Waterloo Food Flow Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Neilson Dairy Sold to Saputo

www.independentfreepress.com Recipe ofTHE the week: INDEPENDENT Wheels & Car Care Spinach quiche special section Page 23 & FREE PRESS 8-Pages 50 cents (+GST) Circulation 22,500 Friday, October 24, 2008 56 Pages Halton Hills’ award-winning newspaper INSIDE Local workforce remains unchanged Neilson Dairy sold to Saputo LISA TALLYN Where did the Staff Writer downtown flowers go? George Weston Ltd. has sold its Neilson Dairy business to Saputo Inc. for $465 million. The Guelph St. Georgetown location is one of Page 7 two plants owned by Weston. The other plant is located in Ottawa and combined they employ 390 employees. Karine Vachon, a spokesperson for Saputo Inc., said under the agreed-upon deal, which is expected to close Nov. 24 subject to approval by the Competition Bureau, “Saputo will continue business as usual” at Neilson. “Work force and operations will remain the same,” said Vachon when asked if there would be any staff reductions at the Georgetown plant. Geoff Wilson, senior vice-president of George Weston Ltd., also said it was his “understanding Parenting everyone is moving over” and there would be no special impact to staff in Georgetown. According to Halton Hills Chamber of section Commerce the Georgetown plant employs 200 full-time and 150 part-time employees. 4-Pages Vachon said the “Neilson” brand would also remain the same. Wilson called the sale, “a great fit for Saputo and very good for Weston and its shareholders.” Editorial 6 “We believe this transaction allows Neilson Dairy to continue to grow under the national Calendar 10, 11 presence of Canada’s largest dairy processor,” said Entertainment 14 Wilson. -

PRESS RELEASE Saputo Inc. Completes the Acquisition of The

PRESS RELEASE Saputo Inc. completes the acquisition of the activities of Neilson Dairy (Montréal, December 1, 2008) – Saputo Inc. completed today the transaction announced on October 22, 2008 and acquired the activities of Neilson Dairy, the dairy division of Weston Foods (Canada) Inc. which manufactures, sells and distributes, primarily in Ontario, fluid milk and dairy beverages, cream products and non dairy creamers, butter, yogurt, juices and drinks under the Neilson brand and other brands (Neilson Dairy). Neilson Dairy employs approximately 390 people at its two facilities located in Halton Hills and Ottawa, Ontario. It generates annual sales of approximately $600 million and annual earnings before interest, income taxes, depreciation and amortization of approximately $50 million. The purchase price of $465 million on a debt-free basis was paid in cash by drawing on available lines of credit and additional financing. This transaction will enable Saputo Dairy Products Division (Canada) to increase its presence in the Ontario fluid milk and cream market. Neilson Dairy primarily operates within the retail market segment and, as part of the transaction, Saputo inherits Neilson Dairy’s long term relationships with its customers. About Saputo Together, over the years, we have aspired to grow, exploring new opportunities while staying true to our culture. Our progress is owed to the continued dedication of our 9,500 employees, who, across 5 countries, team up every day to go further. They craft, market and distribute a wide range of high- quality products, including cheese, fluid milk, yogurt, dairy ingredients and snack-cakes. Saputo is the 15th largest dairy processor in the world, the largest in Canada, the third largest in Argentina, among the top three cheese producers in the United States, and the largest snack-cake manufacturer in Canada. -

Woodgreen AR 7

Woodgreen AR 04 5 10/12/04 12:56 PM Page 2 WOODGREEN COMMUNITY SERVICES ANNUAL REPORT 2003/2004 WOODGREEN COMMUNITY SERVICES ANNUAL REPORT 2003/2004 Because Everyone WOODGREEN Deserves the COMMUNITY SERVICES 835 Queen Street East Essentials of Life Toronto, Ontario M4M 1H9 Tel: (416) 469-5211 www.woodgreen.org Charitable Registration No. 10822 0435 RR0002 Woodgreen AR 04 5 10/12/04 12:56 PM Page 4 Maintaining independence and dignity Mary is a retired professional with Alzheimer’s disease. Her husband, who works full time, could no longer leave her home alone during the day because Last year, WoodGreen provided she needed constant supervision. Mary’s essential services to more than husband did not want to admit her to 6,000 seniors and caregivers in the community. a long term care facility – he wanted to keep his wife at home and in their familiar neighbourhood. Mary and her husband turned to WoodGreen’s Adult love to hold the hand of our staff, go for a walk in Day Program so Mary could be in a safe environment the garden patio and participate in activities with during the day, where she could be helped to maintain other seniors in the program. the best physical and cognitive functioning possible. Thanks to WoodGreen, Mary is one of more By participating in the Adult Day Program, Mary has than 70 seniors in the Adult Day Program who are made friends and she has lots of opportunity for able to continue to live at home with their families social interaction. While she may have lost a lot in and loved ones – helping them maintain dignity terms of her cognitive functioning, she continues to and independence. -

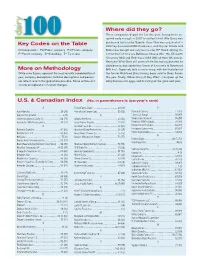

Key Codes on the Table More on Methodology Where Did They

Where did they go? Three companies depart the list this year, having been ac- quired early enough in 2007 to not be listed. Alto Dairy was Key Codes on the Table purchased last year by Saputo, Cass Clay was acquired at in 2007 by Associated Milk Producers, and Crystal Cream and C=Cooperative Pu=Public company Pr=Private company Butter was bought out early last year by HP Hood. Joining the P=Parent company S=Subsidiary T= Tie in rank list for the first time are BelGioso Cheese (No. 75), Ellsworth Creamery (84) and Roth Kase USA (96) all from Wisconsin. Next year Winn-Dixie will come off the list, having divested its dairy processing capabilities (some of it recently to Southeast More on Methodology Milk Inc.). Supervalu tells a similar story, with the final plant of While sales figures represent the most recently completed fiscal the former Richfood Dairy having been sold to Dean Foods year, company descriptions, facilities descriptions and person- this year. Finally, Wilcox Dairy of Roy, Wash., has given up the nel reflect recent changed where possible. Some entries will dairy business for eggs, and its listing will be gone next year. include an explanation of recent changes. U.S. & Canadian Index (No. in parentheses is last year’s rank) A Foster Farms Dairy ....................................... 50 (48) P Agri-Mark Inc. .............................................. 29 (29) Friendly Ice Cream Corp. ...............................55 (56) Parmalat Canada .........................................12 (13) Agropur Cooperative .........................................6 (9) G Perry’s Ice Cream ........................................ 97 (97) Anderson Erickson Dairy Co. ......................... 66 (71) Glanbia Foods Inc. ........................................ 23 (32) Plains Dairy Products ....................................95 (99) Associated Milk Producers Inc. -

2001 Annual Report

Annual Report 2001 George Weston Limited on the rise Financial Highlights 2 | Report to Shareholders 3 | Operating Review 8 | Management’s Discussion and Analysis 14 Consolidated Financial Statements 29 | Eleven Year Summary 48 | Results by Quarter 51 | Contributing to the Community 52 Corporate Directory 53 | Operating Group Directory and Shareholder Information 54 George Weston Limited is a broadly based Canadian company founded in Weston at a Glance ➝ 1882. It operates in two distinct business segments: Food Processing, which encompasses fresh and frozen bakeries, biscuit, dairy and fresh farmed salmon operations; and Food Distribution, operated through Loblaw Companies Limited, the largest food distributor in Canada. Sales in 2001 reached a new high of $25 billion, exceeding 2000 sales by more than $2 billion including the effects of the July, 2001 acquisition of Bestfoods Baking Co., Inc., which added such well known brands as Thomas’ English muffins, Entenmann’s sweet baked goods and Arnold Brick Oven bread. Basic net earnings per common share, including unusual items, net of tax, were $4.42, 21% or 76 cents above the $3.66 earned in 2000. Basic net earnings per common share, excluding the 2001 unusual items and the effects of the 2000 federal and provincial tax rate reductions on future income tax balances, improved 19% to $4.00 from the $3.35 earned in 2000. George Weston Limited is committed to creating value for its shareholders and to participating along with its more than 139,000 employees throughout its businesses in supporting -

UPDATED and RESTATED ANNUAL INFORMATION FORM June 2, 2014

UPDATED AND RESTATED ANNUAL INFORMATION FORM (for the year ended December 28, 2013; updated to June 2, 2014) June 2, 2014 LOBLAW COMPANIES LIMITED UPDATED AND RESTATED ANNUAL INFORMATION FORM (for the year ended December 28, 2013; updated to June 2, 2014) TABLE OF CONTENTS DATE OF INFORMATION .............................................................................................................................................................. 3 FORWARD-LOOKING STATEMENTS .......................................................................................................................................... 3 CORPORATE STRUCTURE .......................................................................................................................................................... 4 Incorporation ................................................................................................................................................................................... 4 Intercorporate Relationships ........................................................................................................................................................... 4 GENERAL DEVELOPMENT OF THE BUSINESS ........................................................................................................................ 5 Retail…. .......................................................................................................................................................................................... 6 Financial Services ........................................................................................................................................................................ -

Communication Creative 184

Table of Contents 2. A Message from the IABC/Toronto President 3. A Message from the Ovation Awards Organizers 4. OVATION Awards Gala Sponsors 5. 2009 IABC/Toronto OVATION Award Winners 15. IABC/Toronto Awards of Distinction 15. 2009 IABC/Toronto MAVERICK PR Student of the Year Award 15. Bobbie Resnick Philanthropy Award 16. Independent or Small Agency of the Year 16. Agency of the Year 16. Corporate Communications Department of the Year 16. People‘s Choice Award 17. 2009 OVATION Awards Winning Entries Communication Management 17. Brand Communication 22. Community Relations 28. Electronic and Digital Communication 40. Employee/Member/HR Communications 68. Issues Management and Crisis Communication 74. Marketing Communications 86. Media Relations sponsored by News Canada 113. Social Responsibility including Economic, Societal and Environmental Development 138. Special Events Communication Skills 150. Audiovisual 156. Electronic/Interactive Communication 160. Publications 170. Writing Communication Creative 184. Publication Design Awards of Distinction 189. 2009 IABC/Toronto MAVERICK PR Student of the Year Award 192. Bobbie Resnick Philanthropy Award 197. People‘s Choice Award 203. OVATION Awards Judges 204. OVATION Awards Judges‘ Biographies 211. 2008/2009 IABC/Toronto Board 212. 2009 OVATION Awards Committee Members 1 A Message from the IABC/Toronto President In 1985, IABC/Toronto established the OVATION Awards to challenge communicators to take stock of their best campaigns and subject them to the scrutiny of accredited and accomplished peers – who select those few that exemplify excellence in communications. This year, communicators throughout the chapter demonstrated a heightened drive to excel by submitting a record breaking number of entries to both the OVATION Awards and the Bobbie Resnick Philanthropy Award. -

“Veggemo” Non-Dairy Vegetable Based Beverage Line Across Canada

GLOBAL GARDENS GROUP – VEGGEMO NOW AVAILABLE IN LOBLAWS Vancouver, BC, November 3, 2016 – Global Gardens Group Inc. (the "Company") (CSE: VGM) is pleased to announce that it has increased the in-store distribution of its “Veggemo” non-dairy vegetable based beverage line across Canada. Veggemo is now available in approximately 400 Loblaw Companies Limited stores. Veggemo can be found in select Loblaws, Fortinos, Zehrs, Provigo, Real Atlantic Superstores and Real Canadian Superstores across Canada. Veggemo will be merchandised in those stores which have a “natural products section” providing an excellent healthy product assortment to customers. “We are thrilled to have Veggemo available in a multitude of Loblaw Companies Ltd. banners and in hundreds of stores,” comments Global Gardens Group President and CEO, Rob Harrison. Mr. Harrison continued, “Loblaw’s purpose – Live Life Well – supports the needs and well-being of Canadians, is well connected to the growth of consumers making healthier food choices and is consistent with Veggemo’s allergen friendly, nutritious, cholesterol and GMO free veggie based non-dairy beverage.” With the addition of Loblaw banners stores, Veggemo is now available in over 2000 locations across Canada. This new listing complements the brand’s availability already secured in Sobeys, Metro, Longos, Calgary Coop, Save-On-Foods, Urban Fare, Price Smart, Thrifty Foods, IGA Market Place, Whole Foods B.C., London Drugs and select Walmart locations. Veggemo has received many awards and accolades including being named 1 of 10 most innovative new products at the 2015 Grocery Innovation Canada Show; out of over 500 entries was 1 of 3 finalist brands for “Best New Beverage” for the coveted NEXTY Awards at the Natural Products Show in Anaheim, California; and at the same show was voted the “Best New Vegan Product” by VegNews. -

THE TORONTO STAR In-Home Care

28 OAKVILLE BEAVER, Wednesday, January 30, 2008 $375/MO. Room for rent, **A1 Mattress Factory- KITCHEN Cabinets, oak, 3 WASHER/ Dryer, moffat, 1990 Honda Accord LX. kitchen facilities, separate *Free Delivery* Ortho- pantry cupboards, lower & heavy duty, 7 cycle, Ener- Excellent running condi- HEALTHY'S entrance. Close to Oakville petic sets starting at upper- complete; pool ta- guide, white, $200/ pair. tion. Lady driven, used Place. Non-smoker. 905- $240, Delux Pillow-top ble, slate, new black felt; Call 905-829-8320. everyday, selling as is Nutrition Stores 842-0272. $445, no flip Pillow-top full size beer fridge; bar. $2000 o.b.o. 905-336- requires $395. Euro-top $445. Fu- Best offer 905-631-7624 0599 FURNISHED Room(s) in tons available. Water- • Managers executive home. Ensuite beds Black leather soft, LAWN Mower, Trimmer, 1996 Hyundai Elantra, • Supplement super single & queen. Treadmill, Baby Stroller, auto, excellent condition, bathroom; kitchen area; ATTENTION Buying fur Complete w/frame, mat- Car seat, crib mattress, white, 149,000km, runs Advisors(F & P/T) use of rec room; laundry; coats, jewelery, gold and tress, heater. Starting bedroom set, dinning table great, e-tested, will certify. pool; parking. Non-smok- silver coins. Coin Collec- New Store Opening $395. 905-847-2020; 905- with chairs, bookcase, so- $1875.obo. 905-257-1925 er. $500 per room or $900 tions, sterling silver. Moor- in Milton Feb./08 for both rooms if required 681-9496 fa, love seat. 905-635- 4761 croft pottery 905-633-7531 by one person (could be 1997 Chrysler Intrepid, Fax resume to Dale: used as home office) 905- 905-913-1008 LEATHER! 3 piece Italian power windows, power 469-7383 set. -

Proquest Dissertations

INDEPENDENT FOOD RETAILING: EXPLORING THE INTERFACE BETWEEN CONVENTIONAL AND ALTERNATIVE 'LOCAL' FOOD SYSTEMS A Thesis Presented to The Faculty of Graduate Studies of The University of Guelph by EMILY LOUISE SHAPIRO In partial fulfilment of requirements for the degree of Master of the Arts August, 2008 © Emily Shapiro, 2008 Library and Bibliotheque et 1*1 Archives Canada Archives Canada Published Heritage Direction du Branch Patrimoine de I'edition 395 Wellington Street 395, rue Wellington Ottawa ON K1A0N4 Ottawa ON K1A0N4 Canada Canada Your file Votre reference ISBN: 978-0-494-42835-1 Our file Notre reference ISBN: 978-0-494-42835-1 NOTICE: AVIS: The author has granted a non L'auteur a accorde une licence non exclusive exclusive license allowing Library permettant a la Bibliotheque et Archives and Archives Canada to reproduce, Canada de reproduire, publier, archiver, publish, archive, preserve, conserve, sauvegarder, conserver, transmettre au public communicate to the public by par telecommunication ou par Plntemet, prefer, telecommunication or on the Internet, distribuer et vendre des theses partout dans loan, distribute and sell theses le monde, a des fins commerciales ou autres, worldwide, for commercial or non sur support microforme, papier, electronique commercial purposes, in microform, et/ou autres formats. paper, electronic and/or any other formats. The author retains copyright L'auteur conserve la propriete du droit d'auteur ownership and moral rights in et des droits moraux qui protege cette these. this thesis. Neither the thesis Ni la these ni des extraits substantiels de nor substantial extracts from it celle-ci ne doivent etre imprimes ou autrement may be printed or otherwise reproduits sans son autorisation. -

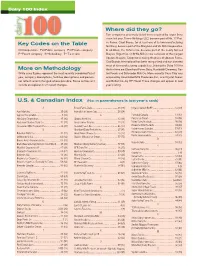

Key Codes on the Table More on Methodology Where Did They

Dairy 100 Index Where did they go? Two companies previously listed were acquired by larger firms since last year. Turner Holdings LLC, became part of No. 17 Prai- Key Codes on the Table rie Farms. Giant Foods, (or at least one of its two manufacturing facilities), became part of the Maryland and Va. Milk Cooperative. C=Cooperative Pu=Public company Pr=Private company In addition, the Yofarm Co. became part of the newly formed P=Parent company S=Subsidiary T= Tie in rank Breyers Yogurt Co. O-At-Ka Milk is now a division of the merged Upstate Niagara Cooperative taking the place of Upstate Farms. CoolBrands International has been reorganized and has divested most of its manufacturing capabilities. Joining the Dairy 100 for More on Methodology the first time are Cloverland Farms Dairy, Humboldt Creamery, Sar- While sales figures represent the most recently completed fiscal tori Foods and Schroeder Milk Co. More recently Cass Clay was year, company descriptions, facilities descriptions and person- acquired by Associated Milk Producers Inc., and Crystal Cream nel reflect recent changed where possible. Some entries will and Butter Co., by HP Hood. Those changes will appear in next include an explanation of recent changes. year’s listing. U.S. & Canadian Index (No. in parentheses is last year’s rank) A Foster Farms Dairy ....................................... 48 (49) Organic Valley/CROPP .................................. 52 (59) Agri-Mark Inc. .............................................. 29 (28) Friendly Ice Cream Corp. ...............................56 (54) P Agropur Cooperative .......................................9 (10) G Parmalat Canada .........................................13 (13) Alto Dairy Cooperative................................... 37 (36) Glanbia Foods Inc. ........................................ 32 (31) Perry’s Ice Cream ....................................... -

View Annual Report

Dedicated Everyday 2010 AnnuAl report WHEN DEDICATION LEADS TO SUCCESS By being dedicated everyday, Saputo’s 9,800 employees contribute to the success of the Company. Since its humble beginnings, Saputo Inc. has grown to become the 12th largest dairy processor in the world, the largest in Canada, the 3rd largest in Argentina, among the top 3 cheese producers in the United States and the largest snack-cake manufacturer in Canada. By being dedicated everyday, we process approximately 6 billion litres of raw milk per year and are determined to reach new heights. We remain focused on being better and stronger through optimization of our activities, product innovation and acquisitions. By being dedicated everyday, we strive to provide consumers with high quality products including cheese, fluid milk, yogurt, dairy ingredients and snack-cakes. Our major brands such as Saputo, Alexis de Portneuf, Armstrong, Baxter, Dairyland, Danscorella, De Lucia, Dragone, DuVillage 1860, Frigo Cheese Heads, Kingsey, La Paulina, Neilson, Nutrilait, Ricrem, Stella, Treasure Cave, HOP&GO!, Rondeau and Vachon are well-known and distributed in over 40 countries worldwide. our organizaTion 2 SectorS 5 DiviSionS Dairy ProDucts • Dairy ProDucts Division (canaDa) • Dairy ProDucts Division (euroPe) Canada, EuropE and argEntina (CEa) dairy produCts Sector • Dairy ProDucts Division (argentina) USA dairy produCts Sector • Dairy ProDucts Division (USA) grocery ProDucts • Bakery Division DAIRY PRODUCTS SECTOR GROCERY ProDucts as at March 31, 2010 CEA USA sector number of Plants 30 15 1 Saputo Inc. (Company or Saputo) is a publicly number of traded company whose shares are listed on the Employees 5,990 2,927 936 Toronto Stock Exchange under the symbol SAP.