Dallas- Fort Worth by Tracy Hadden Loh, Phd Christopher B

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2019 Uptown Demographic Study

Uptown Dallas Prepared for Uptown Dallas, Inc. Market Study December 2019 Metrostudy-Dallas/Ft. Worth 1255 West 15th Street, Suite 240 Plano, TX 75075 Phone: 214.869.4916 Email: [email protected] Web: www.metrostudy.com Table of Contents Profile 3 – 8 Economic/Demographic 7 – 11 Employment 12 – 14 Real Estate 15 – 21 Transportation 22 – 24 Uptown Data 25 – 28 Uptown Residents 29 – 37 UPTOWN DALLAS, INC. CUSTOM STUDY Page 2 Profile Uptown Dallas 1993 Development in Uptown began in the 1980s with residential and commercial growth. As the neighborhood began to take shape, developers and residents alike saw an opportunity to enhance the area. Through consensus with the City of Dallas, Uptown Dallas, Inc. was formed in 1993 to scale, maintain and further improve the neighborhood. Uptown Dallas, Inc. celebrated 25 years in 2018. 591.8 Acres Stretching just under one square mile, or 591.8 acres, Uptown is a diverse and dense neighborhood. The community includes numerous residential options, reputable companies, schools and a variety of retail and dining options. 58.1 Acres Uptown has 19 square feet of greenspace per person totaling 58.1 acres. Open space includes Griggs Park which is 8 acres and Greenwood Cemetery, Calvary, Temple Emanuel, Anita Phelps Park and Freedman’s Memorial comprise 44 acres. Katy Trail, a 3.5-mile, privately funded trail system built on an old railroad line defines Uptown’s western border. Additionally, there are 53.5 acres of greenspace bordering Uptown including the award-winning Klyde Warren Park. 4.6 Miles Founded in 1983 with the intent of returning heritage streetcars to the streets of Uptown, the McKinney Avenue Transit Authority successfully accomplished that goal in July of 1989. -

Downtown Walking Map

DOWNTOWN WALKING MAP To To121/ DFW Stockyards District To Airport 26 I-35W Bluff 17 Harding MC ★ Trinity Trails 31 Elm North Main ➤ E. Belknap ➤ Trinity Trails ★ Pecan E. Weatherford Crump Calhoun Grov Jones e 1 1st ➤ 25 Terry 2nd Main St. MC 24 ➤ 3rd To To To 11 I-35W I-30 287 ➤ ➤ 21 Commerce ➤ 4th Taylor 22 B 280 ➤ ➤ W. Belknap 23 18 9 ➤ 4 5th W. Weatherford 13 ➤ 3 Houston 8 6th 1st Burnett 7 Florence ➤ Henderson Lamar ➤ 2 7th 2nd B 20 ➤ 8th 15 3rd 16 ➤ 4th B ➤ Commerce ➤ B 9th Jones B ➤ Calhoun 5th B 5th 14 B B ➤ MC Throckmorton➤ To Cultural District & West 7th 7th 10 B 19 12 10th B 6 Throckmorton 28 14th Henderson Florence St. ➤ Cherr Jennings Macon Texas Burnett Lamar Taylor Monroe 32 15th Commerce y Houston St. ➤ 5 29 13th JANUARY 2016 ★ To I-30 From I-30, sitors Bureau To Cultural District Lancaster Vi B Lancaster exit Lancaster 30 27 (westbound) to Commerce ention & to Downtown nv Co From I-30, h exit Cherry / Lancaster rt Wo (eastbound) or rt Summit (westbound) I-30 To Fo to Downtown To Near Southside I-35W © Copyright 1 Major Ripley Allen Arnold Statue 9 Etta’s Place 17 LaGrave Field 25 Tarrant County Courthouse 398 N. Taylor St. TrinityRiverVision.org 200 W. 3rd St. 817.255.5760 301 N.E. 6th St. 817.332.2287 100 W. Weatherford St. 817.884.1111 2 The Ashton Hotel 10 Federal Building 18 Maddox-Muse Center 26 TownePlace Suites by Marriott Fort Worth Downtown 610 Main St. -

Vol. 5 No. 2 Feb. 1996

Complimentary to churches -/// j c' -/u<< lt /< (D/t/i< /-///////// and community groups pmaritij %j>ortumtu Jlew* African American Pastors Coalition's MLK Day celebration Are you Miss Thomas Ethnic Notes: Muhammad asks Bachelorette '96? The Black "Why are we see page 29 Cowboy, pt.l waiting to exhale?" From The Publisher /, \^' Thurman Jones L.J'X il—^ P*">to by Dtrrick Waiters Coalitiosi tells the 100 - ca1994 Marks story, ES3 1995 Pirogr©ss not TAG As I am sure many of our readers have heard, Dallas is often viewed as not being The continuing controversy Carter Lincoln Pinkston S. Oak Cliff All Schools the most progressive city on the face on the over the Talented and Gifted Kimbal! Madison Roosevelt Tag Magnet planet. In fact, there are those who believe Magnet at Townview seems to be an that we are at least 10-15 years behind issue that refuses to yield to a far other major American cities as it related to more critical one in DISD. As READING the overall lot for African Americans. Minority Opportunity News reviewed in last month's edition, Within the last two weeks, I have again the focus on the TAG matter has received irrefutable proof that Dallas is diminished the level of attention not as far behind the rest of the known that should be given to the more universe as we might have suspected. important concern of the low pass E^ 1994 Last fall, many of us witnessed one of rate on the Texas Assessment of E3 1995 the major events of our modem times, the Academic Skills test (TAAS) for Million Man March. -

Ten Year Strategic Action Plan

PLANDOWNTOWN 2023 FORT WORTH TEN YEAR STRATEGIC ACTION PLAN 1 12 SH Uptown TRINITY Area ch ea W P UPTOWN S a 5 m u 3 e l - Trinity s H S I H Bluffs 19 9 M Northeast a in Edge Area Tarrant County t 1s Ex Courthouse Expansion d Area 3 2n rd EASTSIDE 3 h ap 4t lkn Be Downtown S f h P r C 5t H he at o U e e Core m n W d M m R e a e h r i r t s n c 6 o H e n o 2 u Southeast T s 8 h t th r o 7 o n 0 c k Edge Area m o h r t t 8 o n ITC h 9t CULTURAL 5th Expansion 7th 7th DISTRICT Burnett Area 2 Henderson- Plaza 10th vention Center Summit J City o n e Hall s Texas H C o e C m n h S d m e u e r e m r r r y s c m e o i n t Expansion Area 1 Lancaster J Lancaster e Lancaster n n i n g s d lv B k r a Holly P t s e Treatment IH-30 r o F Plant Parkview SOUTHEAST Area NEAR FORT SOUTHSIDE WORTH Table of Contents Message from Plan 2023 Chair 1 Executive Summary 2 The Plan 4 Vision 10 Business Development 16 Education 24 Housing 32 Retail, Arts and Entertainment 38 Transportation 42 Urban Design, Open Space and Public Art 50 Committee List, Acknowledgements 62 Message from Plan 2023 Chair Since the summer of 2003, Downtown Fort Worth has made advance - ments on many fronts. -

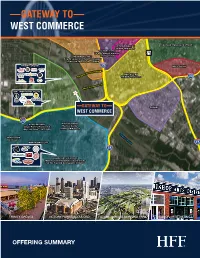

West Commerce Gateway To

GATEWAY TO WEST COMMERCE UPTOWN DALLAS BAYLOR MEDICAL DISTRICT 22,000 employees VICTORY PARK 75-acre master-planned DESIGN DISTRICT development Fourth largest portfolio of designer showroom space in the country TRINITY GROVES DEEP ELLUM Bridge nt Hill Hu ret DALLAS CBD rga Ma 113,000 employees West Commerce St FORT WORTH AVE RETAIL GATEWAY TO CEDARS WEST COMMERCE KESSLER PARK Methodist Dallas Single Family Residential Medical Center Avg. List Price - $675,000 2,900+ Employees TRINITY RIVER Stevens Park Golf Course NORTH OAK CLIFF BISHOP ARTS DISTRICT 100+ Restaurants & Retail Destinations 7 of the Top 100 Restaurants in Dallas TRINITY GROVES VICTORY PARK/DALLAS CBD FUTURE HAROLD SIMMONS PARK BISHOP ARTS DISTRICT OFFERING SUMMARY In ment Overview HFF has been exclusively retained to offer an opportunity for qualified investors to purchase the fee simple interest in a site known as Gateway to West Commerce (the “Site”). The 4.75-acre site is located in Trinity Groves at the SW corner of W Commerce Street and N Beckley Avenue. The Site is located in the Planned Development District 714, allowing for a variety of uses including office, retail, and apartments. Gateway to West Commerce boasts excellent access to Dallas’ Airports and primary traffic arteries as well as close proximity to a wide array of lifestyle amenities including the acclaimed Trinity Groves, Victory Park, Bishop Arts District, and more. Additionally, Gateway to West Commerce is located just minutes from Downtown Dallas (approximately 1 mile from the Site). This highly visible location represents a unique opportunity to acquire/develop in an infill location with access to the best economic drivers the city has to offer. -

Co M M U Te R

RAIL COMMUTER Effective August 12, 2019 Monday – Saturday EBJ Union Station Victory Station Medical/Market Center Station Downtown Irving/ Heritage Crossing Station West Irving Station CentrePort DFW Airport Station (Fare Boundary) Bell Station Richland Hills Station Fort Worth Central Station Fort Worth T & P Station TRE Schedule booklet_AUG 2019 Designer: JH 525-008-0619 SIZE: 3.25X9 CMYK w/Bleeds TrinityRailwayExpress.org RideTrinityMetro.org DART.org 817-215-8600 214-979 -1111 DART TICKETS & PASS PRICES PRECIOS DE PASES Y BOLETOS DE DART FARES TARIFAS Fare Category FARE Categoría de tarifa TARIFA Single Ride - Local (Bus Only) $2.50 Viaje Sencillo - Local (Sólo Autobús) $2.50 Single Ride - Reduced* (Bus Only) $1.25 Viaje Sencillo - Reducido* (Sólo Autobús) $1.25 AM/PM Pass - Local $3.00 Pase AM/PM - Local $3.00 AM/PM Pass - Reduced* $1.50 Pase AM/PM - Reducido* $1.50 Midday - Local (9:30 a.m. - 2:30 p.m.) $2.00 Mediodía - Local (9:30 a.m. - 2:30 p.m.) $2.00 Day Pass - Local $6.00 Pase Diario - Local $6.00 Day Pass - Reduced* $3.00 Pase Diario - Reducido* $3.00 Day Pass - Regional $12.00 Pase Diario - Regional $12.00 Monthly Pass - Local † $96.00 Pase Mensual - Local † $96.00 Monthly Pass - Reduced* † $48.00 Pase Mensual - Reducido* † $48.00 Monthly Pass - Regional $192.00 Pase Mensual - Regional $192.00 Local: DART rail and buses; Trinity Railway Express Local: ferroviario y autobuses de DART; servicio de (TRE) service between EBJ Union Station & CentrePort Trinity Railway Express (TRE) entre EBJ Union Station y Station; GoLink & Flex service. -

Walkability Premium

Center Piece Southlake’s town center may be all new construction, but it follows an old model by placing CHAPTER THREE its town hall at its heart. The George Washington University Center for Real Estate and Urban Analysis, working with the Urban Land Institute, the North Central Texas THE Council of Governments, and D Magazine, are in the process of completing the WalkUP Wake-Up Call for the DFW metro area. This never-before-completed analysis will be a nearly 100 percent census of all real estate product in the region, including owner-user and publicly owned space. It will define where Walkability Premium the potential, emerging, and established walkable urban places are and how they compare to the drivable sub-urban locations in Dallas-Fort Worth with regard to place-based economic and social equity performance. This article is Other cities have discovered huge value based on preliminary results of the WalkUP analysis. The complete analysis will be published in October 2018. Our appreciation to Shea Byers of PM in walkable urban places while Dallas-Fort Worth lags. Realty Group for leading this effort locally, Scott Polikov of Gateway Plan- But that is changing—fast. ning, Brandon Palanker of 3BL Strategies, and DFW donors to the George Washington University for their support. PHOTOGRAPHY LEWIS MARK BY CHRISTOPHER B. LEINBERGER AND TRACY LOH 60 D MAGAZINE SPECIAL EDITION DALLAS AND THE NEW URBANISM 61 Forms of the Built Environment first, it is important to understand that the built environment takes two basic forms: walkable urban and drivable sub-urban. There are many variations, but broadly speaking there are just these two. -

Victory Park

SOUTH VICTORY DISTRICT Victory Park DALLAS, TEXAS Victory Park, a walkable, urban development in the Uptown neighborhood of Dallas, is home to some of the cities best restaurants, entertainment, and retail. • Victory Park is a 75 acre masterplanned, mixed-use development in Downtown Dallas anchored by the American Airlines Center (home of the Dallas Mavericks & Stars), The House of Blues, HERO, Tom Thumb, W Dallas Hotel and the new 44,000 SF Cinepolis Luxury Cinemas. • The bar and restaurant scene at Victory Park is about to experience a dramatic change as we welcome new concepts, opening later this year, from some of Dallas' top food and beverage operators. • WeWork opened in early 2019 on the 2nd & 3rd floors of the Victory Plaza Office building. The space features their signature mid-century modern decor, open floor plan, floor to ceiling glass and steel framing, private office suites and communal working space. 2 Demographics DALLAS LOVE NORTHEAST FIELD AIRPORT PARK DALLAS CITIES 1 MI RADIUS GREENWAY Population (2018) – 29,603 PARKS 75 Households – 13,124 Avg. HH Income – $117,552 3 MILES Median Age – 33 Daytime Demo – 141,525 Education (Bach+) – 57% 3 MI RADIUS 35E Population (2018) – 187,692 Households – 87,023 1 MILE Avg. HH Income – $91,322 Trinity UPTOWN OLD EAST Median Age – 34 River DALLAS Daytime Demo – 393,259 30 Education (Bach+) – 48% Victory Park 5 MI RADIUS Deep DOWNTOWN Ellum Population (2018) – 398,518 DALLAS Households – 163,296 Avg. HH Income – $94,878 CEDARS Median Age – 34 Daytime Demo – 642,221 30 Education (Bach+) -

2017 Dallas National Night out Events

2017 Dallas National Night Out Events City Council District Service NA/HOA/CW Date Time Location Area Oak Cliff Cultural Center -223 W Jefferson Griggs 1 SW Jefferson Blvd Business Association 10/3/17 6-8PM Blvd. Dallas, TX 75208 Griggs 1 SW LO DANIEL 10/3/17 6:30pm 235 N Waverly Griggs 1 SW Kessler Plaza 10/3/17 6:30pm 2600 Sunset Ave Griggs 1 SW Wynnewood North 10/3/17 6:30pm 500 Block of Hoel Griggs 1 SW Oaks West 8th 10/3/17 6:45pm 521 W 8th St Griggs 1 SW El Tivoli 10/3/17 6:45pm 2700 Block of El Tivoli Dr Griggs 1 SW WHNA 10/3/17 7:15pm 500 N Rosemont (Davis/Rosemont) Griggs 1 SW Sunset Hill 10/3/17 7:15pm 1700 W 10th St Griggs 1 SW East Kessler 10/3/17 7:15pm Coombs Creek Trl/Junior Medrano 2 C Jubilee 10/3/17 5:30pm-7:30pm 917 Bank St. Medrano 2 C Cedars 10/3/17 6:00pm–8:00pm 1515 S Harwood (Dallas Heritage Village-50s) Medrano 2 C Camden Belmont/Henderson 10/3/17 5:00pm-8:00pm 5222 Belmont The Elm Thicket/North park Medrano 2 NW Community 10/3/16 6:00pm-8:00pm 6801 Roper St (KB Polk Recreation Center) Medrano 2 NW Love field West 10/3/17 5:30pm-8:00pm 7780 Harry Hines Blvd Medrano 2 NW Camden Design District 10/3/17 5:30pm-7:30pm 1551 Oak Lawn Ave The Rose Community Center, 3535 Munger, Medrano 2 C Rose Community Center 10/3/2017 6:00pm-8:00pm 21A, Dallas, TX 75204 Oak Cliff Presbyterian Church "Outside in the Thomas 3 SC Twin Oaks & Red Bird-Hampton NAs 10/3/17 6-8PM Parking Lot" - 6000 S. -

Living in Dallas, Texas Demographics Dallas Is the Third-Largest City in Texas and the Ninth-Largest in the United States

Living in Dallas, Texas Demographics Dallas is the third-largest city in Texas and the ninth-largest in the United States. Dallas forms the heart of the large metropolitan area in north central Texas, commonly referred to as the “metroplex”. The metroplex, a 12-county area encompassing more than 120 cities, is anchored by the City of Dallas in the east and the City of Fort Worth in the west. The population of Dallas is around 1.3 million according to the US Census Bureau. This ultra- modern and sophisticated city is the largest economic center of the 12-county Dallas-Fort Worth metropolitan area, which is the fourth-largest metropolitan area in the United States. The Dallas community is world-class with a diverse population located on a total land area of 384 square miles. Dallas is centrally located within the US and serves as a commercial and cultural hub of the Southwest region. Within a four-hour flight from most North American destinations, the travel possibilities are endless. Dallas is also a leading business and meeting city. Dallas-Fort Worth is home to 24 Fortune 500 companies and has become a hotspot in recent years for corporate relocations. Notable Fortune 500 companies include: Exxon Mobil, AT&T, Energy Transfer Equity, American Airlines Group, Southwest Airlines, Texas Instruments, GameStop, D.R. Horton, and Dr. Pepper Snapple Group. Entertainment/Culture With many entertainment districts within a short distance of downtown, Dallas is a unique melting pot which mixes local history with arts, culture, dining, and more. Dallas is stylish and cosmopolitan, a city with a well-earned reputation for fashion, shopping, and prosperity. -

Member FDIC Bishop Arts Downtown Dallas Cedars Deep Ellum Garland

Uptown Garland Deep Ellum Bishop Arts Cedars Downtown Dallas 2020 Member FDIC “What a long, strange trip it’s been.” GROWTH - Year-end assets increased DEAR SHAREHOLDERS, 2020 was best described by the 34.37% to $307,327,273. Deposits famous song line by the Grateful Dead – were up 37.8% to $274,208,306, while “What a long, strange trip it’s been.” our loan portfolio increased 23.5% to We went from a booming economy $235,296,015. We anticipate continued early in the year, to a massive drop strong growth in 2021, although we in the stock market and an almost expect that growth to be at slower total lockdown of the country due to levels than the record increases that the worst pandemic in over 100 years we saw in 2020. in the spring, to civil unrest in the CAPITAL - Our capital to assets ratio, summer and finally to the anticipation considered by many the primary of a new administration and a stock indicator of bank strength and market boom in the fall. solvency, was 9.97% at year end, Last year was truly a year like no significantly above “well capitalized” other in recent memory. regulatory requirements. Despite our Despite all of these headwinds, strong capital ratio, our after-tax Texas Brand Bancshares, Inc., return on equity from continuing and Texas Brand Bank are pleased operations was 9.66%. Return on to announce a record year. average assets was 0.99%. Borrower dissatisfaction with large, money center banks, EARNINGS – Earnings were up sharply particularly with respect to the in 2020, rising 41.42% over 2019. -

The Official Publication of the Dallas Police Association Volume XXXVII No

The S hield The Official Publication of the Dallas Police Association Volume XXXVII No. 11 November 2017 Dallas Police Association 1412 Griffin Street E, Dallas, Texas 75215 214.747.6839 fax 214.747.8194 [email protected] Contents Executive Board Mike Mata, President Northeast 214.725.0261 Frederick Frazier, First Vice President 4 President Criminal Intel 214.549.4918 Beth Sundquist, Second Vice President Youth 214.232.5053 8 Thank You Jaime Castro, Third Vice President Alarm Unit 214.228.6895 Steve Myers, Fourth Vice President Narcotics 214.457.3380 13 Trunk or Treat James Parnell, Secretary/Treasurer Fire Arms Training Center 214.537.5200 16 People Central North Central Billy Taylor 214.476.7669 Roy Jenkins 972.741.6781 Branden Helms 817.692.4550 Todd Woolum 972.754.5773 Northwest Northeast 20 Your Health Kevin Janse 214.930.3174 Casey Tharp 214.642.0707 Vince Garst 972.415.7324 Phillip Gordon 469.766.6756 South Central Southeast 21 Johnny Sides Award George Gonzales 214.632.1596 DeMarcus Turner 214.929.1067 J.T. Courson 817.600.0335 Haydee Duran Bowen 214.641.7301 Southwest Nick Lybrand 469.404.0115 23 Business Gracie Hernandez 214.808.2436 Special Investigations Special Operations Mark Rickerman 214.808.2047 Silver Valencia 214.460.1918 Lance White 972.977.3096 Headquarters Omar Figueroa 214.609.0694 Tony Castleberg 214.801.4758 Richard Forness 972.955.9820 Patty Carter 469.955.9052 Reserves Latino Community Liaison Steve Brody 214.728.2422 Jaime Castro 214.228.6895 Sergeant at Arms Major Berry 469.438.1161 James Bristo 254.718.5323 J.D.