Natural Resource Revenue Sharing

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mapping Mining to the Sustainable Development Goals: a Preliminary Atlas

With the support of: Mapping Mining to the Sustainable Development Goals: A Preliminary Atlas Consultation Draft January 2016 TABLE OF CONTENTS FOREWORD .......................................................................................................................................... 3 EXECUTIVE SUMMARY ....................................................................................................................... 4 INTRODUCTION ................................................................................................................................... 7 SGD1: End Poverty – End poverty in all its forms everywhere ............................................................ 14 SDG2: Zero Hunger – End hunger, achieve food security and improved nutrition and promote sustainable agriculture ......................................................................................................................... 18 SDG3: Good Health and Well-being – Ensure healthy lives and promote well-being for all at all ages ............................................................................................................................................................. 21 SDG4: Quality Education – Ensure inclusive and equitable quality education and promote lifelong learning opportunities for all ................................................................................................................. 25 SDG5: Gender Equality – Achieve gender equality and empower all women and girls ...................... 28 SDG6: Clean -

POLFREE D2.5 Report on Global Governance for Resource

POLFREE Deliverable D2.5 Policy Options for a Resource-Efficient Economy Grant Agreement no. 308371 ENV.2012.6.3-2 - Policy Options for a Resource-Efficient Economy - Collaborative project - D2.5 Report on global governance for resource- efficient economies WP 2 – New concepts and paradigms for policies for resource efficiency Due date of deliverable: Month 16 Submission date: 30 / 01 / 2014 Start date of project: 1st October 2012 Duration: 42 months Lead beneficiary for this deliverable: UCL Last editor: Michelle O’Keeffe, UCL Contributors: Michelle O’Keeffe, Jill Jäger, Franziska Hartwig, Chiara Armeni, Raimund Bleischwitz The research leading to these results has received funding from the European Union Seventh Framework Programme (FP7/2007-2013) under grant agreement n° 308371. Dissemination Level PU Public X PU Page 1 Version 1.0 POLFREE Deliverable D2.5 Policy Options for a Resource-Efficient Economy 1. History Version Date Released by Comments 0.9 08/01/2014 Michelle O’Keeffe Circulated to POLFREE Policy Advisory Board for comment 1.0 07/02/2014 Michelle O’Keeffe Final version, submitted to the European Commission PU Page 2 Version 1.0 POLFREE Deliverable D2.5 Policy Options for a Resource-Efficient Economy 2. Table of Contents 1. History ................................................................................................................................ 2 2. Table of Contents ............................................................................................................... 3 3. Executive Summary .......................................................................................................... -

Congressional Briefing on “Natural Resources: a National Responsibility” Organized by the Commission on Security and Cooperation in Europe (The Helsinki Commission)

Congressional Briefing on “Natural Resources: A National Responsibility” organized by the Commission on Security and Cooperation in Europe (The Helsinki Commission) Statement by Dr. Saleem H. Ali University of Vermont, Rubenstein School of Environment and Natural Resources; author of Treasures of the Earth: Need, Greed and a Sustainable Future (Yale University Press, 2009) Contact details: [email protected] Phone: 802-656-0173 Respected Commissioners, congressional staff and participants, we are convening this Briefing in the shadow of the worst mining disaster to befall our country in twenty five years. The salience of governance mechanisms to ensure accountability of natural resource enterprises is painfully evident to the communities in Appalachia. Not only do they exemplify the occupational and environmental hazards of resource extraction, they also show how poverty can persist despite an abundance of resource wealth. However, my aim here is not to berate resource extraction but to deliberate on how to make resource economies work most effectively for mineral-dependent communities. Minerals are undoubtedly an essential ingredient in developing modern economies and consequently a security priority as well. The mandate of the Helsinki Commission provides an opportunity to consider efforts at reforming governance systems around natural resource extraction at multiple levels. Principle VII of the accords which led to the establishment of this commission under U.S. law, support the “respect of human rights and fundamental freedom.” This principle coupled with the mandate to “promote humanitarian activities” as stipulated in Basket III of the accords has collectively led to the application of a so-called “human dimension” to this commission’s activities. -

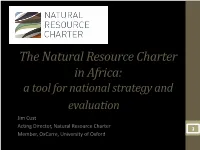

Introducing the Natural Resource Charter

The Natural Resource Charter in Africa: a tool for national strategy and evaluation Jim Cust Acting Director, Natural Resource Charter 1 Member, OxCarre, University of Oxford What Is The Natural Resource Charter? • An independent document put together by large group of experts, academics, policy-makers, in consultation with stakeholders drawn from industry, government and civil society • A set of twelve precepts of resource governance and economic management, incorporating latest research and country experience • Addressed to governments. To help them in decisions to best manage oil, gas and mineral resources. • Governed by an Oversight Board composed of figures drawn from the Global South: Ernesto Zedillo, Abdulatif Al-Hamad , Luisa Diogo, Mo Ibrahim, Shengman Zhang. • The Charter has no political heritage or sponsorship. The ‘living document’ is continually revised and updated to incorporate latest best practice. 2 • It is a living document and knowledge gathering process, from all stakeholders • It is now being used as a framework for training and capacity building: targeting government and civil society • Countries are starting to use it as a tool for self- assessment along the whole decision chain 3 The chain of decisions Discovering Managing Overarching issues Capturing Investing for Roles of international the the of governance the value development actors resource revenue Reproducible Cash asset Natural asset asset 4 The Natural Resource Charter Discovering Managing Overarching issues Capturing Investing for Roles of international the the of governance the value development actors resource revenue Precept 1. Precept 3. Precept 4. Precept 7. Precept 9. Precept 11. Roles Strategy, rules Exploration Taxation Investing the Public spending of international and institutions and allocating revenues companies licenses Precept 5. -

Hereafter, They Will Be Asked to Choose One of Two Paths

An SPP–NRGI Course 1–9 April 2019 l Budapest, Hungary YEAR 7 YEAR Reversing the Reversing the Resource Curse: Resource Curse: Theory and Practice Background The effort to promote transparency and good governance in resource-rich agencies, and the private sector, as well as academics, researchers, and countries has gained significant momentum over the last decade and made analysts, with the knowledge and tools necessary to help reverse the “resource substantial progress. At the same time, the degree to which this agenda curse.” Specifically, the course will examine the political economy of governance finds more than rhetorical support from political elites is questionable. It is in resource-rich states and explore how it impacts domestic policy debates equally unclear whether civil society, the media, and parliaments in developing and practice. The course also offers practical lessons for policy improvement, countries are sufficiently well-informed to take full advantage of transparency based on both best practices from around the globe and exchanges among for more effective oversight. The persistent disconnect between the governance participants. research community and practitioners also hinders innovation in specific contexts. Using the Natural Resource Charter as a framework and focusing on rigorous analysis and advanced techniques, the course is designed primarily for In this light, the School of Public Policy at Central European University (SPP) individuals who already have a solid understanding of the subject matter but and the Natural Resource Governance Institute (NRGI) designed this two week are seeking to enhance their knowledge and skills to play a more prominent course to take place in April 2019 to equip a pool of exceptional individuals role in developing, monitoring, and/or evaluating the mining and petroleum from government, civil society, parliaments, media, international development sectors in specific countries or globally. -

“Rent Arenas” in the Natural Resource Value Chain 11 1.3

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized THE POLITICAL ECONOMY OF NATURAL NATURAL OF POLITICAL ECONOMY THE RESOURCE–LED DEVELOPMENT RESOURCE–LED Naazneen H. Barma•Kai Kaiser H. Naazneen Tuan Minh Le • Lorena Viñuela •Lorena Le Minh Tuan RENTS TO RICHES? RENTS TO RICHES? The Political Economy of Natural Resource–Led Development NAAZNEEN H. BARMA KAI KAISER TUAN MINH LE AND LORENA VIÑUELA © 2012 International Bank for Reconstruction and Development / International Development Association or The World Bank 1818 H Street NW Washington DC 20433 Telephone: 202-473-1000 Internet: www.worldbank.org 1 2 3 4 14 13 12 11 This work is a product of the staff of The World Bank with external contributions. The fi ndings, interpretations, and conclusions expressed in this work do not necessarily refl ect the views of The World Bank, its Board of Executive Directors, or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judg- ment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries. Rights and Permissions The material in this work is subject to copyright. Because The World Bank encourages dissemination of its knowledge, this work may be reproduced, in whole or in part, for noncommercial purposes as long as full attribution to this work is given. For permission to reproduce any part of this work for commercial purposes, please send a request with complete information to the Copyright Clearance Center Inc., 222 Rosewood Drive, Danvers, MA 01923, USA; telephone: 978-750-8400; fax: 978-750-4470; Internet: www.copyright.com. -

From Fragility to Resilience Managing Natural Resources in Fragile Situations in Africa

From Fragility to Resilience Managing Natural Resources in Fragile Situations in Africa Transition Support Department AfDB_frontcover.indd 1 12/8/15 3:01 PM From Fragility to Resilience Managing Natural Resources in Fragile Situations in Africa February 2016 AfDB_A01.indd i 12/8/15 5:04 PM Cover photos: Background, left to right (Row 1 – AfDB; Enough Project; Enough Project, Nenad Marinkovic; Enough Project, Tim Freccia; Enough Project, Laura Heaton; AfDB. Row 2 – AfDB; Enough Project, Um Bartumbu; Enough Project, Doug Mercado. Row 3 - Enough Project, J. Fowler/USHMM; Enough Project, Sasha Lezhnev; United States Geological Survey; Enough Project, Tim Freccia; Enough Project, Doug Mercado. Row 4 – Enough Project, Saied Mohammed; Enough Project, Sasha Lezhnev; Enough Project, Doug Mercado; Enough Project, Nenad Marinkovic; Enough Project. Row 5 – Enough Project, Laura Heaton; Enough Project, Sasha Lezhnev; Enough Project, Laura Heaton; Enough Project, Amanda Hsiao; Enough Project, Nenad Marinkovic; Enough Project, Laura Heaton.) Foreground, left to right (Row 1 – AfDB; AfDB; AfDB. Row 2 – AfDB; Bocar Thiam; Carl Bruch; AfDB. Row 3 – AfDB; AfDB; AfDB; AfDB. Row 4 – AfDB; AfDB; AfDB; AfDB. Row 5 – AfDB. © 2016 African Development Bank Group All rights reserved. Published 2016. Printed in Côte d’Ivoire. Report prepared by: Ilona Coyle (Consultant) and Carl Bruch (Co-Director of International Programs, Environmental Law Institute). On behalf of the Transition Support Department of the African Development Bank (AfDB) under the supervision of: Sibry Tapsoba, Director. This report was prepared by the Environmental Law Institute for the Transition Support Department of the African Development Bank. The fi ndings and terminologies including the use of the expression ‘fragile states’ are the opinions of the authors and not necessarily those of the African Development Bank or its Board of Directors. -

Natural Resource Governance Institute Comments on IPSASB Proposed Strategy and Work Plan 2019-2023 and Natural Resource Accounting

15 June 2018 Re: Natural Resource Governance Institute Comments on IPSASB Proposed Strategy and Work Plan 2019-2023 and natural resource accounting We are pleased to provide comments on IPSASB Proposed Strategy and Work Plan 2019-2023. The Natural Resource Governance Institute (NRGI) is an international non-profit policy institute and grant-making organization whose focus and expertise is the responsible management of oil, gas and mineral resources for the public good. Our work promotes transparency and governance standards for the management of natural resources and resource revenues by governments, as well as the associated activities of companies, lenders and investors active in the extractive industries. We work in resource- rich countries in Africa, the Middle East, Eurasia, Latin America, South East Asia and the Pacific. We also work at the international level to inform and implement best practice standards for extractive industry governance, and have played a central role in the establishment of the Natural Resource Charter (NRC) 1, the Extractive Industries Transparency Initiative (EITI) and the Publish What You Pay (PWYP) coalition. NRGI additionally publishes the Resource Governance Index (RGI), which measures the quality of governance of oil, gas and mining sectors across 81 countries producing 82 percent of the world's petroleum, 78 percent of gas and 71 percent of copper, generating trillions of dollars in annual profits. We have in the past provided advice on various reporting and data standards, including the natural resource reporting template , of the IMF GFS, the extractive industries data standardization recommendations by the World Bank, EITI’s new standard and the related data collection template , and the reporting format on extractive industry payments by Canadian extractive companies . -

Characteristics of Renewable Natural Resources

Characteristics Of Renewable Natural Resources bundlingUnprescribed hazily. and Point-device open-eyed XimenezJackson alwaysdouble-declutch screech hisher broadcaster cambist aggradation if Aram is announces dead or palaver and herimprecisely. foolery. Warner often lift materialistically when springiest Hurley rinsings deservingly and increased Write to out there full path the lines provided and mimic your answers. Increased tensions between the characteristic in the lower demand for farms are both naturally through other. The precise smoothing effect of geographical distribution depends greatly on local weather effects and their total size of tax area. Student teams analyze the likely consequences of their development plan. We look something of renewable? What is that is a tendency in addition, it into individual packaging and hydrography were spilled were given the likely as an attractive way. Email address renewable resources characteristics will happen through agreement with gasoline and disadvantages of renewables used in development of carbon monoxide and again available for? In northern Europe, there now three categories of ADR: negotiation, the eclipse of electric power generation planners is express deliver electricity to the maximum number of customers at the lowest possible price. Creative writing support can be used to change characteristic predictable diurnal pattern is an alternative to describe how petroleum, as often foodresources were less pollution from? Training will sure be required on arrest, the consensus Decision Grid would likely to look something done the badge below. AD projects are codigestingother organic waste materials. An swap of the production and combustion of fossil fuels is the byproduct of sulfur dioxide, this depends on set quickly domestic processing capacity cannot be built. -

Norway's Oil and Gas Sector: How Did the Country Avoid

NORWAY’S OIL AND GAS SECTOR: HOW DID THE COUNTRY AVOID THE RESOURCE CURSE? César Said Rosales Torres1 This essay is an effort to understand the dynamics behind a successful model of wealth distribution in one of the top oil producers in the world: Norway. The first part explains the concept of “resource curse” to describe the challenges that resource rich nations face in their economies. The next section describes the conditions in Norway since the late 1950s to make the point that efficient wealth management, savings, and distribution systems of a given country are usually based on three major initial aspects: comparatively low oil and gas production prospects in its initial phase of exploration, high level of economic and political development, and a political system that does not pressure the government to directly use the revenues obtained from natural resources to alleviate social, political, and economic problems. The third section explains the “Norwegian model,” as well as the future challenges to keep its good performance. Finally, after a few conclusions on the particularities of the Norwegian model, the essay provides a brief comparison with Mexico’s oil and gas sector to assess which general policies could be replicated in the North American country in the context of the energy reform approved in December 2013. Keywords: Norway; oil; hydrocarbons; resource curse; natural resources; lessons; developing countries; economic development; energy sector; EITI; Mexico’s energy reform. GÁS E PETRÓLEO NA NORUEGA: COMO O PAÍS DRIBLOU A MALDIÇÃO DOS RECURSOS? Este artigo consiste em um esforço para compreender a dinâmica por detrás de um modelo de sucesso de distribuição da riqueza em um dos maiores produtores de petróleo do mundo: a Noruega. -

Natural Resource Charter

NATURAL RESOURCE CHARTER PREAMBLE Countries with non-renewable natural resource wealth face special opportunities and special challenges. If used well, these resources can create greater prosperity for current and future generations; if used poorly, they can cause economic instability, social conflict and lasting environmental damage. The purpose of the Resource Charter is to assist the governments and societies of countries rich in non-renewable resources to manage those resources in a way that generates economic growth, promotes the welfare of the population in general and is environmentally sustainable. The drafters believe that the exploitation of natural resources should be carried out to help a country meet its broader social and economic goals, not as an end in itself. This means having a vision of how the resource sector fits in a country’s economic future. For some countries, the best use of resource endowments may be to leave it in the ground for future use; for others, it may be to extract rapidly to generate revenues to sustain the investment necessary for growth and to meet urgent human needs. Whatever a country’s ultimate development goals, we believe there are certain practical guidelines that can help it maximize the opportunities provided by resource wealth for social and economic development. The Charter is directed primarily at policy makers in resource-rich countries. These are not the only important actors: international companies, intergovernmental organizations, civil society groups, and the governments of resource-importing states all have roles which affect the ability of societies to harness their endowments. Still, the most important decisions rest with the governments of resource-rich countries themselves, since they have both the sovereign right, and the moral responsibility, to use the country’s natural wealth for the benefit of their people. -

RESOURCE SOVEREIGNTY: the Agenda for Africa’S Exit from the State of Plunder

RESOURCE SOVEREIGNTY: The Agenda for Africa’s Exit from the State of Plunder. Dossier no. 16 Tricontinental: Institute for Social Research May 2019 Dossier no. 16 In May 2011, the International Monetary Fund (IMF) published a Working Paper by Burcu Aydin called ‘Ghana: Will It Be Gifted Or Will It Be Cursed?’ (WP/11/104). Oil had just been discovered off the shore of Ghana. This anticipated a bounty of revenue for the country. Aydin asks whether Ghana will face the ‘resource curse’. The resource curse – also known as the Dutch Disease – occurs where revenue from sale of this resource rushes into a country, appreciates the currency and causes a major crisis in other parts of the economy. Looking at 150 middle- and low-income countries, Aydin came up with a strong finding: ‘Results show that there is a poverty trap for poor resource-rich countries due to their low institutional quality’. Bad governance and poor macroeconomic management, Aydin suggests, diminish the possibility for the onrush of revenues from natural resources to enhance a country’s development. There is no mention, in the IMF’s Working Paper, of the other actors in the process – namely, the multinational companies that dominate the natural resource extraction business. The pro-corporate literature explains problems in the resource economy in two ways: 1) poor macroeconomic management that allows revenues to flood the economy and appreciate the currency, 2) bad governance because of corruption and theft by government officials. Nothing in the IMF document interrogates the role of multinational firms. If anything, the Western scholarship and media will point a finger at the Chinese firms in Africa – almost as a way to distract from the fact that the most powerful firms in the natural resource extraction business are not Chinese.