Norwegian Public Limited Liability Companies Act

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Nominating and Corporate Governance Committee Charter

HORIZON THERAPEUTICS PUBLIC LIMITED COMPANY CHARTER OF THE NOMINATING AND CORPORATE GOVERNANCE COMMITTEE OF THE BOARD OF DIRECTORS AMENDED EFFECTIVE: 18 FEBRUARY 2021 PURPOSE AND POLICY The primary purpose of the Nominating and Corporate Governance Committee (the “Committee”) of the Board of Directors (the “Board”) of Horizon Therapeutics Public Limited Company, an Irish public limited company (the “Company”), shall be to oversee all aspects of the Company’s corporate governance functions on behalf of the Board, including to (i) make recommendations to the Board regarding corporate governance issues; (ii) identify, review and evaluate candidates to serve as directors of the Company consistent with criteria approved by the Board and review and evaluate incumbent directors; (iii) serve as a focal point for communication between such candidates, non-committee directors and the Company’s management; (iv) nominate candidates to serve as directors; and (v) make other recommendations to the Board regarding affairs relating to the directors of the Company. The Committee shall also provide oversight assistance in connection with the Company’s legal, regulatory and ethical compliance programs, policies and procedures as established by management and the Board. The operation of the Committee and this Nominating and Corporate Governance Charter shall be subject to the constitution of the Company as in effect from time to time and the Irish Companies Act 2014, as amended by the Irish Companies (Amendment) Act 2017, the Irish Companies (Accounting) Act 2017 and as may be subsequently amended, updated or replaced from time to time (the “Companies Act”). COMPOSITION The Committee shall consist of at least two members of the Board. -

The Limited Liability Company: Lessons for Corporate Law

THE LIMITED LIABILITY COMPANY: LESSONS FOR CORPORATE LAW JONATHAN R. MACEY· INTRODUCTION Legal scholarship examining the recent emergence of the limited liability company has primarily focused on the legal treatment of these entities. l A successfully formed limited liability company is a noncorporate entity that provides its owners with protection against liability for enterprise obligations, as well as the pass-through tax treatment traditionally associated with partnerships and Subchapter S corporations. At the same time, the limited liability company form allows investors to remain actively involved in the management of the enterprise. The purpose of this Article is different. Rather than exploring whether (or how well) the limited liability companies achieve their common intended purpose of reducing the contract, tort and tax liabilities of their investors, this Article explores the implications of the emergence of the limited liability company for our understanding of corporate law. What does the modem emergence of the limited liability company tell us about the state ofAmerican corporate law? This Article argues that the emergence of the limited liability company has much to tell us about a variety of important topics in corporate law, particularly the reasons for requiring fonnal incorporation, jurisdictional competition for corporate charters, the costs and benefits oflimited liability, and the structural problems that may hamper sweeping reform ofcorporate and tort law rules affecting enterprise and investor liability. This Article begins with a brief discussion of the limited liability company. The second part of the Article discusses the features that may * J. DuPratt White Professor of Law, Cornell University, and Director, John M. -

Ownership and Control of Private Firms

WJEC BUSINESS STUDIES A LEVEL 2008 Spec. Issue 2 2012 Page 1 RESOURCES. Ownership and Control of Private Firms. Introduction Sole traders are the most popular of business Business managers as a businesses steadily legal forms, owned and often run by a single in- grows in size, are in the main able to cope, dividual they are found on every street corner learn and develop new skills. Change is grad- in the country. A quick examination of a busi- ual, there are few major shocks. Unfortu- ness directory such as yellow pages, will show nately business growth is unlikely to be a that there are thousands in every town or city. steady process, with regular growth of say There are both advantages and disadvantages 5% a year. Instead business growth often oc- to operating as a sole trader, and these are: curs as rapid bursts, followed by a period of steady growth, then followed again by a rapid Advantages. burst in growth.. Easy to set up – it is just a matter of in- The change in legal form of business often forming the Inland Revenue that an individ- mirrors this growth pattern. The move from ual is self employed and registering for sole trader to partnership involves injections class 2 national insurance contributions of further capital, move into new markets or within three months of starting in business. market niches. The switch from partnership Low cost – no legal formalities mean there to private limited company expands the num- is little administrative costs to setting up ber of manager / owners, moves and rear- as a sole trader. -

Limited Liability Partnerships

inbrief Limited Liability Partnerships Inside Key features Incorporation and administration Members’ Agreements Taxation inbrief Introduction Key features • any members’ agreement is a confidential Introduction document; and It first became possible to incorporate limited Originally conceived as a vehicle liability partnerships (“LLPs”) in the UK in 2001 • the accounting and filing requirements are for use by professional practices to after the Limited Liability Partnerships Act 2000 essentially the same as those for a company. obtain the benefit of limited liability came into force. LLPs have an interesting An LLP can be incorporated with two or more background. In the late 1990s some of the major while retaining the tax advantages of members. A company can be a member of an UK accountancy firms faced big negligence claims a partnership, LLPs have a far wider LLP. As noted, it is a distinct legal entity from its and were experiencing a difficult market for use as is evidenced by their increasing members and, accordingly, can contract and own professional indemnity insurance. Their lobbying property in its own right. In this respect, as in popularity as an alternative business of the Government led to the introduction of many others, an LLP is more akin to a company vehicle in a wide range of sectors. the Limited Liability Partnerships Act 2000 which than a partnership. The members of an LLP, like gave birth to the LLP as a new business vehicle in the shareholders of a company, have limited the UK. LLPs were originally seen as vehicles for liability. As he is an agent, when a member professional services partnerships as demonstrated contracts on behalf of the LLP, he binds the LLP as by the almost immediate conversion of the major a director would bind a company. -

AIG Guide to Key Features of Private Limited Companies

PrivateEdge Key features and requirements of private limited companies It is crucial for businesses set up as private limited companies to comply with the requirements of the Companies Act 2006. This guidance note sets out the key legal requirements for private limited companies in the UK, discusses shareholders’ rights and duties, and the process for convening company meetings and the passing of resolutions 1 What is a private limited company? 1.1 A private limited company is the most common form of trading vehicle for companies in the UK. 1.2 The key features and requirements of a private limited company are that: – It will have a separate legal personality from its owners (shareholders). – Responsibility for the management of a company generally falls to its directors; – The liability of each shareholder for the company's debt and other liabilities is generally limited to the amount which remains unpaid on that shareholder's shares; • It must have an issued share capital comprising at least one share. Each issued share must have a fixed nominal value. The ways in which a company can alter its share capital is strictly controlled by the Companies Act 2006 (“CA 2006”). There are also strict statutory controls on a company's ability to make returns of value (dividends) to its shareholders; • It must have at least one director. A private limited company is not required to have a company secretary, although it may choose to do so; and • The nominal value of a private limited company does not have to exceed a specified amount. It is common practice for a private company to be incorporated with a share capital made up of just one £1 share. -

Limited Liability Entities (DE 231LLC)

LIMITED LIABILITY ENTITIES The purpose of this information sheet is to explain Section 675 of the CUIC, the employing unit becomes California’s payroll tax* treatment of the following types of an employer when it employs one or more employees limited liability entities: within California and pays wages in excess of $100 during any calendar quarter. Refer to Information • Limited Liability Company (LLC) Sheet: Employment (DE 231). • Limited Partnership (LP) • Limited Liability Partnership (LLP) • For California Personal Income Tax (PIT) purposes, • Limited Liability Limited Partnership (LLLP) Section 13005(a) of the CUIC specifically includes an LLC as an employer subject to withholding PIT Each of the above business entity types is created when it and reporting PIT wages for its California employees. formally organizes and registers as required by the laws of (For residents performing services within or without the jurisdiction where the organization is formed. They are California, or nonresidents performing services within classified as either domestic or foreign entities. Domestic California, refer to Information Sheet: Multistate entities are those organized in California under the Employment [DE 231D].) California Corporations Code. Foreign entities are organized under the laws of jurisdictions other than California. Before California Payroll Taxes for LLC Members transacting business in California, the foreign entities must first register with the California Secretary of State. Generally, the Internal Revenue Service (IRS) and the Franchise Tax Board (FTB) treat an LLC as a sole LLC ENTITIES proprietorship, partnership, or corporation, depending on the circumstances. However, the CUIC requires the An LLC is a hybrid entity that combines the liability Employment Development Department (EDD) to treat the protection of a corporation with the benefit of pass-through LLC as a unique entity type, instead of classifying it as a taxation of a partnership or sole proprietorship. -

Establishing and Managing a Company

ESTABLISHING AND MANAGING A COMPANY 5.1 Corporate Structures ........................................................ 59 5.2 Accounting ........................................................................ 63 5.3 Auditing ............................................................................. 63 5 5.4 Establishing A Company .................................................. 64 Image Signing a contract, studio shot Establishing a company can be done quickly and easily. 5.1 CORPORATE STRUCTURES Economic freedom, which is guaranteed under the Swiss Consti Numerous official and private organizations assist tution, allows anyone, including foreign nationals, to operate a entrepreneurs in selecting the appropriate legal form for business in Switzerland, to form a company or to hold an interest in one. No approval by the authorities, no membership of chambers of their company and can provide advice and support. commerce or professional associations, and no annual reporting of The federal government’s various websites offer a wide operating figures are required to establish a business. However, foreign nationals must have both work and residence permits in range of information on all aspects of the company order to conduct a business personally on a permanent basis. formation process – from business plan to official Swiss law distinguishes between the following types of business regis tration. entities: partnershiptype unincorporated companies (sole proprietorship, limited partnership or general partnership) and capitalbased incorporated -

Limited Liability with One-Man Companies and Subsidiary Corporations

LIMITED LIABILITY WITH ONE-MAN COMPANIES AND SUBSIDIARY CORPORATIONS Bm Nmw F. CATALDO* Limited liability, usually regarded as the most significant feature of corporate enterprise, has received extravagant praise. Among those who have paid verbal homage to the concept of limited liability are two former university presidents who cut a large figure in the intellectual manners of the nation during the last half century. President Eliot of Harvard regarded limited liability as "the corporation's most precious characteristic" and "by far the most effective legal invention ... made in the nineteenth century."' President Nicholas Murray Butler of Columbia made the pronouncement in i91: "I weigh my words when I say that in my judg- ment the limited liability corporation is the greatest single discovery of modern times.... Even steam and electricity are far less important than the limited liability corporation, and they would be reduced to comparative impotence without it."' Our courts have rested-unnecessarily, it is believed 3 -the concept of limited lia- bility on the legal entity theory. This theory, familiar to every elementary student of corporation law and finance, treats the corporation as a legal persona or juristic person constituting an entity in itself separate and distinct from the members. The essence of this theory, stated in stark terms, is that the shareholders own "the corporation" and the latter owns and operates the assets and the business. The questionable4 but judicially accepted reasoning which regards limited liability as a * A.B. 1929, LL.B. 1932, LL.M. 1936, University of Pennsylvania. Member of Philadelphia bar; Special Attorney, Department of Justice, Washington, D. -

I. Differences Between a Co-Operative and a PC in India II. Comparison Of

I. Differences between a co-operative and a PC in India Feature Co-operative PC Registration under Co-op societies Act Companies Act Membership Open to any individual or co- Only to producer members operative and their agencies Professionals on Board Not provided Can be co-opted Area of operation Restricted Throughout India Relation with other entities Only transaction based Can form joint ventures and alliances Shares Not tradable Tradable within membership only Member stakes No linkage with no. of shares Articles of association can held provide for linking shares and delivery rights Voting rights One person one vote but RoC Only one member one vote and government have veto and non-producer can’t vote power Reserves Can be created if made profit Mandatory to create reserves Profit sharing Limited dividend on capital Based on patronage but reserves must and limit on dividend Role of government Significant Minimal Disclosure and audit Annual report to regulator Very strict as per the requirements Companies Act Administrative control Excessive None External equity No provision No provision Borrowing power Restricted Many options Dispute settlement Through co-op system Through arbitration II. Comparison of diff options for registration under the companies Act Type of company> Private limited Limited Company PC Parameter Company Minimum No. of 2 3 5 Directors required Number of Members Minimum 2; Minimum 7 Minimum 10 primary Maximum 50 producer members or two producer institutional members Membership Any one Any one Only primary eligibility producer or producer institutions can be member. Type of shares Equity and Equity and Preference Only Equity Preference Voting rights based on number of based on number of Only one vote equity shares held equity shares held irrespective of number of shares held. -

Differences Between Joint Stock and Limited Liability Companies in Turkey

PART 4 BY ELİF ECE CESUR | [email protected] DIFFERENCES BETWEEN JOINT STOCK AND LIMITED LIABILITY COMPANIES IN TURKEY he new Turkish Commercial Code (NTCC) tthat came into force on July 1st 2012 conveyed important changes to businesses and company law. Apart from providing general information on joint stock and limited liability companies, this article aims to set out the innovation transported by the NTCC and distinguish the two types of corporations. Turkish Joint Stock Company (Anonim Șirket), is a corpo- ration that has a title, with a certain capital, divided into shares that is only liable to its creditors with its assets. Both types of corporations are classed as stock corpora- tions although Turkish joint stock companies are typical stock corporations with legal identity and title1. Com- pany capital is registered and divided into shares. All the debts and obligations owed to third parties are owed by the company itself, not by the members or directors. Joint stock company is only liable to its creditors with its assets; members’ liability is limited to the value of their shares. Company could be established for all kinds of commercial purposes that are not restricted by law. It has its own legal identity separate from that of the human beings who are involved in the company. There is a transferability of own- ership, shares can easily be bought and sold. This provides for small capital to come together to form large funds and undertake greater business that would not be possible otherwise. Turkish Limited Liability Company (Limited Șirket) is formed by one or more real or legal persons gathering under a commercial title. -

The German Supervisory Board

The German Supervisory Board: A Practical Introduction for US Public Company Directors The German Supervisory Board: | A Practical Introduction for US Public Company Directors The German Supervisory Board: | A Practical Introduction for US Public Company Directors Contents Foreword Foreword 03 As the world’s economy globalizes, there is often an expectation that business practices will Executive Summary 04 harmonize along with it. This is an expectation The German Supervisory Board: Characteristics and Context 05 that we will see a kind of convergence of corporate The German Supervisory Board in Action: Regular Order, M&A, Crisis 14 governance forms and practices, where boards the world over resemble each other, perhaps Conclusion 15 with a large majority of independent directors, an Endnotes 17 audit committee, a separate chair and CEO, and so on. A lot of this reflects a certain familiarity Claus Buhleier with the Anglo-Saxon board model among Partner, Center for Corporate institutional investors in London and New York. Governance Deloitte Germany [email protected] The reality, however, is quite different. Despite real advances in globalization in other areas, differences in what boards look like and how they work in practice persist across countries. This publication brings to light the differences between the predominant Anglo Saxon, one-tier corporate governance model on the one hand, and the still influential Germanic two-tier-model on the other. The authors, Yvonne Schlaeppi and Michael Marquardt, both experienced corporate directors Kai Bruehl who have served on European company boards, Director, Risk Advisory Deloitte highlight the main characteristics of the German Germany [email protected] supervisory board model and how it demands accountability from its members, despite looking rather different than the combined board model. -

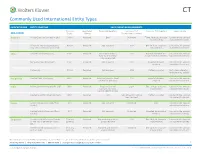

Commonly Used International Entity Types

Commonly Used International Entity Types COUNTRY/REGION ENTITY STRUCTURE BASIC FORMATION REQUIREMENTS Minimum Registered Corporate Secretary Minimum # of Minimum # of Directors Legal Liability ASIA-PACIFIC Capital Address Shareholders/Partners Australia Public Company (Limited or Ltd.) AUD 0 Required One Unlimited Three. At least 2 must be Limited to the amount local residents subscribed for shares Private or Proprietary Company AUD 0 Required Not required 1-50 One. At least 1 must be Limited to the amount (Pty. Ltd. or Proprietary Limited) local resident subscribed for shares China Limited Liability Company CNY 0 Required Not required. But a 1-50 Board of directors or a Limited to the amount local representative single executive director subscribed for shares may be required. Company Limited by Shares CNY 0 Required Not required 2-200 Board of directors Limited to the amount required subscribed for shares Partnership CNY 0 Required Not required 2-50 Partner managed Not a separate legal entity from its parent Hong Kong Limited Private Company HKD 0 Required Required, must be local 1-50 Board of directors Limited to the amount resident or company required subscribed for shares India Private Limited Company (Pvt Ltd) INR 0 Required Required if initial 2-200 Two. At least 1 must be Limited to the amount capital investment local resident subscribed for shares exceeds INR100 million Limited Liability Partnership (LLP) INR 0 Required N/A Two. At least 1 must be Partner managed Limited to the amount local resident subscribed for shares Japan General Corporation (Kabushiki JPY 1 Required Not required Unlimited One Limited to the amount Kaisha) subscribed for shares Limited Liability Company (Godo- JPY 1 Required Not required Unlimited Managed by managing Limited to the amount Kaisha) members subscribed for shares Singapore Private Limited Company (Private $1 in any Required Required and must be 1-50 One.