Huaneng Renewables (958 HK)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

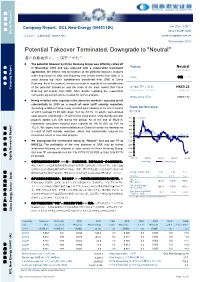

Potential Takeover Terminated, Downgrade to "Neutral" 潜在收购被终止,下调至“中性”

股 票 研 [Table_Title] Company Report: GCL New Energy (00451 HK) Jun Zhu 朱俊杰 究 (852) 2509 7592 Equity Research 公司报告: 协鑫新能源 (00451 HK) [email protected] 19 December 2019 [Table_Summary] Potential Takeover Terminated, Downgrade to "Neutral" 潜在收购被终止,下调至“中性” The potential takeover by China Huaneng Group was officially called off [Table_Rank] 公 in November 2019 and was replaced with a cooperation framework Rating: Neutral Downgraded agreement. We believe that termination of the potential takeover (majority 司 stake acquisition) of GNE and acquiring only certain assets from GNE is to 报 评级: 中性 (下调) avoid having too much indebtedness transferred from GNE to China 告 Huaneng. As of the moment, we are uncertain in regards to the consideration of the potential transaction and the scale of the solar assets that China 6[Table_Price-18m TP 目标价] : HK$0.22 Company Report Huaneng will acquire from GNE. More details regarding the cooperation Revised from 原目标价: HK$0.45 framework agreement will be needed for further analysis. Share price 股价: HK$0.172 Newly installed solar capacity in the domestic market is expected to fall substantially in 2019 as a result of solar tariff subsidy reduction. According to NEA of China, newly installed solar capacity in the first 9 months Stock performance of 2019 reached 15.99 GW, down YoY by 53.7%. In which, concentrated 股价表现 solar projects contributed 7.73 GW of new installations, while distributed solar [Table_QuotePic] 50.0 % of return projects added 8.26 GW during the period. As at the end of 9M2019, 40.0 nationwide cumulative installed solar capacity hit 190.19 GW, up YoY by 30.0 证 15.2%. -

Roadmap for the Demonstration of Carbon Capture and Storage (CCS) in China

Final Report/June 2011 ADB TA‐7286 (PRC) People’s Republic of China Carbon Dioxide Capture and Storage Demonstration – Strategic Analysis and Capacity Strengthening Roadmap for the Demonstration of Carbon Capture and Storage (CCS) in China Final Report June 2011 Final Report /June 2011 ADB TA‐7286 (PRC) People’s Republic of China Carbon Dioxide Capture and Storage Demonstration – Strategic Analysis and Capacity Strengthening Roadmap for the Demonstration of Carbon Capture and Storage (CCS) in China Final Report June 2011 Report submitted by Project Team Prof. J. YAN – Team Leader & CCS Experts Prof. H. JIN – National Co‐leader Prof. Li Z., Dr. J. Hetland, Dr. Teng F., Prof. Jiang K.J., Ms. C. J. Vincent, Dr. A. Minchener, Prof. Zeng RS, Prof. Shen PP, Dr. X. D. Pei, Dr. Wang C., Prof. Hu J, Dr. Zhang JT The views expressed are those of the Consultants and do not necessarily reflect those of the Ministry or the Asian Development Bank (ADB). i Final Report /June 2011 TABLE OF CONTENTS Tables .............................................................................................................................. iv Figures ............................................................................................................................. v Key findings: .................................................................................................................... ix Main Recommendations: ................................................................................................. xi 1. Background and Objectives ....................................................................................... -

Announcement on Replies to the Letter of Enquiry from The

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. (a Sino-foreign joint stock limited company incorporated in the People’s Republic of China) (Stock Code: 902) ANNOUNCEMENT ON REPLIES TO THE LETTER OF ENQUIRY FROM THE SHANGHAI STOCK EXCHANGE Huaneng Power International, Inc. (“the Company”), on 14 April 2020, received a Letter of Enquiry regarding Information Disclosure of 2019 Annual Report of Huaneng Power International, Inc. (Shang Zheng Gong Han [2020] No. 0350) (the “Letter of Enquiry”) from the Shanghai Stock Exchange. Upon receiving the Letter of Enquiry, the Company proactively arranged with relevant parties to carry out diligent research as well as discussion and analysis on the issues raised in the Letter of Enquiry. In accordance with the requirements of the Letter of Enquiry, replies to relevant issues are as follows: I. In relation to Assets Impairment with Significant Amount According to the annual report, the Company accrued significant asset impairment of RMB5.886 billion at the end of the reporting period. To this, please supplement and explain each of the following items: 1. In relation to aggregate impairment amount of RMB3.818 billion for the 10 asset groups, including Huaneng Yushe Power Generation Co., -

Advancing Clean Energy & Sustainable Energy Infrastructure

Advancing Clean Energy & Sustainable Energy Infrastructure through PEER A BRIEF ON CHINA’S ENERGY INITIATIVES MAY 2020 BACKGROUND China’s power sector services 1.1 billion consumers, supplying 6,994 TWh from more than 1.91 TW of installed capacity. Coal is the primary source of electricity generation in China. The total installed capacity of renewable energy (including hydropower) in China is more than 728 GW. At the end of 2018, China’s power sector continued to be dominated by large state-owned companies. Source: China Energy Portal The country’s grid is owned and operated primarily by the state-owned State Grid Corporation of China (which supplies power to 88 percent of the country), while China Southern Grid, also state-owned, accounts for most of the remainder. A handful of large state-owned power generation companies are responsible for generating most electricity, including the so-called “big five” – China Datang Corporation, China Guodian Corporation, China Huadian Group, China Huaneng Group, and China Power Investment Corporation – that account for 47 percent of power capacity. In 2016, the 13th Five-Year Plan targeted 2,000 GW of capacity to be installed by The world’s biggest energy 2020 – a nearly 20 percent increase from consumer is aiming for renewables the current capacity – and a 15 percent to account for at least 35 percent increase in the share of non-fossil fuel of electricity consumption by 2030, energy. Based on this five-year plan, according to a revised draft plan China aims to achieve 6.5 percent annual from the National Development & average growth in their GDP from 2016- Reform Commission (NDRC). -

About CR Power

Electric power generation is our business. "We do everything at our best efforts" is the cornerstone of our business philosophy. Our company mission is to become one of the leading independent power producers ("IPP"s) in the world and the best IPP in China. We are committed to accomplishing this mission. About CR Power China Resources Power Holdings Company Limited (the “Company” or “CR Power”) is a fast-growing independent power producer which invests, develops, operates and manages power plants and coal mine projects in the more affluent regions and regions with abundant coal resources in China. As at 31 December 2009, CR Power has 41 power plants in commercial operation. The total attributable operational generation capacity of the power plants held by the Company is 17,753 MW, with 37% located in Eastern China, 22% located in Southern China, 20% located in Central China, 12% located in Northern China, and 9% located in Northeastern China. Corporate Structure China Resources (Holdings) Company Limited 64.59% China Resources Power Holdings Company Limited Coal-fired Coal-fired Coal-fired Clean Energy (≥600MW) (300MW) (≤200MW) • Changshu • Huaxin • Yixing • Danan Wind • Fuyang • Liyujiang A • Xingning • Shantou Wind • Liyujiang B • Cangzhou • Tangshan • Penglai Wind • Shouyangshan • Dengfeng • Jiaozuo • Chaonan Wind • Changzhou • Gucheng • Luoyang • Dahao Wind • Shazhou • Hubei • Jinzhou • Huilaixian’an Wind • Zhenjiang • Lianyuan • Shenhai Thermal • Honghe Hydro • Yangzhou No. 2 • Caofeidian • Banqiao • Beijing Thermal • Shaojiao C • -

Roshan Power (Private) Limited

..t ROSHAN POWER (PRIVATE) LIMITED The Registrar, Date: February 10, 2014 National Electric Power Regulatory Authority, Ref: RPL/14/I/003 2nd Floor, OPF Building, SeCtor G-5/2, Reg. 50/2010 Islamabad. Dear Sir, APPLICATION FOR A GENERATION LICENSE OF 10 MW SOLAR POWER PROJECT ROSHAN POWER (PRIVATE) LIMITED 1, Rao Mahmud Ilahi, Director Energy projects being the duly Authorized representative of Roshan Power Pvt. Ltd. by virtue of board resolution dated January 28, 2014, hereby apply to the National Electric Power Regulatory Authority (NEPRA) and for the Grant of a Generation License of 10 MW Solar Power Project to Roshan Power (Pvt.) Ltd pursuant to the section 15 of the Regulation of Generation, Transmission and Distribution of Electric Power Act, 1997. I certify that the documents-in-support attached with this application are prepared and submitted in conformity with the provision of National Electric Power Regulatory Authority Licensing (Application and Modification Procedure) Regulations, 1999, and undertake to abide by the terms and provisions of above-said regulations. I further undertake and confirm that the information provided in the attached documents-in-support is true and correct to the best of my knowledge and belief. Two Bank drafts (DD3050621 & DD3050671) in the sum of Rupees 131,632 (One Hundred Thirty One Thousand, Six Hundred & Thirty Two only) being the non-refundable License application fee calculated in accordance with Schedule-II to National Electric Power Regulatory Authority Licensing (Application and Modification Procedure) Regulations, 1999, is • also attached herewith. Best Regards, - R o M. Ilahi Director Energy Projects u-11 Gurumangat Road, Gulberg-III, Lahore, Pakistan. -

Green Energy Powering Life with China Resources Power Holdings Company Limited Holdings Company Power China Resources Sustainable Development Report 2020

Green Energy Green Powering Life with with Life Powering China Resources Power Holdings Company Limited Holdings Company Power China Resources Sustainable Development Report 2020 China Resources Power Holdings Company Limited SUSTAINABLE DEVELOPMENT REPORT 2020 润电力���限�司 This is the 11th annual Sustainable Development Report published by China Resources Power About Holdings Company Limited (“CR Power”) for the year from January 1 to December 31, 2020. the Report Basis of Preparation Scope This Report is prepared with reference to the This Report relates to China Resources Power following important standards: Holdings Company Limited and its affiliates • Environmental, Social and Governance (see Organizational Structure at page 13), Reporting Guide as set forth in Appendix referred to herein as “We,” “the Company,” 27 of the Rules Governing the Listing of or “CR Power.” Securities on the Stock Exchange of Hong Kong Limited issued by the Stock Exchange We have engaged an independent of Hong Kong Limited (“HKEx” ) third party to provide assurance of 16 • Sustainability Reporting Guidelines of the performance indicators in this Report. Global Reporting Initiative (GRI Standards) See pages 4-5 for the Assurance Report. • Guidelines on Corporate Social Responsibility Reporting for Chinese Enterprises (CASS-CSR4.0) – Basic Framework of the Chinese Academy of Social Sciences • Guidelines on Corporate Social Responsibility Reporting for Chinese Enterprises - Power Production Industry (CASS-CSR3.0) • Guidelines to the State-Owned Enterprises Directly -

SINOSING SERVICES PTE. LTD. (A Company Incorporated Under the Laws of Singapore)

NOT FOR DISTRIBUTION IN THE UNITED STATES Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. This announcement is for information purposes only and does not constitute an invitation or a solicitation of an offer to acquire, purchase or subscribe for securities or an invitation to enter into an agreement to do any such things, nor is it calculated to invite any offer to acquire, purchase or subscribe for any securities. This announcement is not an offer of securities for sale in the PRC, Hong Kong and the United States or elsewhere. The Bonds are not available for general subscription in Hong Kong or elsewhere. This announcement is not for distribution, directly or indirectly, in or into the United States (including its territories and possessions, any state of the United States and the District of Columbia). This announcement does not constitute or form a part of an offer to sell or the solicitation of an offer to buy any securities in the United States or any other jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. The securities referred to herein have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”) and may not be offered or sold in the United States absent registration or an applicable exemption from the registration requirements of the Securities Act. -

ENGIE Signed Two Major Agreements in China Press Release

Press release November 2, 2015 ENGIE signed two major agreements in China In presence of the French and Chinese Heads of State, ENGIE signed two major agreements in Beijing this Monday 2nd November 2015, with Chinese energy groups, respectively China Huaneng Group and Beijing Enterprises Group. Both agreements express the ambition of ENGIE to pursue its growth through partnerships and cooperation activities with key Chinese partners, not only in China, but also abroad. Those global agreements consider the entire energy value chain: power, natural gas and energy services, with a specific focus on efficient and innovative solutions able to take on the challenges of energy’s transition to a low-carbon economy. China Huaneng and ENGIE are leading energy companies with a strong base in their respective country, but also expanding abroad and considering each other as partners of business development. Both parties wish to further expand their scope of cooperation including development and investment in the areas of the gas value chain (LNG infrastructures, LNG supply and downstream natural gas industry chain, coal-bed methane), conventional and renewable energy resources, scientific and technological cooperation on advanced power technologies, with a view to cleaner and renewable energy, energy saving and emissions reduction. Beijing Enterprises Group and ENGIE are willing to carry out their historical and trustful cooperation with a view to partner in China, jointly study and develop green supply and efficient management of energy for the 2022 Winter Olympic Games hosted by Beijing and the province of Hebei and energy infrastructures and services to the Beijing - Tianjin - Hebei “capital circle” region. -

EWG 19 13A Anx 2 Confirmed Attendees

No. Name Company Name Title Email Phone Address Gender Role Senior Management & 626 Cochrans Mill Road P.O.Box 10940 1 Scott Smouse US DOE;APEC EGCFE [email protected] Male Speaker Technical Advisor OV 202 5866278 Pittsburgh,PA 15236-0940 Andrew 2 (IEA) Clean Coal Centre General Manager Andrew.Minchener@iea- Park House 14 Northfields London SW18 IDD UK Male Speaker Minchener coal.org 44 20 88776280 5th Floor, Heddon House, 149-151 Regent Street, 3 Benjamin Sporton World Coal Association(London) Acting Chief Executive Male Speaker [email protected] 44 2078510052 London, W1B 4JD, UK 3F Daiwa Nishi-shimbashi Building 3-2-1 Nishi- 4 Keiji Makino Japan coal energy center Professor Male Speaker [email protected] 8 13 64026101 Shimbashi, Minato-ku, Tokyo 105-0003 Japan 1300 West W. T. Harris Blvd, Charlotte, NC 5 Jeffrey N. Phillips EPRI Sr. Program Mgr Male Speaker [email protected] 1 704 9414188 28262, USA 26th Floor FFC No.5 North 3rd Ring Road, 6 Murray Mortson Airbone President m.mortson@airbornecleanen Male Speaker ergy.com 86 13466688305 Chaoyang District, Beijing 26th Floor FFC No.5 North 4rd Ring Road, 7 Michael Zhao Airbone CEO Male Participant [email protected] 86 13910538135 Chaoyang District, Beijing Forest Power & Energy Holdings, 2nd Floor No 7 Building YuquanHuigu No 3 8 Croll Xue Vice-president Male Participant Inc. [email protected] 86 13321156701 Minzhuang Road Haidian District Beijing Forest Power & Energy Holdings, 2nd Floor No 7 Building YuquanHuigu No 3 9 Mingtao Zhu Senior manager Male Participant Inc. [email protected] 86 13901383638 Minzhuang Road Haidian District Beijing 10 Daming Yang CARE-Gen, LLC.(GP Strategies) President Male Speaker [email protected] 86 18515099980 Shijingshan District, Beijing Rm K-M, 7/F, Tower A, The East Gate Plaza, #9 11 Xiaoliang Yang World Resources Institute Research Analyst Male Participant [email protected] 86 18510568512 Dongzhong Street, Beijing, China, 100027 Manager (Energy & Hongkong Electric Centre, 44 Kennedy Road, 12 Mr. -

SPDR® FTSE® Greater China ETF a Sub-Fund of the SPDR® Etfs Stock Code: 3073 Website

SPDR® FTSE® Greater China ETF A Sub-Fund of the SPDR® ETFs Stock Code: 3073 Website: www.spdrs.com.hk/etf/fund/fund_detail_3073_EN.html Interim Report 2021 1st October 2020 to 31st March 2021 SPDR® FTSE® Greater China ETF A Sub-Fund of the SPDR® ETFs Stock Code: 3073 Website: www.spdrs.com.hk/etf/fund/fund_detail_3073_EN.html Interim Report 2021 Contents Page Condensed Statement of Financial Position (Unaudited) 2 Condensed Statement of Comprehensive Income (Unaudited) 3 Condensed Statement of Changes in Equity (Unaudited) 4 Condensed Statement of Cash Flows (Unaudited) 5 Notes to the Unaudited Condensed Financial Statements 6 Investment Portfolio (Unaudited) 10 Statement of Movements in Portfolio Holdings (Unaudited) 41 Derivative Financial Instruments (Unaudited) 42 Performance Record (Unaudited) 42 Administration and Management 43 1 SPDR® FTSE® Greater China ETF a Sub-Fund of the SPDR® ETFs Interim Report 2021 CONDENSED STATEMENT OF FINANCIAL POSITION (UNAUDITED) As at 31st March 2021 31.03.2021 30.09.2020 Notes HK$ HK$ Assets Current assets Investments 1,385,908,557 969,438,426 Derivative financial instruments 54,331 47,229 Amounts due from brokers – 1,529,953 Dividends receivable 994,452 1,771,941 Other receivables 6(i) 122,017 347,255 Margin deposits 104,721 1,032,223 Cash at bank 6(f) 3,100,556 2,423,717 Total Assets 1,390,284,634 976,590,744 Liabilities Current liabilities Derivative financial instruments – 14 Amounts due to brokers – 1,500,560 Audit fee payable 154,612 309,225 Trustee fee payable 6(e) 382,474 270,773 Management fee payable 6(d) 684,377 481,283 Tax provision 156,265 214,282 Total Liabilities 1,377,728 2,776,137 Equity Net assets attributable to unitholders 4 1,388,906,906 973,814,607 The notes on pages 6 to 9 form part of these financial statements. -

Achtergrond Bedrijvenlijst Klimaatlabel

Achtergrond bedrijvenlijst klimaatlabel Olie- en gasbedrijven We kijken naar investeringen in olie- en gasbedrijven die opgenomen zijn in de Carbon Underground ranking. Dit zijn beursgenoteerde bedrijven met de grootste koolstofinhoud in hun bewezen voorraden – die dus het sterkst bijdragen aan klimaatverandering bij ontginning van de voorraden waarop ze rekenen. Zie http://fossilfreeindexes.Com Anadarko Petroleum Antero Resources Apache ARC Resources BASF Bashneft BHP Billiton Birchcliff Energy BP Cabot Oil & Gas California Resources Canadian Natural Resources Cenovus Energy Centrica Chesapeake Energy Chevron China Petroleum & Chemical Corp Cimarex Energy CNOOC Concho Resources ConocoPhillips CONSOL Energy Continental Resources Crescent Point Energy Denbury Resources Det Norske Devon Energy DNO International Ecopetrol Encana Energen ENI EOG Resources EP Energy EQT ExxonMobil Freeport-McMoRan Galp Energia Gazprom GDF SUEZ Great Eastern Gulfport Energy Hess Husky Energy Imperial Oil Inpex JX Holdings KazMunaiGas EP Linn Energy Lukoil Lundin Petroleum Maersk Marathon Oil MEG Energy Memorial Resource Mitsui MOL Murphy Oil National Fuel Gas Newfield Exploration Noble Energy Novatek Oando Energy Occidental Oil India Oil Search OMV ONGC - Oil & Natural Gas Corp Ltd (India) Painted Pony Petroleum PDC Energy Petrobras PetroChina Peyto E&D Pioneer Natural Resources Polish Oil & Gas (Polskie Gornictwo, Gazownictwo) PTT QEP Resources Range Resources Repsol Rosneft Royal Dutch Shell SandRidge Energy Santos Sasol Seven Generations Energy SK Innovation