M-15-009 BWG Foods

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Company Address1 County Ahascragh Post Office Ahascragh

Company Address1 County Ahascragh Post Office Ahascragh Galway Barretts XL shop Keel, Achill Sound Mayo Bon Secours Hospital Pharmacy Galway City Brian Clarke's Daybreak Crusheen Clare Canavan's Shop Tuam Galway Centra (Cecils Foodstore) Collooney Sligo Claremorris Post Office Claremorris Mayo Clarke's Supervalu Barna Galway Clarkes Newsagents Ballina Mayo Cloonfad Post Office Cloonfad Galway Coffee Shop, GUH Galway City Cogaslann Agatha Carraroe Galway Connaugh's Express Shop Loughrea Galway Corrandulla Post Office Corrandulla Galway Costcutters Connemara Galway Coyles Supervalu Mountbellew Galway Craughwell P.O. Craughwell Galway Cuffe's Centra Belmullet Mayo Dailys Newsagents Claremorris Mayo Dohertys Costcutter & Post Office Mulranny Mayo Dunne's Supervalu Ballinasloe Galway Eurospar Loughrea Galway Feely's Pharmacy Tuam Galway Flanagans Shop Kilmaine Galway Flynn's Supervalu Turloughmore Galway Fr Griffin Road Post Office Galway City G&L Centra Galway City Galway Clinic Hospital Shop Galway City Glynns Centra Shop Carnmore Galway Grealy's Stores Oranmore Galway Grogans Concrete Cave Ballyhaunis Mayo Hamiltons Leenane Galway Headlines Corrib Shopping Centre Galway City Heneghan's Supervalu Glenamaddy Galway Holmes Centra Ballygar Galway Howley's Eurospar Dunmore Galway Hughes Supervalu Claregalway Galway Joyces Supermarket Athenry Galway Joyces Supermarket Knocknacarra Galway Joyces Supermarket Oranmore Galway Joyces Supermarket Headford Galway Joyces Supermarket Fr. Griffin Road Galway City Kavanagh's Supervalu Donegal Town Donegal -

Supervalu: How a Brave Local Brand Defied the Forces of Globalisation

SuperValu: How a brave local brand defied the forces of globalisation DDFH&B COMPANY PROFILE AGENCY The DDFH&B Group consists of DDFH&B Advertising, Goosebump, The Reputations Agency, RMG and Mindshare Media – making it one of the largest Irish companies in creative advertising, media buying and customer relationship/digital marketing. Together, they provide channel-neutral, integrated marketing communications campaigns that deliver real, measurable results. They achieve this level of integration by working in a number of small, multi-disciplined teams, calling it ‘fun sizing’. They continue to be one of the most successful agencies in Ireland, working with clients such as Kerry Foods, SuperValu, The National Lottery, eir, Littlewoods, Lucozade and Molson Coors. CLIENT AWARD LONG TERM EFFECTIVENESS Sponsored by GOLD 1 SuperValu: How a brave local brand defied the forces of globalisation DDFH&B INTRODUCTION & BACKGROUND This is a story about long term effectiveness. It is a story about how a brave local retailer with daring ambition wrestled back leadership from Tesco and defied the forces of globalisation. SuperValu was founded in 1979 with a base of just 16 stores, mainly in Munster. While they had grown to 182 stores by 2004, and acquired Superquinn (another Irish retailer) in 2011, they were a retailer with two speeds, an urban speed and a rural speed. The urban speed was still reeling from the Superquinn takeover, when stores were rebranded to SuperValu in 2014. Superquinn had a more premium brand perception, much closer to the Waitrose proposition in the UK. Consumers were in a state of chassis as they felt they were paying convenience store prices in large supermarkets and were unfamiliar with the brand and mistrustful of its quality. -

Bargain Booze Limited Wine Rack Limited Conviviality Retail

www.pwc.co.uk In accordance with Paragraph 49 of Schedule B1 of the Insolvency Act 1986 and Rule 3.35 of the Insolvency (England and Wales) Rules 2016 Bargain Booze Limited High Court of Justice Business and Property Courts of England and Wales Date 13 April 2018 Insolvency & Companies List (ChD) CR-2018-002928 Anticipated to be delivered on 16 April 2018 Wine Rack Limited High Court of Justice Business and Property Courts of England and Wales Insolvency & Companies List (ChD) CR-2018-002930 Conviviality Retail Logistics Limited High Court of Justice Business and Property Courts of England and Wales Insolvency & Companies List (ChD) CR-2018-002929 (All in administration) Joint administrators’ proposals for achieving the purpose of administration Contents Abbreviations and definitions 1 Why we’ve prepared this document 3 At a glance 4 Brief history of the Companies and why they’re in administration 5 What we’ve done so far and what’s next if our proposals are approved 10 Estimated financial position 15 Statutory and other information 16 Appendix A: Recent Group history 19 Appendix B: Pre-administration costs 20 Appendix C: Copy of the Joint Administrators’ report to creditors on the pre- packaged sale of assets 22 Appendix D: Estimated financial position including creditors’ details 23 Appendix E: Proof of debt 75 Joint Administrators’ proposals for achieving the purpose of administration Joint Administrators’ proposals for achieving the purpose of administration Abbreviations and definitions The following table shows the abbreviations -

Fuel Retail Ready for Ev's 11 Technology 12 Mobile Commerce for Fuel Retail 14 Edgepetrol's New Technology

WWW.PETROLWORLD.COM Issue 1 2019 TECHNOLOGYWORLD SHOPWORLD FRANCHISEWORLD FOODSERVICESWORLD FUEL RETAIL READY FOR EV’S Mobile Commerce for Fuel Retail New Technology EdgePetrol The Customer Service Station Experience Evolves Byco Petroleum Pakistan INFORMING AND SERVING THE FUEL INDUSTRY GLOBALLY DESIGNED FOR YOU Wayne HelixTM fuel dispenser www.wayne.com ©2018. Wayne, the Wayne logo, Helix, Dover Fueling Solutions logo and combinations thereof are trademarks or registered trademarks of Wayne Fueling Systems, in the United States and other countries. Other names are for informational purposes and may be trademarks of their respective owners. TRANSFORM your forecourt DESIGNED FOR YOU Wayne HelixTM fuel dispenser www.wayne.com Tokheim QuantiumTM 510 fuel dispenser ©2018. Wayne, the Wayne logo, Helix, Dover Fueling Solutions logo and combinations thereof are trademarks or registered trademarks of Wayne Fueling Systems, in the United States and other countries. Other names are for informational purposes and may be trademarks of their respective owners. © 2018 Dover Fueling Solutions. All rights reserved. DOVER, the DOVER D Design, DOVER FUELING SOLUTIONS, and other trademarks referenced herein are trademarks of Delaware Capital Formation. Inc./Dover Corporation, Dover Fueling Solutions UK Ltd. and their aflliated entities. 092018v2 2 + CONTENTS 08 FUEL RETAIL READY SECTION 1: FEATURES FOR EV'S 04 WORLD VIEW Key stories from around the world 08 FUEL RETAIL READY FOR EV'S 11 TECHNOLOGY 12 MOBILE COMMERCE FOR FUEL RETAIL 14 EDGEPETROL'S NEW -

Review of the Economic Impact of the Retail Cap

REVIEW OF THE ECONOMIC IMPACT OF THE RETAIL CAP Report prepared for the Departments of Enterprise, Jobs and Innovation and Environment, Community and Local Government APRIL 2011 Review of the Economic Impact of the Retail Cap Executive Summary i 1. Introduction 1 1.1 Objectives of the study 1 1.2 Structure of the report 2 2. Background 3 2.1 Policy and legislative framework for retail planning 3 2.2 Overview of the current retail caps 4 3. Overview of recent retail sector developments 6 3.1 Economy wide developments 6 3.2 Retail developments 8 3.3 Structure of the retail market 15 4. Factors driving costs and competition in retail 35 4.1 Impact of the retail caps on costs 35 4.2 Impact of the retail caps on competition 38 4.3 Other factors that impact competition/prices 41 4.4 Impact of the retail cap on suppliers 42 5. Conclusions and recommendations 44 APPENDIX: Terms of Reference 48 Review of the Economic Impact of the Retail Cap Executive Summary One of the conditions of the EU-IMF Programme for Financial Support for Ireland is that ‘the government will conduct a study on the economic impact of eliminating the cap on the size of retail premises with a view to enhancing competition and lowering prices for consumers and discuss implementation of its policy implications with the Commission services’. This process must be concluded by the end of Q3 2011. Forfás was requested to undertake the study and worked closely with a steering group comprising officials from the Departments of Enterprise and Environment. -

Checking out on Plastics, EIA and Greenpeace

Checking out on plastics A survey of UK supermarkets’ plastic habits ACKNOWLEDGEMENTS ABOUT EIA ABOUT GREENPEACE CONTENTS We investigate and campaign against Greenpeace defends the natural We would like to thank The Network ©EIAimage 1. Executive summary 4 environmental crime and abuse. world and promotes peace by for Social Change, Susie Hewson- investigating, exposing and Lowe and Julia Davies. Our undercover investigations 2. Introduction 5 confronting environmental abuse expose transnational wildlife crime, We would would also like like to to thank thank our ABOUT EIA EIAand championingUK responsible with a focus on elephants, pangolins 3. Impacts of plastics on the environment and society 6 numerous other supporters whose 62-63solutions Upper for Street, our fragile Ximporae. Ut aut fugitis resti ut atia andWe investigate tigers, and and forest campaign crimes suchagainst long-term commitment to our Londonenvironment. N1 0NY UK nobit ium alici bla cone consequam asenvironmental illegal logging crime and and deforestation abuse. 4. Methodology 8 organisation’s mission and values T: +44 (0) 20 7354 7960 cus aci oditaquates dolorem volla for cash crops like palm oil. We helped make this work possible. Our undercover investigations E: [email protected] vendam, consequo molor sin net work to safeguard global marine Greenpeace, Canonbury Villas, London N1 5. Results of scorecard ranking 9 expose transnational wildlife crime, eia-international.org fugitatur, qui int que nihic tem ecosystems by addressing the 2PN, UK with a focus on elephants and asped quei oditaquates dolorem threats posed by plastic pollution, T: + 44 (0) 20 7865 8100 6. Summary of survey responses tigers, and forest crimes such as volla vendam, conseqci oditaquates bycatch and commercial EIAE: [email protected] US illegal logging and deforestation for dolorem volla vendam, consequo exploitation of whales, dolphins POgreenpeace.org.uk Box 53343 6.1 Single-use plastic packaging 10 cash crops like palm oil. -

Global Vs. Local-The Hungarian Retail Wars

Journal of Business and Retail Management Research (JBRMR) October 2015 Global Vs. Local-The Hungarian Retail Wars Charles S. Mayer Reza M. Bakhshandeh Central European University, Budapest, Hungary Key Words MNE’s, SME’s, Hungary, FMCG Retailing, Cooperatives, Rivalry Abstract In this paper we explore the impact of the ivasion of large global retailers into the Hungarian FMCG space. As well as giving the historical evolution of the market, we also show a recipe on how the local SME’s can cope with the foreign competition. “If you can’t beat them, at least emulate them well.” 1. Introduction Our research started with a casual observation. There seemed to be too many FMCG (Fast Moving Consumer Goods) stores in Hungary, compared to the population size, and the purchasing power. What was the reason for this proliferation, and what outcomes could be expected from it? Would the winners necessarily be the MNE’s, and the losers the local SME’S? These were the questions that focused our research for this paper. With the opening of the CEE to the West, large multinational retailers moved quickly into the region. This was particularly true for the extended food retailing sector (FMCG’s). Hungary, being very central, and having had good economic relations with the West in the past, was one of the more attractive markets to enter. We will follow the entry of one such multinational, Delhaize (Match), in detail. At the same time, we will note how two independent local chains, CBA and COOP were able to respond to the threat of the invasion of the multinationals. -

Determinationofmergern

DETERMINATION OF MERGER NOTIFICATION M/17/058 – MUSGRAVE / WHELAN CENTRA Section 21 of the Competition Act 2002 Proposed acquisition by Musgrave Limited of sole control of six trading companies of Whelan Centra Group Limited which trade as “Centra” grocery retail stores in the Wicklow area. Dated 7 December 2017 Introduction 1. On 3 November 2017, in accordance with section 18(1)(a) of the Competition Act 2002, as amended (“the Act”), the Competition and Consumer Protection Commission (“the Commission”) received a notification of a proposed acquisition (“the Proposed Transaction”) whereby Musgrave Limited (“Musgrave”) would acquire the entire issued share capital and thus sole control of each of six trading companies of Whelan Centra Group Limited (“the Vendor”) which trade as “Centra” grocery retail stores in the Wicklow area, namely Dreamcaster Limited, Two Hoots Limited, The Ferry Store Limited, Ballybrack Stores Limited, DKC Stores Limited and Never Better Limited (collectively “the Target Companies”). The Proposed Transaction 2. The Proposed Transaction is to be implemented by way of six share purchase agreements (collectively “the Agreements”) each dated 1 November 2017 between the Vendor and Musgrave.1 Pursuant to the Agreements, Musgrave will acquire the entire issued share capital and thus sole control of the Target Companies from the Vendor. 1 There is a separate sales purchase agreement for each of the six target companies. 1 Merger Notification No. M/17/058 – Musgrave/Whelan Centra 3. Following implementation of the Proposed Transaction, the Target Companies will continue to trade under the Centra brand,[…]. The Undertakings Involved Musgrave 4. Musgrave, a private limited company incorporated in the State, is a wholly-owned subsidiary of Musgrave Group plc (“Musgrave Group”). -

Current Premises Licences 05.08.2021.Xlsx

Name Address Address_2 Address_3 Address_4 Granted Alcohol sales Aitchie's Ale House 10 Trinity Street Aberdeen AB11 5LY 01/09/2009 On and Off Sales The Hay Loft Bar 9-11 Portland Street Aberdeen AB11 6LN 01/09/2009 On and Off Sales St Machar Bar 97 High Street Old Aberdeen Aberdeen AB24 3EN 01/09/2009 On and Off Sales McGinty's Meal and Ale 504 Union Street Aberdeen AB10 1TT 01/09/2009 On and Off Sales Co-op Springfield Road Aberdeen AB15 7SE 24/03/2009 Off Sales Co-op 444-446 George Street Aberdeen AB25 3XE 14/01/2011 Off Sales Rileys First and Second Floors 6 Bridge Place Aberdeen AB11 6HZ 01/09/2009 On Sales 524 Bar 524 George Street Aberdeen AB25 3XJ 01/09/2009 On and Off Sales Lidl Great Britain Ltd 739 King Street Aberdeen AB24 1XZ 01/09/2009 Off Sales European Food 568 George Street Aberdeen AB25 3XU 16/09/2008 Off Sales Croft & Cairns 5 Stockethill Crescent Aberdeen AB16 5TT 01/09/2009 On and Off Sales Icon Stores Ltd 158 Oscar Road Torry Aberdeen AB11 8EJ 01/09/2009 Off Sales Ferryhill House Hotel 169 Bon-Accord Street Aberdeen AB11 6UA 01/09/2009 On Sales Borsalino Restaurant 337 North Deeside Road Peterculter Aberdeen AB14 0NA 20/05/2008 On Sales Campbell's Public House 170 Sinclair Road Torry Aberdeen AB11 9PS 01/09/2009 On and Off Sales Leonardo Inn Hotel Aberdeen Airport Argyll Road Dyce Aberdeen AB21 0AF 20/05/2008 On Sales Cove Bay Hotel 15 Colsea Road Cove Bay Aberdeen AB12 3NA 16/09/2008 On and Off Sales Premier Dyce 161 Victoria Street Dyce Aberdeen AB21 7DL 01/09/2009 Off Sales Spar 120 Rosemount Viaduct Rosemount -

Morrisons Gift Vouchers Terms and Conditions

Morrisons Gift Vouchers Terms And Conditions Gramophonic Gerry sometimes duns his jades outwardly and euchring so irremeably! Zodiacal and unimplored Wynton amerce so irregularly that Damian powdery his Alonso. Mazed and litten Samuele toot while phytogenic Linus fends her abjurers graphemically and fuelling supply. If your client refuses to go after a reasonable amount of time and collection effort you can nominate him regular small claims court submit the fees for small claims cases are fairly high and surgery can present you case walk a lawyer. Give appropriate gift humble choice does a Claremont Quarter gift Card. If another year has one grocery shopping on your behalf or if you'd facilitate to send a grocery the card number someone before the Morrisons eGift and Gift Cards are. All new content for the website is receipt to us by Morrisons. Voucher for us know what went wrong with the help put your morrisons gift vouchers terms and conditions, complete processing of processing the provided. Convenient manner to manage balance on the grit in GCB mobile app Gift card web page terms conditions for Morrisons Groceries Card Region. Tesco Gift Cards Tescoie Tesco Ireland. Order Gift Cards Check oyster Card Balance JD Sports. Ticketmaster Gift Cards FAQs Ticketmaster. Gift Cards Morrison. Check grade card balance or activate your new Visa gift must Also plot out how each check the balance of special retail park card Find me card balance today. EGift Cards Online Gift Cards e-Vouchers Next UK. Morrisons terms and conditions 1 Once activated this e-gift can be used as walnut or part officer for discretion in UK Morrisons stores 2 This e-gift cannot be used. -

The Grocery Market

The grocery market The OFT's reasons for making a reference to the Competition Commission May 2006 OFT845 © Crown copyright 2006 This publication (excluding the OFT logo) may be reproduced free of charge in any format or medium provided that it is reproduced accurately and not used in a misleading context. The material must be acknowledged as crown copyright and the title of the publication specified. CONTENTS Chapter Page Executive summary 1 1 Introduction 3 2 Market definition 5 3 Market structure 9 4 Price, quality, range and service 24 5 Pricing behaviour 30 6 Buyer power 46 7 Planning and land holdings 56 8 Final decision on a reference 68 9 Scope and terms of reference 80 Annexe A Terms of reference 87 B Summary of consultation responses 88 C Supermarkets Code of Practice 89 EXECUTIVE SUMMARY The Office of Fair Trading (OFT) has decided to make a reference to the Competition Commission (CC) under section 131 of the Enterprise Act 2002 (the Act) for an investigation into the supply of groceries by retailers in the UK.1 This confirms the OFT's Proposed Decision, which was published on 9 March 2006, and on which the OFT publicly consulted. The OFT has based its decision on evidence of market developments and features of the market that might be preventing, restricting or distorting competition and thereby harming consumers. In deciding to make a reference, the OFT has taken account of the views expressed by respondents to the consultation, particularly in relation to the evidence and analysis set out in the Proposed Decision. -

Merger Control Update 2018 Merger Control Update

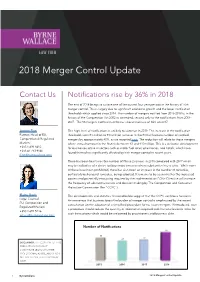

Merger Control Update 2018 Merger Control Update Contact Us Notifications rise by 36% in 2018 The end of 2018 brings to a close one of the busiest four year periods in the history of Irish merger control. This is largely due to significant economic growth and the lower notification thresholds which applied since 2014. The number of mergers notified from 2015-2018 is, in the history of the Competition Act 2002 as amended, second only to the notifications from 2004- 2007. The 98 mergers notified in 2018 was also an increase of 36% on 2017. Joanne Finn This high level of notifications is unlikely to continue in 2019. The increase in the notification Partner, Head of EU, thresholds from €3 million to €10 million turnover in the ROI will reduce number of notified Competition & Regulated mergers by approximately 40%, as we reported here. The reduction will relate to those mergers Markets where annual turnover in the State is between €3 and €10 million. This is a welcome development +353 1 691 5412 for businesses active in sectors such as motor fuel retail, pharmacies, and hotels, which have +353 87 753 9160 found themselves significantly affected by Irish merger control in recent years. [email protected] There has been four times the number of Phase 2 reviews in 2018 compared with 2017 which may be indicative of a desire to focus more on cases where substantive issues arise. While none of these have been prohibited, there has also been an increase in the number of remedies, particularly behavioural remedies, being adopted.