Authority Monitoring Report 2017 (2015/16)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

North Tyneside Strategic Traffic Model Modelling Technical Note February 2015

North Tyneside Strategic Traffic Model Modelling Technical Note February 2015 North Tyneside Strategic Contents Traffic Model February 2015 Contents 1. Introduction 1 1.1 Commission 1 1.2 A19 HAM 1 2. Review of A19 HAM 4 2.1 Origin-Destination Data 4 2.2 Estimates of Delay 4 2.3 Network Coding 4 2.4 General Issues 4 3. Development of Base Model 5 3.1 Network and Matrix Coding 5 3.2 Analysis of Model Output 5 3.3 Matrix Estimation 5 4. Future Year Trip Matrices 6 4.1 Forecasting 6 4.2 Distribution 6 4.3 Trip Generation 6 5. Development of Do-Minimum Model 7 6. Analysis of Impacts 9 6.1 Network Improvement Schemes 9 6.2 Impacted Junctions 9 7. Limitations of Study 11 7.1 Origin-Destination Data 11 7.2 Wider Calibration 11 7.3 Transport Improvements 11 7.4 Development Trips 11 7.5 Capacity Analysis 11 7.6 Improvement Schemes 12 7.7 Next Steps 12 Appendices Appendix A i North Tyneside Strategic Traffic Model February 2015 1/ Introduction 1. Introduction 1.1 Commission Capita have been commissioned by North Tyneside Council to develop the existing A19 Highway Assignment Model (HAM) – developed for the HA by Arups in 2013 – to provide a model that calibrates successfully against observed traffic flow and journey time data for North Tyneside. The model is to be used initially in assessing the impacts on the highway network of the future developments identified in the draft North Tyneside Local Plan – together with those granted planning permission since the development of the A19 HAM. -

Whitfield Green Benton

Whitfield Green Benton An excellent choice of 2, 3, 4 & 5 bedroom homes Affordable homes 3 bedroom homes 4 bedroom homes 5 bedroom homes AA22 The Aldenham The Downham The Lindale The Lavenham Plots: 18-30 3 bedroom 4 bedroom 4 bedroom 5 bedroom detached home detached home detached home detached home Plots: 5, 14, 33, 46, 54 Plots: 10, 11, 13, 34, Plots: 1, 58, 60, 71 Plots: 3, 9, 37, 41, 43, PA30 40, 55, 62, 64, 69 52, 53, 59, 68 Plots: 15-17, 31, 32 The Shelford The Eynsham 4 bedroom The Wilton *ah affordale homes 4 bedroom detached home 5 bedroom detached home Plots: 45, 50, 66 detached home Plots: 2, 4, 8, 12, 36, Plots: 39, 42, 44, 49, 38, 47, 51, 57, 65, 70 61, 67 The Haddenham 4 bedroom detached home Plots: 6, 7, 35, 48, 56, 63 Hello. You’ll find our showhomes VP and sales office right here 7 VP 8 VP VP 9 6 5 10 4 VP 3 33 VP Welcome to VP 34 11 VP 2 VP VP 35 VP 1 36 VP 12 Whitfield 58 45 71 13 Green 57 60 14 59 44 70 37 Ideally located in the popular Newcastle 56 15 63 *ah VP 15 suburb of Benton, Whitfield Green 69 61 16 38 15 55 43 *ah 16 offers an excellent choice of 2, 3, 4 & 5 17 41 16 *ah 17 62 40 VP bedroom homes. 68 54 17 39 18 *ah VP 18 19 The local area offers all of the amenities you could need for daily life – including 42 *ah 19 VP 53 20 24 hour supermarkets, convenience stores, pubs, cafés and a selection of *ah 20 restaurants, as well as a nearby post office and a choice of schools. -

Recalling Earl, King of the Rink

36 The Northern Echo Saturday, February 26, 2011 Local Heroes Saturday, February 26, 2011 The Northern Echo 37 Football Football Sunderland and District Cameron lost 6-2 at home BACKTRACK BRIEFS against Billingham Veterans. Steels SC Over 40s The Marden Inn are doing well, Silks they defeated Darsley Park 4-1 Recalling Earl,king of the rink TUESDAY’S column was suggests. League at home. They are now in fifth headed “One wedding, two The original 10in x 8in funerals.” Tom Harvey seeks drawing is by someone N THE Robson Cup quarter- place and still have an excellent chance of gaining promotion. an equaliser. called Captain Wade and quit final Marden defeated Ryhope I Premier League Hartlepool lad and very proud appeared in the Echo, Foresters 6-2 at home. PW LD FAPts HILLING out as al- of it, Tom’s a life member of though it may well have Marden’s Ferencs Deverdics Heaton Stannington . .14 12 2042 13 38 Durham FA and still been the Sunderland Echo. scored four goals and Lowther Steels SC . .14 10 2235 23 32 ways, recent BACKTRACK refereeing at 78. “Not so As well as the reference to league Touchdown Hotel . .19 847332728 and Payne netted one apiece. columns have been much now,” he concedes, Marden’s keeper Ian Hall Blackhall Hardwick . .1681731 27 25 Tootie playing for Ferryhill Greyhound . .12 732281024 recalling the early, “but I still have my boots brilliantly saved a spot-kick. Cembryonic, master- Hartlepools, the observant Marden . .13 724302123 By polished for charity games Wearside League preview Red House WMC played Chilton WMC . -

North Tyneside Community Infrastructure Levy Area Wide

1.1 1.2 North Tyneside Community Infrastructure Levy Area Wide Viability Assessment 2018 PAGE INTENTIONALLY LEFT BLANK North Tyneside Local Plan Area Wide Viability Assessment CIL Update, 2018 1. Introduction ......................................................................................................................... 4 Previous area wide viability assessments .......................................................................... 4 Viability assessment to inform CIL submission and Proposed Modifications ................... 4 2. The Role and Scope of the North Tyneside Viability Assessment ....................................... 5 Proposed “key outcomes” for the North Tyneside Area Wide Viability Assessment ....... 6 3. The Assessment Methodology ............................................................................................ 8 4. Summary of evidence informing the proposed Community Infrastructure Levy ............. 10 Neighbouring Local Authorities – The duty to co-operate ............................................... 15 5. Residential Housing Market Analysis ................................................................................ 17 Understanding sales values by floor area and location ................................................... 25 6. The Viability Assessment – Assumptions and Development Typology ............................. 27 7. Benchmarking the AWVA .................................................................................................. 40 8. Residential Appraisal Outcomes ....................................................................................... -

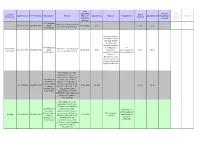

Section 106 - July 2017 Monies Received and Not Yet Spent Sub (All)

Section 106 - July 2017 Monies Received and not yet spent Sub (All) Roy Rachael Mark Sam CCG (James Colin Sam Sam Paul Paul Colin LEAD OFFICER Marsden Sam Dand Steve Bishop Steve Bishop Coyne Barrett Dand Martin) MacDonald Dand Dand Youlden Youlden MacDonald Sum of Amount Employ- Environ- Third Affordable Community Cultural ment mental Highway Open Parks & Sports Party Travel Development Housing Allotments Facilities Facilities/Works Education Initiatives Works Health care Works Spaces Playsites Recreation Facilities Works Provisions Grand Total Comments Environmental Works - £56k originally allocated for biodiversity at Silverlink Park and Waggon way. £27k remaining 00/02134/S106 - Collingwood Ward (S0056) - which is drawn down for Plot 6, Cobalt Business Park, Silver Fox Way, infrastructure and biodiversity Wallsend - Highbridge - 00/01360/FUL -27,000 -27,000 projects. No end deadline. 02/03264/S106 - Chirton Ward (S0008) - Land Parcels West of First Avenue and North of Travel Provisions - Held pending Second Avenue Off Narvik Way Tyne revised proposals for TTTE Tunnel Trading Estate North Shields - following completion of 2nd Tyne UK Land Estates (Partnership) Ltd - Tunnel & associated highway 02/00566/FUL -7,500 -7,500 works Highways - The spend will be utilised to supplement the proposed highway improvement works on the A188 / A189 corridor (Westmoor Roundabout 03/02991/S106 -Longbenton Ward (S0011) - to Weetslade Roundabout). Land at Gosforth Park Way Gosforth Business Options currently being Park - Beazer Homes Ltd - 03/01832/FUL -

Ward Profile of of Benton Ward Is 10,264 Benton Ward

The usual resident population Ward Profile of of Benton Ward is 10,264 Benton Ward Ward Description Benton ward includes the areas of Benton, Forest Hall and the ‘Manors’ estate adjacent to Coach Lane. The northern boundary is provided by Great Lime Road and the Southern boundary by the Northumbria University (Coach Lane Campus) and Tyneview Park. The eastern boundary heads north up past Darsley Park, across Whitley Road and behind (but not including)the Bellway Industrial Estate, with its final point along Bamburgh Road and onto Great Lime Road. The western boundary runs along Fir Tree Farm and past (but not including) Benton Dene Primary School, it then heads to Benton Metro Station (including St Bartholomew’s church on the way – but not St Andrew’s), after a short spell on Station Road it follows the metro line to Four Lane Ends and then continues for a short distance down Benton road as far as Manor Road where it carries on to Coach Lane. Benton ward’s neighbours are Longbenton ward (W), Northumberland ward (SE), Killingworth (NE) and Camperdown (NW). Select Ward Benton Produced by Policy, Performance & Research Dear Reader This document aims to provide a collection of information to give an overview of the ward. It is designed to offer quick and easy access to regularly requested data. It is updated on an annual basis where most recent data will be provided with comparisons where appropriate. Large elements of the information contained in this booklet has been obtained from the Office of National Statistics (ONS) and is based on census data. -

North Tyneside Council Local Plan

North Tyneside Council Local Plan Habitat Regulations Assessment - Appropriate Assessment Addendum January 2017 Contents 1. Introduction .......................................................................................................................................................................................................... 3 2. Assessment of Vision, Objectives and Policies ..................................................................................................................................................... 4 3. Assessment of Supporting Text .......................................................................................................................................................................... 59 4. Conclusions ......................................................................................................................................................................................................... 94 2 1. Introduction 1.1 North Tyneside Council submitted its Local Plan (“the Plan”) to the Secretary of State in June 2016 and it was subject to an Examination in Public in November 2016. Following this, North Tyneside Council are proposing a collection of Main Modifications to the Plan, which will be subject to public consultation in early 2017. 1.2 The Council are required to undertake a Habitats Regulations Assessment (HRA) in line with the requirements set by the amended Conservation of Habitats and Species Regulations (2010) to assess the effects of the Plan of European Sites. The -

Former County of Tyne & Wear

Archaeological Investigations Project 2002 Desk-Based Assessments North East Region FORMER COUNTY OF TYNE & WEAR Gateshead 1/171 (B.05.K001) NZ 25356355 HALF MOON LANE, GATESHEAD Half Moon Lane, Gateshead Wearing, N Lancaster : Oxford Archaeology North, 2002, 47pp, colour pls, pls, figs, refs Work undertaken by: Oxford Archaeology North Given that the building on Half Moon Lane have been extensively cellared it is considered that there is no need for an evaluation of this area. However, there is potential for surviving archaeological deposits within the footprint of 18-24 Bottle Bank and the former works building on William IV Yard, and it is recommended that these be subject to trial trenching to investigate the below ground survival of archaeological remains.[Au(abr)] SMR primary record number: 3256 Archaeological periods represented: PM Houghton-le-Spring 1/172 (B.05.K007) NZ 34244988 HALL LANE, HOUGHTON-LE-SPRING Hall Lane, Houghton-Le-Spring: Archaeological Assessment The Archaeological Practice Newcastle upon Tyne : The Archaeological Practice, 2002, 18pp, colour pls, pls, figs, refs Work undertaken by: The Archaeological Practice Previously recorded features can be discounted, since none are of great significance, nor likely to survive beneath the modern overburden. The precense or absence of medieval or earlier remains on the site can not be confirmed withough excavation. [Au(adp)] SMR primary record number: 2002/17 Archaeological periods represented: PM Newcastle-upon-Tyne 1/173 (B.05.K011) NZ 24996374 46-54 CLOSE, QUAYSIDE 46-54 Close, Quayside, Newcastle-upon-Tyne, Archaeological Desk-Top Study EC Harris Leeds : EC Harris, 2002, 77pp, colour pls, pls, figs, tabs, refs Work undertaken by: EC Harris The results of the desk-top Study show that there is a high potential for archaeological remains on the site, despite development and re-development of the site since the mid 19th century. -

A191 Corridor Full Business Case November 2015

A191 Corridor Full Business Case November 2015 A191 Corridor OBC November 2015 Contents Contents 1. Executive Summary 1 1.1 Background 1 1.2 Scheme Description 1 1.3 Strategic Case 2 1.4 Economic Case 2 1.5 Management Case 2 1.6 Commercial Case 4 1.7 Financial Case 4 2. The Strategic Case 6 2.1 Business Strategy 6 2.2 Responsibility of the Scheme Promoter 6 2.3 Description of the Corridor 7 2.4 The Problem Identified & Justification for the Scheme 8 2.5 Background to scheme development 10 2.6 What is the impact of not changing 13 2.7 Objectives 13 2.8 Scope 14 2.9 Key Constraints 15 2.10 Stakeholders 16 2.11 Stakeholder Considerations 16 2.12 Key Stakeholders 16 2.13 Stakeholder Conflicts 17 2.14 The Option 17 3. The Economic Case 19 3.1 Proportionate Approach to Scheme Appraisal 19 3.2 Options Appraised 43 3.3 Assumptions 45 3.4 Sensitivity and Risk Profile 45 3.5 Value for Money Statement 47 3.6 Appraisal Summary Table 48 4. The Management Case 49 4.1 Introduction 49 4.2 Evidence of similar projects 49 4.3 Outline Programme 50 4.4 Governance, organisation structure & role 51 4.5 Assurances & approvals plan 53 4.6 Stakeholder Engagement Strategy 53 4.7 Risk management strategy 53 4.8 Monitoring & Evaluation 59 4.9 Project management options 59 4.10 Quality management 61 4.11 Roles and responsibilities 64 4.12 Specific Roles for Quality Management 64 4.13 Contingency Planning 65 5. -

Planning Committee

Planning Committee 8 September 2017 To be held on Tuesday 19 September 2017 in Room 0.02, Ground Floor, Quadrant East, The Silverlink North, Cobalt Business Park, North Tyneside, NE27 0BY commencing at 10.00am. Agenda Page Item 1. Apologies for absence To receive apologies for absence from the meeting. 2. Appointment of substitutes To be informed of the appointment of any substitute members for the meeting. 3. To receive any declarations of interest You are invited to declare any registerable and/or non-registerable interests in matters appearing on the agenda, and the nature of that interest. You are also requested to complete the Declarations of Interests card available at the meeting and return it to the Democratic Services Officer before leaving the meeting. You are also invited to disclose any dispensation from the requirement to declare any registerable and/or non-registerable interests that have been granted to you in respect of any matters appearing on the agenda. 4. Minutes 3 To confirm the minutes of the meeting held on 29 August 2017. Continued overleaf Members of the public are welcome to attend this meeting and receive information about it. North Tyneside Council wants to make it easier for you to get hold of the information you need. We are able to provide our documents in alternative formats including Braille, audiotape, large print and alternative languages. For further information please call 0191 643 5359. Contact Officer – Michael Robson – (0191) 643 5359 1 5. Planning officer reports 7 To give consideration to the planning applications contained in the above report relating to: 5.1 16/01885/FUL Land to the West of Station Road North and Land South of East 12 Benton Farm Cottages, Station Road North Wallsend. -

S106 Monitoring Spreadsheet Updated

Date Agreement Amount Date Spending Money App Reference S106 Reference Site Location Proposal Signed (or Amount Due Purpose Trigger Event Amount Spent Remaining to payment Amount Directorate Received permission be spent received granted) 76/77 Rudyerd Conversion of two retail units 20/00116/FUL 20/01146/S106 Street 20/08/2020 £674 £0.00 £0.00 into two ground floor flats North Shields Towards provision of a mitigation service including Warden provision and associated projects 76/77 Rudyerd to mitigate the On Environment Conversion of two retail units 20/00116/FUL 20/01146/S106 Street 20/08/2020 £674 impact and commencement of £0.00 £0.00 and Leisure into two ground floor flats North Shields recreational activity the development along this Northumbria coast SPA and Durham SAC as defined by Natural England at the time. Hybrid application: Full application for Aldi store, associated car parking and Land At Former landscaping; outline Tynemouth application (with means of Victoria Jubilee access) for residential use 19/01388/FUL 20/00997/S106 17/06/2020 £99,511 £0.00 £0.00 Infirmary (REVISED LANDSCAPE PLAN, Hawkeys Lane TREE REPORTS AND North Shields ADDITIONAL MITIGATION STATEMENT) (Legal Agreement section 106 linked to 19/01388/FUL) Hybrid application: Full application for Aldi store, associated car parking and Land At Former landscaping; outline Scheme prior to Tynemouth application (with means of commencement of Victoria Jubilee access) for residential use 25% affordable Housing 19/01388/FUL 20/00997/S106 17/06/2020 development of Infirmary -

Section 106 - January 2017 Monies Received and Not Yet Spent Sub (All)

Section 106 - January 2017 Monies Received and not yet spent Sub (All) Sum of Amount Cultural Employ- Environ- Third Affordable Facilities/W ment mental Health Highway Open Parks & Sports Party Travel Development Housing Allotments orks Education Initiatives Works care Works Spaces Playsites Recreation Facilities Works Provisions Grand Total Comments 00/02134/S106 - Collingwood Ward (S0056) - Plot 6, Cobalt Business Park, Silver Sum being used for on going maintenance of Silverlink Biodiversity Fox Way, Wallsend - Highbridge - 00/01360/FUL -27,000 -27,000 park 02/03264/S106 - Chirton Ward (S0008) - Land Parcels West of First Avenue and North of Second Avenue Off Narvik Way Tyne Tunnel Trading Estate Held pending revised proposals for TTTE following completion of North Shields - UK Land Estates (Partnership) Ltd - 02/00566/FUL -7,500 -7,500 2nd Tyne Tunnel & associated highway works The spend will be utilised to supplement the proposed highway improvement works on the A188 / A189 corridor (Westmoor 03/02991/S106 -Longbenton Ward (S0011) - Land at Gosforth Park Way Roundabout to Weetslade Roundabout). Options currently being Gosforth Business Park - Beazer Homes Ltd - 03/01832/FUL -256,600 -256,600 considered 04/00054/S106 - Whitley Bay Ward (S0016) - Group of Buildings at Whitley Road Development has not taken place and sum to be returned to and York Road Whitley Bay - Redacre Developments Ltd - 03/01232/FUL -15,283 -15,283 developer 06/00247/S106 - Collingwood Ward (S0026) - Land and Buildings South of Awaiting start of development on