Bank of Melbourne Customer Complaint

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Investor Relations Presentation

Investor Relations Presentation 1 DISCLAIMER Disclaimer: Commercial in Confidence. Not to be shared or reproduced without the authority of Cashwerkz Limited (ACN: 010 653 862). Cashwerkz Group I Cashwerkz Limited ABN 42 010 653 862 AFSL 260033 | Cashwerkz Technologies Pty Ltd ABN 70 164 806 357 AFSL 459645 | RIM Securities Ltd ABN 86 111 273 048 AFSL 283119 | Trustees Australia Limited ABN 63 010 579 058 AFSL 260038. This Presentation contains general information only and is, or is based upon, information that has been released to ASX. This document is not an invitation, offer or recommendation (expressed or implied) to apply for or purchase or to take any other action in respect of securities and is not a prospectus, product disclosure statement or disclosure document for the purposes of the Corporations Act 2001 (Cth) and has not been lodged with ASIC. Investment Risk An investment in Cashwerkz Limited (‘CWZ’ or ‘Group’), is subject to known and unknown risks both specific to CWZ and of a general nature, some of which are beyond the control of the Group. Such risks either may individually or in combination adversely affect the future operating and financial performance of CWZ, its investment return and value of its securities. There can be no guarantee, and the directors and management give no assurances, (notwithstanding that they will use their conscientious best endeavours), that CWZ will achieve its stated objectives or that any forward-looking statement or forecast will eventuate. Forward-Looking Statements This Presentation contains certain statements that may constitute forward-looking statements or information (“forward-looking statements”), including statements regarding the use of proceeds of any funds available to the Group. -

Stepping Forward in Private Credit When Others Step Back Introduction

Current Key Investment Themes JANUARY 2021 THOUGHT LEADERSHIP: STEPPING FORWARD IN PRIVATE CREDIT WHEN OTHERS STEP BACK INTRODUCTION One of the reasons the COVID-19 pandemic hit In this article we review the potential for Australia’s developed economies so hard was that it struck superannuation funds to provide credit to support the parts of economies that until that point had the nation’s SMEs, mid-market and large remained resilient, notwithstanding the geopolitical corporates, real estate developments and other turmoil of Brexit and the US/China trade tensions borrowers, while earning attractive risk adjusted of 2018. The part we are referring to is of course, returns for their members – many of whom are in the consumer. turn the employees or owners of these borrowers. The consumer accounted for 54% of GDP in Australia’s superannuation system is the fourth Australia in 2019, and 68% in the US1, and can be largest pension asset pool globally, with US$1.9 likened to the heart of many developed trillion (A$2.7 trillion) in assets at the end of 2019, economies. The consumer’s resilience changed representing just shy of 4% of OECD pension dramatically with the outbreak of COVID-19 with assets2 - more than the Netherlands, Japan and the lockdowns and travel restrictions decimating Switzerland. consumers' ability to spend. Spending by Australia’s superannuation funds have a well- consumers is also intertwined with the financial known home bias in equity exposure, with the health of their employers, be they small and largest of Australia’s balanced funds holding medium enterprises (SMEs) or mid and large approximately half of their equity assets in corporates. -

Fees and Charges

Fees and Charges PART 2 – SUPPLEMENTARY PRODUCT DISCLOSURE STATEMENT BANKVIC QANTAS VISA CREDIT CARD September 2020 This Fees and Charges brochure is required to be given by us to members when issuing a financial product to them. It contains details that might reasonably be expected to have a material influence on the decision of a customer as to whether to acquire product. This fees and charges table details those transactions for which a fee or charge is payable when using the BankVic Qantas Visa credit card by you. This also forms part of the Visa credit card Terms and Conditions of Use. This Fees and Charges brochure is current as at 01 September 2020. BANKVIC QANTAS VISA CREDIT CARD ACCOUNT FEES Annual fee Nil Late payment - debited on or after the day when an amount that is $9.00 due for payment is not paid on or before its due date. Card issued in normal course of business Nil Disputed transactions voucher retrieval - fee not charged if transaction $25.00 per transaction found to be merchant error BANKVIC QANTAS REWARDS PROGRAM BankVic Qantas Rewards program Nil TRANSACTIONAL Visa international transaction currency conversion fee 2.00% of the AUD transaction amount1 Visa Cash Advance includes: over the counter (domestic & international) $1.80 per transaction Westpac, St George, Bank SA or Bank of Melbourne ATM withdrawal2 $1.80 per transaction LOST/STOLEN CARDS Replacement in Australia $10.00 Emergency replacement overseas $0 Emergency cash overseas $0 AVOIDING CREDIT CARD FEES To avoid fees ensure that BankVic has received your total payment by the due date as outlined below. -

Australia's Best Banking Methodology Report

Mozo Experts Choice Awards Australia’s Best Banking 2021 This report covers Mozo Experts Choice Australia’s Best Banking Awards for 2021. These awards recognise financial product providers who consistently provide great value across a range of different retail banking products. Throughout the past 12 months, we’ve announced awards for the best value products in home loans, personal loans, bank accounts, savings and term deposit accounts, credit cards, kids’ accounts. In each area we identified the most important features of each product, grouped each product into like-for-like comparisons, and then calculated which are better value than most. The Mozo Experts Choice Australia's Best Banking awards take into account all of the analysis we've done in that period. We look at which banking providers were most successful in taking home Mozo Experts Choice Awards in each of the product areas. But we also assess how well their products ranked against everyone else, even where they didn't necessarily win an award, to ensure that we recognise banking providers who are providing consistent value as well as areas of exceptional value. Product providers don’t pay to be in the running and we don’t play favourites. Our judges base their decision on hard-nosed calculations of value to the consumer, using Mozo’s extensive product database and research capacity. When you see a banking provider proudly displaying a Mozo Experts Choice Awards badge, you know that they are a leader in their field and are worthy of being on your banking shortlist. 1 Mozo Experts Choice Awards Australia’s Best Banking 2021 Australia’s Best Bank Australia’s Best Online Bank Australia's Best Large Mutual Bank Australia's Best Small Mutual Bank Australia’s Best Credit Union Australia’s Best Major Bank 2 About the winners ING has continued to offer Australians a leading range of competitively priced home and personal loans, credit cards and deposits, earning its place as Australia's Best Bank for the third year in a row. -

The World's Most Active Banking Professionals on Social

Oceania's Most Active Banking Professionals on Social - February 2021 Industry at a glance: Why should you care? So, where does your company rank? Position Company Name LinkedIn URL Location Employees on LinkedIn No. Employees Shared (Last 30 Days) % Shared (Last 30 Days) Rank Change 1 Teachers Mutual Bank https://www.linkedin.com/company/285023Australia 451 34 7.54% ▲ 4 2 P&N Bank https://www.linkedin.com/company/2993310Australia 246 18 7.32% ▲ 8 3 Reserve Bank of New Zealand https://www.linkedin.com/company/691462New Zealand 401 29 7.23% ▲ 9 4 Heritage Bank https://www.linkedin.com/company/68461Australia 640 46 7.19% ▲ 9 5 Bendigo Bank https://www.linkedin.com/company/10851946Australia 609 34 5.58% ▼ -4 6 Westpac Institutional Bank https://www.linkedin.com/company/2731362Australia 1,403 73 5.20% ▲ 16 7 Kiwibank https://www.linkedin.com/company/8730New Zealand 1,658 84 5.07% ▲ 10 8 Greater Bank https://www.linkedin.com/company/1111921Australia 621 31 4.99% ▲ 0 9 Heartland Bank https://www.linkedin.com/company/2791687New Zealand 362 18 4.97% ▼ -6 10 ME Bank https://www.linkedin.com/company/927944Australia 1,241 61 4.92% ▲ 1 11 Beyond Bank Australia https://www.linkedin.com/company/141977Australia 468 22 4.70% ▼ -2 12 Bank of New Zealand https://www.linkedin.com/company/7841New Zealand 4,733 216 4.56% ▼ -10 13 ING Australia https://www.linkedin.com/company/387202Australia 1,319 59 4.47% ▲ 16 14 Credit Union Australia https://www.linkedin.com/company/784868Australia 952 42 4.41% ▼ -7 15 Westpac https://www.linkedin.com/company/3597Australia -

Global Currency Card Funds Redemption Form

Global Currency Card Funds Redemption Form. Complete this form to transfer any remaining balances from your closed Global Currency Card account to a nominated account. Funds Redemption Details. To transfer any remaining funds, provide your Global Currency Card information and Australian bank account details below. Please note, any remaining funds will be paid to you in Australian Dollars (AUD) within 20 business days of receipt of this form. First name: Suburb: Postcode: Middle name: Mobile: Surname: Last 4 digits of your card number: Date of birth: / / Destination BSB: Scan a signed and completed copy of this form to: Bank of Melbourne Global Currency Card Service Centre PO Box 3845 Destination account number: RHODES NSW 2138 Or fax to + 61 1300 781 289 Questions? Please call 1300 804 266 in Australia or +61 3 8536 7873 when travelling for 24/7 support. I authorise Bank of Melbourne to transfer the Available Balance of my Global Currency Card account less any outstanding transactions, fees or amounts owed by me, in accordance with the account details provided by me. Signature Date ✗ / / Internal use only Residual value AUD: Authoriser name: Authoriser signature ✗ The details: Bank of Melbourne Global Currency Card is issued by Cuscal Limited ACN 087 822 455 AFSL 244116 (Cuscal). Cuscal is an authorised deposit taking institution and a member of Visa International and does not take deposits from you. Westpac Banking Corporation is the distributor of the product and is not responsible for and does not guarantee the product or card or your ability to access any prepaid value or the use of the product or card. -

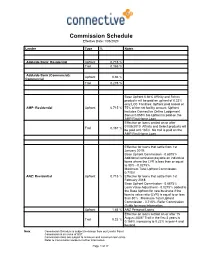

Commission Schedule Effective Date: 1/06/2020

Commission Schedule Effective Date: 1/06/2020 Lender Type % Notes Adelaide Bank: Residential Upfront 0.715 % Trail 0.165 % Adelaide Bank (Commercial): Upfront 0.66 % Commercial Trail 0.275 % Base Upfront 0.66% Affinity and Select products will be paid an upfront of 0.33% only LOC Facilities: Upfront paid based on AMP: Residential Upfront 0.715 % 75% of the net facility amount Upfront includes Connective Online Lodgement Bonus 0.055% No Upfront is paid on the AMP First Home Loan. Effective on loans settled on or after 01/05/2010 Affinity and Select products will Trail 0.187 % be paid at 0.165% No trail is paid on the AMP First Home Loan Effective for loans that settle from 1st January 2019: Base Upfront Commission - 0.6875% Additional comission payable on individual loans where the LVR is less than or equal to 80% - 0.0275% Maximum Total Upfront Commission: 0.715% ANZ: Residential Upfront 0.715 % Effective for loans that settle from 1st February 2018: Base Upfront Commission - 0.6875% Loan Value Adjustment - 0.0275% added to the Base Upfront for new business if the loan to value ratio (LVR) is equal to or less than 80% . Maximum Total Upfront Commission - 0.715%. Refer Commission Guide for more information. Upfront 1.65 % ANZ Personal Loans Effective on loans settled on or after 15 August 2008* Trail in the first 3 years is Trail 0.22 % 0.165% increasing to 0.22% in year 4 and beyond. Note: Commission Schedule is subject to change from our Lender Panel. Commission is inclusive of GST. -

List of Participating Lenders - Phase 2

List of Participating lenders - Phase 2 The Government is currently considering applications from lenders interested in participating in Phase 2 of the Scheme. The following lenders have been approved to participate in Phase 2. ANZ Banjo Bank Australia Bank of Queensland Bendigo and Adelaide Bank Ltd Bigstone Lending Commonwealth Bank of Australia Community First Credit Union Limited Credabl Earlypay Fifo Capital Finstro Securities Pty Ltd Flexirent Capital Get Capital Heritage Bank Limited Hume Bank Limited IQumulate Premium Funding Judo Bank Pty Ltd Liberty Financial Metro Finance Pty Ltd Moneytech Finance Moula Money National Australia Bank Limited Prospa Queensland Country Bank Limited / Regional Australia Bank Ltd Social Enterprise Finance Australia Southern Cross Credit Union South West Credit Union Speedy Finance Suncorp-Metway Limited TrailBlazer Finance Unity Bank Volkswagen Financial Services Australia Westpac Banking Corporation Zip Business List of Participating Lenders - Phase 1 The Government approved 44 lenders to participate in the Coronavirus SME Guarantee Scheme Phase 1. The following lenders were approved to participate in the Scheme. Phase 1 of the Scheme commenced on 23 March 2020 and closed for new loans on 30 September 2020. ANZ Australian Mutual Bank Limited Banjo Bank Australia Bank of Queensland Bank of us Bendigo and Adelaide Bank Ltd Commonwealth Bank of Australia Community First Credit Union Credabl Fifo Capital Australia Pty Ltd First Choice Credit Union Get Capital / Goulburn Murray Credit Union Heritage -

Home Loan Redraw Request Form

Redraw Request Form – Residential Home Loans Note to (1) Redraw is not available for Super Fund Home Loans, Senior Access Home Loans, Senior Access Plus Home Loans and Money borrower(s): For Livings Loans. (2) For variable rate loans, amounts which you have prepaid under your agreement less than a month before a monthly repayment date cannot be redrawn until after that monthly repayment date has passed and the amount redrawn does not result in the balance owing on your loan account exceeding the amount which would be owing if you had paid all scheduled repayments on time. (3) For fixed rate loans, redraw is only available for loans fixed on and after 30 November 2009 and only for excess funds paid into the loan during the current fixed rate period up to the value of the prepayment threshold. (4) Please complete (i) all questions, (ii) use a black pen, AND (iii) use CAPITAL LETTERS. (5) All Borrowers on your loan account must sign. (6) The Bank does not promise it will relend you the redraw amount. This request is subject to its consent. (7) You should obtain your own tax advice in relation to the redraw. (8) The Bank only accepts this request by lending the redraw amount. The Bank is not treated as accepting the request in any other circumstances. (9) Redraw requests up to $30,000 made in a branch can be processed immediately. The processing of other redraw requests using this form will take approximately five working days. Our privacy policy is available at bankofmelbourne.com.au or by calling Date Loan account number 13 22 66 and covers how we handle your / / personal information. -

Customer Identification Form (CIF)

Customer Identification Form (CIF) Information Required Individual Customers must complete section 1, 3 and 4 Sole Traders must complete sections 1, 2, 3 and 4 CIS No. (if known) Account number (if known) Account Name Section 1 Details of Individual to Individual (name in full) Date of birth Gender be identified (Individual Customers and Sole Are you known by any other name(s)? If yes, please specify all names (use a separate sheet if required) Traders) Yes No Residential address (PO Box not allowed) Employment Type: Please select the employment type that reflects your current situation best. Casual Other Social Security Recipient Dependant Contractor Part Time Student Full Time Retired Temporary Independent Contractor Self Employed Unemployed Occupation Purpose of business relationship: This refers to your reasons for engaging with us to obtain products and services. Customers may have multiple reasons for dealing with us. Please indicate all of these reasons below. Transactional Long Term Borrowing Financial Markets Savings Protection Correspondent Banking Short Term Borrowing Wealth Additional information (please specify) Source of Funds: This refers to the origin of the funds that are the subject of the business relationship between you and us. Please note that many customers have multiple sources of funds. Please indicate all sources of funds below. Salary/Wages Superannuation/Pension Redundancy Commission Loan Inheritance Bonus Insurance payment Gift/Donation Business income/earnings Compensation payment Windfall Business profits Government benefits Tax refund Investment income/earnings Sale of assets Additional Sources (please specify) Rental income Liquidation of assets © Bank of Melbourne – A Division of Westpac Banking Corporation ABN 33 007 457 141 AFSL and Australian credit licence 233714. -

Report: Inquiry Into Aspects of Bank Mergers

The Senate Economics References Committee Report on Bank Mergers September 2009 © Commonwealth of Australia 2009 ISBN 978-1-74229-148-2 Printed by the Senate Printing Unit, Parliament House, Canberra. Senate Economics References Committee Members Senator Alan Eggleston, Chair Western Australia, LP Senator Annette Hurley, Deputy Chair South Australia, ALP Senator David Bushby Tasmania, LP Senator Barnaby Joyce Queensland, NATS Senator Louise Pratt Western Australia, ALP Senator Nick Xenophon South Australia, IND Participating members participating in this inquiry Senator John Williams New South Wales, NATS Former Members Senator Doug Cameron New South Wales, ALP Senator Mark Furner Queensland, ALP Secretariat Mr John Hawkins, Secretary Mr Greg Lake, Principal Research Officer Mr Glenn Ryall, Senior Research Officer Ms Hanako Jones, Executive Assistant Ms Lauren McDougall, Executive Assistant PO Box 6100 Parliament House Canberra ACT 2600 Ph: 02 6277 3540 Fax: 02 6277 5719 E-mail: [email protected] Internet: http://www.aph.gov.au/senate_economics/ iii TABLE OF CONTENTS Membership of Committee iii Chapter 1.............................................................................................................. 1 Introduction .............................................................................................................. 1 Referral of the Inquiry ............................................................................................ 1 Conduct of the inquiry ........................................................................................... -

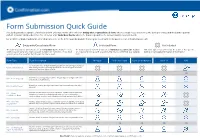

Form Submission Quick Guide This Guide Provides a Sample of Banks and Form Offerings

Form Submission Quick Guide This guide provides a sample of banks and form offerings. Banks offer either an Entity wide / Consolidated form, where a single request is sent to the bank per entity, and the bank responds with all accounts and products for that entity; or offer Individual Forms where the bank responds to the account number provided only. For a full list of banks and forms offered, please refer to the In Network Responder Report generated from the Reports section in Confirmation.com. Entity wide/Consolidated Form Individual Form Not Included The bank responds to form details on an entity wide basis. Auditors send a The bank responds to form details on an individual account basis. Auditors This form type is not offered by the bank as the specific single request using one main account number for reference. If no main are required to set up each account number to be confirmed as a separate bank does not supply information in this manner. account exists the customer identification number is used. form. Form Type Form Description Westpac St George Bank Bank of Melbourne Bank SA NAB For each form sent, the bank will then provide an extensive report of all your Client Consolidated bank dealings for the legal entity specified. No other form types should be submitted if this form option is used. OR An asset account is typically a current, cheque, deposit, savings, investment AU – Asset (Deposit) and any other credit balance. A liability account is typically a bank loans, term loans and any other debit AU – Liability (Loan) balances.