Overcoming Fragmentation – the Payments Platform Challenge OVERCOMING FRAGMENTATION – the PAYMENTS PLATFORM CHALLENGE

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chinese Online Payment Platforms for Their Individual Needs

SNAPSHOT GUIDE TO ONLINE PAYMENT PLATFORMS FOR CHINESE VISITORS JULY 2017 OVERVIEW The use of online payment platforms has reshaped the way people pay for goods and services in China. Over the past five years, financial transactions are increasingly being handled through the use of advanced technology in a smartphone device, creating a fast and easy way for customers to pay for goods and services. While there are over 700 million registered users of online payment platforms in China – who complete approximately 380 million transactions a day – use of these platforms in Australia is relatively limited. In the year ending March 2017, 1.2 million Chinese visited Australia (up 12% from the previous year). Chinese visitors to Australia are the highest spending ($9.2 billion in 2016, or around $8,000 per visitor). Integrating online payment platforms recognised by Chinese visitors into business operations provides Australian businesses significant revenue yield opportunities and options better aligned to customer expectations. ONLINE PAYMENT PLATFORMS Also known as a digital wallet or e-wallet, these platforms are linked to a bank account, where transactions are processed without the use of a bank card i.e. similar to the way PayPal works. Online payment platforms can be used for purchases online or in-person. How an online payment platform works: Using a payment platform app, the customer generates a one- time QR code on their smartphone. The merchant uses a small device to scan the QR code given by the customer to process payment for the purchase of goods or services. In Australia, funds are in the merchant’s account within two business days after the date of transaction. -

Is China's New Payment System the Future?

THE BROOKINGS INSTITUTION | JUNE 2019 Is China’s new payment system the future? Aaron Klein BROOKINGS INSTITUTION ECONOMIC STUDIES AT BROOKINGS Contents About the Author ......................................................................................................................3 Statement of Independence .....................................................................................................3 Acknowledgements ...................................................................................................................3 Executive Summary ................................................................................................................. 4 Introduction .............................................................................................................................. 5 Understanding the Chinese System: Starting Points ............................................................ 6 Figure 1: QR Codes as means of payment in China ................................................. 7 China’s Transformation .......................................................................................................... 8 How Alipay and WeChat Pay work ..................................................................................... 9 Figure 2: QR codes being used as payment methods ............................................. 9 The parking garage metaphor ............................................................................................ 10 How to Fund a Chinese Digital Wallet .......................................................................... -

India's Open Payments Competition Can Spread

India’s open payments competition can spread to other markets By Eric Grover PaymentsSource October 3, 2017 India promises to be an epic payments battleground between traditional payment systems and tech giants, and perhaps a harbinger for emerging markets in general. Traditional retail payment systems such as Mastercard and Visa enjoy powerful network effects and market position in Europe and North America. But they were restricted in China, mobile commerce phenoms Alipay and WeChat Pay, and card network monopoly China UnionPay sewed up the market. The world’s largest in-play payments market India, however, is a wide open creative and competitive ferment, with Indian consumers and merchants the ultimate winners. With backing from Ant Financial, Paytm is just one of many well-heeled competitors battling in India's wide open payments market. Card networks including national champion RuPay, U.S. tech titans, Chinese fintech powers, MNOs, and an etailer are among the major players in India. MasterCard and Visa bring the power of their global networks tailored to the subcontinent to bear. Unlike in the U.S., they face formidable and nontraditional competitors on near equal footing. For U.S. tech behemoths, India is irresistible. Like the global payment networks they’ve largely been boxed out of China. In mature European and North American markets consumers and merchants are well served by existing payment systems and banks. Consequently, American tech titans haven’t attempted to build payment networks. Instead they use and facilitate access to existing systems, thereby increasing consumer engagement on and the value of their platforms. Tech platforms such as Google, Apple, Facebook and Amazon enjoy network effects in markets where the winner takes all or there are only a couple winners. -

How Will Traditional Credit-Card Networks Fare in an Era of Alipay, Google Tez, PSD2 and W3C Payments?

How will traditional credit-card networks fare in an era of Alipay, Google Tez, PSD2 and W3C payments? Eric Grover April 20, 2018 988 Bella Rosa Drive Minden, NV 89423 * Views expressed are strictly the author’s. USA +1 775-392-0559 +1 775-552-9802 (fax) [email protected] Discussion topics • Retail-payment systems and credit cards state of play • Growth drivers • Tectonic shifts and attendant risks and opportunities • US • Europe • China • India • Closing thoughts Retail-payment systems • General-purpose retail-payment networks were the greatest payments and retail-banking innovation in the 20th century. • >300 retail-payment schemes worldwide • Global traditional payment networks • Mastercard • Visa • Tier-two global networks • American Express, • China UnionPay • Discover/Diners Club • JCB Retail-payment systems • Alternative networks building claims to critical mass • Alipay • Rolling up payments assets in Asia • Partnering with acquirers to build global acceptance • M-Pesa • PayPal • Trading margin for volume, modus vivendi with Mastercard, Visa and large credit-card issuers • Opening up, partnering with African MNOs • Paytm • WeChat Pay • Partnering with acquirers to build overseas acceptance • National systems – Axept, Pago Bancomat, BCC, Cartes Bancaires, Dankort, Elo, iDeal, Interac, Mir, Rupay, Star, Troy, Euro6000, Redsys, Sistema 4b, et al The global payments land grab • There have been campaigns and retreats by credit-card issuers building multinational businesses, e.g. Citi, Banco Santander, Discover, GE, HSBC, and Capital One. • Discover’s attempts overseas thus far have been unsuccessful • UK • Diners Club • Network reciprocity • Under Jeff Immelt GE was the worst-performer on the Dow –a) and Synchrony unwound its global franchise • Amex remains US-centric • Merchant acquiring and processing imperative to expand internationally. -

China's Alipay and Wechat Pay: Reaching Rural Users

China’s Alipay and WeChat Pay: Reaching Rural Users Chinese information technology conglomerates Alibaba1 and Tencent own or operate dozens of competing online businesses, and yet, their affiliate mobile wallets stand out for how they have fundamentally influenced everyday living in China’s cities. Alibaba through its dominance in e-commerce and Tencent through its mobile social media and messaging platforms (WeChat and QQ) connect mass-market audiences with their respective wallet products: Alipay and WeChat Pay. Although these services are the product of unique market conditions, they offer many learning opportunities. Perhaps most extraordinary has been the companies’ ability to build trust with users. Tencent and Ant Financial, Alibaba’s financial affiliate, are redefining the relationship users have with finance. Finance is becoming simpler; it is also remarkably more social in nature. This holds great promise for advancing rural financial inclusion in China. However, challenges in serving last-mile clients remain. BRIEF Today, the Alipay and WeChat Pay mobile wallets, which technical experience, a massive user base, and extensive link users’ bank cards to a smartphone application, each bank networks, but transactions were predominantly still has hundreds of millions of active users; combined they done on desktop devices for e-commerce. By the time hold 92 percent of market share (most users have both Tencent rolled out its own wallet in 2013 as a part of wallets). China Internet Network Information Center its mobile-only WeChat application—a messaging and (CNNIC), a government agency, reports that China now social media platform (Shrader 2014)—online activity has 502 million unique mobile payment users—almost as was quickly shifting to mobile. -

Payment Facilitation Terms Australia 28 April 2020

Payment Facilitation Terms Australia 28 April 2020 1 PAYMENT FACILITATION TERMS AUSTRALIA 1. THESE TERMS 1.1. These Payment Facilitation Terms (these ‘Terms’) govern the provision of the Services by Airwallex Pty Ltd ABN 37 609 653 312 (‘Airwallex’, ‘us’, ‘our’ or ‘we’) to the entity or person (‘you’, ‘your’, or ‘Merchant’) identified in the Customer Details. Airwallex and Merchant are each a ‘Party’ and together the ‘Parties’. 1.2. If you receive Services from any additional party, we will provide you with details of those additional parties. The entities providing Services as referred to above as we make known to you will be deemed to be a party to these Terms. 1.3. You must not access or use the Services unless you agree to abide by all of the terms and conditions in these Terms including any Additional Terms. You must agree to the Payment and FX Terms prior to us being obliged to provide you with the Services under these Terms. 1.4. The Parties agree that the Master Services Agreement (if applicable), the Schedules to these Terms, any Additional Terms and other terms referenced in these Terms are incorporated into and form part of these Terms, in each case, as may be amended, varied, supplemented, modified or novated from time to time. 1.5. Please read the following additional documents which also apply to your use of the Airwallex Platform and Services and should be read together with this Agreement: (a) Acceptable Use Policy; (b) Privacy Policy; (c) Electronic Communications Consent; (d) Identity Verification Terms; (e) API Documentation. -

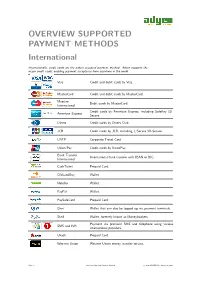

OVERVIEW SUPPORTED PAYMENT METHODS International

OVERVIEW SUPPORTED PAYMENT METHODS International Internationally, credit cards are the widest accepted payment method. Adyen supports the major credit cards, enabling payment acceptance from anywhere in the world. Visa Credit and debit cards by Visa. MasterCard Credit and debit cards by MasterCard. Maestro Debit cards by MasterCard. International Credit cards by American Express, including SafeKey 3D- American Express Secure. Diners Credit cards by Diners Club. JCB Credit cards by JCB, including J/Secure 3D-Secure. UATP Corporate Travel Card. Union Pay Credit cards by UnionPay. Bank Transfer International bank transfer with IBAN or BIC. International CashTicket Prepaid Card. ClickandBuy Wallet. Neteller Wallet. PayPal Wallet. PaySafeCard Prepaid Card. Qiwi Wallet that can also be topped up via payment terminals. Skrill Wallet, formerly known as Moneybookers. Payment via premium SMS and telephone using various SMS and IVR international providers. Ukash Prepaid Card. Western Union Western Union money transfer service. Page 1 Overview Supported Payment Methods c 2012 ADYEN BV - August 23, 2012 Europe Loyalty cards Support for various loyalty and store cards. Austria Bank Transfer Offline bank transfer. Sofortbanking Online banking supporting various local banks. Belgium Bank Transfer Offline bank transfer. BanContact / Mr. Debit card in Belgium. Cash Sofortbanking Online banking supporting various local banks. Denmark Primarily credit card and the local debit scheme. Bank Transfer Offline bank transfer. Dankort Local debit card scheme. Open Invoice Payments on credit by open invoice. Finland Primarily Credit Card. Besides this there is a very good market share for online banking. Bank Transfer Offline bank transfer. Ålandsbanken Online banking. Handelsbanken Online banking. Nordea Online banking. -

Qr Code Payments Landscape

THE QR CODE PAYMENTS LANDSCAPE A LEVEL ONE PROJECT PERSPECTIVE OCTOBER 2019 THE LEVEL ONE PROJECT IS AN INITIATVE OF THE BILL AND MELINDA GATES FOUNDATION GLENBROOK PARTNERS This is A lAndscApe review of QR For this report we looked At the following CONTENTS PayMents Models Around the world, with MArket developments: an emphasis on developments in • SingApore SGQR emerging economies. • IndonesiA QRIS In this report, we describe the vArious • IndiA BhArAtQR and BHIM QR models, with pArticulAr Attention to how QR code iMpleMentAtions connect with • ThAilAnd StAndArdized QR Code the underlying pAyMents systeMs used • AlipAy w/ Europe WAllet Providers to process the pAyMents. • Mexico CoDi We Also Assess how the vArious Models • ChinA AlipAy are aligned with the Level One Project design principles and key concepts. • South AfricA SnApScAn • AsiA GrAbPAy This docuMent is A continuAtion of prior reseArch done for the Level One Project. The 2017 report “Research on QR Code-Based PayMents And its ApplicAtion in Emerging Markets”, which provides A detAiled history on how QR codes were introduced, cAn be downloaded from leveloneproject.org. 2 Glenbrook for Bill And MelindA Gates FoundAtion CONTENTS 5 INTRODUCTION 11 QR CODE MARKET MODELS 29 MARKET LANDSCAPE 48 FRAUD MANAGEMENT 57 FUTURE DIRECTIONS 62 LEVEL ONE ALIGNMENT 72 APPENDIX: QR CODE DATA FORMATS 3 Glenbrook for Bill And MelindA Gates FoundAtion Executive Summary QR Codes used for mercHAnt pAyments Are gAining rApid trAction worldwide. THese pAyments in generAl support Level One goals of growing the digitAl ecosystem: those tHAt work in conjunction with interoperAble payments systems are particularly well-aligned. -

Mobile Payment in China: Practice and Its Effects*

Mobile Payment in China: Practice and Its Effects* Yiping Huang National School of Development / Institute of Digital Finance Peking University [email protected] Xue Wang National School of Development / Institute of Digital Finance Downloaded from http://direct.mit.edu/asep/article-pdf/19/3/1/1847008/asep_a_00779.pdf by guest on 24 September 2021 Peking University [email protected] Xun Wang National School of Development / Institute of Digital Finance Peking University [email protected] Abstract This paper offers a comprehensive review and careful assessment of China’s mobile payment busi- ness. With broad access, low costs, and reliable transactions, mobile payments are creating a revolu- tion of financial inclusion, changing people’s daily lives and commercial business models. This study also confirms that mobile payment improves risk sharing among individuals and increases entrepreneurial opportunities. These mobile payment successes can be traced to three key factors: supply shortages of alternative payment services, a friendly regulatory environment, and recent technological develop- ments. A number of outstanding issues remain, however,including data ownership, data inequality,and regulatory shortcomings. 1. Introduction Mobile payment services, dominated by two leading players, Alibaba’s (now owned by Ant Financial Services) Alipay and Tencent’s WeChat Pay, have become a fixture in China’s daily lives and businesses. Both players have built eco-systems around their mo- bile payment tools. People use Alipay or WeChat Pay to purchase goods, order coffee and * Xun Wang is the corresponding author. The authors are grateful for the financial support by Na- tional Social Science Foundation of China (project no. -

Wechat Pay Alipay

Connect your business to 1 Billion shoppers CHINESE PAYMENTS HOW PEOPLE MAKE PAYMENTS IN CHINA WeChat Pay Alipay WeChat is the most used social Alipay lets users make mobile network and mobile application in payments quickly and easily. China. Its main purpose is to connect users. It is the best platform to reach potential Chinese consumers. Our WeChat Pay is a service integrated Alipay marketing strategy will make into Wechat, which allows Chinese your business more visible and users to make quick payments attractive to these shoppers than without leaving their favorite App. the competition. WHO USES THESE METHODS Alipay WeChat Pay >1 billion users globally 20 MILLION 1 MILLION 27% ages 21-25 35% ages 24-30 Registered 1 Million business accounts shops offer Wechat Pay 3.4 out of 10 consumers paid via mobile in 2019 3H 900 MILLION Fashion, cosmetics and local brands account for More than half of users Active users/month the largest share of spend 3 hours/day on purchases the app WHY MERCHANTS NEED CHINESE PAYMENT METHODS Merchants can... Chinese tourists travel 4 Attract Chinese consumers 4 trips times a year on average 7 days Speed up cashier processes and spend 7 days/trip. Eliminate exchange costs Monitor transaction in real-time Chinese tourists spent an average of €690 per person on shopping €690 during each overseas trip, while non-Chinese tourists averaged €440 per person. Chinese shoppers enjoy… 65% of Chinese tourists used 65% mobile payment platforms during Convenience their overseas travel. Cost savings Secure purchases Cashless processes Source: Nielsen, Outbound Chinese Tourism and Consumption Trends 2018 OUR IN-STORE PAYMENT METHODS IN-STORE WeChat WeChat MIR MIR PAYXPRESS POS TERMINAL PAYXPRESS MOBILE POS TERMINAL OUR ONLINE PAYMENT METHODS ONLINE 499,00 EUR PAY WITH WEBSITE APP INSIDE WECHAT Add WeChat Pay and Alipay as a payment Integrate payments into your Apps Integrate WeChat Pay into your official method in your website easily. -

Notes 12 Bibliography 13

Bringing E-money to the Poor E-money to Bringing Public Disclosure Authorized Public Disclosure Authorized DIRECTIONS IN DEVELOPMENT Finance Riley and Kulathunga Bringing E-money to the Poor Public Disclosure Authorized Successes and Failures Thyra A. Riley and Anoma Kulathunga Public Disclosure Authorized Bringing E-money to the Poor DIRECTIONS IN DEVELOPMENT Finance Bringing E-money to the Poor Successes and Failures Thyra A. Riley and Anoma Kulathunga © 2017 International Bank for Reconstruction and Development / The World Bank 1818 H Street NW, Washington, DC 20433 Telephone: 202-473-1000; Internet: www.worldbank.org Some rights reserved 1 2 3 4 20 19 18 17 This work is a product of the staff of The World Bank with external contributions. The findings, interpreta- tions, and conclusions expressed in this work do not necessarily reflect the views of The World Bank, its Board of Executive Directors, or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries. Nothing herein shall constitute or be considered to be a limitation upon or waiver of the privileges and immunities of The World Bank, all of which are specifically reserved. Rights and Permissions This work is available under the Creative Commons Attribution 3.0 IGO license (CC BY 3.0 IGO) http:// creativecommons.org/licenses/by/3.0/igo. -

Raas Initiating 20210203

BANXA Holdings Inc Initiation of Coverage Providing secure access to digital assets Fintech BANXA Holdings Inc (TSX-V:BNXA) is a global Payments Service Provider (PSP) serving the digital asset/cryptocurrency industry. It does so by using its platform as a 3 February 2021 “bridge” between the fiat/cash/banking system and the digital asset/exchange system. Share detail The company is headquartered in Australia where it has pioneered easy to access, TSX-V Code BNXA local payments platforms for retail investors to acquire cryptocurrencies. More recently it has expanded its infrastructure to the B2B market, partnering with the Share price (1 Feb ’21) C$2.10 leading cryptocurrency exchanges, including OK Group, Binance, KuCoin and EDGE Market Capitalisation C$85.5M Wallet. It has also expanded to the UK, the European Union, USA and Canada. Since Shares on issue 40.7M the launch of its flagship B2B product, BANXA has seen significant growth in Total Net cash post IPO ~$6.0M Payments Volumes (TPV), including 1,000% growth in January 2021 TPV to A$55m. BANXA listed on the Toronto Stock Exchange on January 6, through a reverse merger Free float ~65% with Toronto-listed A-Labs Capital I Corp, with a market capitalisation at listing of Upside Case C$40.7m. We initiate coverage of BANXA with a base case discounted cashflow Scalable business model in high growth sector derived valuation of C$3.47/share, which implies a CAGR of 36% in 10-year free Delivering both online and offline payments cashflows, in a sector that is forecasted to generate >50% CAGR over the same period.