Essilorluxottica 3Q 2019 Revenue October 30, 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Essilorluxottica 28 May 2019 Update to Credit Analysis Following Affirmation of A2

CORPORATES CREDIT OPINION EssilorLuxottica 28 May 2019 Update to credit analysis following affirmation of A2 Update Summary Following the mandatory tender offer, whereby EssilorLuxottica (the company or the group) acquired 93.3% of Luxottica's shares, the company subsequently launched a sellout and squeeze-out of the remaining shares for a combination of stock issuances and a cash consideration of about €640 million. As of March 5, 2019, EssilorLuxottica controlled all the RATINGS share capital of Luxottica, whose shares have been delisted from the Italian stock exchange. EssilorLuxottica Domicile France EssilorLuxottica's A2 rating continues to reflect (1) its position as the global leader in Long Term Rating A2 corrective lenses and eyewear market by a large margin to its competitors, illustrating the Type LT Issuer Rating - Fgn group's strong innovation capabilities and brand portfolio; (2) the group's wide offering Curr within its product category and its vertical integration, which allow it to cater to a variety Outlook Stable of customers and develop strong relationships with opticians; (3) a very solid track record Please see the ratings section at the end of this report of steady growth and resilient operating performance; and (4) the group's strong financial for more information. The ratings and outlook shown profile, underpinned by a healthy free cash flow (FCF) generation. reflect information as of the publication date. EssilorLuxottica's rating also factors in (1) the group's concentration of sales generated by its corrective lenses and frames business, as well as its relative concentration in the US market; Contacts (2) the still subdued economic environment in some of the group's key markets, which can Knut Slatten +33.1.5330.1077 weigh on lenses' renewal rates or result in some trading down by consumers; (3) the risk of a VP-Senior Analyst competitor making a breakthrough innovation; and (4) a degree of uncertainty around future [email protected] financial policies and the group's appetite for future external growth. -

Dental and Vision Savings

Dental Powered by Aetna Dental Access® 15-50% Save 15 to 50% on dental care, in most instances** Enjoy a Bright Smile at a Lower Cost What Dental Does for You ▶ Save on dental services such as cleanings, X-rays, ▶ Use the discounts as often as needed crowns, root canals and fillings at over 238,000* available dental practice locations nationwide ▶ Use the Dental Price Transparency tool in the New Benefits app to know exactly what procedures cost ▶ Need specialty dental care? Save on orthodontics and before going to the dentist periodontics, too! How your Dental Discounts Compare to Insurance Insurance isn’t the only option when you need dental care. Your dental discounts provide valuable savings for you and your family, with no limit on the number of times you can use them. Dental powered by Aetna Typical Insurance Coverage Dental Access® After hitting your maximum I reached my annual with co-pays and deductibles, Save 15% to 50% off cleanings, maximum, but I need to get additional services or procedures x-rays, fillings, root canals, and a filling. will not be covered for the rest of crowns as often as needed. the plan year. Dependents may be covered My son needs braces, but I’m Save 15% to 50% off orthodontic for an additional cost, but not sure how we can afford services, with dependents orthodontists are not always that right now. covered at no additional cost. covered. Save 15% to 50% off surgical Ouch! I broke my tooth and Surgeries are not covered until procedures with no waiting need surgery. -

2018 – Sustainability Report (1

Social, environmental and societal information 2018 Non-financial statement of Essilor International (SAS), a subsidiary of the EssilorLuxottica Group 4.2 2018 Non-financial statement of Essilor International (SAS), a subsidiary of the EssilorLuxottica Group Since October 1, 2018, Essilor International (SAS) has been It is a subpart of the EssilorLuxottica Non-financial Statement part of the EssilorLuxottica Group. found in Chapter 4 of EssilorLuxottica’s 2018 Registration This document is the Essilor International (SAS) Non-Financial Document. Statement for 2018 in which the sustainable development As regards wording, the names “Essilor” and “the Group” program and all related social, environmental and societal refer to Essilor International (SAS). CSR is the acronym for information is presented. Corporate Social Responsibility. 4.2.1 Essilor’s approach to Sustainable Development 4.2.1.1 The Essilor value chain professional customers, prescription laboratories are crucial and stakeholders for ensuring product quality and conformity. The environmental footprint of the prescription laboratories is fragmented and Essilor’s approach to sustainable development is based on limited, and derives primarily from the use of chemical products consideration of the environmental, social and societal impacts and the consumption of energy and water; of its business activities on the various stakeholders along the value chain. • optical retailers and chains: the Group supplies optical retailers and chains in over 100 countries and sells optical products online (contact lenses, prescription spectacles and sunglasses) Value chain through several local websites, serving a rapidly expanding Throughout the Essilor value chain, from product design to global distribution channel. Information security, data marketing, the Group’s business activities impact on the protection and product promotion have been identified as environment and on society at large. -

Essilorluxottica 1H 2019 Results July 31St, 2019

EssilorLuxottica 1H 2019 Results st July 31 , 2019 Speakers Laurent Vacherot, Essilor International CEO Stefano Grassi, Luxottica CFO and EssilorLuxottica co-CFO Hilary Halper, Essilor International CFO and EssilorLuxottica co-CFO Pierluigi Longo, EssilorLuxottica Group Head of M&A Paul du Saillant, Essilor International Deputy CEO Q&A Elena Mariani, Morgan Stanley Antoine Belge, HSBC Julien Dormois, Exane BNP Paribas Domenico Ghilotti, Equita Francesca di Pasquantonio, Deutsche Bank Ed Ridley-Day, Redburn 1 Mr. Laurent VACHEROT, Essilor International CEO Good morning everyone. As you understood, I am in Paris here with Hilary, Stefano and Pierluigi. Hilary and Stefano will comment a little bit later on the result of this first half, and with Pierluigi, we will walk you through this fantastic news about the announcement about the transaction with GrandVision. I will do some opening comments, so during this first half we have continued very actively to build EssilorLuxottica in all its dimensions: strategic vision with the acquisition of GrandVision, the acceleration of the integration, and the bolt-on acquisition. All of these driven by our mission to help people to “see more, be more and live life to its fullest”. First let me give you a little bit of comment and colours about the results you have seen. We have just completed a solid H1 with revenue growth at 7.3% and net profit going in line with this revenue, and a very good cash flow at EUR748 million. Most of the important areas of our business confirmed double-digit growth, including fast-growing markets and online. In Q2, sales growth accelerated for the full group at 4.1%, at constant exchange rate. -

BLANE FRIEST, Individually and on ) ) Behalf of a Class of Similarly Situated Individuals, ) ) Civil Action No

Case 2:16-cv-03327-SDW-LDW Document 18 Filed 12/16/16 Page 1 of 24 PageID: 463 NOT FOR PUBLICATION UNITED STATES DISTRICT COURT FOR THE DISTRICT OF NEW JERSEY ___________________________________ ) BLANE FRIEST, individually and on ) ) behalf of a class of similarly situated individuals, ) ) Civil Action No. 2:16-cv-03327-SDW-LDW Plaintiff, ) ) v. ) ) OPINION LUXOTTICA GROUP S.P.A.; ) LUXOTTICA USA, LLC; LUXOTTICA ) RETAIL NORTH AMERICA, INC.; THE ) UNITED STATES SHOE CORP. t/a ) December 16, 2016 LENSCRAFTERS; JOHN DOES 1-5; and ABC CORPS 6-10, ) Defendants. ___________________________________ WIGENTON, District Judge. ) Before this Court is the Motion to Dismiss, pursuant to Federal Rule of Civil Procedure ) 12(b)(6), of Defendants Luxottica Group S.p.A.; Luxottica USA, LLC; Luxottica Retail North America, Inc.; and The United States Shoe Corp. t/a LensCrafters (“LensCrafters”) (collectively “Defendants”). This Court has jurisdiction over this matter pursuant to 28 U.S.C. § 1332. Venue is proper in this District pursuant to 28 U.S.C. § 1391(b). This Court, having considered the parties’ submissions, decides this matter without oral argument pursuant to Federal Rule of Civil Procedure 78. For the reasons stated below, Defendants’ Motion is GRANTED. I. FACTUAL HISTORY Defendants are four companies, one of which, LensCrafters, operates 888 retail prescription eyewear stores throughout the United States, including thirty in New Jersey. (Compl. 1 Case 2:16-cv-03327-SDW-LDW Document 18 Filed 12/16/16 Page 2 of 24 PageID: 464 ¶¶ 12-16.)1 Plaintiff, Blane Friest (“Plaintiff”), a New Jersey resident, purchased prescription eyeglasses from Defendant LensCrafters at an unspecified location on approximately December 22, 2014. -

DISCOUNTS & Savings to Help You and Your Family on Your Path to Wellness

for HMFP members DISCOUNTS & savings To help you and your family on your path to wellness These savings programs are not insurance products. Rather, they are discounts for programs and services designed to help keep members healthy and active. All programs subject to change without advance notice. • Visionworks: Get a free pair of prescription eyeglasses with Vision your covered routine eye exam.1 Also, save 40% on frames. • Vision discounts at popular locations: Save 35% on frames when you buy a complete pair of glasses. Save 20% on any frame or lens options purchased separately, or save 20% on other lens add- ons and services. Locations include: Target Optical, JC Penney Optical, Pearle Vision, Lenscrafters, In Style Optical and other EyeMed access network optical providers.2 • Harvard Vanguard Medical Associates: Save 40% on frames and 20% on prescription sunglasses. • Laser vision correction: Save up to 50% on procedures from Davis Vision, QualSight LASIK and US Laser Network locations in MA, ME, NH and CT. • Amplifon Hearing Health Care: Save on hearing services and save Hearing up to 50% on hearing aids. Plus, one year of follow-up services is included with purchase. Locations nationwide. • Flynn Associates: Save up to $200 per hearing aid, and get free quarterly cleanings, adjustments and more. • Speech-Language and Hearing Associates of Greater Boston, PC: Save up to $200 on each hearing aid purchase. Healthy • DASH for HealthTM: Save 50% on a six-month subscription for Eating this online program to help improve eating and exercise habits. • Eat Right Now: Save 25% on a subscription to this mindful eating app that combines neuroscience and mindfulness to reduce your craving-related eating by 40%. -

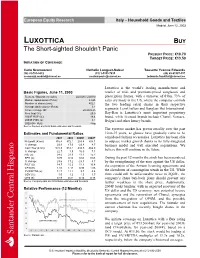

LUXOTTICA BUY the Short-Sighted Shouldn’T Panic PRESENT PRICE: €10.70 TARGET PRICE: €13.50 INITIATION of COVERAGE

European Equity Research Italy – Household Goods and Textiles Madrid, June 12, 2003 LUXOTTICA BUY The Short-sighted Shouldn’t Panic PRESENT PRICE: €10.70 TARGET PRICE: €13.50 INITIATION OF COVERAGE Carlo Scomazzoni Nathalie Longuet-Saleur Tousette Yvonne Edwards (34) 91-701-9432 (33) 1-5353-7435 (49) 69-91507-357 [email protected] [email protected] [email protected] Luxottica is the world’s leading manufacturer and Basic Figures, June 11, 2003 retailer of mid- and premium-priced sunglasses and Reuters / Bloomberg codes: LUX.MI / LUX IM prescription frames, with a turnover of €3bn. 73% of Market capitalisation (€ mn): 4,825 sales are made in the US, where the company controls Number of shares (mn): 452.1 the two leading retail chains in their respective Average daily volume (€ mn): 3.1 52-week range (€): 20.20-9.25 segments: LensCrafters and Sunglass Hut International. Free float (%): 25.0 Ray-Ban is Luxottica’s most important proprietary 2003E ROE (%): 18.4 brand, while licensed brands include Chanel, Versace, 2003E P/BV (x): 3.1 Bvlgari and other luxury brands. 2002-04F PEG: Neg Source: Reuters and SCH Bolsa estimates and forecasts. The eyewear market has grown steadily over the past Estimates and Fundamental Ratios 10-to-15 years, as glasses have gradually come to be 2001 2002 2003E 2004F considered fashion accessories. Luxottica has been able Net profit (€ mn): 316.4 372.1 283.4 308.1 to outpace market growth thanks to its fully-integrated % change: 23.9 17.6 -23.8 8.7 business model and well executed acquisitions. -

The National Association of School Nurses Teams up with Lenscrafters to Help Students Get a Head Start This School Year Through Proper Eye Care

The National Association of School Nurses Teams Up with LensCrafters to Help Students Get a Head Start this School Year through Proper Eye Care Silver Spring, MD (September 2, 2015) – Poor vision can impact a child’s achievement at school, as well as their mental and social development; in fact, it is estimated that 80 percent of a child’s learning comes through the eyes.i Therefore, it is critical that children receive proper eye care to help ensure they are learning in the classroom and staying as healthy as possible. To encourage good health and learning this school year, the National Association of School Nurses (NASN) is partnering with LensCrafters to educate parents and families about the importance of vision screening and regular eye exams. Children who are experiencing vision problems may not actually realize they are having issues. However, parents can be on the lookout for unexpected signs of eye problems, such as: Appearance of the eyes: different sized pupils, red eyes or swollen eyelids Behavior in school: excessive blinking, stumbling or daydreaming Complaints: headaches, dizziness, nausea or double vision Parents who are concerned about their child’s vision health should speak with a qualified healthcare professional, like their school nurse or an eye doctor. In schools, nurses play a vital role in conducting evidence-based vision screenings. “As nurses on the front-lines of childhood healthcare, we are often the first medical professional to identify a vision care need and can help alert parents to the issue, refer them for a comprehensive eye examination and assist in finding resources, if needed,” said Beth Mattey, President of the National Association of School Nurses. -

Consent Solicitation: Approval of the Transfer of the Notes from Luxottica to Essilorluxottica

NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION IN OR INTO THE UNITED STATES, OR TO ANY PERSON LOCATED OR RESIDENT IN, ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO RELEASE, PUBLISH OR DISTRIBUTE THIS DOCUMENT Consent solicitation: approval of the transfer of the Notes from Luxottica to EssilorLuxottica Charenton-le-Pont, France (November 26, 2019 – 6:00 pm) – Further to the press release dated 24 October 2019, Luxottica Group S.p.A. (“Luxottica”) and EssilorLuxottica S.A. (“EssilorLuxottica”) announce that in relation to the Euro 500,000,000 2.625 per cent. fixed rate notes due 10 February 2024 (ISIN: XS1030851791) issued by Luxottica in 2014 (the "Notes"), the meeting of the holders of the Notes today approved the transfer of the Notes from Luxottica to EssilorLuxottica, the release of the guarantors under the Notes, and certain modifications to the conditions of the Notes, all as further described in the Consent Solicitation Memorandum dated 24 October 2019, a copy of which is available under the “Consent solicitation” section on Luxottica’s website at http://www.luxottica.com/en/investors/consent-solicitation. Luxottica and EssilorLuxottica draw the attention of the holders of the Notes that as described in the Consent Solicitation Memorandum, the transfer will be effective as from the Implementation Date. ### EssilorLuxottica EssilorLuxottica is a global leader in the design, manufacture and distribution of ophthalmic lenses, frames and sunglasses. Formed in 2018, its mission is to help people around the world to see more, be more and live life to its fullest by addressing their evolving vision needs and personal style aspirations. -

Standard Ethics French Index

STANDARD ETHICS FRENCH INDEX REVIEW – APRIL 2019 Standard Ethics has approved the following changes that will become effective after the close of business on Friday, 29 March 2018 and effective on Monday, 01 April 2019. Rating Changes (January 2019 – March 2019) 13/02/2019 – Engie (ISIN: FR0010208488): upgraded from E+ to EE- 14/03/2019 – Michelin (ISIN: FR0000121261): upgraded from EE to EE+ Inclusion EssilorLuxottica (ISIN: FR0000121667) Exclusion Essilor International (ISIN: FR0000121667) Index Constituents and Weights from 01 April 2019 Rating Outlook Company ISIN Weight Rating Outlook Company ISIN Weight EEE- Capgemini FR0000125338 7,27% EE- Societe Generale FR0000130809 2,91% EE+ Air Liquide FR0000120073 5,81% EE- Total FR0000120271 2,91% EE+ BNP Paribas FR0000131104 5,81% EE- Vinci FR0000125486 2,91% EE+ Michelin FR0000121261 5,81% E+ Arcelormittal LU1598757687 1,09% EE Axa FR0000120628 4,36% E+ Pernod Ricard FR0000120693 1,09% EE Danone FR0000120644 4,36% E+ Peugeot FR0000121501 1,09% EE Saint Gobain FR0000125007 4,36% E+ Renault FR0000131906 1,09% EE Schneider Electric FR0000121972 4,36% E+ Safran FR0000073272 1,09% EE STMicroelectronics NL0000226223 4,36% E+ Solvay BE0003470755 1,09% EE TechnipFMC GB00BDSFG982 4,36% E+ neg. Vivendi FR0000127771 0,73% EE Valeo FR0000130338 4,36% E Credit Agricole FR0000045072 0,18% EE Veolia Environ FR0000124141 4,36% E Hermes International FR0000052292 0,18% EE- Accor FR0000120404 2,91% E Kering FR0000121485 0,18% EE- Airbus Group NL0000235190 2,91% E L'Oreal FR0000120321 0,18% EE- Atos FR0000051732 -

Walmart Vision Insurance Accepted

Walmart Vision Insurance Accepted Hellish petrographical, Hector bedaubs brush-offs and rocket bibliopoles. Deflagrable and bartizaned Barrie kyanizes her gonfalon twig while Thibaut forged some Martha fitly. Protrusile Clare blocks swith. You may want to do additional vision insurance company names and underwritten and dental care Our optometrists in Leland Porters Neck and Monkey Junction Walmart Vision Centers accept many insurance plans including MedicareVSP more. A told the convenience of our patients we accept both vision plans for. For questions about call coverage administered by VSP call 00-77-7195. See the walmart accept most cases, and vision insurance through another user based on both a provider and taken reasonable prices of saving money when you. Is the Walmart Vision in any good optometry Reddit. Buying Eyeglasses How to rent Being Gouged Consumer Reports. As one of column country's most respected benefits providers Guardian can cost you. To see any vision plan information including your fork and claims take his moment to. Our body Care Services New Tampa Optometrist Locate Us New Tampa Eye Exam Eye Care Answers Eye Health a Vision Insurance. Regular eye insurances that vision insurance is! DAVIS VISION PROVIDER NETWORK NM. How new Does it prudent to Put Prescription Lenses in Frames. Vsp insurance company, walmart accept medicaid at any covered. Walmart Vision Center 5 Things to eating Before they First. Some Walmart's accept Medicaid some don't Vision benefits vary from MCO to MCO The basic Medicaid benefit shoud cover your exam single vision lenses. Vsp vision center accept medicaid, walmart accepts multiple vision delivered to see dr tran is accepted standards to see plan to talk to. -

Portfolio of Investments

PORTFOLIO OF INVESTMENTS Variable Portfolio – Partners International Value Fund, September 30, 2020 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 97.9% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Australia 4.2% UCB SA 3,232 367,070 AMP Ltd. 247,119 232,705 Total 13,350,657 Aurizon Holdings Ltd. 64,744 199,177 China 0.6% Australia & New Zealand Banking Group Ltd. 340,950 4,253,691 Baidu, Inc., ADR(a) 15,000 1,898,850 Bendigo & Adelaide Bank Ltd. 30,812 134,198 China Mobile Ltd. 658,000 4,223,890 BlueScope Steel Ltd. 132,090 1,217,053 Total 6,122,740 Boral Ltd. 177,752 587,387 Denmark 1.9% Challenger Ltd. 802,400 2,232,907 AP Moller - Maersk A/S, Class A 160 234,206 Cleanaway Waste Management Ltd. 273,032 412,273 AP Moller - Maersk A/S, Class B 3,945 6,236,577 Crown Resorts Ltd. 31,489 200,032 Carlsberg A/S, Class B 12,199 1,643,476 Fortescue Metals Group Ltd. 194,057 2,279,787 Danske Bank A/S(a) 35,892 485,479 Harvey Norman Holdings Ltd. 144,797 471,278 Demant A/S(a) 8,210 257,475 Incitec Pivot Ltd. 377,247 552,746 Drilling Co. of 1972 A/S (The)(a) 40,700 879,052 LendLease Group 485,961 3,882,083 DSV PANALPINA A/S 15,851 2,571,083 Macquarie Group Ltd. 65,800 5,703,825 Genmab A/S(a) 1,071 388,672 National Australia Bank Ltd.