An Investigation of the Relationship Between Financial

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bank Bic Namibia Holdings Limited (Registration

BANK BIC NAMIBIA HOLDINGS LIMITED (REGISTRATION NUMBER : 2015/0371) CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019 BANK BIC NAMIBIA HOLDINGS LIMITED REGISTRATION NUMBER : 2015/0371 ANNUAL FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019 (Amounts expressed in Namibia Dollar (N$), unless otherwise indicated) CONTENTS Page DIRECTORS' RESPONSIBILTY FOR THE FINANCIAL REPORTING 2-3 DIRECTORS' APPROVAL OF THE FINANCIAL STATEMENTS 3 AUDITORS' REPORT 4-6 DIRECTORS' REPORT 7-8 CONSOLIDATED BALANCE SHEET 9 CONSOLIDATED STATEMENT OF PROFIT AND LOSS AND OTHER COMPREHENSIVE INCOME 10 CONSOLIDATED STATEMENT OF CHANGES IN EQUITY 11 CONSOLIDATED STATEMENT OF CASH FLOWS (REGISTRATION NUMBER :2015/0371) 12 NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 13-40 ANNEXURE A: RISK REPORT 41-46 Page 1 BANK BIC NAMIBIA HOLDINGS LIMITED REGISTRATION NUMBER : 2015/0371 ANNUAL FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019 (Amounts expressed in Namibia Dollar (N$), unless otherwise indicated) DIRECTORS' REPORT REGISTRATION NUMBER 2015/0371 COUNTRY OF INCORPORATION Republic of Namibia NATURE OF BUSINESS Bank BIC Namibia Holdings Limited is a Holding company with no operating activity, all costs being incurred from an auditing and secretarial nature. The consolidated financial statements are, in general, those of Bank BIC Namibia Limited, that started its operations on 20 June 2016. COMPANY INFORMATION Bank BIC Namibia Holdings Limited was incorporated in Namibia on 27 April 2015 with registration number 2015/0371. SUBSIDIARIES As at 31 December 2019, Bank BIC Namibia Holdings Ltd had the following directly held subsidiaries: Name of subsidiary Type of business Issued share capital Proportion held Bank BIC Namibia Ltd Commercial bank 421.000.000 95% FINANCIAL RESULTS FOR THE YEAR The results and financial position of the Company and Group for the year ended 31 December 2019 are fully disclosed in the financial statements set out on pages 9 to 46. -

Memorandum N° 190/2014 | 08/10/2014

1 MEMORANDUM N° 190/2014 | 08/10/2014 The EBCAM’s Memoranda are issued with the sole purpose to provide daily basic business and economic information on Africa, to the 4,000 European Companies affiliated with our Members, as well as their business parties in Africa. Should a reader require a copy of the Memoranda, please address the request to the respective National Member. See list of National Members at www.ebcam.org. 2013 – 40 Years devoted to reinforce Europe – Africa Business and Development SUMMARY Ebola Crisis: EU organises airlift operation to West Africa Page 2 Frontex Joint Operation 'Triton' – Concerted efforts to manage migration in the Central Mediterranean Page 3 Angola expected to produce 2 million barrels of oil per day in 2017 Page 4 Africa’s richest woman to expand banking empire to Namibia Page 4 Mozambique is Africa’s third largest charcoal producer Page 5 Zambia considers simpler tax for miners as VAT row simmers Page 5 Unused land reverts to the state in Mozambique Page 6 Tanzania: Regional Power Project Planned Page 6 Metals of Africa conducts aerial prospecting in Mozambique Page 7 Rolling stock firm to expand in Africa Page 8 Portuguese-speaking African countries owe Portugal US$3.508 billion Page 8 EU, Malawi discuss €600m non-budgetary support Page 8 Government of Mozambique launches tender to grant new oil blocks Page 9 Local banks join power plant deal in Ghana Page 9 China is main buyer of Angolan products in 1st half Page 10 Libya: EU condemns growing violence in Benghazi Page 10 EBCAM news – NABC – Netherlands Africa Business Council – Africa Works! Page 11 EBCAM news - business Council for Africa West & Southern Page 11 European Business Council for Africa and the Mediterranean The European Private Sector Organisation for Africa’s Development 2 EBOLA CRISIS: EU ORGANISES AIRLIFT OPERATION TO WEST AFRICA The European Union is scaling up its response to the Ebola disease in West Africa with an airlift operation to the affected countries. -

2016 Bank Bic Namibia Annual Management Report

2016 MANAGEMENT REPORT An Overview of Annual Performance Dr. Agostinho Neto Road, Unit 6 (+264) 83 330 9000 [email protected] P.O. Box 5001 - Auspannplatz Windhoek, Namibia www.bankbic.na 0 INTRODUCTION After obtaining the final approval and the respective license from the Central Bank of Namibia in May 2016, Bank BIC Namibia commenced operations in June 2016. 1 CONTENTS I. FINANCIAL HIGHLIGHTS ................................................................................................................................... 3 II. MESSAGE FROM THE CHAIRMAN .................................................................................................................. 4 III. DIRECTORS RESPONSIBILITY FOR THE FINANCIAL REPORTING ...................................................... 6 IV. AUDITORS’ REPORT .................................................................................... Error! Bookmark not defined. V. DIRECTORS’ REPORT....................................................................................................................................... 10 VI. HISTORY .............................................................................................................................................................. 13 VII. ORGANIZATIONAL STRUCTURE .................................................................................................................. 15 VIII. HUMAN RESOURCES ...................................................................................................................................... -

The Monetary Sector Objectives

UNIT 3 THE MONETARY SECTOR OBJECTIVES • Define money and explain the requirements of money • Describe the functions of money • Discuss the functions of a central bank and commercial banks • Describe the money creation process • Explain how the supply of money and the demand for money are determined • Explain the instruments of monetary policy DEFINITION OF MONEY • Money is any generally acceptable or accepted medium of exchange that is accepted in the payment of debts, and/or for goods and services rendered. DEFINITION OF MONEY • Gold and silver were once used as money, but today money consists primarily of paper notes, coins made of various metals and cheque account deposits. • Each country has its own system of money. – In Namibia we use the Namibian dollar, – South Africa uses the rand and – Botswana uses the pula. We call the money in use in a country its currency. BARTER ECONOMIES • Barter is the direct exchange of one good for another without using money as medium of exchange. • If people want to trade, there has to be a double coincidence of wants. • This means there is a need to find a match between what each of the two traders wants to obtain and what each wants to offer in exchange. • Barter system is not efficient and is time consuming process and not suitable for a modern economy where a wide range of goods and services are produced. What is money than? REQUIREMENTS OF MONEY Objects that we can use as money should meet the following requirements: – General acceptability: It should be desired and accepted by all as medium of exchange. -

Consideration of Funding Proposals – Addendum IX Funding Proposal Package for FP090

Meeting of the Board 1– 4 July 2018 GCF/B.20/10/Add. 09 Songdo, Incheon, Republic of Korea Provisional Agenda Item 17 8 June 2018 Consideration of funding proposals – Addendum IX Funding proposal package for FP090 Summary This addendum contains the following three parts: a) A funding proposal summary titled “DBSA Climate Finance Facility” submitted by the Development Bank of Southern Africa; b) No-objection letters issued by the national designated authorities or focal points; and c) Environmental and social report(s) disclosure; These documents are presented as submitted by the accredited entity and the national designated authority(ies) or focal point(s), respectively. Pursuant to the Comprehensive Information Disclosure Policy of the Fund, the funding proposal titled “DBSA Climate Finance Facility” submitted by the Development Bank of Southern Africa is being circulated on a limited distribution basis only to Board Members and Alternate Board Members to ensure confidentiality of certain proprietary, legally privileged or commercially sensitive information of the entity. GCF/B.20/10/Add. 09 Page b Table of Contents Funding proposal submitted by the accredited entity 1 No-objection letters issued by the national designated authorities or focal points 115 Environmental and social report(s) disclosure 120 ■ Project/Programme Title: DBSA Climate Finance Facility South Africa & Southern Africa Development Community Country/Region: (SADC) Region Accredited Entity: Development Bank of Southern Africa Date of Submission: March 29, 2018 Contents Section A PROJECT / PROGRAMME SUMMARY Section B FINANCING / COST INFORMATION Section C DETAILED PROJECT / PROGRAMME DESCRIPTION Section D RATIONALE FOR GCF INVOLVEMENT Section E EXPECTED PERFORMANCE AGAINST INVESTMENT CRITERIA Section F APPRAISAL SUMMARY Section G RISK ASSESSMENT AND MANAGEMENT Section H RESULTS MONITORING AND REPORTING Section I ANNEXES Note to accredited entities on the use of the funding proposal template • Sections A, B, D, E and H of the funding proposal require detailed inputs from the accredited entity. -

Factors Influencing Customer Perceptions on Adoption of Internet

FACTORS INFLUENCING CUSTOMER PERCEPTIONS ON ADOPTION OF INTERNET BANKING IN NAMIBIA A THESIS SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION OF THE UNIVERSITY OF NAMIBIA BY NAMAKAU MUYUNDA SICHONE STUDENT NUMBER - 201154544 MAY 2017 SUPERVISOR: DR. SRINIVAS MADISHETTI PROFESSOR SCHOOL OF BUSINESS MZUMBE UNIVERSITY MZUMBE TANZANIA DECLARATION “This thesis is my own original work and has not been submitted elsewhere in fulfilment of the requirements of this or any other award” Signature:………………………………………. Date:…………………………………………….. i DEDICATION I dedicate this research work to my supervisor who did all he could to guide me throughout the entire research, to my husband and family for the continuous love and support in everything, my friends for encouragements and most of all to the Almighty God who gives power, strength and health while doing the research. ii Table of Contents CHAPTER 1 .............................................................................................................................. 1 INTRODUCTION ..................................................................................................................... 1 1.1 Background ................................................................................................................ 1 1.2 Statement of the problem ........................................................................................... 4 1.3 Research objectives ................................................................................................... -

ICIJ- Luanda Leaks

ICIJ companyCompany # name Former companyDate name of CompanyJurisdiction name change (MM/DD/YYYY)IdS bought stake?IdS (Y/N) created? (Y/N)Incorporation dateDissolution (MM/DD/YYYY) date Stake(MM/DD/YYYY) start date (MM/DD/YYYY)Stake exit date (MM/DD/YYYY)Shares held by IdS orGroup SD? (Galp/NOS/EFACEC/others)Industry Level 1 Industry(=ICB Industry) Level 2 (=ICB sector) 1 Allinmotion Holdings N/ALimited N/A Belize N Y 10/07/2013 Still active 10/07/2013 N/A Isabel dos Santos Financials Investment Banking and Brokerage Services 2 Gleaming InvestmentsSantoro Limited International Holding10/06/2015 LimitedBritish Virgin IslandsN Y 09/12/2013 Unknown 09/12/2013 N/A Isabel dos Santos TelecommunicationsTelecommunications Service Providers 3 Sillery Investments Ltd.N/A N/A British Virgin IslandsN Y 09/12/2013 Unknown 09/12/2013 N/A Isabel dos Santos TelecommunicationsTelecommunications Service Providers 4 De Grisogono SA N/A N/A Switzerland Y N 12/12/1995 Still active 02/27/2012 N/A Sindika Dokolo Consumer DiscretionaryPersonal Goods 5 De Grisogono Italia SrlN/A N/A Italy Y N 02/05/2003 Still active 02/27/2012 N/A Sindika Dokolo Consumer DiscretionaryPersonal Goods 6 de Grisogono U.K. LimitedN/A N/A United Kingdom Y N 11/26/1997 Still active 02/27/2012 N/A Sindika Dokolo Consumer DiscretionaryPersonal Goods 7 De Grisogono U.S.A.N/A Inc. N/A New York Y N 11/29/2000 Still active 02/27/2012 N/A Sindika Dokolo Consumer DiscretionaryPersonal Goods 8 De Grisogono HoldingN/A S.A. -

DBSA Climate Finance Facility

FP098: DBSA Climate Finance Facility South Africa & Southern Africa Development Community (SADC) Region | Development Bank of Southern Africa (DBSA) | Decision B.21/34 28 November 2018 ■ Project/Programme Title: DBSA Climate Finance Facility South Africa & Southern Africa Development Community Country/Region: (SADC) Region Accredited Entity: Development Bank of Southern Africa Date of Submission: March 29, 2018 Contents Section A PROJECT / PROGRAMME SUMMARY Section B FINANCING / COST INFORMATION Section C DETAILED PROJECT / PROGRAMME DESCRIPTION Section D RATIONALE FOR GCF INVOLVEMENT Section E EXPECTED PERFORMANCE AGAINST INVESTMENT CRITERIA Section F APPRAISAL SUMMARY Section G RISK ASSESSMENT AND MANAGEMENT Section H RESULTS MONITORING AND REPORTING Section I ANNEXES Note to accredited entities on the use of the funding proposal template • Sections A, B, D, E and H of the funding proposal require detailed inputs from the accredited entity. For all other sections, including the Appraisal Summary in section F, accredited entities have discretion in how they wish to present the information. Accredited entities can either directly incorporate information into this proposal, or provide summary information in the proposal with cross-reference to other project documents such as project appraisal document. • The total number of pages for the funding proposal (excluding annexes) is expected not to exceed 50. Please submit the completed form to: [email protected] Please use the following name convention for the file name: “[FP]-[Agency -

General Information Manual – “The Fine Print”

General Information Manual – “The Fine Print” This General Information Manual sets out the policies and procedures that agents, should follow during the quoting and booking process. INTRODUCTION The General Information Manual is a source of information and a supporting document that must be read and referred to in conjunction with the nett Rate Sheets, quotations, booking processes and all other Ongava documentation. Should you have any further queries, require additional information or explanation at any stage, please do not hesitate to contact your Reservations Consultant. Whilst the pandemic remains official Ongava hospitality services will operate in Safe Mode. Please familiarise yourself with the Safe Mode separate Terms & Conditions. Please contact [email protected] for further information. RESERVATIONS OFFICE Company Name ONGAVA (PTY) LTD (Company Registration Number 91 / 358) (VAT Number 0520823-01-5) CONTACT DETAILS 102A Nelson Mandela Avenue | Klein Windhoek Private Bag 12041 | Suite No. 10 | Ausspannplatz | Namibia 9000 Office: +264 (0) 83 330 3920 Reservations email - [email protected] Website - www.ongava.com Ongava offices are open from 08:00 to 17:00 on weekdays should you have any queries. RESERVATIONS HOW TO MAKE A RESERVATION When making the initial enquiry, please provide us with the following minimum information, in order for us to respond efficiently and accurately in creating a booking that will best suit the guests’ requirements: • Name of party • Number of persons in the party and ages of children for a family booking 2 • Accommodation requirements – Lodge, number of twin and/or single rooms • If a guide/pilot is travelling with the guests, please specify if they are looking for a single guide room or a guide bed • Rate basis (DBB or FI) • Dates of travel and whether flexible (Arrival, departure and length of stay) • Any other additional information (e.g. -

2018 CAHF Yearbook.Qxp Layout 1

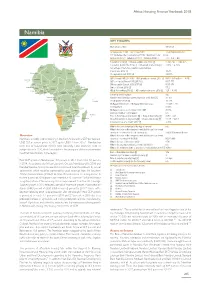

Africa Housing Finance Yearbook 2018 Namibia KEY FIGURES Main urban centres Windhoek Exchange rate: 1 US$ = [a] 23 Aug 2018 13.40 Namibian Dollar PPP Exchange rate (Local currency/PPP$) 1 Namibian Dollar = [b] 6.6 Inflation 2016 [b] | Inflation 2017 [c] | Inflation 2018 [c] 7.0 | 6.2 | 4.0 Population 2016 [d] | Urban population size 2016 [d] 2 280 716 | 1 068 625 Population growth rate 2016 [d] | Urbanisation rate 2016 [d] 1.90% | 4.25% Percentage of the total population below National Poverty Line 2016 [d] 10.7% Unemployment rate 2016 [d] 34.00% GDP (Current US$) 2017 [d] | GDP growth rate annual 2017 [d] US$13 159 million | -8.8% GDP per capita (Current US$) 2017 [d] US$5 555 GNI per capita (Current US$) 2017 [d] US$5 474 Gini co-efficient 2016 [d] 57.2 HDI global ranking 2016 [e] | HD country index score 2016 [e] 125 | 0.340 Is there a deeds registry? Yes Number of residential properties that have a title deed [d] 92 161 Lending interest rate [f] 10.12% Mortgage interest rate | Mortgage term (years) [g] 11.50% | 20 Downpayment 0.00% Mortgage book as a percentage of the GDP 2.10% Estimated number of mortgages n/a Price to Rent Ratio in City Centre [h] | Outside City Centre [h] 8.95 | 9.81 Gross Rental Yield in City Centre [h] | Outside City Centre [h] 11.17 | 10.19 Construction as a % of GDP 2017 [d] 2.90% What is the cost of standard 50kg bag of cement? n/a What is the price of the cheapest, newly built house by a formal developer or contractor? (Local currency) [i] 280 000 Namibian Dollars Overview What is the price of the cheapest, newly -

Towards Responsible Lending in Namibian Consumer Credit Law: a Comparative Investigation

TOWARDS RESPONSIBLE LENDING IN NAMIBIAN CONSUMER CREDIT LAW: A COMPARATIVE INVESTIGATION By NDATEGA VICTORIA ASHEELA submitted in accordance with the requirements for the degree DOCTOR LEGUM in the FACULTY OF LAW UNIVERSITY OF PRETORIA SUPERVISOR: PROF DR S RENKE CO-SUPERVISOR: PROF DR M ROESTOFF NOVEMBER 2017 ACKNOWLEDGEMENTS I gratefully acknowledge the following people for their assistance and support in the process of writing this thesis. Genuine appreciation goes to my supervisors, Professor Stéfan Renke and Professor Melanie Roestoff, for their unwavering support and guidance in all the stages of producing this work. They have believed in me from day one and have made the road very comfortable for me, both academically and on a personal level. Be blessed more abundantly. I am very grateful to Ms. Nicola Howell of the Queensland University of Technology, Professor Gail Pearson of the University of Sydney and Professor Jeannie Paterson of the University of Melbourne Law School for their assistance in retrieving research material in Australia and for their willingness to share with me their work in the field. I am indebted to Ms. Howell for agreeing to read through my draft Australian chapter and for offering many useful suggestions. I gratefully acknowledge the University of Pretoria for granting me a bursary to pursue this degree. I am also thankful to my employer, the University of Namibia, for granting me a year of staff development leave to complete this degree. I am grateful to Dr Kenneth Ferdie Mundia, my former lecturer and colleague, for his continuous support. Thank you for encouraging me to embark on this important project. -

Banking in Africa: Delivering on Financial Inclusion, Supporting Stability

Banking in Africa: Delivering on Financial Inclusion, Supporting Stability EUROPEAN INVESTMENT BANK Banking in Africa: Delivering on Financial Inclusion, Supporting Financial Stability years Banking in Africa: Delivering on Financial Inclusion, Supporting Financial Stability October 2018 Banking in Africa: Delivering on Financial Inclusion, Supporting Financial Stability About the Report At its fourth edition, this report provides an analysis of recent development in the African banking sectors and specific structural topics of relevance. It combines in house research with contribution from leading market experts from commercial banks operating in the region, IFIs and other institutions. About the Economics Department of the EIB The mission of the EIB Economics Department is to provide economic analyses and studies to support the Bank in its operations and in the definition of its positioning, strategy and policy. The Department, a team of 30 economists, is headed by Debora Revoltella, Director of Economics. Main Contributors to This Year’s Report Economic Editor: Jean-Philippe Stijns, under the lead of Barbara Marchitto, Head of the Country & Financial Sector Analysis Division, and Debora Revoltella, Director of the Economics Department Introduction - Jean-Philippe Stijns Chapter 1 - Sub-Saharan African Banking Sectors: Results from a Survey of Banking Groups: Jean- Philippe Stijns and Adeline Pelletier. Chapter 2 - Banking Sector Trends in West Africa: Claudio Cali, Emmanouil Davradakis, Nina Fenton and Amine El Kourchi Chapter 3 - The