTEMBER 1, 2020 P15.00 IN TACLOBAN As health workers getting COVID-19 infection Alfred calls DOH JOEY A. GABIETAto fix protocols TACLOBAN CITY- Mayor Alfred Romual- Samar student dez has called on the Department of Health (DOH) to improve its system to ensure that no uses local fern health workers would further be infected of the coronavirus disease (COVID-19). to create portraits Romualdez said that tract tracing, we have seen TACLOBAN CITY- during this time of pan- based on the report he has most of the transmissions Who would want to have demic,” he said. received from the contact are coming from health his or her portraits to be While the village where tracers of the city, many workers which led to trans- made out of leaves from a the young artist wanna-be health workers have be- mission to their houses and fern? lives, Barangay Binalayan, come sources of the virus, close contacts. So we have This was exactly what remain to be COVID-19 infecting their loved ones to address this immediately Ryan Managaysay, a 21-year free, the town of Tarang- and those that they are in- once and for all,” Romual- old second-year student nan is considered to be one teracting. dez said in a press confer- taking up education major of the hot spot areas in Sa- As of the latest count, ence Monday (August 31). in Social Sciences at the Sa- mar province of the dread- there are about 27 health “My concern is it’s not mar State University (SSU), ed virus. -

Aid Money Drying Up

Aid money drying up Daily Tribune - Published 2 days ago on April 27, 2020 12:07 AM By Hananeel Bordey Photo credit: Facebook page — Department of Social Welfare and Development @dswdserves As a result of the enhanced community quarantine (ECQ) in Metro Manila and other hotbeds of the coronavirus disease 2019 being stretched until 15 May, relief money is about to run out, Department of Social Welfare and Development (DSWD) Secretary Rolando Bautista said. Bautista, on Sunday, indicated that funds for the Social Amelioration Program (SAP) given to the country’s poor is fast being depleted and the remaining resources will have to be distributed only to those who badly needed assistance. Under SAP, the government distributed P8,000 to each poor family in Metro Manila and P5,000 per household in the provinces. “The implementation of the SAP only to beneficiaries in ECQ areas is in consideration with the budget availability,” he said. Bautista referred to the statements of Department of Finance (DoF) Secretary Carlos Dominguez and Department of Budget and Management (DBM) Secretary Wendel Avisado during a recent briefing led by President Rodrigo Duterte where both officials said only P45 billion remains of available funds after the government spent P352.7 billion for SAP in the ECQ’s initial one-and-a-half month scheduled to end 30 April. Only in ECQ areas “The bottomline there is really the budget intended for the succeeding days of the quarantine period is running short,” Bautista said. Under the new directive announced by the government, ECQ will be retained until mid-May in Metro Manila, Benguet, Pangasinan, Bataan, Bulacan, Nueva Ecija, Pampanga, Tarlac, Zambales, Batangas, Laguna, Cavite, Rizal, Quezon, Oriental Mindoro, Occidental Mindoro, Albay and Catanduanes, Davao del Norte and Davao City. -

24Th Issue Mar. 2

“Radiating positivity, creating connectivity” March 2 - March 8, 2020 P15.00 CEBU Volume 2 Series 24 12 PAGES BUSINESS Room 310-A, 3rd floor WDC Bldg. Osmeña Blvd., Cebu City WEEK You may visit Cebu Business Week Facebook page. Yap wants 50-50 share in budget Bohol guv urges RDC to review budget share of LGUs Bohol Governor Arthur national agencies such as Yap has urged the Regional Department of Agriculture Development Council (RDC) (DA) and the Department of 7 to analyze how much is the Public Works and Highways budget for national agencies (DPWH). and how much for local “How much is the RDC government units in the 7 and the Local Government total amount it endorsed for Units (LGUs) get their way inclusion in annual General to the national budget or Appropriations Acts (GAAs). inclusion in the GAA?” Speaking during the Yap asked. He echoed the RDC Full Council meeting statement of Carreon that last Feb. 28, 2020, Yap was only 15 percent of what the among those informed by RDC 7 endorsed got it to the Efren Carreon, National GAA 2020. Economic and Development Yap said that was Authority (NEDA) 7 director the reason he once asked Bohol Governor Arthur Yap (extreme right) during the full council meeting of the Regional Development (RDC) last and RDC 7 co-chairman, that Department of Budget Feb. 28, 2020 at Mezzo Hotel, Cebu City. Others in photo are (left to right) Cebu City Mayor Edgar Labella, RDC 7 of the P633 billion RDC 7 has Secretary Wendell Avisado Co-Chair Kenneth Cobonpue, and NEDA 7 and RCC 7 Co-Chair Director Efren Carreon. -

2020 1St Quarter Report

JANUARY 06 2020 National Budget Passed into Law President Rodrigo Roa Duterte signed into law the Fiscal Year (FY) 2020 General Appropriations Act (GAA) on January 6, 2020. The 4.1-trillion Budget, which carries the theme “Continuing the journey to a more peaceful and progressive Philippines”, is 12 percent higher than the FY 2019 National Budget. It builds on the gains made over the first three and a half years of the Duterte Administration by continuing the thrust for genuine change, inclusive growth, and equitable development for the country and the Filipino people. The 2020 National Budget will sustain the critical infrastructure, human capital development, and peace and order initiatives of the Administration to support socio-economic growth. 2 3 Salary increase for gov’t workers implemented President Rodrigo Roa Duterte has signed into law a measure that increases the take-home pay of government employees, including teachers RA 11466 and nurses. Republic Act (RA) No. 11466 , otherwise known R.A. 11466 as the “Salary Standardization Law (SSL) of 2019,” was enacted on January 8, 2020. With this, civilian government employees will benefit from another round of salary increases starting January 2020 until 2023. The salaries, particularly of those in the rank-and-file, will be brought closer to, if not higher than, market-rate levels. The SSL 5 likewise institutionalized the grant of the Mid-Year Bonus, which is equivalent to one month basic salary. JANUARY 08 JANUARY Duterte Administration’s budget priorities tackled in DBM’s Budget Fora These Budget Fora have been an annual event of the DBM to set the parameters and procedures that will guide various offices/ agencies in the execution of the 2020 National Budget and the preparation of their respective proposed budgets for 2021. -

Change in Schedule of Pre-SONA Forum 2020

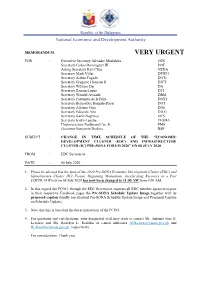

Republic of the Philippines National Economic and Development Authority MEMORANDUM VERY URGENT FOR : Executive Secretary Salvador Medialdea OES Secretary Carlos Dominguez III DOF Acting Secretary Karl Chua NEDA Secretary Mark Villar DPWH Secretary Arthur Tugade DOTr Secretary Gregorio Honasan II DICT Secretary William Dar DA Secretary Ramon Lopez DTI Secretary Wendel Avisado DBM Secretary Fortunato de la Peña DOST Secretary Bernadette Romulo-Puyat DOT Secretary Alfonso Cusi DOE Secretary Eduardo Año DILG Secretary Karlo Nograles OCS Secretary Isidro Lapeña TESDA Undersecretary Ferdinand Cui, Jr. PMS Governor Benjamin Diokno BSP SUBJECT : CHANGE IN TIME SCHEDULE OF THE “ECONOMIC DEVELOPMENT CLUSTER (EDC) AND INFRASTRUCTURE CLUSTER (IC) PRE-SONA FORUM 2020” ON 08 JULY 2020 FROM : EDC Secretariat DATE : 06 July 2020 1. Please be advised that the time of the 2020 Pre-SONA Economic Development Cluster (EDC) and Infrastructure Cluster (IC) Forum: Regaining Momentum, Accelerating Recovery in a Post COVID-19 World on 08 July 2020 has now been changed to 11:00 AM from 9:00 AM. 2. In this regard, the PCOO, through the EDC Secretariat, requests all EDC member agencies to post in their respective Facebook pages the Pre-SONA Schedule Update Image together with its proposed caption (kindly see attached Pre-SONA Schedule Update Image and Proposed Caption on Schedule Update). 3. Note that this is based on the latest instruction of the PCOO. 4. For questions and clarifications, your designated staff may wish to contact Mr. Antonio Jose G. Leuterio and Ms. Rodelyn L. Rodillas at e-mail addresses [email protected] and [email protected], respectively. -

President Rodrigo Duterte's Economic Team

Received by NSD/FARA Registration Unit 07/31/2020 6:07:26 PM Media Releases (February to June 2020) 1. March 16 Media Release: Philippine DoF pledges over USD525 million to support health authorities and provide economic relief during COVID-19 March 16, 2020 PRESS RELEASE Gov’t economic team rolls out P27.1 B package vs COVID-19 pandemic President Rodrigo Duterte’s economic team has announced a P27.i-billion package of priority actions to help frontliners fight the 2019 coronavirus disease (COVID-19) pandemic and provide economic relief to people and sectors affected by the virus-induced slowdown in economic activity. The package consists of government initiatives to better equip our health authorities in fighting COVID-19 and also for the relief and recovery efforts for infected people and the various sectors now reeling from the adverse impact of the lethal pathogen. Finance Secretary Carlos Dominguez III, who chairs the Duterte Cabinet's Economic Development Cluster (EDC), said on Monday the measures in the package “are designed to do two things: First is to ensure that funding is available for the efforts of the Department of Health (DOH) to contain the spread of COVID-19. Second is to provide economic relief to those whose businesses and livelihoods have been affected by the spread of this disease.” “As directed by President Duterte, the government will provide targeted and direct programs to guarantee that benefits will go to our workers and other affected sectors. We have enough but limited resources, so our job is to make sure that we have sufficient funds for programs mitigating the adverse effects of COVID-19 on our economy,” he added. -

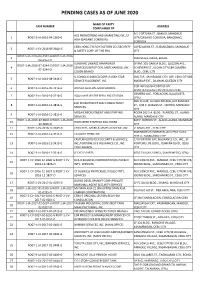

Pending Cases As of June 2020

PENDING CASES AS OF JUNE 2020 NAME OF PARTY CASE NUMBER ADDRESS COMPLAINED OF A.S. FORTUNA ST., BAKILID, MANDAUE ACE PROMOTIONS AND MARKETING INC./LF 1 RO07-2-JA-2016-04-2589-G CITY/GAISANO CORDOVA, BANGBANG, ASIA (GAISANO CORDOVA) CORDOVA CEBU HONG TIN SOY FACTORY CO./SECURITY LOPEZ JAENA ST., SUBANGDAKU, MANDAUE 2 RO07-1-CV-2016-05-2810-G & SAFETY CORP. OF THE PHIL CITY RO07-5-JA-2016-06-2952-G RO07-5-JA-2016- 3 MARIVELES, DAUIS, BOHOL 06-2952-O SUNSHINE LINKAGE MANPOWER 3F RM. 301 GARCIA BLDG., QUEZON AVE., RO07-1-JA-2016-07-3244-G RO07-1-JA-2016- 4 SERVICES/UNITOP GEN. MERCHANDISE, INC. - ECHEVERRI ST., ILIGAN CITY/184 OSMEÑA 07-3244-O COLON BRANCH BLVD., CEBU CITY IL CONIGLIO BIANCO CORP./LUCKY STAR 2ND FLR., SM SEASIDE CITY, SRP, CEBU CITY/85 5 RO07-1-JA-2016-08-3441-G SERVICE PLACEMENT, INC. MASIKAP EXT., DILIMAN, QUEZON CITY COR.INAYAGAN-CANTAO-AN 6 RO07-2-JA-2016-09-3516-G BOJANA GENERAL MERCHANDISE ROAD,INAYAGAN,CITY OF NAGA,CEBU OSMEÑA AVE., POBLACION, DALAGUETE, 7 RO07-2-JA-2016-10-3718-G AQUA MAE WATER REFILLING STATION CEBU 2ND FLOOR, LA CHEF ARCADE, 607 ZAMORA JASI RECRUITMENT AND CONSULTANCY 8 RO07-1-JA-2016-12-3814-G ST., COR P. BURGOS ST., CENTRO, MANDAUE SERVICES CITY MOZAIC RECRUITMENT AND STAFFING ROOM 202 S.A. BLDG., PLARIDEL ST., ALANG- 9 RO07-1-JA-2016-12-3815-G SERVICES ALANG, MANDAUE CITY RO07-1-JA-2016-12-3816-G RO07-1-JA-2016- 829 P. -

Secure Meds Via Hi-Tech

Headline Secure meds via hi-tech MediaTitle Philippines Daily Tribune(www.tribune.net.ph) Date 18 Sep 2019 Section NEWS Order Rank 2 Language English Journalist N/A Frequency Daily Secure meds via hi-tech Health Secretary Francisco Duque III, in turn, assured lawmakers that there are no expired medicines as of the moment as the drugs were already cascaded to DoH regional offices which will be distributed to the provincial hospitals. The use of advanced technology or computerization was pushed yesterday as a solution to the overstocking of medicine, worth P367.158 million, that the Commission on Audit recently reported were close to expiry. Senator Christopher Lawrence “Bong” Go, who presided over the budget deliberations on the P160- billion budget of the Health Department along with Senators Nancy Binay and Cynthia Villar flagged the inefficient system of the Department of Health (DoH) in stocking medicines in warehouses. “Secretary Duque, who determines the medicine that we need and procure, especially in hospitals because we notice that you are letting the medicines expire inside the warehouses. I think there is a problem in the way or the system of distribution,” Go told DoH officials. Subsequently, Villar asked if they are using a computerized system in handling and monitoring the stock medicines. “In the procurement, we already have the Procurement Operations and Management Information System but with regards to the SCMO (Supply Chain Management Office), we are now creating an end-to-end information system,” Undersecretary Myrna Cabotaje told the panel. DoH warned Villar, for her part, was not convinced of DoH’s vow to improve its operations and further explained that given the P19 billion requested budget for medicines in 2020, the agency’s inventory should already be computerized. -

Cebu Province Government Directory 2012

PROVINCIAL ACCOUNTANT’S OFFICE Assessment Operations Evaluation Mechanical Division PROVINCIAL OFFICES G/F East Wing, Cebu Capitol Head: Alma Sibonga Tel.: 2533987 Tel.: 2539065 / 2541139 / 2555135 Assessment Records Mgt. Section Head: Head: Emmanuel Guial Head: Dolores Esmero Property Section PROVINCIAL GOVERNOR’S OFFICE Internal Audit Section Property Valuation-Assessment Tel: 2533105 2/F East Wing, Cebu Capitol Tel.: 2539063/ 2554071 Standard Examination Section Head: Edgar Bajares Tel.: 2531970 / 2536070/ 2539613/ Head: Emmanuel Guial 2541882 / 2543399/ 2550642 (fax) PROVINCIAL AUDITOR’S OFFICE Prov’l. Waterworks Devt. Task Force HON. GWENDOLYN F. GARCIA PROVINCIAL ADMINISTRATOR’S OFFICE 2/F Baex Bldg., Capitol Cmpd., Cebu City Tel. 2533105 / 2533977 PROVINCIAL GOVERNOR 2/F East Wing, Cebu Capitol Tel.: 2538180 / 2538192 Prov’l. Roads & Bridge Maintenance Exec. Asst.V: Elizabeth C. Francia Tel.: 2541629/ 2548842 (fax) Head: Barbara Ann H. Aloba Division Prov’l. Administrator: Mr. Eduardo T. Habin 3/F West Wing, Cebu Capitol Secretary: Amor Sarmiento PROVINCIAL BUDGET OFFICE Administrative Division Human Resource Management Division Head: Engr. Rodel Arreza 2/F West Wing, Cebu Capitol, Cebu City 2/F East Wing, Cebu Capitol Tel.: 2556123 2/F East Wing, Cebu Capitol Tel.: 2538576/ 4165836 Tel.: 2553896 / 2556004 / 4165723 Motorpool Section Tel.: 2543399 Head: Emmy Gingoyon Head: Elizabeth C. Francia Head: Noli Vincent A. Valencia DA Compound, M.Velez St., Cebu City Information & Technology Office Records Section PROV’L. EMPLOYMENT & SERVICES OFFICE Tel. 2533987 G/F BAEx Bldg., Capitol Cmpd. Tel.: 2533975 G/F Cebu Capitol, Cebu City Head: Noli Vincent Valencia Head: Elizabeth C. Francia Tel.: 2535710/ 2556235 PROV’L. ENVIRONMENT & Sugbo News Head: Dr. -

Economic-Nationalism-Conference

NNAATTIIOONNAALL CCOO NNFFEERREENNCCEE ““AA NNaattiioonn iinn CCrriissiiss:: AAggeennddaa ffoorr SSuurrvviivvaall”” JJaannuuaarryy 2222- -2233,,, 22000033 CCllluubb FFiiillliiippiiinnoo,,, GGrreeeennhhiiillllllss,,, SSaann JJuuaann DDooccuummeennttaattiioonn ooff PPrroocceeeeddiinnggss F AIR T RADE REPUBLIC OF THE PHILIPPINES OFFICE OF THE VICE-PRESIDENT A LLIANCE 2 Documentation of Proceedings National Conference on A Nation in Crisis: Agenda for Survival 3 NATIONAL CONFERENCE “A Nation in Crisis: Agenda for Survival” January 22-23, 2003 Club Filipino, Greenhills, San Juan Background and Rationale of the Conference In December 2002, the Convenors of the Fair Trade Alliance (FTA) held a dialogue with Vice President Teofisto Guingona and his staff. What came out of the dialogue was the crystallization of a grim reality -- the gravity of the present national economic crisis and the threats of more conflict-laden divisions in Philippine society. However, there was also a consensus that the crisis is rooted primarily in the failure by the Philippine economic policy makers to pursue an independent and nationalist program of economic development. Unlike what the leaders of our successful neighboring Asian countries did, our economic policy makers, the neo-liberal technocrats in particular, abandoned nationalism in favor of a narrow type of agro- industrial development model dependent on the exportation of light export products, the uncertain flow of foreign investments and a high level of dependence on foreign borrowings. The performance of