Domestic Carbon Standards in Europe

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Carbon Dioxide Removal Policy in the Making: Assessing Developments in 9 OECD Cases

POLICY AND PRACTICE REVIEWS published: 04 March 2021 doi: 10.3389/fclim.2021.638805 Carbon Dioxide Removal Policy in the Making: Assessing Developments in 9 OECD Cases Felix Schenuit 1,2*, Rebecca Colvin 3, Mathias Fridahl 4, Barry McMullin 5, Andy Reisinger 6, Daniel L. Sanchez 7, Stephen M. Smith 8, Asbjørn Torvanger 9, Anita Wreford 10 and Oliver Geden 2 1 Center for Sustainable Society Research, University of Hamburg, Hamburg, Germany, 2 German Institute for International and Security Affairs (SWP), Berlin, Germany, 3 Crawford School of Public Policy, Australian National University, Canberra, ACT, Australia, 4 Department of Thematic Studies, Environmental Change, Centre for Climate Science and Policy Research, Linköping University, Linköping, Sweden, 5 Dublin City University, Dublin, Ireland, 6 Ministry for the Environment, Wellington, New Zealand, 7 Department of Environmental Science, Policy, and Management (ESPM), University of California, Berkeley, Berkeley, CA, United States, 8 Smith School of Enterprise and the Environment, Oxford University, Oxford, United Kingdom, 9 Center for International Climate Research (CICERO), Oslo, Norway, 10 Agribusiness and Economics Research Unit (AERU), Lincoln University, Christchurch, New Zealand Edited by: William C. Burns, Since the adoption of the Paris Agreement in 2015, spurred by the 2018 IPCC Special American University, United States Report on Global Warming of 1.5◦C, net zero emission targets have emerged as a Reviewed by: new organizing principle of climate policy. In this context, climate policymakers and Phillip Williamson, University of East Anglia, stakeholders have been shifting their attention to carbon dioxide removal (CDR) as United Kingdom an inevitable component of net zero targets. The importance of CDR would increase Charithea Charalambous, Heriot-Watt University, further if countries and other entities set net-negative emissions targets. -

Carbon Innovation for Business Impact

Carbon Innovation for Business Impact Accelerating climate solutions and private sector finance to make real change possible Contents Executive summary ............................................................................................. 3 Introduction ........................................................................................................... 4 Advancing practical and scalable solutions ................................................ 6 Evaluating carbon finance projects ............................................................... 8 Proven methodologies ................................................................................ 9 Emerging methodologies .........................................................................13 High-potential technologies ...................................................................15 Experimental technologies .....................................................................16 Adding value with values.................................................................................17 Delivering quality carbon credits .................................................................19 Ensuring credible standards ..........................................................................20 Conclusion ............................................................................................................22 Teak Afforestation, Mexico Cover Photo: SELCO Solar Energy Access, India 2 Executive summary Since the Paris Agreement was existing and new methodologies to signed -

Greenhouse Gas Removal (GGR) Policy Options – Final Report

Greenhouse Gas Removal (GGR) policy options – Final Report Report prepared for BEIS Final June 2019 Greenhouse Gas Removal (GGR) policy options – Final Report Contents Executive Summary ........................................................................................................................... 4 Introduction ....................................................................................................................................... 7 1 Scale and cost of future Greenhouse Gas Removal ........................................................................... 9 2 The need for a policy portfolio to support GGRs ............................................................................. 17 3 Review of current GGR policies ....................................................................................................... 22 4 Policy pathways to support GGR ..................................................................................................... 25 5 Enabling and integrating policies ..................................................................................................... 41 6 Frequently Asked Questions ............................................................................................................ 50 7 References ....................................................................................................................................... 52 8 Appendix: Assessment of direct policies ........................................................................................ -

England Tree Strategy Erattum

Department for Environment, Food and Rural Affairs England Tree Strategy Consultation - Technical Annex June 2020 Erattum 17th August 2020: The estimate of vacant land on page 11 has been updated to replace an error and explain the source of the estimate on page 12 of the consultation document. Contents Erattum ................................................................................................................................ 1 General background, ............................................................................................................ 1 Expanding and connecting our woods ................................................................................. 3 Ambition ........................................................................................................................... 4 Creating space for nature ................................................................................................. 5 Planting trees for water .................................................................................................... 6 Helping landowners create woodlands ............................................................................. 8 Working together to create landscape scale change ...................................................... 10 Restoring degraded land ................................................................................................ 11 Funding future woodland creation – markets for ecosystem services such as carbon ... 12 Supplying the trees we need to plant and -

WWC V2.0 08March2018.Pdf

Woodland Carbon Code Requirements for voluntary carbon sequestration projects ® Version 2.0 March 2018 © Crown Copyright 2018 You may re-use this information (not Contents including logos) free of charge in any format or medium, under the terms of the Open Government Licence. To view this licence, visit: www.nationalarchives.gov.uk/doc/ open-government-licence or write to the Information Policy Team, The National Introduction 1 Archives, Kew, London, TW9 4DU or e-mail: [email protected] 1. Eligibility 4 Version 2.0 published March 2018 1.1 Key project dates 4 1.2 Eligible activities 5 ISBN 978-0-85538-843-0 1.3 Eligible land 5 FCMS017/FC-GB(KA)/0K/MAR2018 1.4 Compliance with the law 6 Enquiries relating to this publication should 1.5 Conformance to the UK Forestry Standard 6 be sent to: 1.6 Additionality 7 [email protected] 2. Project governance 8 2.1 Commitment of landowners and project/group managers 8 2.2 Management plan 9 2.3 Management of risks and permanence 10 2.4 Consultation 11 2.5 Monitoring 11 2.6 Registry and avoidance of double counting 12 2.7 Carbon statements and reporting 13 3. Carbon sequestration 14 3.1 Carbon baseline 14 3.2 Carbon leakage 15 3.3 Project carbon sequestration 15 3.4 Net carbon sequestration 16 4. Environmental quality 17 5. Social responsibility 18 Glossary 19 O2 CO2 C C Introduction Background and purpose Application Process Trees and forests can mitigate climate change through Registration sequestering carbon. Woodland creation therefore All projects should be registered on the UK Woodland provides an attractive option for companies, organisations Carbon Registry within two years of the start of planting. -

STATE of EUROPEAN MARKETS 2017 Voluntary Carbon

STATE OF EUROPEAN MARKETS 2017 Voluntary Carbon MAIN PARTNER PROMOTED BY ABOUT FOREST TRENDS’ ECOSYSTEM MARKETPLACE Ecosystem Marketplace, an initiative of the non-profit organisation Forest Trends, is the leading global source of information on environmental finance, markets, and payments for ecosystem services. As a web-based service, Ecosystem Marketplace publishes newsletters, breaking news, original feature articles, and annual reports about market-based approaches to valuing and financing ecosystem services. We believe that transparency is a hallmark of robust markets and that by providing accessible and trustworthy information on prices, regulation, science, and other market-relevant issues, we can contribute to market growth, catalyse new thinking, and spur the development of new markets, and the policies and infrastructure needed to support them. Ecosystem Marketplace is financially supported by a diverse set of organisations including multilateral and bilateral government agencies, private foundations, and corporations involved in banking, investment, and various ecosystem services. Forest Trends works to conserve forests and other ecosystems through the creation and wide adoption of a broad range of environmental finance, markets and other payment and incentive mechanisms. Forest Trends does so by 1) providing transparent information on ecosystem values, finance, and markets through knowledge acquisition, analysis, and dissemination; 2) convening diverse coalitions, partners, and communities of practice to promote environmental -

Ecosystem Marketplace

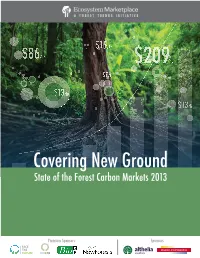

$15 /ha $86/ha $209/ha $7/ha $13/ha $13/ha Covering New Ground State of the Forest Carbon Markets 2013 Premium Sponsors Sponsors About Forest Trendsʼ Ecosystem Marketplace Ecosystem Marketplace, an initiative of the non-profi t organization Forest Trends, is a leading source of information on environmental markets and payments for ecosystem services. Our publicly available information sources include annual reports, quantitative market tracking, weekly articles, daily news, and news briefs designed for different payments for ecosystem services stakeholders. We believe that by providing solid and trustworthy information on prices, regulation, science, and other market-relevant issues, we can help payments for ecosystem services and incentives for reducing pollution become a fundamental part of our economic and environmental systems, helping make the priceless valuable. Ecosystem Marketplace is fi nancially supported by organizations such as the Skoll Foundation, the Swiss Agency for Development and Cooperation, the International Climate Initiative (Germany), the Gesellschaft für Internationale Zusammenarbeit/Federal Ministry of Economic Cooperation and Development (Germany), the Gordon and Betty Moore Foundation, PROFOR (the World Bank’s Program on Forests), as well as sponsors and supporters of this report. Forest Trends is a Washington, DC-based international non-profi t organization whose mission is to maintain, restore, and enhance forests and connected natural ecosystems, which provide life-sustaining processes, by promoting incentives stemming from a broad range of ecosystem services and products. Specifi cally, Forest Trends seeks to catalyze the development of integrated carbon, water, and biodiversity incentives that deliver real conservation outcomes and benefi ts to local communities and other stewards of our natural resources. -

Forestry for a Low-Carbon Future

177 177 FAO FORESTRY PAPER Forestry for a low-carbon future Forestry for a low-carbon future Forestry for a low-carbon future Integrating forests and wood products Integrating forests and wood products in climate change strategies in climate change strategie s Forests are critical to mitigation, having a dual role; they function globally as a net carbon sink but are also responsible for about 10 to 12 percent of global emissions. Forests and forest products offer both – developed and developing countries a wide range of Integrating forests and wood products in climate change strategies options for timely and cost-effective mitigation. Afforestation/reforestation offers the best option because of its short timescale and ease of implementation. Reducing deforestation, forest management and forest restoration also offer good mitigation potential, especially because of the possibility for immediate action. Yet forest contributions to mitigation also go beyond forest activities. Wood products and wood energy can replace fossil-intense products in other sectors, creating a virtuous cycle towards low-carbon economies. The mitigation potential and costs of the various options differ greatly by activity, region, system boundaries and time horizon. Policymakers must decide on the optimal mix of options, adapted to local circumstances, for meeting national climate change and development goals. This publication assesses the options and highlights the enabling conditions, opportunities and potential bottlenecks to be considered in making apt choices. -

Woodland Carbon Code Requirements for Voluntary Carbon Sequestration Schemes Woodland Carbon Code

Woodland Carbon Code Requirements for voluntary carbon sequestration schemes Woodland Carbon Code The Woodland Carbon Code is a voluntary code designed to encourage a consistent approach to Woodland Creation Projects involving carbon statements & claims. forestry.gov.uk/carboncode Outline • Rationale & Objectives • How it works • Certification • Progress • What next ? forestry.gov.uk/carboncode Rationale • Woodland creation is an attractive & cost-effective means of climate change mitigation • Increasing interest in using woodlands to capture carbon • Previously no clear standards, consistency or clarity in UK carbon projects • Investors are cautious and seek quality assurance forestry.gov.uk/carboncode Objectives Offer clarity Encourage a and consistent transparency to Provide rigorous approach to customers carbon measurement woodland carbon projects protocols Construct a Reassure the framework that market and may support a compliance market investors about for woodland voluntary carbon credits in woodland carbon the future projects forestry.gov.uk/carboncode How it works 1 The Code enables voluntary woodland carbon projects to demonstrate best practice and to create/sell/report verified Woodland Carbon Units Under the Kyoto Protocol, the UK govt doesn’t currently allow compliance market ‘offsets’ to be generated by UK based projects e.g. for use under the EU ETS or CRC. New UK GHG reporting guidelines now allow companies to report voluntary woodland carbon units but only from WCC certified projects forestry.gov.uk/carboncode How it -

Forest Carbon Asia Brief No.4

Forest Carbon Asia Brief No.4 Policy Updates April 2011 to January 2012 Rise and spread of national and sub-national forest carbon schemes Unna Chokkalingam and S. Anuradha Vanniarachchy International climate change negotiations at COP17 in Durban, December 2011 saw further developments on the proposed REDD+ mechanism to reduce forest-based emissions and enhance forest carbon sinks. A binding international REDD+ agreement and a larger climate change agreement will likely be many years in the making. In the meantime, countries and states or provinces within countries have initiated their own forest-related emission reduction and offsetting schemes within the last year. Developed countries and states with emission reduction targets such as Australia, California (USA), Quebec (Canada), UK, Japan and South Korea are allowing domestic polluters to use forest carbon offsets, and are setting up domestic forest carbon offsetting standards and/or supporting forest offset projects in developing countries. Developing countries like China, India and Ecuador are launching their own forest carbon sequestration or protection programs independent of or in advance of agreement on a REDD+ mechanism under the UNFCCC. This brief provides an update on national and international REDD+ and other forest carbon policies from April 2011 to January 2012. Please see FCA Brief No. 2 for an earlier global policy review up to March 2011. International Schemes and Proposals A brief respite for the Kyoto Protocol The international climate change agreement, the Kyoto Protocol set emissions reduction (ER) targets for more than 30 developed countries during the first commitment period 2008-12. It included specific forest-related mitigation activities for different groups of countries. -

Responding to the Climate Emergency with New Trees and Woodlands

Responding to the climate emergency with new trees and woodlands A guide to help local authorities and landowning businesses achieve net zero Contents Focus of woodland creation 3 So why choose trees? 3 Using woodland creation to reach net zero emissions by 2050 4 Using woodland creation in development plans to contribute to net zero 7 Creating woodland through natural colonisation 7 Reduce the use of non-renewable resources with wood and timber products 8 Managing woodland is good for carbon too! 8 In summary…what can you do to help? 9 Sources of further information on grant funding 10 Woodland creation and plastic tree guards 11 Aiming to achieve net zero emissions Focus of woodland creation The UK’s climate is changing. Even with very ambitious actions to reduce greenhouse gas emissions globally, some further climate change is inevitable up to at least 2050. The Committee on Climate Change (CCC) has recommended that the UK Government adopt a net zero greenhouse gas (GHG) emissions target for 2050 and on the 27th June 2019, the UK Parliament amended the Climate Change Act (2008)1 to include a commitment to net zero emissions by 2050. The UK Parliament and a growing number of local councils and some businesses have declared climate change emergencies and committed to achieving net zero targets over varying timeframes. Trees, woodlands and forests play a key role in greenhouse gas removal. The CCC has recommended that we should be aiming to plant around 30,000 hectares of new woodland in the UK every year until 2050. That is nearly a million hectares over the next 30 years. -

The UK Woodland Carbon Code

The UK Woodland Carbon Code LES ENJEUX DE LA CERTIFICATION CARBONE AGRICOLE ET FORESTIERE EN EUROPE Espace Génération Climat, Paris Le Bourget 10 December 2015 Dr. Pat Snowdon Forestry Commission Edinburgh, UK UK forestry context Policy - finance for woodland Research creation sound science new business models & mechanisms • Forestry • payments for ecosystem services Commission • financial instruments commissioned an • new business models assessment of • valuing & accounting for natural the role of trees capital and forests (2009) Business new outlooks & motivations “Instead of measuring the destruction of nature as a economic gain, we need to address its stewardship as an economic opportunity” (Aldersgate Group) State of voluntary carbon markets Value transacted by project type Objectives • Ensure high standards in UK forest carbon market • Clarity and transparency to bolster market confidence • Rigorous scientific basis • increase private investment in woodland creation • similar principles to VCS, GS… forestry.gov.uk/carboncode Governance iema Institute of Environmental Management & Assessment WCC Advisory Board UKWAS UK Woodland Assurance Standard WCC Executive Board forestry.gov.uk/carboncode Development 2007 - 2011 Design 2010 -2011 Pilot Launch Woodland July 2011 Carbon Code Launch group 2013 certification Launch carbon 2013 registry @ Markit Units available for 2014 sale Still developing… forestry.gov.uk/carboncode UK as of 30 June 2015: • 204 Projects registered • 15,400 ha woodland • 5.7 MtCO2 over lifetime • 101 projects validated