Liberum Research Suite

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

COVERAGE LIST GEO Group, Inc

UNITED STATES: REIT/REOC cont’d. UNITED STATES: REIT/REOC cont’d. UNITED STATES: NON-TRADED REITS cont’d. COVERAGE LIST GEO Group, Inc. GEO Sabra Health Care REIT, Inc. SBRA KBS Strategic Opportunity REIT, Inc. Getty Realty Corp. GTY Saul Centers, Inc. BFS Landmark Apartment Trust, Inc. Gladstone Commercial Corporation GOOD Select Income REIT SIR Lightstone Value Plus Real Estate Investment Trust II, Inc. Gladstone Land Corporation LAND Senior Housing Properties Trust SNH Lightstone Value Plus Real Estate Investment Trust III, Inc. WINTER 2015/2016 • DEVELOPED & EMERGING MARKETS Global Healthcare REIT, Inc. GBCS Seritage Growth Properties SRG Lightstone Value Plus Real Estate Investment Trust, Inc. Global Net Lease, Inc. GNL Silver Bay Realty Trust Corp. SBY Moody National REIT I, Inc. Government Properties Income Trust GOV Simon Property Group, Inc. SPG Moody National REIT II, Inc. EUROPE | AFRICA | ASIA-PACIFIC | MIDDLE EAST | SOUTH AMERICA | NORTH AMERICA Gramercy Property Trust Inc. GPT SL Green Realty Corp. SLG MVP REIT, Inc. Gyrodyne, LLC GYRO SoTHERLY Hotels Inc. SOHO NetREIT, Inc. HCP, Inc. HCP Sovran Self Storage, Inc. SSS NorthStar Healthcare Income, Inc. UNITED KINGDOM cont’d. Healthcare Realty Trust Incorporated HR Spirit Realty Capital, Inc. SRC O’Donnell Strategic Industrial REIT, Inc. EUROPE Healthcare Trust of America, Inc. HTA St. Joe Company JOE Phillips Edison Grocery Center REIT I, Inc. GREECE: Athens Stock Exchange (ATH) AFI Development Plc AFRB Hersha Hospitality Trust HT STAG Industrial, Inc. STAG Phillips Edison Grocery Center REIT II, Inc. AUSTRIA: Vienna Stock Exchange (WBO) Babis Vovos International Construction S.A. VOVOS Alpha Pyrenees Trust Limited ALPH Highwoods Properties, Inc. -

Marten & Co / Quoted Data Word Template

Monthly roundup | Real estate August 2020 Kindly sponsored by Aberdeen Standard Investments Winners and losers in July Best performing companies in price terms in July Worst performing companies in price terms in July (%) (%) AEW UK REIT 18.9 Hammerson (20.0) UK Commercial Property REIT 14.9 Countryside Properties (14.4) Schroder REIT 14.5 U and I Group (14.0) Empiric Student Property 11.4 Real Estate Investors (13.4) Palace Capital 10.6 Tritax EuroBox (11.8) LondonMetric Property 9.7 St Modwen Properties (10.9) Triple Point Social Housing REIT 9.2 Drum Income Plus REIT (10.0) RDI REIT 8.5 Alternative Income REIT (8.4) SEGRO 8.3 Panther Securities (8.2) CLS Holdings 5.5 BMO Commercial Property Trust (7.1) Source: Bloomberg, Marten & Co Source: Bloomberg, Marten & Co. AEW UK REIT share price YTD A number of REITs Hammerson share price YTD Retail landlord and property Hammerson continued 110 companies saw big 300 to see its share price 95 255 share price gains 210 fall during July and has 80 over the month of 165 now lost 79.2% of its 120 65 July as covid-19 value in the year to 75 50 restrictions started to 30 date – the worst in the Dec Jan Feb Mar Apr May Jun Jul ease across the UK Dec Jan Feb Mar Apr May Jun Jul real estate sector. The Source: Bloomberg, Marten & Co and greater Source: Bloomberg, Marten & Co company, which owns economic stimulus shopping centres, retail was revealed. The biggest mover was AEW UK REIT. -

FTSE Factsheet

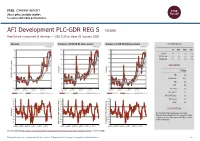

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Data as at: 30 January 2020 AFI Development PLC-GDR REG S TICKER Real Estate Investment & Services — USD 0.36 at close 30 January 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 30-Jan-2020 30-Jan-2020 30-Jan-2020 0.4 150 160 1D WTD MTD YTD Absolute -1.6 -5.3 -6.3 -6.3 140 150 Rel.Sector -1.4 -3.8 -5.7 -5.7 0.35 140 Rel.Market -0.4 -2.8 -4.2 -4.2 130 130 120 0.3 VALUATION 120 110 110 Trailing RelativePrice 0.25 RelativePrice 100 100 PE 6.3 Absolute(localPrice currency) 90 EV/EBITDA 11.6 90 0.2 PB 0.2 80 80 PCF 5.8 0.15 70 70 Div Yield 0.0 Jan-2019 Apr-2019 Jul-2019 Oct-2019 Jan-2019 Apr-2019 Jul-2019 Oct-2019 Jan-2019 Apr-2019 Jul-2019 Oct-2019 Price/Sales 1.2 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.7 100 100 100 Div Payout 0.0 90 90 90 ROE 4.1 80 80 80 70 70 Index) Share 70 Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 The Company's main activities are real estate 40 40 40 RSI RSI (Absolute) development and investment. -

November 2020

November 2020 Monthly roundup | Real estate Kindly sponsored by Aberdeen Standard Investments Winners and losers in October Best performing funds in price terms Worst performing funds in price terms (%) (%) NewRiver REIT 28.7 Panther Securities (28.6) Schroder European REIT 27.4 Raven Property Group (20.3) Helical 15.1 Grit Real Estate Income Group (11.5) Workspace Group 14.6 Empiric Student Property (11.5) Standard Life Inv. Property Income 14.1 Ground Rents Income Fund (10.2) Alternative Income REIT 12.2 Secure Income REIT (9.4) CEIBA Investments 9.3 PRS REIT (9.3) BMO Real Estate Investments 7.8 GCP Student Living (9.2) Inland Homes 6.8 Sigma Capital Group (7.8) Real Estate Investors 6.3 Alpha Real Trust (7.2) Source: Bloomberg, Marten & Co Source: Bloomberg, Marten & Co kjjjj October finished with the threat of a second lockdown The heaviest share price faller in October – Panther looming over the UK as COVID-19 cases continued to rise. Securities – is very illiquid so its share price can be However, this did not dampen demand for shares in some distorted with one big transaction. Of the rest, Grit Real of the companies that have already been battered during Estate Income saw a double-digit fall in its share price after the pandemic, even before news of a potential vaccine reporting a big drop in NAV. Student accommodation breakthrough broke in early November. Successful sales specialists Empiric Student Property and GCP Student of retail assets by NewRiver REIT saw its share price Living both continue to be impacted by COVID-19, with bounce 28.7% in the month to top the table. -

Schroder UK Mid Cap Fund Plc Unaudited Portfolio Holdings at 31St July 2020

Schroder UK Mid Cap Fund plc Unaudited portfolio holdings at 31st July 2020 The investments listed below have been valued on a fair value basis using closing bid prices. Market Nominal value Investment SEDOL ISIN holding £ 4Imprint Group Ord GBP0.385 664097 GB0006640972 105,000 2,493,750 A G Barr Ord GBP0.04167 B6XZKY7 GB00B6XZKY75 700,000 2,999,500 Anglo Pacific Group Ord GBP0.02 644936 GB0006449366 2,050,000 2,423,100 Bodycote PLC Ord GBP0.173 B3FLWH9 GB00B3FLWH99 800,000 4,504,000 Brewin Dolphin Ord GBP0.01 176581 GB0001765816 1,610,000 4,218,200 Cairn Energy Ord GBP0.0136686 B74CDH8 GB00B74CDH82 2,300,000 2,748,500 Capita Plc B23K0M2 GB00B23K0M20 2,700,000 924,210 CLS Holdings Plc Ord GBP0.025 BF04459 GB00BF044593 1,749,950 3,415,902 Computacenter Plc Ord 0.075555 BV9FP30 GB00BV9FP302 300,000 5,943,000 Cranswick Ord GBP0.10 231888 GB0002318888 114,000 4,078,920 Crest Nicholson Holdings Ltd Ord GBP0.05 B8VZXT9 GB00B8VZXT93 800,000 1,496,000 Dechra Pharmaceuticals Ord GBP0.01 963318 GB0009633180 143,310 4,087,201 Diploma Ord GBP0.05 182663 GB0001826634 320,000 5,801,600 Dunelm Group GBP.01 B1CKQ73 GB00B1CKQ739 790,000 9,709,100 Fisher (James) Ord GBP0.25 339500 GB0003395000 266,000 3,037,720 Future PLC Ord GBP0.15 BYZN904 GB00BYZN9041 212,000 2,925,600 Games Workshop Ord GBP0.05 371847 GB0003718474 80,000 7,024,000 Gamesys Group Plc Ord NPV BZ14BX5 GB00BZ14BX56 132,072 1,226,949 Genus Ord GBP0.10 207458 GB0002074580 80,000 2,716,800 Grafton Group New Units B00MZ44 IE00B00MZ448 530,000 3,407,900 Grainger Ord GBP0.05 B04V127 GB00B04V1276 -

FTSE Russell Publications

2 FTSE Russell Publications 19 August 2021 FTSE 250 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Infrastructure 0.43 UNITED Bytes Technology Group 0.23 UNITED Edinburgh Investment Trust 0.25 UNITED KINGDOM KINGDOM KINGDOM 4imprint Group 0.18 UNITED C&C Group 0.23 UNITED Edinburgh Worldwide Inv Tst 0.35 UNITED KINGDOM KINGDOM KINGDOM 888 Holdings 0.25 UNITED Cairn Energy 0.17 UNITED Electrocomponents 1.18 UNITED KINGDOM KINGDOM KINGDOM Aberforth Smaller Companies Tst 0.33 UNITED Caledonia Investments 0.25 UNITED Elementis 0.21 UNITED KINGDOM KINGDOM KINGDOM Aggreko 0.51 UNITED Capita 0.15 UNITED Energean 0.21 UNITED KINGDOM KINGDOM KINGDOM Airtel Africa 0.19 UNITED Capital & Counties Properties 0.29 UNITED Essentra 0.23 UNITED KINGDOM KINGDOM KINGDOM AJ Bell 0.31 UNITED Carnival 0.54 UNITED Euromoney Institutional Investor 0.26 UNITED KINGDOM KINGDOM KINGDOM Alliance Trust 0.77 UNITED Centamin 0.27 UNITED European Opportunities Trust 0.19 UNITED KINGDOM KINGDOM KINGDOM Allianz Technology Trust 0.31 UNITED Centrica 0.74 UNITED F&C Investment Trust 1.1 UNITED KINGDOM KINGDOM KINGDOM AO World 0.18 UNITED Chemring Group 0.2 UNITED FDM Group Holdings 0.21 UNITED KINGDOM KINGDOM KINGDOM Apax Global Alpha 0.17 UNITED Chrysalis Investments 0.33 UNITED Ferrexpo 0.3 UNITED KINGDOM KINGDOM KINGDOM Ascential 0.4 UNITED Cineworld Group 0.19 UNITED Fidelity China Special Situations 0.35 UNITED KINGDOM KINGDOM KINGDOM Ashmore -

CLS Holdings Plc Annual Report and Accounts 2020

CLS Holdings plc Annual Report and Accounts 2020 Well placed for the future Our business CLS is a London-based FTSE 250 office investment Through our business model, we seek to be company with a £2.2 billion portfolio of 97 properties a responsible business by employing sustainable comprising 6.4m sq. ft (over 597,000 sqm) in the long-term thinking with the environment in mind. UK, Germany and France. We provide workspaces As well as benefiting our own business and shareholders, for over 740 tenants including leading blue-chip this supports other key stakeholders like our tenants companies and government bodies. in their efforts to reduce their environmental impacts and achieve their sustainability objectives. We actively manage our portfolio with in-house teams across all functions of the business. This allows us to engage with our tenants to build long-term relationships and develop a detailed understanding of their needs. It also allows us to embed sustainable behaviours throughout the business which support and drive our progress towards our commitments. Who we are and what we believe Statutory and alternative performance measures Throughout the strategic report we use a range of financial and non-financial measures to assess our performance. The majority of those are European Public Real Estate Association (EPRA) measures. EPRA is a recognised body in the property industry which is involved in the formulation of accounting metrics and sustainability reporting, which give the European listed real estate sector greater transparency and consistency. These standards also provide visibility and comparability to industry stakeholders in addition to being appreciated by the investment community. -

INVITATION BERENBERG Is Delighted to Invite You to Its

INVITATION BERENBERG is delighted to invite you to its UK CORPORATE CONFERENCE 2019 on Wednesday 27th – Thursday 28th March 2019 at The Grove Chandler’s Cross • Watford • Hertfordshire • WD3 4TG • United Kingdom LIST OF ATTENDING COMPANIES BY SECTOR (SUBJECT TO CHANGE) Business Services Consumer Financials Alpha Financial Markets Consulting plc Applegreen plc Ashmore Group plc BBA Aviation plc Compass Group plc Burford Capital Ltd Big Yellow Group plc Cranswick plc Legal & General Group plc Clipper Logistics plc Dalata Hotel Group plc Lloyds Banking Group plc CLS Holdings plc DFS Furniture plc London Stock Exchange plc Green REIT plc Greggs plc Provident Financial plc Hibernia REIT plc Hollywood Bowl Group plc Schroders plc HomeServe plc IG Design Group plc St. James’s Place plc International Consolidated Airlines Group SA Inchcape plc Intertek Group plc On The Beach Group plc John Menzies plc PPHE Hotel Group Ltd Marlowe plc TUI Group RWS Holdings plc Whitbread plc Safestore Holdings plc WM Morrison plc Sirius Real Estate Ltd Staffline Group plc Healthcare Materials TMT Abcam plc Anglo Pacific Group plc Ascential plc Clinigen Group plc BAE Systems plc BT Group plc Dechra Pharmaceuticals PLC Bodycote plc Computacenter plc GlaxoSmithKline plc BP plc Craneware plc Huntsworth plc Cairn Energy plc Daily Mail & General Trust plc IP Group Plc Central Asia Metals plc GB Group plc NMC Health plc Centrica plc GVC Holdings plc Smith & Nephew plc Ceres Power Holdings plc JPJ Group plc (formerly Jackpotjoy) Spire Healthcare Group plc Coats Group plc -

201009 September Property Roundup

October 2020 Monthly roundup | Real estate Kindly sponsored by Aberdeen Standard Investments Winners and losers in September Best performing funds in price terms Worst performing funds in price terms (%) (%) Sigma Capital Group 34.2 Capital & Regional (46.3) Panther Securities 19.5 Hammerson (26.3) Macau Property Opportunities 9.4 BMO Real Estate Investments (24.1) CLS Holdings 8.6 U and I Group (18.5) Phoenix Spree Deutschland 7.2 NewRiver REIT (17.1) Schroder REIT 6.6 Hibernia REIT (14.8) Yew Grove REIT 6.2 Alternative Income REIT (14.6) Helical 3.9 Regional REIT (14.4) RDI REIT 3.5 Capital & Counties (13.5) Custodian REIT 2.9 Grit Real Estate (13.3) Source: Bloomberg, Marten & Co Source: Bloomberg, Marten & Co kjjjj There was an eclectic mix of property companies to feature It is no surprise that once again it was shopping centre in the top price movers for September. Top of the tree was owners Capital & Regional and Hammerson that topped private rented sector and residential development the chart of worst performing property companies in specialist Sigma Capital Group, with a 34.2% rise. The September. Capital & Regional published results at the group launched a £1bn joint venture with EQT Real Estate, beginning of the month in which it posted a 36.6% fall in the real estate platform of global investment firm EQT, to net asset value (NAV) in just six months. Meanwhile, deliver 3,000 private rental homes in Greater London. Hammerson completed a rights issue and share Micro-cap investor Panther Securities also hit double-digit consolidation plan during September, as well as gains, while Macau Property Opportunities saw an uplift in announcing a new chief executive. -

United Kingdom Small Company Portfolio-Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings Are Subject to Change

United Kingdom Small Company Portfolio-Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. This fund operates as a feeder fund in a master-feeder structure and the holdings listed below are the investment holdings of the corresponding master fund. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of use in the Legal Notices. -

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance CLS Holdings CLI Real Estate Investment and Services Development — GBP 2.4 at close 18 June 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 18-Jun-2021 18-Jun-2021 18-Jun-2021 2.6 110 115 1D WTD MTD YTD Absolute -0.8 -4.0 -2.8 6.9 2.5 Rel.Sector -0.4 -4.1 -5.9 -2.2 110 Rel.Market 0.9 -2.4 -2.5 -1.9 2.4 105 2.3 105 VALUATION 2.2 100 Trailing Relative Price Relative Relative Price Relative 100 2.1 PE 13.0 Absolute Price (local currency) (local Price Absolute 2 95 EV/EBITDA 27.2 95 PB 0.8 1.9 PCF 28.5 1.8 90 90 Div Yield 3.1 Jun-2020 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Jun-2020 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Jun-2020 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Price/Sales 6.7 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.8 100 90 80 Div Payout 39.8 90 80 70 ROE 6.3 80 70 60 Share Index) Share Share Sector) Share - 70 - 60 50 DESCRIPTION 60 50 40 50 The Company invests in commercial property. The 40 30 RSI RSI (Absolute) 40 Company maintains a portfolio of buildings, investing 30 20 mainly in offices which are then let on long leases to 30 tenants.