BCSBI NEWS Since the Last Issue of 'Customer Matters'

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Srl No Folio/Client ID Name of the Member to Whom the Amount of Dividend Is Due (To Be Given in Alphabetical Order) Last Known A

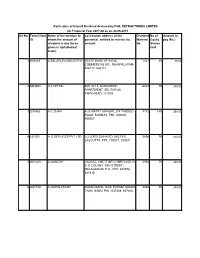

Particulars of Unpaid Dividend declared by IFGL REFRACTORIES LIMITED for Financial Year 2007-08 as on 20.09.2015 Srl No Folio/Client Name of the member to Last known address of the Dividend No of Amount to ID whom the amount of person(s) entitled to receive the Warrant Equity pay (Rs.) dividend is due (to be amount No. Shares given in alphabetical held order) 1 B03445 A BALAGURU MOORTHY STATE BANK OF INDIA, 1421 35 70.00 COMMERCIAL BR., RAJAPALAYAM- 626117, 626117 2 M03408 A C MITTAL 305, GH-8, SARASWATI 6429 70 140.00 APARTMENT, SECTOR-46, FARIDABAD, 121003 3 S01862 A C SHAH 8/23 MATRY MANDIR, 278 TARDEO 9172 140 280.00 ROAD, BOMBAY, PIN : 400007, 400007 4 L01301 A G SERVICES PVT LTD 1/2 LORD SINHA RD 2ND FLR, 5696 70 140.00 CALCUTTA, PIN : 700071, 700071 5 G01203 A GANESH VADIVEL CHETTIAR COMPOUND, N 2934 70 140.00 G O COLONY 6TH STREET, MELAGARAM P.O., PIN : 627818, 627818 6 G01749 A GOPALASAMY INDIAN BANK, RASI PURAM, SALEM 3057 70 140.00 TAMIL NADU, PIN : 637408, 637408 7 C01906 A HUKMI CHAND SUPREME COMPUTER SERVICES, 1933 105 210.00 44 M K TEMPLE ST OPP UBI SRI VITTAL, COMPLEX 1ST FLR B V K IYENGAR RD, BANGALORE PIN : 560053, 560053 8 J03026 A JOY HEMANTH, B M C POST, COCHIN, 4303 35 70.00 PIN : 682021, 682021 9 D03059 A K DHINAKARAN Y-94 2ND FLOOR 8TH STREET, 6TH 2658 70 140.00 MAIN ROAD, ANNA NAGAR CHENNAI, PIN : 600040, 600040 10 S08488 A KUMARA SWAMY HOUSE NO 12-6*48 S U N ROAD, 10344 70 140.00 WARANGAI, A P, PIN : 506002, 506002 11 12348869IN A MALLESHWAR RAO H NO 12-1-118, P V STREET, 14501 5 10.00 300394 WARANGAL, 506002 -

A1076 A2201 Jagjit Singh Sethi Prithvijit Singh Wz-30

A1076 A2201 JAGJIT SINGH SETHI PRITHVIJIT SINGH WZ-30, MEENAKSHI GARDEN, NEAR SUBHASH TOWER 17,FLAT NO.603,SOUTH CLOSER NAGAR MERTRO STATION, NEW DELHI SECTOR-50,GURGOAN Contact: ----- Contact: 9810411980 ----- ----- NEW DELHI - 110018, Delhi GURGAON - 0, Haryana A1190 A2263 M.P. AGARWAL BHUPINDER SINGH 517, BRAHMANIPURA, RAJA RAM AGARWAL HOUSE NO. 22, SECTOR-3, CHANDIGARH- MARG, BEHIND JAIN MANDIR, BAHRAICH - (UP) Contact: ----- Contact: ----- ----- ----- BAHRAICH - 271801, Uttar Pradesh CHANDIGARH - 0, Chandigarh A1564 A2693 SHAMJIT SINGH SODHI MOHD. AFZAL E-352, GREATER KAILASH-II, 2ND FLOOR, NEW M/S KHAIR-UD-DIN SONS & CO., 7- EXTN DELHI- 110048 INDUSTRIAL ESTATE, JAMMU- 180 003 Contact: 9810592921 Contact: 191,2431390,09419141625 ----- ----- GREATER KAILASH-II - 110048, Delhi JAMMU - 180003, Jammu And Kashmir A1603 A3288 DR. ABUL FAZAL SYED KHALID HUSSAIN C/O- DR. A. F. FAIZY DEPTT. OF BIOCHEMISTRY, C-3/7, VASANT VIHAR, NEW DELHI J. N. MEDICAL COLLEGE, AMU, ALIGARH, UP Contact: 09756956133 Contact: ----- ----- ----- ALIGARH - 202002, Uttar Pradesh VASANT VIHAR - 110057, Delhi A2171 A3372 NARENDRA KUMAR MEHTA SATYAPADOO BHATTACHARYA 638,DDA SFS POCKET-I SECTOR22,DWARKA-I D-26/17 NARAD GHAT, VARANASI (U.P) NEW DELHI Contact: 9313573057 Contact: ----- ----- ----- DELHI - 110075, Delhi VARANASI - 0, Uttar Pradesh A3483 A5106 ASHOK KUMAR SINHA RAJIV BHATIA ASHOK MANSION , ANNIE BESANT ROAD, A-4/537,PACHIM VIHAR,NEW DELHI OPP- PATNA COLLEGE, PATNA- 100004 (BIHAR) Contact: ----- Contact: 9871811444 ----- ----- PATNA - 800004, Bihar PASCHIM VIHAR - 110063, Delhi A3655 A5126 H. C. PATHIK MOHD. G. ANSARI RAJA DY. DIR. SPORTS (RETD.) VILL & POST- ROHRU, 4107, MANDI STREET, NEAR PUL DISTT- SHIMLA HILLS, HIMACHAL PRADESH KAMBOH, SAHARANPUR (UP) Contact: ----- Contact: 09358971388 ----- ----- SHIMLA - 171207, Himachal Pradesh SAHARANPUR - 247001, Uttar Pradesh A4147 A5181 S. -

Tedxgriet Report

GOKARAJU RANGARAJU INSTITUTE OF ENGINEERING AND TECHNOLOGY (AUTONOMOUS) 2017 - 2020 REPORT " TEDxGRIET License Approval " 2019 - 2020 TEDxGRIET CORE COMMITTEE ADVISORS TEAM MEMBERS " SPEAKER MANAGEMENT TECH AND VIDEOGRAPHY " INNOVATION AND PUBLICITY " LOGISTICS AND SPONSORSHIP HOST " Team Members BRANCH: CSE ROLL NO. NAME YEAR OF STUDY 16241A05I6 ANAGHA BANDARU FOURTH 16241A05L1 MOUNYA ARUMALLA FOURTH 16241A05J1 BHAVANA DANDU FOURTH 16241A0543 PRAFULLA DEVI BHUPATHI FOURTH RAJU 16241A05N7 VASIKARLA SATYA FOURTH SRI VIRINCHI 16241A05L4 MEHER VISHWANATH FOURTH 17241A0505 RAM SWARUP THIRD 17241A0593 SAI KRISHNA MATTA THIRD 17241A0543 PATLOLLA GNANDEEP THIRD 18241A05H4 THANAY METTA SECOND BRANCH: IT ROLL NO. NAME YEAR OF STUDY 16241A1201 AAKRITI RAJU C. FOURTH 16241A0212 PONUGOTI VENKAT FOURTH BHAVISHYA 17241A12B0 SUGANDHA THIRD PADULLAPARTI 17241A1235 MAHALAKSHMI THIRD MUKKAMALA 17241A12E3 SREETHI MUSUNURU THIRD 17241A1219 GEETHA GHULEKAR THIRD 18241A1256 SINDHU KORUTURI SECOND 18241A1221 HARIKA MANTHENA SECOND 18241A1280 G.MANISH SAI TEJA SECOND " BRANCH: CIVIL ROLL NO. NAME YEAR OF STUDY 17241A01A1 VINAY VARMA THIRD 17241A01A2 R.V. SURAJ THIRD 16241A0101 PAVAN SAI FOURTH BRANCH: MECH ROLL NO. NAME YEAR OF STUDY 17241A0384 VIJAY KIRAN THIRD Freelancers ROLL NO. NAME YEAR OF STUDY 17241A0509 AKSHAY THIRD 16241A01B6 VIJAY VIHAR FOURTH Host ROLL NO. NAME YEAR OF STUDY 18241A0440 PERLI NETHRA SECOND " TEDxGRIET (SEASON 3) Theme The Theme for this season is “Echoes and Reflections”. Our experiences and journeys in different aspects of life help us shape our thoughts. We constantly Reflect upon these thoughts. These reflections help shape our work and lifestyle as Echoes. We believe echoes are the consequences of our reflections.This season, we want to use our platform to share the ideas that shape your minds and the consequences of those ideas. -

April Founded by Prof MMS Ahuja and Prof BB Tripathy in 1972 EXECUTIVE PATRONS 30Th Annual Scientific Meeting of THEME SUBJECTS Prof

RSSDI RSSDIRSSDI NEWSNEWS 2002 • 30 • 2 • April Founded by Prof MMS Ahuja and Prof BB Tripathy in 1972 EXECUTIVE PATRONS 30th Annual Scientific Meeting of THEME SUBJECTS Prof. Sam G.P. MOSES Chennai the Research Society for the Prof. B.B. TRIPATHY Cuttack Study of Diabetes in India Nutrition Section Prof. H.B. CHANDALIA Mumbai International Conference Centre ANTOXIDANTS, DIET Vs. DRUGS Prof. P. GEEVERGHESE Kochi GULFFAR Dr. C. MUNICHOODAPPA Bangalore Scientific Section Kochi, Kerala PRESIDENT Ahuja Symposium: October 11, 12 and 13, 2002 Prof. SIDHARTHA DAS Cuttack PANCREATOPATHY VICE PRESIDENTS Dear Doctor Prof. MURALIDHAR S. RAO Gulbarga Diabetes researchers are invited to collect Prof. R.V. JAYAKUMAR Kottayam It is an honour and privilege to host the relevant data for presenting theme papers 2002 Annual Conference of RSSDI at and for sending research abstracts of oral PAST PRESIDENT Cochin. This conference will give the Prof. V. SESHIAH Chennai or poster presentations to Chairman, opportunity for academic knowledge and Scientific Committee SECRETARY experience sharing with each other and Prof. P.V. RAO Hyderabad the rare opportunity of seeing GOD’S Prof. Ashok K. Das OWN COUNTRY—Kerala. Cochin is Director-Professor-Medicine JOINT SECRETARY Dean Dr. S.V. MADHU New Delhi known as the Queen of Arabian Sea and is well known for its traditional hospitality. Jawaharlal Institute of Post Graduate TREASURER You must avail the full benefit of attending Medical Education and Research Prof. N. SUDHAKAR RAO Hyderabad the conference by planning your pre and Pondicherry 605 006 EXECUTIVE COMMITTEE post conference sight seeing tours well in [email protected] Prof. -

Life Membership List from L01 to L 7091

L01 L08 H. M. PATEL I.C.S. RASIKLAL PHUNDILAL SHAH VALLABH VIDYANAGAR, VIA- ANAND, WEST JIMA PRAKASH ROAD, SHAHADA, DISTT- RAILWAY, GUJARAT DHULIA, MAHARASHTRA+ Contact: ----- Contact: ----- ----- ----- ANAND - 0, Gujrat DHULIA - 0, Maharashtra L03 L09 PRAMUKHLAL M PATEL N.C. SHAH FRIENDS HOME, VEER NARIMAN ROAD, SHAHADA, WEST KHANDESH, MAHARASHTRA MUMBAI- 400001 Contact: ----- Contact: ----- ----- ----- MUMBAI - 400001, Maharashtra WEST KHANDESH - 0, Maharashtra L05 L10 GIRDHAR LAL DAMODARDAS MADAN MOHAN MURAR KA REID ROAD, AHMADABAD, GUJARAT 7, LYONS RANGE P.O. BOX NO. 204 CALCUTA - 700001 Contact: ----- Contact: ----- ----- ----- AHMADABAD - 0, Gujrat CALCUTTA - 0, West Bengal L06 L1000 LAVE GIRDHAR LAL RAMESH NARAIAN MATHUR REID ROAD, AHMADABAD, GUJARAT 45, SUBHAS NAGAR, GANDHI COLONY, MUZAFFAR NAGAR (UP) Contact: ----- Contact: ----- ----- ----- AHMADABAD - 0, Gujrat MUZAFFAR NAGAR - 0, Uttar Pradesh L07 L1001 SHIBA PRASAD BANERJEE CHANAN SINGH RAMGARHIA 44, RAI BAHADUR SATISH, CHANDRA ROAD, PO- 1410/7, RAM NAGAR, LONI ROAD, SHAHDARA HOOGHLY BANDEL, WEST BENGAL- NEW DELHI-110032 Contact: ----- Contact: ----- ----- ----- HOOGLY - 0, West Bengal SHAHDARA - 0, Delhi L1002 L1008 JUTA OBEROI GURDIP SINGH SAHI C/O MADDENS HOTEL DELHI 3035, SECTOR 28-D, CHANDIGARH Contact: ----- Contact: ----- ----- ----- DELHI - 0, Delhi CHANDIGARH - 0, Chandigarh L1004 L1009 HABIB ULLAH KHAN BALRAJ SINGH GREWAL AT & P.O. BUTRAVA. DISTT. MUZAFFARNAGAR BXX-546, OPP. MUNNI LALA ATTA CHAKKI. (UP) GHUMAR MANDI, CIVIL LINES. LUDHIANA Contact: ----- Contact: ----- ----- ----- MUZFFARNAGAR - 0, Uttar Pradesh LUDHIANA - 0, Punjab L1005 L101 ASGHAR ALI KHAN MADHUSUDAN C. PAREKH VILL & P.O. BUTRAVA DISTT. MUZAFFARNAGAR C/O. RAJNAGAR SPG & WVG. MILLS LTD (UP) Contact: ----- Contact: ----- ----- ----- MUZAFFARNAGAR - 0, Uttar Pradesh AHMEDABAD - 0, Gujrat L1006 L1010 RAJ PAL SINGH MANN ASHOK NORONHA B-14, GEETANJALI ENCLAVE , MEHRAULI ROAD, E-1/42- AREA COLONY, S/O SHRI R.P. -

Chandrayaan-2 for Pre-Dawn Launch

c m y k c m y k THE LARGEST CIRCULATED ENGLISH DAILY IN SOUTH INDIA HYDERABAD I SUNDAY I 14 JULY 2019 www.deccanchronicle.com WEATHER PAGE | 13 Max: 34.8OC Min: 23.3OC SUNDAY RH: 80% R’fall: Traces BEING PATRIOTS IN Forecast: CHRONICLE DisCourse Cloudy sky. TIME OF NATIONALISM Rain, thundershowers RUN THE EXTRA MILE: likely. Max/Min 34/23ºC THE VERY POPULAR TRUMP WARNS MIGRANT CRACKDOWN SET TO START >> PG 8 ULTRAMARATHONS ASTROGUIDE Vol. 82 No. 194 Established 1938 | 48 PAGES PLUS A FREE COPY OF 16-PAGE SUNDAY CHRONICLE | `5.00 Vikari; Uttarayana Tithi: Ashada Shuddha TERROR FIGHT ■ Kamal Nath also rushed to Bengaluru Trayodasi till 12.56 am (Monday) Star: Jyeshta till 5.28 pm Varjyam: Nil NIA busts terror module in TN 5 K’taka MLAs move Durmuhurtam: 5.06 pm to 5.58 pm ■ Plan to carry out multiple attacks across India thwarted Rahukalam: 4.30 pm SINDHIYA SAMUEL | DC Indian Penal Code (IPC) to 6 pm CHENNAI, JULY 13 ● Investigations revealed that the and UA (P) Act after NIA SC against Speaker HIJRI CALENDAR accused had planned to wage a war received credible informa- Ziqaad 10,1440 AH The National Investiga- tion that the accused per- DC CORRESPONDENTS tion Agency on Saturday against India and could be in contact sons were conspiring and BENGALURU, JULY 13 PRAYERS carried out raids at multi- with some other terror groups. conducted consequent Fajar: 4.41 am ple locations in Chennai preparations to wage war Posing a fresh challenge to Zohar: 12.31 pm and Nagapattinam and against the government. -

Vol.15 Issue 2 Final.Qxd

SRI PRAKASH NEWSLETTER A Scientific Extra-ordinaire, Our Inspiration - Our Guide Prof. Arvind Gupta , Sri Ch.V.K. Narasimha Rao VOL.: 15 - ISSUE : 2 An Incredible Innovator, A master toymaker NOVEMBER 2016 - JANUARY 2017 True values make happy lives. A happy individual is also a universal Sabah for interacting with the prakashites. I am very thankful to Sri Mathematics, Statistics and Computer Science, Hyderabad and individual who can make difference not only to himself but also to P.Muralidhar Rao,BJP General Secretary for interacting with the chil- Prof.P.V.S Anand for interacting with the children on career. I am the people around. To nurture such individuals who can emerge dren of X std. Iam also thankful to Sri J.Narayana Rao, Director, really thankful to Dr.C.V.Narasimham, Principal, Ramnath successful in any challenging situation is our prime watchword as Global Network, India; Mr.Bruce K.Garg, Mr. William Griffin and Secondary School & Dr.Anand Kumar, Scientist, NSTL for agreeing to we strongly believe that Great men were Children one day and Mr.David Webb for interacting with the children. I also thank Sri conduct the book quiz on ‘The Story of Solar Energy’. I am truly Children can be Great men someday. 3rd International Children's S.G.Srinivas, Prof.P.Srinivas, Dept.of Zoology & Prof S.Pallamsetty, thankful to Dr.K.B.Subramaniam, Rtd. Principal,RIE, Bhopal for Science and Mathematics Festival was grand and eventful owing to Dept. of CSE, A.U. for encouraging children to exercise their imagi- being a part of Ganit Utsav. -

Accountant Allocation Through CGLE-2014

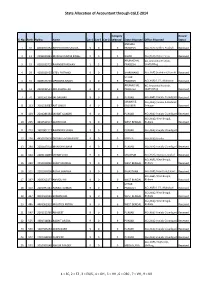

State Allocation of Accountant through CGLE-2014 Category Dossier S. No. Rank Rollno. Name Cat-1 Cat-2 Cat-3 selected State Allocated Office Allocated Status ANDHRA 1 10 8002091052 POTHUGANTI SAILAJA 9 0 9 PRADESH AG (A&E) Andhra Pradesh Received 2 11 3206623845 MANISH KUMAR SINGH 9 0 9 BIHAR AG (A&E), Bihar, Patna Received ARUNACHAL AG, Arunachal Pradesh, 3 19 8201033715 RAVINDER MOHAN 1 3 3 PRADESH (A&E) Wing 4 29 4205028435 JITEN PAITANDI 9 0 9 JHARKHAND AG (A&E) Jharkhand, Ranchi Received UTTAR 5 45 3009543453 UPENDRA SINGH 6 0 9 PRADESH AG (A&E)-I, UP, Allahabad Received ARUNACHAL AG, Arunachal Pradesh, 6 51 2201182531 MD ASHRAF ALI 6 0 9 PRADESH (A&E) Wing Received 7 70 1601561364 JAI GAURAV 9 0 9 PUNJAB AG (A&E) Punjab, Chandigarh Received JAMMU & AG (A&E), Jammu & Kashmir, 8 133 3001530587 AJIT SINGH 9 0 9 KASHMIR Srinagar Received 9 139 2201286164 JAYANT GANDHI 9 0 9 PUNJAB AG (A&E) Punjab, Chandigarh Received AG (A&E), West Bengal, 10 215 4410511517 SANTU DAS 9 0 9 WEST BENGAL Kolkata Received 11 223 1601002117 RAVINDER SINGH 9 0 9 PUNJAB AG (A&E) Punjab, Chandigarh 12 226 4410010616 DIPSIKHA MUKHERJEE 9 0 9 KERALA AG (A&E), Kerala 13 284 2201107014 MANISH KUMAR 9 0 9 PUNJAB AG (A&E) Punjab, Chandigarh Received 14 324 2405110889 JAYANT JAIN 9 0 9 MANIPUR AG (A&E), Manipur, Imphal Received AG (A&E), West Bengal, 15 330 4410010050 SUDIP MANDAL 9 0 9 WEST BENGAL Kolkata Received 16 351 2201354008 RICHA SHARMA 9 0 9 RAJASTHAN AG (A&E), Rajasthan, Jaipur Received AG (A&E), West Bengal, 17 397 3003562177 ANMOL RAI 9 0 9 WEST BENGAL -

Jms Empowered to Take Voice Sample for Probe: SC

Follow us on: RNI No. TELENG/2018/76469 @TheDailyPioneer facebook.com/dailypioneer Established 1864 OPINION 8 HYDERABAD 11 SPORTS 16 Published From HYDERABAD DELHI LUCKNOW BIG CAT’S LEAP NO APOLOGIES! #FREEDOMTOFEED RANKIREDDY-SHETTY BHOPAL RAIPUR CHANDIGARH OF FAITH IS ALL THAT WOMEN ASK FOR ENTER THAI SEMIS RANCHI BHUBANESWAR DEHRADUN VIJAYAWADA *LATE CITY VOL. 1 ISSUE 300 HYDERABAD, SATURDAY AUGUST 3, 2019; PAGES 16 `3 *Air Surcharge Extra if Applicable AN ITALIAN JOB FOR SUDHEER { Page 13 } www.dailypioneer.com JMs empowered to take With levels in projects rising, TS brims with joy voice sample for probe: SC PNS n HYDERABAD PNS n NEW DELHI The Srisailam reservoir is brimming with inflows, bring- In a landmark judgment, the Chandrababu ing cheers to farmers, as Actors' Guru Supreme Court on Friday held Krishna River is gushing that judicial magistrates "must ‘voice’ to be through its course in Devadas be conceded" the power to Telangana owing to uninter- direct a person to give voice tested? rupted inflows from upstream sample to investigating agen- and incessant rains. The multi- Kanakala no cies to effectively further probe he Supreme Court's purpose project nestled amid judgment on Friday that in a case. T lush green Nallamalla forest more judicial magistrates have the It used its plenary power power to direct a person to give has received inflows close to 2 HYDERABAD: Veteran under Article 142 of the voice sample to investigating lakh cusecs in the past 24 actor, director and writer Constitution to fill the void in agencies to effectively further hours and, coupled with rains, Devadas Kanakala passed the Code of Criminal probe could open the Pandora's the Srisailam dam has turned away here on Friday, after Procedure, which until now voice for the purpose of inves- It, however, said none of box. -

Family Planning Association of India (Fpa India) Running

FAMILY PLANNING ASSOCIATION OF INDIA (FPA INDIA) RUNNING FOR A CAUSE SINCE 2017 OUR VISION Established in 1949, All people empowered to enjoy their sexual and reproductive health choices and rights in an India free from stigma and FPA India is a social discrimination. impact organisation OUR MISSION A voluntary commitment to SRHR : ADVOCATE for and ENABLE working towards gender equality and empowerment for all including the poor and vulnerable people, ENSURE information, education and services; empowering communities POWERED by knowledge, innovation and technology, towards sus- tainable development. through rights-based information and services encompassing sexual, OUR VALUES: EXCELLENCE: INCLUSIVENESS: reproductive, maternal, Committed to providing high Belief in serving everyone quality services in every aspect irrespective of their sexuality, adolescent and of its work - IN THE FIELD gender, age, health, social or with complete, comprehensive financial status. Respecting child health care and AT THE OFFICE with the basic right of everyone to efficiency and accountability in chooose how they wish to lead management their life and the choices that they make. Being open, compas- PASSION: sionate and helping everyone in Passionate about making a dif- a stigma free environment. ference to people's lives so that no one is denied their health INTEGRITY: rights. FPA India is determined Dedicated to the cause and with to ensure that each person is the courage and fearlessness to aware of his/her rights, can follow through on our words and access and exercise them at all stay steadyand on course even times. The spirit of volunteer- when times get tough. ism resonates with volunteers and employees that are forever committed and passionate about their work. -

Becoming Indians: Cervantes and García Lorca

Indi@logs Vol 6 2019, pp 179-190, ISSN: 2339-8523 DOI https://doi.org/10.5565/rev/indialogs.124 ------------------------------------------------------------------------------------------------ BECOMING INDIANS: CERVANTES AND GARCÍA LORCA SUBHAS YADAV University of Hyderabad, India [email protected] Received: 28-09-2018 Accepted: 03-01-2019 In the year 1831, during an auction of the previously owned books by Sir William Jones, one of the greatest linguists, famed orientalist and the founder of the Asiatic Society in Calcutta in 1784, the Antwerp version (Spanish) of Don Quixote in two volumes published in 1719 along with Viaje al Parnaso, Persiles y Sigismunda and La Galatea published in Madrid 1784 were also listed for sale.1 One of the first generation Indian Hispanic studies scholars, Shyama Prasad Ganguly also sustains the idea that the first copy of Don Quixote arrives in India with Sir William Jones. Indeed he might have brought it himself. In a letter written to Spanish jurist, writer and philologist Francisco Perez Bayer on 4 Oct, 1774, Jones thanks him for giving him the Spanish translation of Sallust done by El Infante Gabriel de Borbon and acknowledged he had read the humorous stories of Cervantes, along with Poemas Heroicas de Don Alonso y Odas de Garcilaso (Lord Teignmouth, 1806: 129). R. D. Waddilove, one of their friends, happens to hand over Sallust’s translation to Sir William Jones. However, the English version of Don Quixote must have reached India at a later date. It would have become the source text for its first Bengali translation in the year 1887 entitled Adbhut Digvijay, by Bipin Behari Chackrabarti. -

DR. VINAY VARMA Date of Birth

BIO-DATA (Updated March 2013) Name : DR. VINAY VARMA Date of Birth : 25th January, 1950 Present Address : Dr. Vinay Varma, Anand Pain Relief & Rehabilitation Institute, Eureka Colony, Sholapur Road, Keshwapur, Hubli – 580023 Karnataka India Phone No. : +91- 9343401146 (Mobile) +91-836-2283977 (Hospital) Email Id. : [email protected] Website : www.acupuncturehabhub.in Educational Qualifications MBBS (Bachelor of Medicine & Bachelor of Surgery), 1974, . Karnataka Medical College, Hubli. Diploma in Acupuncture, 1980 . Conducted by the International College of Acupuncture, Switzerland in India, for the first time, at Raipur M.D. (TM) By Medicina Alternativa, 1983 . Colombo (Sri Lanka) Professional Registrations Medical Council of Karnataka (KMC): Reg. No. 12812 (permanent) Awards, Honors & Fellowships PGCR (Post Graduate Certificate Course in Rehabilitation) from All India Institute of Physical Medicine & Rehabilitation (AIIPMR), Mumbai. Ph.D. (Medicina Alternativa, Sri Lanka), 1985 for original work in splints Membership of Acupuncture Foundation of Sri Lanka (by Examination). Advanced training in non-surgical management of BACK CARE at Tata Memorial Hospital, Mumbai, organized by India’s First Back School – Ashwini Back Institute, Thane, Mumbai. Family Planning Counselor Course by IMA (A.K.N Sinha Institute), New Delhi. Post Graduate Course in HIV / AIDS & STDs Management by IMA (A.K.N Sinha Institute), New Delhi. Presentations Paper Presentation – ‘Acupuncture in Sinusitis’, 1st National Congress of Acupuncture, Raipur 1979. Participated in the First Third World Congress of Acupuncture held at Colombo 1979. Paper Presentation – ‘Acupuncture Treatment Of Osteo-Arthritis Of Knee Joint’ at the II National Congress of Acupuncture, Belgaum 1980. Participated in VII World Congress of Acupuncture, Colombo 1981. Paper Presentation – ‘Comparative Clinical Observations on The Treatment of Post Polio Paralysis’, World Congress of Holistic Medicine, Colombo Oct 1983.