Performance Audit Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Toyota Gear Shift/Select Cable

INDEX PAGES TOYOTA 1 ~ 53 NISSAN 54 ~ 91 MAZDA 92 ~ 104 HINO 105 ~ 115 ISUZU 116 ~ 137 MITSUBISHI 138 ~ 160 PROTON 161 ~ 164 DAIHATSU 165 ~ 172 SUZUKI 173 ~ 180 HONDA 181 ~ 193 SUBARU 194 ~ 195 HYUNDAI 196 ~ 199 DAEWOO & KIA & SSANGYONG 200 ~ 203 AMERICAN & EUROPEAN VEHICLES 204 ~ 212 MOTORCYCLES 213 ~ 215 KUBOTA,TRACTOR & FORK LIFT 216 ~ 218 OTHERS 219 ~ 221 CABLES FOR SOUTH AFRICA MAKET 222 ~ 229 ADDITIONAL ITEMS 230 TOYOTA OEM NUMBER ICI NUMBER MODEL TOYOTA ACCELERATOR CABLE 35520-12050 CATY123 AE 8# 35520-12072 CATY145 KE70 ATM 81.08- 35520-12110 CATY124 TE 7# 35520-12200 CATY158 35520-12201 CATY158 35520-12240 CATY126 HILUX LN85/106 88-92, AE101, AE92, AT171 35520-12300 CATY148 AE100,101,110 4FC 91.08- 35520-12310 CATY151 COROLLA AE101 4A-FE 91.06-93.05 35520-12370 CATY122 35520-12390 CATY150 COROLLA AE101 4A-FE 93.05- , AE102,111 1991-1995 RHD 35520-12391 CATY150 COROLLA AE101 4A-FE 93.05- , AE102,111 1991-1995 RHD 35520-16090 CATY147 EE101,92.05-95.05,EP82 3F .92.01- 35520-20070 CATY141 CRESSIDA 35520-28011 CATY133 35520-30030 CATY146 MS112,122,132,133 8MX73 84.08- 35520-33010 CATY217 CAMRY SXV10# 2.2L 5S-FE DOHC 16V MPFI 4CYL 4SP AUTO, VCV10, MCV10 ATM 1992-2001 35520-33050 CATY234 AVALON XL,XLS (MCX10) 1996-1999/CAMRY CE,LE,XLE (MCV20) 1997-2001/SOLARA MCV20 1999-2003/LEXUS ES300 (MCV20) 1996-2001 47616-26040 CATY192 62-CATY002 CATY002 HILUX LN50 62-CATY004 CATY004 HILUX 62-CATY026 CATY026 HILUX HIACE Y SERIES LN80/85/106/130 LHD 92-94 3L 78120-35013 CATY156 78120-90506 CATY159 DYNA RB10 '77-79 78150-06020 CATY220 TOYOTA CAMRY -

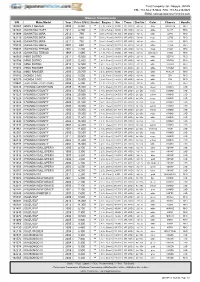

TOYOTA S/N Make,Model Year Price (US$) Grade Engine Km Trans

Trust Company Ltd., Nagoya, JAPAN TEL: +81-52-219-9024 FAX: +81-52-219-9025 EMAIL:[email protected] TOYOTA S/N Make,Model Year Price (US$) Grade Engine Km Trans. Drs/Sts Color Chassis Handle 180781 TOYOTA ALLEX 2002 2,080 ** 1.5 L Petrol 53,000 AT, 2WD 5d / 5s whitepearl NZE121 RHD 181939 TOYOTA ALLEX 2006 3,250 ** 1.5 L Petrol 29,000 AT, 2WD 5d / 5s silver NZE121 RHD 179935 TOYOTA ALLION 2015 18,000 *** 1.5 L Petrol 21,000 AT, 2WD 4d / 5s wine red NZT260 RHD 180777 TOYOTA ALLION 2007 4,990 ** 1.5 L Petrol 56,000 AT, 2WD 4d / 5s silver NZT260 RHD 180874 TOYOTA ALLION 2014 16,000 *** 1.5 L Petrol 26,000 AT, 2WD 5d / 5s silver NZT260 RHD 182577 TOYOTA ALLION 2003 2,350 ** 1.5 L Petrol 88,000 AT, 2WD 4d / 5s white NZT240 RHD 182638 TOYOTA ALLION 2004 2,880 ** 1.5 L Petrol 23,000 AT, 2WD 4d / 5s silver NZT240 RHD 179241 TOYOTA ALPHARD 2015 38,000 *** 2.5 L Petrol 57,000 AT, 4WD 5d / 8s black AGH35 RHD 180621 TOYOTA ALPHARD 2003 2,690 ** 2.4 L Petrol 145,000 AT, 4WD 5d / 8s whitepearl ANH15 RHD 180860 TOYOTA ALPHARD 2004 2,850 ** 2.4 L Petrol 171,000 AT, 4WD 5d / 8s silver ANH15 RHD 182201 TOYOTA ALPHARD 2013 23,000 *** 2.4 L Petrol 61,000 AT, 4WD 5d / 8s white ANH25 RHD 182619 TOYOTA ALPHARD 2007 3,950 ** 2.4 L Petrol 142,000 AT, 4WD 5d / 8s silver ANH15 RHD 180880 TOYOTA ALTEZZA (LEXUS IS) 2002 1,490 ** 2.0 L Petrol 118,000 AT, 2WD 4d / 5s silver GXE10 RHD 181891 TOYOTA ALTEZZA (LEXUS IS) 2000 1,580 ** 2.0 L Petrol 101,000 AT, 2WD 4d / 5s white GXE10 RHD 180857 TOYOTA ALTEZZA GITA 2003 690 ** 2.0 L Petrol 113,000 AT, 2WD 5d / 5s -

Manual Transmission S/N Make,Model Year Price (US$) Grade Engine Km Trans

Trust Company Ltd., Nagoya, JAPAN TEL: +81-52-219-9024 FAX: +81-52-219-9025 EMAIL:[email protected] Manual Transmission S/N Make,Model Year Price (US$) Grade Engine Km Trans. Drs/Sts Color Chassis Handle 180968 BMW 3 SERIES 2008 6,880 ** 2.0 L Petrol 97,000 MT, 2WD 4d / 5s blue WBAVG76 RHD 182342 DAIHATSU HIJET 2012 4,700 ** 0.66 L Petrol 36,000 MT, 4WD 2d / 2s white S211P RHD 181699 DAIHATSU MIRA 2012 790 ** 0.66 L Petrol 151,000 MT, 2WD 3d / 4s white L275V RHD 182115 DAIHATSU MIRA 2008 890 ** 0.66 L Petrol 138,000 MT, 2WD 5d / 4s beige L275S RHD 182449 DAIHATSU MIRA 2011 790 ** 0.66 L Petrol 179,000 MT, 2WD 3d / 4s silver L275V RHD 179832 DAIHATSU MOVE 2007 650 ** 0.66 L Petrol 183,000 MT, 4WD 5d / 4s white L185S RHD 179697 DAIHATSU TERIOS 2001 2,200 ** 1.3 L Petrol 99,000 MT, 4WD 5d / 5s black J102G RHD 182018 DAIHATSU TERIOS 1998 1,690 ** 1.3 L Petrol 97,000 MT, 4WD 5d / 5s white/silver J100G RHD 180569 HINO DUTRO 2011 15,500 ** 4.0 L Diesel 193,000 MT, 2WD 2d / 3s white XZC710 RHD 180756 HINO DUTRO 2007 12,800 ** 4.0 L Diesel 130,000 MT, 2WD 2d / 3s white XZU554 RHD 181123 HINO DUTRO 2010 12,500 ** 4.0 L Diesel 104,000 MT, 2WD 2d / 3s white XZU508 RHD 178382 HINO RANGER 2006 12,500 ** 6.4 L Diesel 202,000 MT, 2WD 2d / 3s white FD7JKW RHD 180544 HINO RANGER 2006 20,700 ** 6.4 L Diesel 56,000 MT, 2WD 2d / 2s white FC7JJW RHD 178582 HONDA CIVIC 2002 5,500 ** 2.0 L Petrol 100,000 MT, 2WD 3d / 4s white EP3 RHD 180275 HONDA CIVIC 2008 10,900 ** 2.0 L Petrol 102,000 MT, 2WD 4d / 4s white FD2 RHD 179841 HONDA INTEGRA (ACURA INTEGRA) -

Acdelco Premium Belt Range

ACDELCO PREMIUM BELT RANGE ACDELCO BELTS ACDelco P/N GM P/N Application Make/Model FORD (Asia & Oceania) Telstar 2.0 / FORD Australia Laser 1.8 / HONDA Integra 1.8 / MAZDA 323 1.8 / MAZDA 323 Astina 1.8 / MAZDA 323 Protege 1.8 / MAZDA 626 2.0 / MAZDA 626 Estate/Wagon 2.0 / MAZDA 4PK920 19376034 Capella 2.0 / MAZDA Familia 1.8 / MAZDA MX6 2.5 / MAZDA Premacy 1.8 / NISSAN Pulsar 2.0 / SUZUKI Alto 1.0 / SUZUKI Cultus 1.0 / TOYOTA Chaser 2.0 / TOYOTA Echo 1.3 / TOYOTA Starlet 1.3 / TOYOTA Supra 3.0 / TOYOTA Yaris 1.3 / TOYOTA Yaris Verso 1.3 FORD (Europe) Fiesta 1.2 / FORD (Europe) Fusion 1.4 / FORD Australia Fiesta 5PK692SF 19375735 1.6 / MAZDA 3 2.0 / MAZDA Axela 2.0 LEXUS ES 300 3.0 / LEXUS RX 300 3.0 / LEXUS RX 330 3.3 / MITSUBISHI Lancer 1.5 / MITSUBISHI Mirage 1.3 / NISSAN 200SX 2.0 / NISSAN 4PK880 19376031 Serena 2.0 / NISSAN Skyline GT-R 2.6 / TOYOTA Avalon 3.0 / TOYOTA Camry 3.0 / TOYOTA Estima 3.0 / TOYOTA Harrier 3.0 / TOYOTA Hiace 2.4 / TOYOTA Kluger 3.3 / TOYOTA Starlet 1.3 HOLDEN Calais 3.6 / HOLDEN Caprice 3.6 / HOLDEN Commodore 3.6 / HOLDEN Crewman 3.6 / HOLDEN Frontera 2.2 / HOLDEN One Tonner 3.6 6PK2045 19376030 / HOLDEN Statesman 3.6 / JEEP Cherokee 3.2 / SUZUKI Grand Vitara 2.4 / SUZUKI SX4 2.0 DAEWOO 1.5i 1.5 / DAEWOO Cielo 1.5 / DAEWOO Lanos 1.5 / HOLDEN Nova 1.4 / SUZUKI Vitara 1.4 / TOYOTA Corolla 1.3 / TOYOTA 5PK970 19376037 Corolla Estate/Wagon 1.6 / TOYOTA Corolla Levin 1.5 / TOYOTA Sprinter 1.6 / TOYOTA Sprinter Carib 1.6 MAZDA 3 2.0 / MAZDA CX3 2.0 / MAZDA CX5 2.0 / MITSUBISHI Galant 6PK965 19376038 2.5 / MITSUBISHI -

Company Profile

Company Profile Find out detailed information regarding Toyota's key personnel and facilities, business activities and corporate entities as well as its sales and production growth around the globe. You can also discover more about the various non-automotive pursuits of Toyota and the museums and plant tours which are open to the public. Overview This section lists basic facts about Toyota in addition to the latest activities relating to latest business results. Find out more Executives Here you will find a list of all of Toyota's top management from the chairman and president down to the managing officers. Find out more Figures See more about the global sales and production figures by region. Find out more Toyota Group A list of companies making up the Toyota Group. Facilities View Toyota's design and R&D bases and production sites all around the globe, as well as the many museums of great knowledge. Find out more Non-automotive Business In addition to automobile production, Toyota is also involved in housing, financial services, e-TOYOTA, Marine, biotechnology and afforestation Toyota From Wikipedia, the free encyclopedia Jump to: navigation, search For other uses, see Toyota (disambiguation). Toyota Motor Corporation Toyota Jidosha Kabushiki-gaisha トヨタ自動車株式会社 Type Public TYO: 7203 Traded as LSE: TYT NYSE: TM Automotive Industry Robotics Financial services Founded August 28, 1937 Founder(s) Kiichiro Toyoda Headquarters Toyota, Aichi, Japan Area served Worldwide Fujio Cho (Chairman) Key people Akio Toyoda (President and CEO) Automobiles Products Financial Services Production output 7,308,039 units (FY2011)[1] Revenue ¥18.583 trillion (2012)[1] [1] Operating income ¥355.62 billion (2012) [1] Profit ¥283.55 billion (2012) [1] Total assets ¥30.650 trillion (2012) [1] Total equity ¥10.550 trillion (2012) Employees 324,747 (2012)[2] Parent Toyota Group Lexus Divisions Scion 522 (Toyota Group) Toyota India Hino Motors, Ltd. -

Bujía - Toyota Yaris P1 | Guía De Sustitución

Cómo cambiar: bujía - Toyota Yaris P1 | Guía de sustitución VIDEO TUTORIAL ¡Importante! Este procedimiento de sustitución puede ser utilizado para: TOYOTA bB I (NCP3_) 1.3 (NCP30_), TOYOTA COROLLA Saloon (_E12_) 1.3 (NZE120_, ZZE120_), TOYOTA IST (NCP6_) 1.3 VVTi, TOYOTA PORTE (_NNP1_) 1.3 VVTi (NNP10), TOYOTA PROBOX / SUCCEED (_P5_) 1.3 VVTi (NCP50_), TOYOTA YARIS (_P13_) 1.3 (NCP130_), TOYOTA YARIS (_P15_) 1.3 (NCP151_), TOYOTA YARIS (_P1_) 1.3 (NCP10_, SCP12_), TOYOTA YARIS (_P9_) 1.3 VVT-i (NCP90_), TOYOTA YARIS / VIOS Saloon (_P15_) 1.3 (NCP151_), TOYOTA YARIS / VIOS Saloon (_P9_) 1.3 (NCP92_), TOYOTA YARIS / VIOS Saloon (_P9_) 1.3 (NCP92_, SCP92_), TOYOTA YARIS VERSO (_P2_) 1.3 (NCP20_, NCP22_) Los pasos a efectuar pueden variar ligeramente dependiendo del diseño del vehículo. WWW.AUTODOC.ES 1–17 SUSTITUCIÓN: BUJÍA - TOYOTA YARIS P1. HERRAMIENTAS QUE PODRÍA NECESITAR: Spray para electrónica. Llave de trinquete Lubricante antigripado de alta Llave dinamométrica temperatura Destornillador Plano Llave de vaso n° 10 Cubreguardabarros Vaso para bujía n° 16 WWW.AUTODOC.ES 2–17 Sustitución: bujía - Toyota Yaris P1. Consejo de AUTODOC: El procedimiento de reemplazo es el mismo para todas las bujías. Todo el trabajo debería ser realizado con el motor parado. SUSTITUCIÓN: BUJÍA - TOYOTA YARIS P1. UTILICE EL SIGUIENTE PROCEDIMIENTO: 1 Abra la capota. 2 Utilice un protector de aletas para evitar daños en la pintura y en las partes de plástico del automóvil. WWW.AUTODOC.ES 3–17 3 Desatornille la sujeción de la cubierta del motor. Use un vaso de impacto del n.º 10. Utilice una llave de trinquete. -

Apr-Jun 2020 (Motor Vehicle Landing Cost).Xlsb

“In accordance with Section 52A of the Fiji Revenue and Customs Service Act and line with the 2016/2017 National Budget Announcement by the Honorable Minister for Economy for Publication of Information in the Public Interest, a list of landed cost of vehicles imported in the country from April to June 2020 is tabulated below.The Fiji Revenue and Customs Service wishes to remind all car dealers to effectively pass on duty concessions to ordinary Fijians. Please be advised that the list of Vehicle Landed Cost will be published on the FRCS Website www.frcs.org.fj on a quarterly basis. Environment and LANDING Import Excise Luxury ECAL,Fiscal Duty, IEX No Commercial Description Chassis No. New or Used CIF Value Climate Adaption Fiscal Duty VAT COST Excluding Mileage Duty Vehicle Levy and LVL Levy VAT 1 2.5TONNE LIFT TRUCK FDA22-1470-00963 New 55,003 2,750 - 5,198 2,750 57,753 0 2 2.5TONNE LIFT TRUCK FGA14-1430-03715 New 56,010 - - 5,041 - 56,010 0 3 2020 MY RANGER DLCAB BSE2 2.2 MNBLMFF80LW077656 New 46,740 2,337 2,337 4,627 4,674 51,414 0 4 2020 MY RANGER DLCAB BSE2 2.2 MNBLMFF80LW077657 New 46,740 2,337 2,337 4,627 4,674 51,414 0 5 2020 MY RANGER DLCAB BSE2 2.2 MNBLMFF80LW081150 New 46,284 2,314 2,314 4,582 4,628 50,913 0 6 2020 MY RANGER DLCAB BSE2 2.2 MNBLMFF80LW081151 New 46,284 2,314 2,314 4,582 4,628 50,913 0 7 2020 MY RANGER DLCAB RDBK 2.0 MPBUMFE60LX272469 New 93,223 4,661 4,661 9,229 9,322 102,546 0 8 2020 MY RANGER DLCAB WTK 3.2 MNBUMFF50LW083584 New 68,884 3,444 3,444 6,820 6,888 75,773 0 9 2020 MY RANGER DLCAB WTK 3.2 MNBUMFF50LW083585 -

Songwe- List of Goods & Vehicles to Be Auctioned 2021

01 SONGWE Malawi Revenue Authority Public Notice A CALL FOR IMPORTERS TO CLEAR OVERSTAYED GOODS AT CUSTOMS AND EXCISE PORTS The Malawi Revenue Authority (MRA) is reminding all importers of motor vehicles and other goods, that pursuant to the Customs and Excise Act, Section 39, the Authority intends to dispose of or sell by public auction the listed vehicles and goods considered to have overstayed at MRA premises. The Authority will dispose of or sell the vehicles and goods if they are not cleared within thirty days (30) from the date of this notice. LIST OF MOTOR VEHICLES EYED FOR AUCTION IN 2021 DATE CHASSIS GOODS LOT No. IT No. DESCRIPTION OF GOODS YEAR RECEIVED INTO OWNER NUMBER CONDITION WAREHOUSE STATION: SONGWE 1 1352 NISSAN DUALIS 21.09.2020 RUNNER UNKNOWN 2 4130 NISSAN JUKE 18.10.2020 RUNNER UNKNOWN 3 3899 MAZDA DEMIO 16.11.2020 RUNNER UNKNOWN 4 7855 MAZDA BONGO 20.10.2020 RUNNER UNKNOWN 5 9054 NISSAN BLUEBIRD SYLPHY 04.07.2019 RUNNER UNKNOWN 6 9366 JAGUAR X-TYPE 31.12.2020 RUNNER UNKNOWN 7 0874 VW GOLF 05.09.2020 RUNNER UNKNOWN 8 8393 NISSAN ELGRAND 31.12.2020 RUNNER UNKNOWN 9 MAZDA PREMACY 2016 NON RUNNER UNKNOWN 10 7172 TOYOTA VITZ 21.01.2020 RUNNER UNKNOWN 11 5591 DIAHATSU MIRA 19.11.2019 RUNNER UNKNOWN 12 1297 SUBARU LEGACY 10.05.2019 RUNNER UNKNOWN 13 TOYOTA CRESITA 2016 NON RUNNER UNKNOWN 14 1827 NISSAN MARCH 01.10.2020 RUNNER UNKNOWN 15 1821 MAZDA AXELA 05.12.2019 RUNNER UNKNOWN 16 8040 HONDA INSIGHT 07.09.2020 RUNNER UNKNOWN 17 4053 HONDA FIT 15.015.2020 RUNNER UNKNOWN 18 9524 TOYOTA VOXY 01.10.2020 RUNNER UNKNOWN 19 -

Gas Vehicle Guide December 2010

Gas Vehicle Guide December 2010 Table of contents 1 Introduction 5 2 Passenger vehicles 9 3 Light transport 117 vehicles 1. Introduction The Gas Vehicle Guide has been developed as part of the ADORE IT project (Adolescence for Renewable Energies in Transport), where the municipality of Östersund co-operates with partners from the Netherlands, Italy, Norway, Estonia and Romania. In Östersund, the goal is to increase the use of eco-friendly vehicles using renewable fuels. The project period is 2008 to 2011. This global guide to gas/CNG vehicles has been developed with a base in the ongoing establishment of biogas as a vehicle fuel, together with our ambition to help establish a rapid market development in our region and on a national level. The presentation of an unbiased and comprehensive information on the availability of gas vehicles is an important component in this work. The guide gives an overview to the gas vehicles available on the global market for the model year 2011. Here you are able to find vehicle prices, technical data such as range on CNG, safety information, links to further reading, official contact information and much more. This guide can work as a reference for municipalities, private and public institutions and individuals who are interested in acquiring gas vehicles, or who simply want to be informed about of the availability. This is the first edition of the guide published in English. We have never seen such an extensive guide to gas vehicles as this, nevertheless it is certainly not complete. We value all contributions on mistakes and missing data/models in the guide. -

[email protected] , [email protected] Mob: +0086 18857742221 TEL:+0086 577 65353530 FAX:+0086 577 65351121 TNF No

WENZHOU TINAFOR AUTOMOBILE BEARING STOCK CO.,LTD www.tinafor.com Wechat ID: TNF_Tinafor Email: [email protected] , [email protected] Mob: +0086 18857742221 TEL:+0086 577 65353530 FAX:+0086 577 65351121 TNF No. Photo OE car model Our No. Toyota Corolla 7AF 1.8 13505-15050 Toyota COROLLA Compact (_E10_) 92/07 - 97/04 7012 13505-15060 Toyota CARINA E Saloon (_T19_) 93/01 - 97/09 13505-02030 Toyota CARINA E (_T19_) 1.6 93/12 - 97/09 Toyota AVENSIS (_T22_) 1.6 97/09 - 00/10 62TB0813B01 Toyota 3L 13505-54021 Toyota LAND CRUISER 85/10 - 90/05 7016 Toyota 4 RUNNER 2.4TD 89/08 - 95/11 13505-54020 Toyota HIACE III Wagon 2.4D 89/08 - 95/08 T41181 Toyota HIACE IV Bus (LH1_) 2.4 D 95/08 - 06/08 13505-16020 13505-16021 Toyota COROLLA Compact (_E9_) 87/08 - 92/04 7028 13505-02020 Toyota COROLLA Coupe (AE86) 83/08 - 87/07 13505-16011 Toyota MR 2 I (AW1_) 1.6 16V (AW11) 84/11 - 90/06 13505-16010 57TB3705B01 13505-74011 Toyota RAV 4 I (SXA1_) 2.0 4WD 94/06 - 00/06 7039 13505-74010 Toyota CAMRY (_CV1_, _XV1_, _V1_) 2.2 93/02 - 95/04 13505-63011 Toyota CAMRY (_V2_) 2.0 (SV21_, SV25_) 86/11 - 91/05 13505-63010 62TB0520B01 13505-64020 Toyota COROLLA Compact (_E10_) 92/07 - 97/04 7042 13505-64010 Toyota COROLLA (_E8_) 1.8 D 83/06 - 88/05 13505-64022 Toyota COROLLA (_E9_) 1.8 D 87/07 - 93/06 13505-64012 Toyota Starlet 2E 1.3 50TB0101 Toyota COROLLA Compact (_E10_) 92/07 - 95/05 7064 13503-10011 Toyota COROLLA (_E8_) 1.3 83/08 - 87/04 13503-10021 Toyota COROLLA (_E9_) 1.3 87/08 - 92/12 Toyota COROLLA (_E11_) 1.3 97/05 - 01/10 Toyota Starlet 2E 1.3 13505-11010 -

Product Bulletin CTY12035 - Air Filter

Product Bulletin CTY12035 - Air Filter Vehicles DAIHATSU, SUBARU, TOYOTA, Technical Info Height (mm) 49 Length (mm) 250 Width (mm) 120 Cross References 1A First Automotive A60719 ACDELCO PC2241E ALCO MD-9592 AMC TA-1678 ASHIKA 20-02-286 BLUE PRINT ADT32262 BORG & BECK BFA2291 BOSCH 1457433972 CHAMPION CAF100811P CLEAN MA1315 COOPERS AG1436 COOPERSFIA PA7357 CROSLAND 8236 DENCKERMANN A140174 FIAAM PA7357 FIBA FA-207 FIBA FA207 FILTRON AP142/2 FRAM CA9295 HENGST E641L HERTH+BUSS J1322077 JAKOPARTS HOFFER 16016 JAPANPARTS FA-286S JAPANPARTS JFA286 JAPKO 20286 KAMOKA F230001 KAVO TA1678 KNECHT LX 1002 MAHLE LX1002 MANN C2513 Notes: Manufacturers details are for guidance only. For pricing enquiries please contact our sales team on 01582 578 888 Comline Auto Parts Limited Unit B1, Luton Enterprise Park, Sundon Road, Luton, Bedfordshire LU3 3GU Tel: 01582 578 888 International Tel: +44 1582 578 888 Fax: 01582 578 889 International Fax: +44 1582 578 889 Email: [email protected] Web: www.comline.uk.com Product Bulletin CTY12035 - Air Filter Cross References KNECHT LX 1002 MAHLE LX1002 MANN C2513 MASTER-SPORT 2513-LF-PCS-MS MEAT&DORIA 16016 MECAFILTER ELP3925 MEYLE 30-12 321 0015 MISFAT P176 MOTAQUIP VFA954 MULLERFILT PA719 NIPPARTS J1322077 PURFLUX A1107 QH QFA0672 SCT SB 2351 SOFIMA S 9102 A SOLID-AUTO T101054 TECNECO AR2019PM-J TECNOCAR A2019 TOYOTA 17801-0Y010 TOYOTA 17801-21030 TRUPARTS FAP1048 UFI 30.176.00 UNION A133 VAICO V70-0215 WIX WA6665 Notes: Manufacturers details are for guidance only. For pricing enquiries please contact our -

January to March 2020 Landing Cost

“In accordance with Section 52A of the Fiji Revenue & Customs Service Act and line with the 2016/2017 National Budget Announcement by the Honorable Minister for Economy for Publication of Information in the Public Interest, a list of landed cost of vehicles imported in the country from January to March 2020 is tabulated below. Environment and ECAL,Fiscal Import Excise Luxury No Commercial Description Chassis No. New or Used CIF Value Climate Adaption Fiscal Duty VAT Duty, IEX and LANDING COST Mileage Duty Vehicle Levy Levy LVL 1 BMW X7 X DIVE M-SPORT WBACW220XO9B14247 New 208,229 20,823 66,633 10,411 7,500 25,675 105,368 339,271 0000 2 BMW X7 X DIVE M-SPORT WBACW220509B69401 New 211,166 21,117 67,573 10,558 7,500 26,037 106,748 343,951 0000 3 CHEVROLET CAPTIVA MK3HAAGA0LJ001880 New 37,113 3,711 5,567 1,856 4,008 11,134 52,255 5 4 CHEVROLET CAPTIVA MK3HAAGA1LJ001984 New 46,803 4,680 7,020 2,340 5,055 14,041 65,898 5 5 CHEVROLET CAPTIVA MK3HAAGA2LJ001881 New 37,113 3,711 5,567 1,856 4,008 11,134 52,255 5 6 CHEVROLET CAPTIVA MK3HAAGA2LJ002075 New 42,859 4,286 6,429 2,143 4,629 12,858 60,345 5 7 CHEVROLET CAPTIVA MK3HAAGA2LJ003775 New 43,193 4,319 6,479 2,160 4,665 12,958 60,815 5 8 CHEVROLET CAPTIVA MK3HAAGA2LJ004635 New 46,803 4,680 7,020 2,340 5,055 14,041 65,898 5 9 CHEVROLET CAPTIVA MK3HAAGA3LJ001985 New 46,803 4,680 7,020 2,340 5,055 14,041 65,898 5 10 CHEVROLET CAPTIVA MK3HAAGA3LJ003767 New 43,193 4,319 6,479 2,160 4,665 12,958 60,815 5 11 CHEVROLET CAPTIVA MK3HAAGA4LJ002076 New 42,859 4,286 6,429 2,143 4,629 12,858 60,345 5 12 CHEVROLET