In California's Congressional Districts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Women and Equality

WOMEN AND EQUALITY A California Review of Women’s Equity Issues in Civil Rights, Education and the Workplace California Senate Office of Research February 1999 Dedicated to Senator Rose Ann Vuich Rose Ann Vuich was elected California’s first woman state senator in 1976 and served four terms through 1992. Although a Democrat by registration, she built a reputation as a political independent who shunned deal-making. Throughout her legislative career, Senator Vuich represented her San Joaquin Valley district first and foremost and relied on her own knowledge and judgment to do it. She was reared on a farm in Tulare County, where she has spent most of her life. With a degree in accounting from the Central California Commercial College in Fresno, she worked as an accountant, tax consultant, estate planner and office manager before her election. After becoming a senator she continued, with her brother, to manage the family farm in Dinuba. The California State Senate began to change after Senator Vuich joined its ranks, followed over the years by other women. She kept a small porcelain bell on her Senate floor desk, and would gently but insistently shake it whenever a colleague addressed the “gentlemen of the Senate.” The Senate chamber originally had no women’s restroom. But that oversight permitted Senator Vuich, during a Capitol restoration in the late 1970s, to design a comfortable “Rose Room” where she and women members into the future could retreat from the Senate floor. A daughter of Yugoslav immigrants, Senator Vuich achieved many “firsts,” from serving as the first woman president of the Dinuba Chamber of Commerce to becoming the first woman to preside over a Senate floor session in 1986. -

OUR VISION for TAX REFORM Pursue a Bipartisan Process | Address the Debt | Prioritize the Middle Class | Create Jobs | Invest in Infrastructure

OUR VISION FOR TAX REFORM Pursue a Bipartisan Process | Address the Debt | Prioritize the Middle Class | Create Jobs | Invest in Infrastructure October 4, 2017 THE BLUE DOG COALITION The Blue Dog Coalition is an official caucus in the U.S. House of Representatives comprised of 18 fiscally-responsible Democrats, who are leading the way to find commonsense solutions. They represent the center of the political spectrum, appealing to the mainstream values of the American public. The Blue Dogs are dedicated to pursuing fiscally-responsible policies, ensuring a strong national defense, and transcending party lines to get things done for the American people. [COALITION LEADERSHIP] Rep. Jim Costa (CA-16) Co-Chair for Administration Rep. Henry Cuellar (TX-28) Co-Chair for Communications Rep. Daniel Lipinski (IL-3) Co-Chair for Policy [POLICY TASK FORCE LEADERSHIP] Rep. Charlie Crist (FL-13) Co-Chair, Task Force on Economic Growth Rep. Lou Correa (CA-46) Co-Chair, Task Force on Economic Growth Rep. Josh Gottheimer (NJ-5) Co-Chair, Task Force on Fiscal Responsibility Rep. Stephanie Murphy (FL-7) Co-Chair, Task Force on Fiscal Responsibility Rep. Tom O’Halleran (AZ-1) Co-Chair, Task Force on Government Reform and Accountability Rep. Kurt Schrader (OR-5) Co-Chair, Task Force on Government Reform and Accountability Rep. Vicente Gonzalez (TX-15) Co-Chair, Task Force on National Defense Rep. Brad Schneider (IL-10) Co-Chair, Task Force on National Defense [MEMBERS] Rep. Sanford Bishop (GA-2) Rep. Jim Cooper (TN-5) Rep. Collin Peterson (MN-7) Rep. David Scott (GA-13) Rep. Kyrsten Sinema (AZ-9) Rep. -

New Congress

Elected Officials for 117th Congress, 1st session Green = new; Yellow = seat changed party; AL = At large (single district) Uncalled races are highlighted in red and will be updated as results are finalized ALABAMA Sen. Alex Padilla (appt’d) D-CA NEW Sen. Tommy Tuberville R-AL NEW Doug LaMalfa (R-CA-01) Re-elected Sen Richard Shelby R-AL Incumbent Jared Huffman (D-CA-02) Re-elected Jerry Carl (R-AL-01) NEW John Garamendi (D-CA-03) Re-elected Barry Moore (R-AL-02) NEW Tom McClintock (R-CA-04) Re-elected Mike Rogers (R-AL-03) Re-elected Mike Thompson (D-CA-05) Re-elected Robert Aderholt (R-AL-04) Re-elected Doris Matsui (D-CA-06) Re-elected Mo Brooks (R-AL-05) Re-elected Ami Bera (D-CA-07) Re-elected Gary Palmer (R-AL-06) Re-elected Jay Obernolte (R-CA-08) NEW Terri Sewell (D-AL-07) Re-elected Jerry McNerney (D-CA-09) Re-elected Josh Harder (D-CA-10) Re-elected ALASKA Mark DeSaulnier (D-CA-11) Re-elected Sen. Lisa Murkowski R-AK Incumbent Nancy Pelosi (D-CA-12) Re-elected Sen. Dan Sullivan R-AK Re-elected Barbara Lee (D-CA-13) Re-elected Don Young (R-AK-AL) Re-elected Jackie Speier (D-CA-14) Re-elected Eric Swalwell (D-CA-15) Re-elected ARIZONA Jim Costa (D-CA-16) Re-elected Sen. Mark Kelly D-AZ NEW Ro Khanna (D-CA-17) Re-elected Sen. Krysten Sinema D-AZ Incumbent Anna Eshoo (D-CA-18) Re-elected Tom O’Halleran (D-AZ-01) Re-elected Zoe Lofgren (D-CA-19) Re-elected Ann Kirkpatrick (D-AZ-02) Re-elected Jimmy Panetta (D-CA-20) Re-elected Raul Grijalva (D-AZ-03) Re-elected David Valadao (*prev served) (R-CA-21) NEW* Paul Gosar (R-AZ-04) Re-elected Devin Nunes (R-CA-22) Re-elected Andy Biggs (R-AZ-05) Re-elected Kevin McCarthy (R-CA-23) Re-elected Dave Schweikert (R-AZ-06) Re-elected Salud Carbajal (D-CA-24) Re-elected Ruben Gallego (D-AZ-07) Re-elected Mike Garcia (R-CA-25) Re-elected Debbie Lesko (R-AZ-08) Re-elected Julia Brownley (D-CA-26) Re-elected Greg Stanton (D-AZ-09) Re-elected Judy Chu (D-CA-27) Re-elected Adam Schiff (D-CA-28) Re-elected ARKANSAS Tony Cardenas (D-CA-29) Re-elected Sen. -

Calling on the Census Bureau

September 3, 2020 Dr. Steven Dillingham Director United States Census Bureau 4600 Silver Hill Road Washington, DC 20233 Dear Dr. Dillingham: This letter is to inquire about the U.S. Census Bureau’s plans for accurately counting our country’s population in the 2020 Census. In California, nearly 15 percent of our residents remain uncounted, many in historically undercounted communities at risk of losing federal funding and resources. In light of the challenges created by COVID-19, the fires burning across California, and the recent decision to end counting operations early, we ask that you provide additional detail about how a complete count will be achieved. It is our understanding that with the shortened counting timeline, Census Bureau workers will need to visit 8 million more homes nationwide than in 2010, in just seven weeks instead of ten weeks. Data accuracy and review procedures for processing apportionment counts have also been reduced from six months to three months. Additional obstacles caused by COVID-19 include a higher number of people experiencing homelessness—an historically undercounted population—as well as difficulties with hiring and retention of census workers. Given these significant barriers to a fair and accurate census, we would appreciate answers to the following questions. With in-person counting operations cut short, the Census Bureau will likely need to utilize administrative records and statistical techniques to complete the enumeration. Do you now anticipate any changes in the number of households that will -

The New Democrat 2 August 2019

TThhee NNeeww DDeemmooccrraatt A Publication of the Peninsula Democratic Coalition (PDC) August 2019 Congresswoman Anna Eshoo Mark Your (CD-18) traveled to Texas Calendar! detention centers: “The Sunday, August 18, 2019 conditions are Inhumane” 4:00-7:00 pm Congresswoman Eshoo Tours Texas Border and Speaks with Border Officials, Families, and Volunteers WASHINGTON, D.C. — Congresswoman Anna PDC Annual G. Eshoo (D-CA) traveled to McAllen and Brownsville, Texas recently Family Potluck to tour the McAllen Border Patrol Processing Center and the Brownsville Port of Picnic & Entry on Saturday, July 13. Eshoo assessed firsthand the deterioration of care in Funwildl ber heald ait as er Texas since her first visit in June 2018. The Cuesta Park , Congresswoman met with located directly beside the El Camino families, questioned U.S. Rep. Anna Eshoo, right, spoke border officials, and heard with a Border Patrol agent in Texas YMCA and El Camino Hospital, from humanitarian on June 22, 2018, during a tour volunteers. Rep. Eshoo with congressional members of in Mountain View. released the following immigration detention facilities. statement after the trip: Photo courtesy of Rep. Anna “The conditions I Eshoo's office. Special Guest witnessed at the border were inhumane. Forty or more detainees are being kept in cells built to Speaker: house a maximum of eight people for days or even weeks, and children are without access to proper hygiene. Since my first visit Ricardo Lara to the southern border last year, the crisis has worsened and it’s clear the Administration’s policies have exacerbated the Insurance humanitarian crisis. The decision to suspend foreign aid to Commissioner of countries in the Northern Triangle has been catastrophic. -

Lobbying Contribution Report

8/1/2016 LD203 Contribution Report LOBBYING CONTRIBUTION REPORT Clerk of the House of Representatives • Legislative Resource Center • 135 Cannon Building • Washington, DC 20515 Secretary of the Senate • Office of Public Records • 232 Hart Building • Washington, DC 20510 1. FILER TYPE AND NAME 2. IDENTIFICATION NUMBERS Type: House Registrant ID: Organization Lobbyist 35195 Organization Name: Senate Registrant ID: Honeywell International 57453 3. REPORTING PERIOD 4. CONTACT INFORMATION Year: Contact Name: 2016 Ms.Stacey Bernards MidYear (January 1 June 30) Email: YearEnd (July 1 December 31) [email protected] Amendment Phone: 2026622629 Address: 101 CONSTITUTION AVENUE, NW WASHINGTON, DC 20001 USA 5. POLITICAL ACTION COMMITTEE NAMES Honeywell International Political Action Committee 6. CONTRIBUTIONS No Contributions #1. Contribution Type: Contributor Name: Amount: Date: FECA Honeywell International Political Action Committee $1,500.00 01/14/2016 Payee: Honoree: Friends of Sam Johnson Sam Johnson #2. Contribution Type: Contributor Name: Amount: Date: FECA Honeywell International Political Action Committee $2,500.00 01/14/2016 Payee: Honoree: Kay Granger Campaign Fund Kay Granger #3. Contribution Type: Contributor Name: Amount: Date: FECA Honeywell International Political Action Committee $2,000.00 01/14/2016 Payee: Honoree: Paul Cook for Congress Paul Cook https://lda.congress.gov/LC/protected/LCWork/2016/MM/57453DOM.xml?1470093694684 1/75 8/1/2016 LD203 Contribution Report #4. Contribution Type: Contributor Name: Amount: Date: FECA Honeywell International Political Action Committee $1,000.00 01/14/2016 Payee: Honoree: DelBene for Congress Suzan DelBene #5. Contribution Type: Contributor Name: Amount: Date: FECA Honeywell International Political Action Committee $1,000.00 01/14/2016 Payee: Honoree: John Carter for Congress John Carter #6. -

Congressional Directory CALIFORNIA

28 Congressional Directory CALIFORNIA *** TWENTIETH DISTRICT JIM COSTA, Democrat, of Fresno, CA; born in Fresno, April 13, 1952; education: B.A., California State University, Fresno, CA, 1974; professional: Chief Executive Officer Costa Group, 2002–present; employee, Costa Brothers Dairy, 1959–74; Senator California State Sen- ate, 1994–2002; assembly member, California State Assembly, 1978–94; administrative assist- ant, California Assemblyman Richard Lehman, 1976–78; special assistant, Congressman John Krebs, 1975–76; member of the California State Assembly, 1978–94; member of the California State Senate, 1994–2002; private advocate; member: Fact Steering Committee, Fresno County Farm Board; religion: Catholic; committees: Agriculture; Foreign Affairs; Natural Resources; elected to the 109th Congress on November 2, 2004; reelected to each succeeding Congress. Office Listings http://www.house.gov/costa 1314 Longworth House Office Building, Washington, DC 20515 ............................. (202) 225–3341 Chief of Staff.—Scott Nishioki. FAX: 225–9308 Deputy Chief of Staff / Scheduler.—Juan Lopez. 2300 Tulare Street, #315, Fresno, CA 93721 .............................................................. (559) 495–1620 District Director.—Vacant. Counties: FRESNO (part), KERN (part), KINGS. Population (2000), 639,088. ZIP Codes: 93202–04, 93206, 93210, 93212, 93215–16, 93220, 93230, 93232, 93234, 93239, 93241–42, 93245–46, 93249– 50, 93263, 93266, 93280, 93282, 93301, 93305, 93307, 93383, 93387, 93518, 93607–09, 93616, 93620, 93622, 93624– -

2017 Political Contributions (January 1 – June 30)

2017 Political Contributions (January 1 – June 30) Amgen is committed to serving patients by transforming the promise of science and biotechnology into therapies that have the power to restore health or even save lives. Amgen recognizes the importance of sound public policy in achieving this goal, and, accordingly, participates in the political process and supports those candidates, committees, and other organizations who work to advance healthcare innovation and improve patient access. Amgen participates in the political process by making direct corporate contributions as well as contributions through its employee-funded Political Action Committee (“Amgen PAC”). In some states, corporate contributions to candidates for state or local elected offices are permissible, while in other states and at the federal level, political contributions are only made through the Amgen PAC. Under certain circumstances, Amgen may lawfully contribute to other political committees and political organizations, including political party committees, industry PACs, leadership PACs, and Section 527 organizations. Amgen also participates in ballot initiatives and referenda at the state and local level. Amgen is committed to complying with all applicable laws, rules, and regulations that govern such contributions. The list below contains information about political contributions for the first half of 2017 by Amgen and the Amgen PAC. It includes contributions to candidate committees, political party committees, industry PACs, leadership PACs, Section 527 organizations, and state and local ballot initiatives and referenda. These contributions are categorized by state, political party (if applicable), political office (where applicable), recipient, contributor (Amgen Inc. or Amgen PAC) and amount. Office Candidate State Party Office Committee/PAC Name Candidate Name Corp. -

Employees of Northrop Grumman Political Action Committee (ENGPAC) 2017 Contributions

Employees of Northrop Grumman Political Action Committee (ENGPAC) 2017 Contributions Name Candidate Office Total ALABAMA $69,000 American Security PAC Rep. Michael Dennis Rogers (R) Leadership PAC $5,000 Byrne for Congress Rep. Bradley Roberts Byrne (R) Congressional District 01 $5,000 BYRNE PAC Rep. Bradley Roberts Byrne (R) Leadership PAC $5,000 Defend America PAC Sen. Richard Craig Shelby (R) Leadership PAC $5,000 Martha Roby for Congress Rep. Martha Roby (R) Congressional District 02 $10,000 Mike Rogers for Congress Rep. Michael Dennis Rogers (R) Congressional District 03 $6,500 MoBrooksForCongress.Com Rep. Morris Jackson Brooks, Jr. (R) Congressional District 05 $5,000 Reaching for a Brighter America PAC Rep. Robert Brown Aderholt (R) Leadership PAC $2,500 Robert Aderholt for Congress Rep. Robert Brown Aderholt (R) Congressional District 04 $7,500 Strange for Senate Sen. Luther Strange (R) United States Senate $15,000 Terri Sewell for Congress Rep. Terri Andrea Sewell (D) Congressional District 07 $2,500 ALASKA $14,000 Sullivan For US Senate Sen. Daniel Scott Sullivan (R) United States Senate $5,000 Denali Leadership PAC Sen. Lisa Ann Murkowski (R) Leadership PAC $5,000 True North PAC Sen. Daniel Scott Sullivan (R) Leadership PAC $4,000 ARIZONA $29,000 Committee To Re-Elect Trent Franks To Congress Rep. Trent Franks (R) Congressional District 08 $4,500 Country First Political Action Committee Inc. Sen. John Sidney McCain, III (R) Leadership PAC $3,500 (COUNTRY FIRST PAC) Gallego for Arizona Rep. Ruben M. Gallego (D) Congressional District 07 $5,000 McSally for Congress Rep. Martha Elizabeth McSally (R) Congressional District 02 $10,000 Sinema for Arizona Rep. -

August 10, 2021 the Honorable Nancy Pelosi the Honorable Steny

August 10, 2021 The Honorable Nancy Pelosi The Honorable Steny Hoyer Speaker Majority Leader U.S. House of Representatives U.S. House of Representatives Washington, D.C. 20515 Washington, D.C. 20515 Dear Speaker Pelosi and Leader Hoyer, As we advance legislation to rebuild and renew America’s infrastructure, we encourage you to continue your commitment to combating the climate crisis by including critical clean energy, energy efficiency, and clean transportation tax incentives in the upcoming infrastructure package. These incentives will play a critical role in America’s economic recovery, alleviate some of the pollution impacts that have been borne by disadvantaged communities, and help the country build back better and cleaner. The clean energy sector was projected to add 175,000 jobs in 2020 but the COVID-19 pandemic upended the industry and roughly 300,000 clean energy workers were still out of work in the beginning of 2021.1 Clean energy, energy efficiency, and clean transportation tax incentives are an important part of bringing these workers back. It is critical that these policies support strong labor standards and domestic manufacturing. The importance of clean energy tax policy is made even more apparent and urgent with record- high temperatures in the Pacific Northwest, unprecedented drought across the West, and the impacts of tropical storms felt up and down the East Coast. We ask that the infrastructure package prioritize inclusion of a stable, predictable, and long-term tax platform that: Provides long-term extensions and expansions to the Production Tax Credit and Investment Tax Credit to meet President Biden’s goal of a carbon pollution-free power sector by 2035; Extends and modernizes tax incentives for commercial and residential energy efficiency improvements and residential electrification; Extends and modifies incentives for clean transportation options and alternative fuel infrastructure; and Supports domestic clean energy, energy efficiency, and clean transportation manufacturing. -

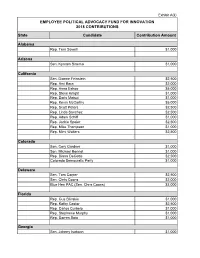

2018 BMS PAC Contributions

Exhibit A(ii) EMPLOYEE POLITICAL ADVOCACY FUND FOR INNOVATION 2018 CONTRIBUTIONS State Candidate Contribution Amount Alabama Rep. Terri Sewell $1,000 Arizona Sen. Kyrsten Sinema $1,000 California Sen. Dianne Feinstein $2,500 Rep. Ami Bera $2,000 Rep. Anna Eshoo $5,000 Rep. Steve Knight $1,000 Rep. Doris Matsui $1,000 Rep. Kevin McCarthy $5,000 Rep. Scott Peters $2,500 Rep. Linda Sanchez $2,500 Rep. Adam Schiff $1,000 Rep. Jackie Speier $2,500 Rep. Mike Thompson $1,000 Rep. Mimi Walters $2,500 Colorado Sen. Cory Gardner $1,000 Sen. Michael Bennet $1,000 Rep. Diana DeGette $2,500 Colorado Democratic Party $1,000 Delaware Sen. Tom Carper $2,500 Sen. Chris Coons $2,000 Blue Hen PAC (Sen. Chris Coons) $3,000 Florida Rep. Gus Bilirakis $1,000 Rep. Kathy Castor $2,500 Rep. Carlos Curbelo $1,000 Rep. Stephanie Murphy $1,000 Rep. Darren Soto $1,000 Georgia Sen. Johnny Isakson $1,000 Sen. David Perdue $2,000 Rep. Buddy Carter $2,500 Iowa Gov. Kim Reynolds $2,000 Sen. Chuck Grassley $2,500 State Sen. Charles Schneider $2,000 State Sen. Tom Shipley $500 Idaho Sen. Mike Crapo $5,000 Illinois Rep. Cheri Bustos $1,000 Rep. Bill Foster $1,000 Rep. Robin Kelly $1,000 Rep. Darin LaHood $1,000 Rep. Pete Roskam $1,000 Rep. Brad Schneider $1,000 Rep. John Shimkus $2,500 Indiana Sen. Mike Braun $1,000 Sen. Joe Donnelly $2,500 Rep. Larry Bucshon $2,500 Rep. Susan Brooks $2,000 Rep. Andre Carson $1,000 Rep. -

The Women Who Lead the San Gabriel Valley Support Mike Eng for State

The women who lead the San Gabriel Valley support Mike Eng for State Senate EL MONTE, CA — There are two candidates for State Senate in our district, a man and a woman. But only Mike Eng is endorsed by California NOW Pac, the California Democratic Party and our Democratic leaders. Why are women uniting for Mike when he is running against a woman? Because Mike Eng is the only candidate with a proven record on the issues we care about most: • Mike fought to strengthen and renew the Violence Against Women Act, and co-authored Senate Joint Resolution 20 to demand the continuation of support for victims and awareness of Domestic Violence. • Mike worked to increase prevention efforts and legal protections for victims of domestic violence, sexual assault and stalking. • Mike has the courage to stand up to Donald Trump and expand access to affordable health care in California. He’s supported by the United Nurses Associations of California, SEIU Nurses 121RN and the California Nurses Association. • Mike — a college teacher and former community college board vice- president — is an effective champion for education and affordable college for all. “Mike Eng has proven that he stands up for school funding, access to healthcare for all, increased childcare and early education, and equality for women.” -Kolieka Seigle, President of California National Organization for Women The women who lead our community unite for Mike Eng for Senate: Congressmember Judy Chu Congressmember Grace Napolitano State Senator Connie Leyva County Supervisor Hilda Solis Congressmember