Route 83 Redevelopment Project Area

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

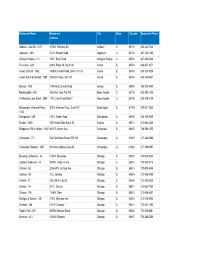

Copy of Chipotle Restuarant List

Restaurant Name Restaurant City State Zipcode Restaurant Phone Address Addison - Lake 53 - 1819 1078 N. Rohlwing Rd Addison IL 60101 630-282-7220 Algonquin - 399 412 N. Randall Road Algonquin IL 60102 847-458-1030 Arlington Heights - 131 338 E. Rand Road Arlington Heights IL 60004 847-392-8328 Fox Valley - 624 848 N. Route 59, Suite 106 Aurora IL 60504 630-851-3271 Aurora Orchard - 1462 1480 N Orchard Road, Suite 114-116 Aurora IL 60506 630-723-5004 Aurora Kirk & Butterfield - 1888 2902 Kirk Road, Unit 100 Aurora IL 60504 630-429-9437 Berwyn - 1753 7140 West Cermak Road Berwyn IL 60402 708-303-5049 Bloomingdale - 858 396 West Army Trail Rd. Bloomingdale IL 60108 630-893-2108 Fairfield and Lake Street - 2884 170 E Lake Street Suite C Bloomingdale IL 60108 630-529-5128 Bloomington Veterans Prkwy - 305 N. Veterans Pkwy., Suite 101 Bloomington IL 61704 309-661-7850 1035 Bolingbrook - 529 274 S. Weber Road Bolingbrook IL 60490 630-759-9359 Bradley - 2609 1601 Illinois State Route 50 Bradley IL 60914 815-932-3225 Bridgeview 87th & Harlem - 3047 8813 S. Harlem Ave Bridgeview IL 60455 708-598-1555 Champaign - 771 528 East Green Street, STE 101 Champaign IL 61820 217-344-0466 Champaign Prospect - 1837 903 West Anthony Drive #A Champaign IL 61820 217-398-0997 Broadway & Belmont - 36 3181 N. Broadway Chicago IL 60657 773-525-5250 Clybourn Commons - 42 2000 N. Clybourn Ave. Chicago IL 60614 773-935-5710 Orchard - 52 2256-58 N. Orchard Ave. Chicago IL 60614 773-935-6744 Jackson - 88 10 E. -

THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden Avenue Downers Grove, Illinois 60515 Governor Br

THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden Avenue Downers Grove, Illinois 60515 Governor Bruce Rauner Director David Gonzalez Acting Secretary Randall Director Mark Peterson Blankenhorn Director Jim Banks Director Jeff Redick Director Terry D’Arcy Director James Sweeney Director Earl S. Dotson Director Tom Weisner Pursuant to the requirements of the Authority’s By-Laws, Notice is hereby given of the Bo ard Meeting of the Authority to be held on Thursday, May 28, 2015 at 9:00 a.m. in the Boardroom of the Administration Building in Downers Grove, Illinois. Paula Wolff, Chair This meeting will be accessible to individuals with disabilities in compliance with Executive Order #5, and pertinent state and federal laws, upon notification of anticipated attendance. Persons with disabilities planning to attend and needing accommodations should contact the Americans with Disabilities Act Coordinator of The Illinois State Toll Highway Authority at (630) 241-6800, Ext. 1010 in advance of the meeting at 2700 Ogden Avenue, Downers Grove, IL, to inform of their anticipated attendance. There will be live feed Webcasting of the Board Meeting while in session. An audio file will be available five business days after the meeting at www.illinoistollway.com THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden, Downers Grove, IL 60515 BOARD MEETING AGENDA May 28, 2015 9:00 a.m. 1.0 CALL TO ORDER 2.0 ROLL CALL 3.0 PUBLIC COMMENT 4.0 CHAIR 1. Approval of the minutes of the Regular Board Meeting and Executive Session held April 23, 2015. 2. Review and approve Executive Session minutes for public release. -

Village of Mundelein

M U N DEL E I N FOR B U S I NESS. FOR L I FE. 35 MILES NORTHWEST OF CHICAGO EASY ACCESS TO DOWNTOWN CHICAGO AND THREE AIRPORTS W E LCOME T O M UNDE L EIN, I LLI NOI S — VILLAGE OF BUSINE SS MINDE D … F O R W ARD THI NKI N G MUNDELEIN INCORPORATED 1909 The Village of Mundelein, a vibrant and progressive community of nearly 32,000 residents, AN AWARD WINNING has a rather simple approach to economic development—we are on YOUR team and we COMMUNITY are committed to doing everything we can to help your business succeed. Mundelein is situated in the center of beautiful Lake County, Illinois—one of the strongest areas GOVERNOR’S HOMETOWN of commercial and industrial growth in the nation, with excellent housing, recreational, AWARD WINNER educational, and business opportunities. TOP 100 SAFEST CITIES IN AMERICA—RANKED 38 Mundelein is a full-service community with municipal services second to none. The Village provides fire and police protection, water delivery, wastewater treatment, building RECIPIENT NEW URBANISM inspection, engineering design and inspection, street maintenance, and economic CNU MERIT AWARD FOR MASTER REDEVELOPMENT development assistance. Each department’s highest priority is providing exceptional IMPLEMENTATION PLAN customer service. Plus, Mundelein’s award-winning schools, Park and Recreation programs and library services offer residents numerous leisure, recreational, and enrichment options. CALEA ACCREDITED— THE GOLD STANDARD IN PUBLIC If you are seeking assistance relocating or expanding your business, we can answer SAFETY ACCREDITATION your questions and offer advice in the areas of economic development, site selection, MUNDELEIN PARK AND engineering, finance, demographics, construction, and marketing, to name just a few. -

THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden Avenue Downers Grove, Illinois 60515 Governor Br

THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden Avenue Downers Grove, Illinois 60515 Governor Bruce Rauner Director Joseph N. Gomez Secretary Randall Blankenhorn Director David Gonzalez Director James Banks Director Craig B. Johnson Director Corey B.Brooks Director Nick Sauer Director Earl S. Dotson, Jr. Director James Sweeney Pursuant to the requirements of the Authority’s By-Laws, Notice is hereby given of the Regular Board Meeting of the Authority to be held on Wednesday, March 23, 2016 at 9:00 a.m. in the Boardroom of the Administration Building in Downers Grove, Illinois. Robert J. Schillerstrom, Chairman This meeting will be accessible to individuals with disabilities in compliance with Executive Order #5, and pertinent state and federal laws, upon notification of anticipated attendance. Persons with disabilities planning to attend and needing accommodations should contact the Americans with Disabilities Act Coordinator of The Illinois State Toll Highway Authority at (630) 241-6800, Ext. 1010 in advance of the meeting at 2700 Ogden Avenue, Downers Grove, IL, to inform of their anticipated attendance. There will be live feed Webcasting of the Board Meeting while in session. A video file will be available five business days after the meeting at www.illinoistollway.com. THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden, Downers Grove, IL 60515 BOARD OF DIRECTORS MEETING AGENDA March 23, 2016 9:00 a.m. 1.0 CALL TO ORDER / PLEDGE OF ALLEGIANCE 2.0 ROLL CALL 3.0 PUBLIC COMMENT 4.0 CHAIRMAN 1. Approval of the Minutes of the Regular Board of Directors Meeting held February 25, 2016. -

Flood Insurance Study Users

The Federal Emergency Management Agency in Cooperation with DuPage County, Illinois Presents: FLOOD INSURANCE STUDY A Report of Flood Hazards in: DUPAGE COUNTY, ILLINOIS AND INCORPORATED AREAS Prepared, in parts, by: FEMA Region V Nika Engineering 536 South Clark Street 421 Mill Street Chicago, Illinois 60605 and Batavia, Illiois 60510 March 2007 1 7043CV000A NOTICE TO FLOOD INSURANCE STUDY USERS Communities participating in the National Flood Insurance Program have established repositories of flood hazard data for floodplain management and flood insurance purposes. This Flood Insurance Study (FIS) may not contain all data available within the repository. It is advisable to contact the community repository for any additional data. Part or all of this FIS may be revised and republished at any time. In addition, part of this FIS may be revised by the Letter of Map Revision process, which does not involve republication or redistribution of the FIS. It is, therefore, the responsibility of the user to consult with community officials and to check the community repository to obtain the most current FIS components. Initial Countywide FIS Effective Date: December 4, 1985 Revised Countywide FIS Date: June 16, 2004 FLOOD INSURANCE STUDY DuPAGE COUNTY, ILLINOIS TABLE OF CONTENTS Page # 1. INTRODUCTION 1 1.1. Purpose of Study 1 1.2. Authority and Acknowledgments 1 1.3. Coordination 5 1.4. Regional Participation and Progress 7 2. AREA STUDIED 8 2.1. Scope of Study 8 2.2. Community Description 8 2.3. Watershed Description 8 2.3.1. DesPlaines River (DP) 9 2.3.1.1. Geographical Description 9 2.3.1.2. -

2009 Annual Report

OUR MISSION We provide safe, cost-effective transportation for Illinois in ways that State of Illinois enhance quality of life, promote economic prosperity, and demonstrate Illinois Department of Transportation respect for our environment. OUR GUIDING PRINCIPLES 2009 We will accomplish our mission while making the following principles ANNUAL REPORT the hallmark of all our work: Safety • Integrity • Diversity • Responsiveness • Quality • Innovation CONTENTS OUR VISION The Illinois Department of Transportation will be recognized as the Governor’s Letter . 1 premier state department of transportation in the nation. Secretary’s Letter . 2 QUALITY POLICY Introduction . 3 IDOT will consistently provide safe, cost-effective transportation for Illinois that meets or exceeds the requirements and expectations of Executive Summary . 4 our customers. We will actively pursue ever improving quality through programs that enable each employee to continually strive to do their Aeronautics . 8 job right the first time, every time. Traffic Safety . 11 QUALITY STATEMENT Planning & Programming . 18 Do it right the first time, every time. Finance & Administration . 19 Chief Counsel . 23 Highways . 25 Business & Workforce Diversity . 42 Public & Intermodal Trans . 48 Quality Compliance & Review . 51 Communications . 53 Secretary . 54 Acknowledgements The Honorable Pat Quinn , Governor ARRA Summary . 55 Gary Hannig , Secretary of Transportation 2009 Motorist Survey . 56 Bill Grunloh , Chief of Staff Marva Boyd , Deputy Chief of Staff Conclusion . 58 David Phelps -

Active Contracts by Type

Active Professional Services Contracts as of 8/14/2018 Compl. Board Contract Suppl. Contract Final Date Date Number Consultant Phase Contract Amount Description Approved State Pymt Contract PM 07/26/18 RR-18-4379 AMEC Foster Wheeler Environment & Infrastructure, Inc. Design $3,000,000 Reagan Memorial Tollway, Roadway and Bridge Rehabilitation, M.P. 117.8 Award No 06/30/24 M. Faraj (Aurora Toll Plaza) to M.P. 123.4 (IL 59). Phase II Engineering Services. 07/26/18 RR-18-4381 Lochmueller Group, Inc. Design $1,511,894 Reagan Memorial Tollway, Pavement and Structural Preservation and Approved No 07/31/24 M. Faraj Rehabilitation, M.P. 113.3 (Illinois Route 56) to M.P. 117.8 (Aurora Toll Plaza). Phase II Engineering Services. 06/28/18 RR-18-4377 The Roderick Group, Inc. (dba Ardmore Roderick) Inspection $6,500,000 Systemwide, Maintenance Facilities, Construction Management Services Upon Obligated No 12/31/21 W. Doyle Request. On-call and as-needed Construction Management Services. 06/28/18 RR-18-4378 Interra Inc. Inspection $2,500,000 Systemwide, Construction Management Upon Request. On-call and as-needed Award No 12/31/22 J. Kim Construction Management Services. 06/28/18 RR-18-4383 Christopher B. Burke, Engineering, Ltd. Study $5,000,000 Tri-State Tollway, 95th Street to Balmoral Avenue, Planning Studies Upon Obligated No 06/30/25 N. Nutter Request. On-call and as-needed Phase I Engineering Services for Planning Studies and Master Plan Services. 06/28/18 RR-18-9008 Singh & Associates, Inc. Design $2,000,000 Systemwide, Design Upon Request, Non-Roadway. -

1830S Roads (PDF)

A Historical Note The basis of many our roads today in Lake County had their begin- Supervisor. The term of office was for one year. The use of county road nings back in the 1830s. The first wave of settlers primarily from New York districts was abandoned in 1850 when the Township form of government was and the New England States began following the ratification of the Treaty adopted. of Chicago between the United States and the United Nations of Chippewa, Portions of these old roads approved in the 1830s still exist today. Ottawa and Potawatomi Indians on February 23, 1835. At this early date, only A few of the better known roads are Illinois Route 21 (Milwaukee Avenue) one public road existed in Lake County. This was the Green Bay Military Road from Cook County to the Village of Gurnee is the old Chicago and Milwaukee established in 1832. Road. Portions of Illinois Route 59 follow the old Dundee and Bristol (An- The establishment of new roads very quickly became a priority issue tioch) Road. Segments of Illinois Routes 45 and 60 follow an old Indian Trail with the settlers. Laws were in place even at this early date which laid out and the Half Day and Nippersink Point Road. Illinois Route 43 follows parts of procedures for establishing a road. The first step was to petition the County the former Corduroy Road. Illinois Route 83 in the north half of the County fol- Commissioners Court, today called the County Board. The road petition had lows the old Fox River Road. -

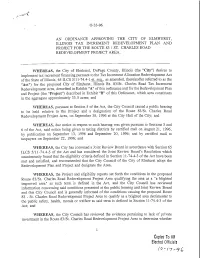

Copies to AI! Elected Officials of This Ordinance

O-33-96 AN ORDINANCE APPROVING THE CITY OF ELMHURST, ILLINOIS TAX INCREMENT REDEVELOPMENT PLAN AND PROJECT FOR THE ROUTE 83 / ST. CHARLES ROAD REDEVELOPMENT PROJECT AREA. WHEREAS, the City of Elmhurst, DuPage County, Illinois (the "City") desires to implement tax increment financing pursuant to the Tax Increment Allocation Redevelopment Act of the State of Illinois, 65 ILCS 5/11-74.4-1 et seq., as amended, (hereinafter referred to as the "Act") for the proposed City of Elmhurst, Illinois Rt. 83/St. Charles Road Tax Increment Redevelopment Area, described hi Exhibit "A" of this ordinance and for the Redevelopment Plan and Project (the "Project") described in Exhibit "B" of this Ordinance, which area constitutes hi the aggregate approximately 33.5 acres; and WHEREAS, pursuant to Section 5 of the Act, the City Council caused a public hearing to be held relative to the Project and a designation of the Route 83/St. Charles Road Redevelopment Project Area, on September 30, 1996 at the City Hall of the City; and WHEREAS, due notice in respect to such hearing was given pursuant to Sections 5 and 6 of the Act, said notice being given to taxing districts by certified mail on August 21, 1996, by publication on September 13, 1996 and September 20, 1996; and by certified mail to taxpayers on September 22, 1996; and WHEREAS, the City has convened a Joint Review Board in accordance with Section 65 ILCS 5/11-74.4-5 of the Act and has considered the Joint Review Board's Resolution which unanimously found that the eligibility criteria defined in Section 11-74-4-3 of the Act have been met and satisfied, and recommended that the City Council of the City of Elmhurst adopt the Redevelopment Plan and Project and designate the Area. -

Kmart Participating Stores

Kmart Participating Stores ADDRESS CITY ST ZIP PHONE 7200 US HIGHWAY 431 ALBERTVILLE AL 35950 (256) 878-9030 3101 MC CLELLAN BLVD ANNISTON AL 36201 (256) 236-5681 104 HIGHWAY 31 NORTH ATHENS AL 35611 (256) 233-1551 2047 E UNIVERSITY DRIVE AUBURN AL 36830 (334) 821-4150 5980 CHALKVILLE MOUNTAIN BIRMINGHAM AL 35235 (205) 655-5150 7845 CRESTWOOD BLVD BIRMINGHAM AL 35210 (205) 956-5186 1525 CHESTNUT BYPASS CENTRE AL 35960 (256) 927-8000 1731 2ND AVE SW CULLMAN AL 35055 (256) 734-4713 1101 BELTLINE RD DECATUR AL 35601 (256) 350-9150 2185 REEVES STREET DOTHAN AL 36303 (334) 794-8756 2214 ROSS CLARK CIRCLE DOTHAN AL 36301 (334) 793-6633 201 GEORGE WALLACE DR GADSDEN AL 35903 (256) 547-5703 901 DECATUR HIGHWAY GARDENDALE AL 35071 (205) 631-5690 230 GREEN SPRINGS HWY HOMEWOOD AL 35209 (205) 916-0610 300 HIGHWAY 78 E JASPER AL 35501 (205) 384-3475 803 MARTIN STREET S PELL CITY AL 35128 (205) 884-2900 2003 US HWY 280 BYPASS PHENIX CITY AL 36867 (334) 291-9773 1880 EAST MAIN STREET PRATTVILLE AL 36066 (334) 365-9460 STATE HIGHWAY 89 #1 KMART PLAZA CABOT AR 72023 (501) 843-2206 2010 SOUTH CARAWAY ROAD JONESBORO AR 72401 (870) 972-9020 10901 RODNEY PARHAM LITTLE ROCK AR 72212 (501) 227-6460 2821 EAST MAIN STREET RUSSELLVILLE AR 72801 (501) 968-4133 3142 WEST SUNSET AVE SPRINGDALE AR 72762 (501) 756-0382 2250 HIGHWAY 95 STE 256 BULLHEAD CITY AZ 86442 (928) 763-7878 1214 E FLORENCE BLVD CASA GRANDE AZ 85222 (602) 836-3466 3340 E ANDY DEVINE AVE KINGMAN AZ 86401 (928) 757-3202 1870 MCCULLOCH BLVD LAKE HAVASU CITY AZ 86403 (928) 453-5919 300 WEST MARIPOSA -

ELGIN O'hare WESTERN ACCESS Frequently Asked Questions

ELGIN O’HARE WESTERN ACCESS Frequently Asked Questions Q. WHAT IS THE ELGIN O’HARE WESTERN ACCESS (EOWA) PROJECT? The EOWA Project consists of construction of a new, all-electronic Tollway around the western border of O'Hare International Airport linking the Jane Addams Memorial Tollway (I-90) and the Tri-State Tollway (I-294), as well as extending the Elgin O'Hare Expressway east along Thorndale Avenue to O'Hare and rehabilitating and widening the existing Elgin O'Hare Expressway from Illinois Route 19 to Meacham/Medinah Road. The 2013-2025 construction plan is broadly supported by local governments and represents a fiscally responsible approach for addressing the area's diverse travel needs - improving travel efficiency, providing new western access to O'Hare, enhancing multi-modal connections and reducing congestion. The project includes: Adding two lanes to the existing Elgin O'Hare Expressway between Illinois Route 19 and Meacham/Medinah Road and converting to a toll road with minor interchange improvements at Illinois Route 19 and Roselle Road and an improved interchange at Meacham/Medinah Road. Extending the Elgin O’Hare Expressway east as a toll road. Constructing or improving interchanges at Illinois Route 53 (Rohlwing Road), I‐290, Park Boulevard/Arlington Heights Road/Prospect Avenue, Wood Dale Road and Illinois Route 83. Provide direct access to O’Hare Airport property from York Road via a new ramp crossing over York Road and the Union Pacific Railroad and Canadian Pacific Railway. Enhance southern access to O’Hare via a new, four-lane Taft Avenue Connector between Illinois Route 19 and Franklin Avenue with a new crossing over the Bensenville Rail Yard. -

STORE # ADDRESS CITY ST ZIP Kmart Collector

Kmart Collector Day - Participating Stores STORE # ADDRESS CITY ST ZIP 9620 7200 US HIGHWAY 431 ALBERTVILLE AL 35950 9648 104 HIGHWAY 31 NORTH ATHENS AL 35611 3931 5980 CHALKVILLE MOUNTAIN BIRMINGHAM AL 35235 9571 1731 2ND AVE SW CULLMAN AL 35055 7066 1101 BELTLINE RD DECATUR AL 35601 7360 2214 ROSS CLARK CIRCLE DOTHAN AL 36301 3082 2185 REEVES STREET DOTHAN AL 36303 3848 105 COX CREEK PKWY SOUTH FLORENCE AL 35630 3359 901 DECATUR HIGHWAY GARDENDALE AL 35071 4817 230 GREEN SPRINGS HWY HOMEWOOD AL 35209 9622 300 HIGHWAY 78 E JASPER AL 35501 7640 312 Z SCHILLINGER RD MOBILE AL 36608 7045 3401 WOODWARD AVE MUSCLE SHOALS AL 35661 4769 803 MARTIN STREET S PELL CITY AL 35128 4760 2003 US HWY 280 BYPASS PHENIX CITY AL 36867 3929 1880 EAST MAIN STREET PRATTVILLE AL 36066 3194 635 SKYLAND BLVD TUSCALOOSA AL 35405 3933 STATE HIGHWAY 89 #1 KMART PLAZA CABOT AR 72023 7356 2010 SOUTH CARAWAY ROAD JONESBORO AR 72401 3120 10901 RODNEY PARHAM LITTLE ROCK AR 72212 9711 2821 EAST MAIN STREET RUSSELLVILLE AR 72801 9623 3142 WEST SUNSET AVE SPRINGDALE AR 72762 3375 2250 HIGHWAY 95 STE 256 BULLHEAD CITY AZ 86442 9101 1214 E FLORENCE BLVD CASA GRANDE AZ 85222 7236 6767 WEST BELL ROAD GLENDALE AZ 85308 9528 3340 E ANDY DEVINE AVE KINGMAN AZ 86401 3707 1870 MCCULLOCH BLVD LAKE HAVASU CITY AZ 86403 7655 1445 SOUTH POWER ROAD MESA AZ 85206 3188 2840 E MAIN ST MESA AZ 85213 3923 300 WEST MARIPOSA RD NOGALES AZ 85621 3228 2526 W NORTHERN AVENUE PHOENIX AZ 85051 4880 7550 EAST HWY 69 PRESCOTT VALLEY AZ 86314 3924 750 W DEUCE OF CLUBS SHOW LOW AZ 85901 3695 2011 EAST