Proposed Regulation of the Office of Economic Development Within the Office of the Governor

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Non-Exhaustive Crew Titles That Will Be Considered for Funding

List of non-exhaustive crew titles that will be considered for funding: Director Best boy (lighting) Key make-up artist Producer Lighting technician / Electrics Special make-up effects Artist Line producer Grips (SFX makeup) Production assistant Key grip Make-up supervisor Production managements Best boy/Best Babe (grip) Make-up artist Production manager Dolly grip Key hair Assistant production Production sound Hair stylist manager Production sound mixer Special effects Unit manager Boom operator Special effects supervisor Production coordinator Second assistant sound Stunts First assistant director Art department Stunt coordinator Second assistant director Production designer Film editor Accounting Art director Editorial[edit] Production accountant Line Standby art director Negative cutter Producer Assistant art director Colorist Location manager Set designer Telecine colorist Assistant location manager Illustrator Visual effects[edit] Location scout Graphic artist Visual effects Unit publicist Set decorator Visual effects producer System administrator Buyer Visual effects creative Continuity Leadman director Script supervisor Set dresser Visual effects supervisor Script Writers Greensman Visual effects editor Casting Construction Compositor Casting director Construction coordinator Matte painter Cast PA Head carpenter Sound and music Drivers Carpenters Sound designer Camera and lighting Studio hands Dialogue editor Director of photography Propmaker Sound editor Camera Scenic Re-recording mixer Camera operator Key scenic Music supervisor First assistant camera Property Foley artist Second assistant camera Propmaster Conductor/ orchestrator Film loader Weapons master Score recorder/ mixer Digital imaging technician Costume department Music preparation Steadicam operator Costume supervisor Music editor Motion control Key costumer Previs technician/Operator Breakdown artist Animation Lighting Costume buyer Gaffer Cutter . -

Glossary of Filmmaker Terms

Above the Line Clapboard Generally the portion of a film's budget that covers A small black or white board with a hinged stick on the costs associated with major creative talent: the top that displays identifying information for each shot stars, the director, the producer(s) and the writer(s). in the movie. Assists with organizing shots during (See also Below the Line) editing process; the clap of the stick allows easier Art Director synchronization of sound and video within each shot. The crew member responsible for the design, look Construction Coordinator and feel of a film's set. Includes props, furniture, sets, Also known as the construction manager, this person etc. Reports to the production designer. supervises and manages the physical construction of Assistant Director (A.D.) sets and reports to the art director and production Carries out the director’s instructions and runs the set. designer. The first A.D. is responsible for preparing the Dailies production schedule and script breakdown, making The rough shots viewed immediately after shooting sure shooting stays on schedule and on budget. The each day by the director, along with the second A.D. is responsible for distributing information cinematographer or editor. Used to help ensure and cast notifications, keeping track of hours worked proper coverage and the quality of the shots gathered. by cast and crew, management of extras, signing Director actors in and out and preparing call sheets. The The person in charge of the overall cinematic vision of second A.D. is also in charge of the production the film and the performance of the actors. -

Almost an Angel Tail Credits

Cast of Characters Terry Dean Paul Hogan Steve Elias Koteas Rose Garner Linda Kozlowski Mrs Garner Doreen Lang Father Douglas Seale Irene Bealeman Ruth Warshawsky George Bealeman Parley Baer Sergeant Freebody Michael Alldredge Detective Bill David Alan Grier Teller Larry Miller Bubba Travis Venable Guido Robert Sutton Reverend Barton Ben Slack Tom the Guard Troy Curvey, Jr, Young Guard Trainee Eddie Frias Thug Peter Mark Vasquez Thug’s Crony Lyle J. Omori Prisoner #1 Joseph Walton 2nd Male Teller Steven Brill Uniformed Cop Richard Grove Mother Susie Duff Small Boy Justin Murphy Driver (Van) Greg Barnett Doctor Ray Reinhardt Young Nurse Laurie Souza Pop Hank Worden Bank Customer #1 Vickilyn Reynolds Bank Customer #2 Shawn Schepps Bank Teller Candi Milo Hood Nervo at Bank Randy Vasquez Hood Driver at Bank Mike Runyard Wino in Lane Tony Veneto Man with “T” Shirt Doug Ford Homeless Man Charles David Richards Bonzo Burger Server Brian Frank Female TV Reporter Linda Kurimoto Diner Waitress Stephanie Hodge Moses Bros. Truck Driver Bob Minor Paradise Bar Bartender Leslie Morris Man at Bar Don G. Ross Paradise Bar Local Hal Landon, Jr. Paradise Bar Pool Player Steph Duvall Small Town Older Hood William DeAcutis Small Town Younger Hood Sean Faro Boxing Boy Christian Benz Belnavis Girl Jeri Windom Boy #1 E’Lon Boy #2 Jason Marsden Boy #3 Bert David DeFrancis Boy #4 Anthony Trujillo Terry’s Hit Truck Driver Peter Stader Paramedic Joey LeMond Special Appearance by Joe Dallesandro as Bank Hood Leader Stunt Players Noon Orsatti Jack Gill Ernie Orsatti James Halty Rawn Hutchinson Andy Gill Gene LaBelle Ronnie Rondell Mike DeLuna Chris Nielsen R. -

The Grip Book

THE GRIP BOOK FOURTH EDITION 01-FM-K81291.indd i 9/4/09 11:15:20 AM 01-FM-K81291.indd ii 9/4/09 11:15:20 AM The Grip Book FOURTH EDITION Michael G. Uva AMSTERDAM • BOSTON • HEIDELBERG • LONDON NEW YORK • OXFORD • PARIS • SAN DIEGO SAN FRANCISCO • SINGAPORE • SYDNEY • TOKYO Focal Press is an imprint of Elsevier 01-FM-K81291.indd iii 9/4/09 11:15:20 AM Focal Press is an imprint of Elsevier 30 Corporate Drive, Suite 400, Burlington, MA 01803, USA Linacre House, Jordan Hill, Oxford OX2 8DP, UK Copyright © 2010 Elsevier Inc. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or any information storage and retrieval system, without permission in writing from the publisher. Details on how to seek permission, further information about the Publisher’s permissions policies and our arrangements with organizations such as the Copyright Clearance Center and the Copyright Licensing Agency, can be found at our website: www.elsevier.com/permissions. This book and the individual contributions contained in it are protected under copyright by the Publisher (other than as may be noted herein). Notices Knowledge and best practice in this fi eld are constantly changing. As new research and experience broaden our understanding, changes in research methods, professional practices, or medical treatment may become necessary. Practitioners and researchers must always rely on their own experience and knowledge in evaluating and using any information, methods, compounds, or experiments described herein. In using such information or methods they should be mindful of their own safety and the safety of others, including parties for whom they have a professional responsibility. -

DOCUMENT RESUME CE 056 758 Central Florida Film Production Technology Training Program. Curriculum. Universal Studios Florida, O

DOCUMENT RESUME ED 326 663 CE 056 758 TITLE Central Florida Film Production Technology Training Program. Curriculum. INSTITUTION Universal Studios Florida, Orlando.; Valencia Community Coll., Orlando, Fla. SPONS AGENCY Office of Vocational and Adult Education (ED), Washington, DC. PUB DATE 90 CONTRACT V199A90113 NOTE 182p.; For a related final report, see CE 056 759. PUB TYPE Guides - Classroom Use - Teaching Guides (For Teacher) (052) EDRS PRICE MF01/PC08 Plus PoQtage. DESCRIPTORS Associate Degrees, Career Choice; *College Programs; Community Colleges; Cooperative Programs; Course Content; Curriculun; *Entry Workers; Film Industry; Film Production; *Film Production Specialists; Films; Institutional Cooperation; *Job Skills; *Occupational Information; On the Job Training; Photographic Equipment; *School TAisiness Relationship; Technical Education; Two Year Colleges IDENTIFIERS *Valencia Community College FL ABSTRACT The Central Florida Film Production Technology Training program provided training to prepare 134 persons for employment in the motion picture industry. Students were trained in stagecraft, sound, set construction, camera/editing, and post production. The project also developed a curriculum model that could be used for establishing an Associate in Science degree in film production technology, unique in the country. The project was conducted by a partnership of Universal Studios Florida and Valencia Community College. The course combined hands-on classroom instruction with participation in the production of a feature-length film. Curriculum development involved seminars with working professionals in the five subject areas, using the Developing a Curriculum (DACUM) process. This curriculum guide for the 15-week course outlines the course and provides information on film production careers. It is organized in three parts. Part 1 includes brief job summaries ofmany technical positions within the film industry. -

The Migration of U.S. Film and Television Production

PREFACE In the early 1990s, important segments of the U.S. film industry became increasingly concerned about the growing loss of film and television production to foreign shores. The phenomenon of “runaway film production” began as a trickle, but has since become a persistent trend that is affecting thousands of jobs in certain segments of the film and television production industry, such as sound engineers, lighting technicians, assistant directors, unit production managers, supporting actors, costume designers, and set designers. In addition, there may be an even greater number of jobs affected that are connected to film and television production, such as caterers, truck drivers, carpenters, electricians, construction workers, hotel employees, and small businesses that provide services or material goods to productions throughout the United States. Some industry observers fear that the exodus of film production could threaten the viability of important segments of the film production industry in the United States, with potentially devastating effects on local communities in many states. Last year, the Department of Commerce was asked to examine the flight of U.S. television and cinematic film production to foreign shores. In September 2000, Commerce received an additional urgent request from a bipartisan group of Members of Congress to ensure that the final report address the following issues: (1) the impact of runaway production on the “below-the-line” employees throughout the United States, including (but not limited to) caterers, -

From the Camera Obscura to Video Assist Author(S): Jean-Pierre Geuens Source: Film Quarterly, Vol

Through the Looking Glasses: From the Camera Obscura to Video Assist Author(s): Jean-Pierre Geuens Source: Film Quarterly, Vol. 49, No. 3 (Spring, 1996), pp. 16-26 Published by: University of California Press Stable URL: http://www.jstor.org/stable/1213467 . Accessed: 15/06/2011 09:08 Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at . http://www.jstor.org/action/showPublisher?publisherCode=ucal. Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. University of California Press is collaborating with JSTOR to digitize, preserve and extend access to Film Quarterly. http://www.jstor.org Through Jean-Pierre Geuens the Looking Glasses From the Camera Obscura to Video Assist The oriiginal video assist apparatus put tog;ether by Bruce Hill in 1970 The studio is finally quiet. -

Film Crew Film Crew

FILM CREW FILM CREW The Film Crew … a typical crew engaged in a feature production. PRE-PRODUCTION During a feature production, a number of key people are brought into the project. The key roles and responsibilities include the following. The creative stage of pre-production begins with the Screenwriter. A Screenwriter creates a screenplay (a written version of a movie before it is filmed) either based on previously written material, such as a book or a play, or as an original work. A Screenwriter may write a screenplay on speculation, then try to sell it, or the Screenwriter may be hired by a Producer or studio to write a screenplay to given specifications. Screenplays are often rewritten, and it’s not uncommon for more than one Screenwriter to work on a script. A Producer is given control over the entire production of a motion picture and is ultimately held responsible for the success or failure of the motion picture project; this person is involved with the project from start to finish. The Producer's task is to organize and guide the project into a successful motion picture. The Producer would be the person who accepts the Academy Award for best picture, should the movie win one. The Producer organizes the development of the film, and is thus quite active in the pre-production phase. Once production (filming) begins, generally the role of the Producer is to supervise and give suggestions—suggestions that must be taken seriously by those creating the film. However, some Producers play a key role throughout the entire production process. -

The Essential Reference Guide for Filmmakers

THE ESSENTIAL REFERENCE GUIDE FOR FILMMAKERS IDEAS AND TECHNOLOGY IDEAS AND TECHNOLOGY AN INTRODUCTION TO THE ESSENTIAL REFERENCE GUIDE FOR FILMMAKERS Good films—those that e1ectively communicate the desired message—are the result of an almost magical blend of ideas and technological ingredients. And with an understanding of the tools and techniques available to the filmmaker, you can truly realize your vision. The “idea” ingredient is well documented, for beginner and professional alike. Books covering virtually all aspects of the aesthetics and mechanics of filmmaking abound—how to choose an appropriate film style, the importance of sound, how to write an e1ective film script, the basic elements of visual continuity, etc. Although equally important, becoming fluent with the technological aspects of filmmaking can be intimidating. With that in mind, we have produced this book, The Essential Reference Guide for Filmmakers. In it you will find technical information—about light meters, cameras, light, film selection, postproduction, and workflows—in an easy-to-read- and-apply format. Ours is a business that’s more than 100 years old, and from the beginning, Kodak has recognized that cinema is a form of artistic expression. Today’s cinematographers have at their disposal a variety of tools to assist them in manipulating and fine-tuning their images. And with all the changes taking place in film, digital, and hybrid technologies, you are involved with the entertainment industry at one of its most dynamic times. As you enter the exciting world of cinematography, remember that Kodak is an absolute treasure trove of information, and we are here to assist you in your journey. -

FAQ About Film Production — 1 Action Movie Makers Training

Action Movie makers training © 2016 FAQ About Film Production — www.actionmoviemakerstraining.com 1 Action Movie makers training FAQ About Film Production By Philippe Deseck July 2016 Content • About the Author • What is a Producer? • What is an Executive Producer? • What is a Line Producer? • What is a Supervising Producer? • What is a Co-Producer? • What is a Director? • What is a Unit Production Manager? • What is a 2nd Unit Director? • What is an Action Director? • What is an Assistant Director? • What is a Director of Photography? • What is a Script Supervisor? © 2016 FAQ About Film Production — www.actionmoviemakerstraining.com 2 Action Movie makers training • What is Sound Recordist? • What is a Video Split Operator? • What is a Key Grip? • What is a Gaffer? • What is a Safety Supervisor? • What is a Stunt Coordinator? • What is a Stunt Double? • What is a Stunt Rigger? • What is a Choreographer? • When is a Stunt Co-ordinator required on your Production? • An Example of all the Different Departments that work on a Feature Film © 2016 FAQ About Film Production — www.actionmoviemakerstraining.com 3 Action Movie makers training About the Author IMDB PROFILE: http://www.imdb.com/name/nm3455222/?ref_=fn_al_nm_1 Since a very young age Philippe has had a love for movies, particularly action movies from Hong Kong. Since 1994 Philippe has been actively involved in film, TV and radio whilst living in Thailand. Philippe’s movie credits include Street Fighter - where he was first introduced to stunt man Ronnie Vreeken, Operation Dumbo Drop and The Quest - where he met stunt man Alex Kuzelicki. -

Bill Witthans

BILL WITTHANS 31315 Tobiah Pl. Castaic, CA. 91384 Home: (661) 257-0196 / Cell: (661) 816-7991 Email: [email protected] WEB page: www.historicalhobbies.com/grip/grip.htm (just for fun and friends to look at) Hi, I am interested in working with you as your Key grip or Dolly grip . I’m well qualified with over 25 years of solid experience to offer you. I enclose my resume as a first step in exploring the possibilities of working with you. Just to get on the right track I realize that you may already have an excellent Key or Dolly grip that you use and I’m trying to move in on anyone’s position. I’m sending you this letter because with the changes in the film business the old ways of making contacts and establishing working relationships just isn’t sufficient. We might work in this business another 20 years a stage away from each other and still never meet. The days when crews stayed together picture after picture are pretty much gone, most will hook up with who ever can fill the next slot of time. It’s because of this that many times your normal crew may not be available. I would like to make myself available to you for these times. As a Key grip or Dolly grip with your team, I would bring a focus on speed, quality and support to your next project. I work well with others, and I am very experienced in crew management and problem solving. I also pride myself in working with UPMs / Line Producers and understanding “productions” needs and problems. -

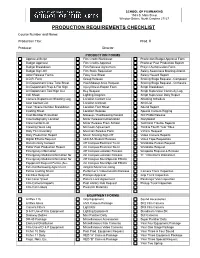

Production Requirements Checklist

SCHOOL OF FILMMAKING 1533 S. Main Street Winston-Salem, North Carolina 27127 PRODUCTION REQUIREMENTS CHECKLIST Course Number and Name: Production Title: Prod. # Producer: Director: PRODUCTION FORMS Approved Script Film Credit Worksheet Production Budget Approval Form Budget Approval Film Credits Approval Producer Post Production Report Budget Breakdown Film Release Agreement Project Authorization Form Budget Sign-Off Film Stock Requisition Safety Awareness Meeting Attend. Actor Release Forms Foley Cue Sheet Safety Hazard Report A.D.R. Form Group Release Scoring Stage Request - Composer Art Department Crew Time Sheet Hair/Makeup Artist Request Scoring Stage Request - Orchestra Art Department Prop & Flat Sign Injury/Illness Report Form Script Breakdown Art Department Tool Sign Out Key Request Script Supervisor Continuity Log Call Sheet Lighting Diagram Script Supervisor Daily Report Camera Department Shooting Log Location Contact List Shooting Schedule Cast Contact List Location Contract Shot List Cast / Scene Number Breakdown Location Fact Sheet Sound Report Casting Sheet Location Release Special Camera Rigging Cast Member Evaluation Makeup / Hairdressing Record Still Photo Release Cinematography Location Minor Release/Authorization Storyboard Crew Contact List Minor Release From School Technical Trouble Reports Crewing Hours Log Mix Lock Agreement Third & Fourth Year Titles Daily Film Inventory Musician Release Form Vehicle Request Daily Production Report Music Scoring Sign-Off Video Camera Reports Digital Effects Request UNCSA Student