Front Cover (Blue)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Managing the BBC's Estate

Managing the BBC’s estate Report by the Comptroller and Auditor General presented to the BBC Trust Value for Money Committee, 3 December 2014 BRITISH BROADCASTING CORPORATION Managing the BBC’s estate Report by the Comptroller and Auditor General presented to the BBC Trust Value for Money Committee, 3 December 2014 Presented to Parliament by the Secretary of State for Culture, Media & Sport by Command of Her Majesty January 2015 © BBC 2015 The text of this document may be reproduced free of charge in any format or medium providing that it is reproduced accurately and not in a misleading context. The material must be acknowledged as BBC copyright and the document title specified. Where third party material has been identified, permission from the respective copyright holder must be sought. BBC Trust response to the National Audit Office value for money study: Managing the BBC’s estate This year the Executive has developed a BBC Trust response new strategy which has been reviewed by As governing body of the BBC, the Trust is the Trust. In the short term, the Executive responsible for ensuring that the licence fee is focused on delivering the disposal of is spent efficiently and effectively. One of the Media Village in west London and associated ways we do this is by receiving and acting staff moves including plans to relocate staff upon value for money reports from the NAO. to surplus space in Birmingham, Salford, This report, which has focused on the BBC’s Bristol and Caversham. This disposal will management of its estate, has found that the reduce vacant space to just 2.6 per cent and BBC has made good progress in rationalising significantly reduce costs. -

I Am Mediacityuk

Useful information Events Cycle Contacts I am MediaCityUK is easy to MediaCityUK is a new Commercial office space: reach by bike and there waterfront destination for 07436 839 969 are over 300 cycle bays Manchester with digital [email protected] dotted across our site. creativity, learning and The Studios: MediaCityUK leisure at its heart. We host 0161 886 5111 a wide range of exciting Eat and drink studiobookings@ events: mediacityuk.co.uk/ We have a wide selection of dock10.co.uk destination/whats-on more than 40 venues for you The Pie Factory: to choose from. To find out 0161 660 3600 Getting here more visit: mediacityuk.co.uk/ [email protected] destination/eat-and-drink Road and parking Apartments: Two minutes from the 0161 238 7404 Manchester motorway Shopping anita.jolley@ network via Junctions 2 The Lowry Outlet at mediacityuk.co.uk and 3 of the M602. We have MediaCityUK is home to Hotel: 6,000 secure car parking a range of designer, high 0845 250 8458 spaces at key locations street and individual brands reservations@ across MediaCityUK. Sat offering discounts of up to himediacityuk.co.uk nav reference: M50 2EQ. 70%. lowryoutlet.co.uk Serviced apartments: 0161 820 6868 Tram reservations@ There are tram stops at Studio audiences theheartapartments.co.uk MediaCityUK, Broadway The Studios, MediaCityUK, and Harbour City and it are operated by dock10. General: takes just 15 minutes to To find out more details 0161 886 5300 get to Manchester city on tickets for shows go to: [email protected] centre for all inter-city mediacityuk.co.uk/studios/ connections. -

BBC B R O a D C a S T I N G

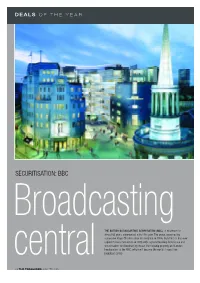

D E A L S O F T H E Y E A R SECURITISATION: BBC B r o a d c a s t i n g THE BRITISH BROADCASTING CORPORATION (BBC), in existence for almost 80 years, experienced a first this year. The group, governed by successive Royal Charters since its inception in 1926, launched its first-ever capital markets transaction in 2003 with a groundbreaking bond issue and securitisation for Broadcasting House, the flagship property and London headquarters of the BBC, which will become the world’s largest live c e n t r a l broadcast centre. 58 THE TREASURER JAN | FEB 2004 Corporate profile The BBC has been in existence for television services, network and local Principal terms of the almost 80 years, governed by radio and online services. The Wo r l d £813m securitisation successive Royal Charters in the UK. S e rvice is its international radio and The group has businesses along three online service (funded by direct grant Amount £813m main strands: public serv i c e from the Foreign & C o m m o n w e a l t h Type Fixed broadcasting in the UK is funded by Office). And BBC Commercial Margin 52bp the annual UK licence fees and Holdings coordinates activity across Maturity July 2033 includes delivery of free-to-air the BBC’s commercial businesses. Bookrunners Morgan Stanley The BBC first began looking at ways to develop its portfolio of over 500 together the transaction with Ernst & Young appointed as additional advisor. The properties back in 1999. -

A Career at BBC North

A Career at BBC North BBC North is the whole of the BBC in the north of England. There are approximately 2700 staff at MediaCityUK in Salford, and 700 staff who work in local radio and regional television across the north in Leeds, Sheffield, Hull, Newcastle, Middlesbrough, Carlisle, York, Blackburn, Lincoln and Liverpool. 200 more posts will move to MediaCityUK in 2015. MediaCityUK is in Salford on the Quays. There are 3 BBC buildings. The whole of BBC Sport is at Media City and there’s also BBC Breakfast, BBC Radio 5 live, the whole of the BBC Children’s department, that’s CBBC and CBeebies. We also have BBC Learning, the BBC Philharmonic Orchestra, North West Tonight and Radio Manchester. There’s Future Media, who build the BBC’s websites and apps and look after the BBC iPlayer and there are Technology teams who provide the support to keep our studios on air. There is Comedy and Entertainment, with programmes like Citizen Khan, Dragons’ Den and A Question of Sport and then there’s Radio Drama and Drama North, and even more radio with Radio 6 music and some Radio 2 and Radio 4 programmes. There is more to MediaCityUK than just the BBC, with many other companies there as well. ITV have around 500 staff there and they make Jeremy Kyle and Countdown and, of course, there’s the new set for Coronation Street. The first recording was done on this set in March. There are lot of smaller companies there too including small production companies, technical companies, sceneshifters, media accountants and lawyers and of course shops and restaurants as well. -

Art and Play on the Piazza Bowling with Lancashire

ART AND PLAY ON THE PIAZZA GARDENING WITH THE ROYAL PLAY WITH THE SCIENCE AND INDUSTRY MUSEUM We’re turning the MediaCity Piazza into a HORTICULTURAL SOCIETY (RHS) Join the Science and Industry Museum for colourful world of art and play. Scoot along Join the RHS for drop in planting sessions, a series of workshops with a STEM-twist; rainbow road, run through a field of daisies or where a team of gardening experts will pass from making flying objects to cracking and creating your own secret code – choose from grab some chalk from the Box on the Docks on tips and tricks. outdoor bar and draw on the Piazza floor. the sessions below and book your ticket. Wednesday, August 25th | 1pm – 3pm Throughout August Wings and Things Workshop Ages 18+ months A hands on session making flying objects. All ages Drop in, no booking necessary 4th August Drop in, no booking necessary Free Free Ages 5 – 12 years Booking essential: IMMERSE YOURSELF IN VIRTUAL www.eventbrite.com/e/163840572563 BOWLING WITH LANCASHIRE REALITY WITH HOST Free CRICKET FOUNDATION Get hands-on with virtual reality (VR) Codebreaker Workshop How fast and accurate is your bowling technology in HOST’s innovation labs. Enjoy Test your codebreaking skills in an interactive technique? It’s all in the grip, the run up, an overview of VR before you play around session and develop your own secret message. twist and throw - come and have a go with with the tech yourself. 11th August Lancashire Cricket Foundation’s inflatable Wednesday August 11th, 18th, 25th | 1pm – 2pm Ages 5 – 12 years bowling range. -

ROLE TITLE Gallery PA, Presentation BBC Children’S DATE BBC GRADE 5 May 2015 MODIFIED Location Mediacityuk

ROLE TITLE Gallery PA, Presentation BBC Children’s DATE BBC GRADE 5 May 2015 MODIFIED Location MediaCityUK Reports to/ Line Production Manager & Producers Manager CONTRACT 6 month FTC/Attachment Department BBC Children's Presentation produces continuity links for both CBeebies and (Sub Division) CBBC brands. In addition, it is also the home of CBBC series “Whoops I Missed The Bus”, CBeebies Bedtime Stories and other generic content such as the CBeebies Number Wraps, songs and other generic content. Presentation works closely with many teams, such as the Red Button, the Short Form content area, Marketing, Scheduling and Production (both Indies and In- House) to produce engaging wrap-around content for BBC Children's. An important aspect of Presentation is its close relationship with Ericsson, the BBC’s current transmission partner, and the Gallery PAs work closely with the embedded schedule planners to ensure we deliver the right content at the right time. The unit, which has over 60 members of staff, is based in Bridge House and has two permanent studios in Dock10, Salford Quays. Context Post holders at this level report to the Production Manager and Producers This role would start in CBeebies Presentation, but there may be scope to work across CBBC during the period of this engagement. Purpose of Role To work in partnership with editorial colleagues to deliver outstanding, distinctive, multi-platform content within operational, financial and timescale constraints. To professionally co-ordinate production(s) using specialist production management skills, knowledge and experience. To play an active role in maintaining a professional pan-BBC production management community. -

The Production of Religious Broadcasting: the Case of The

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by OpenGrey Repository The Production of Religious Broadcasting: The Case of the BBC Caitriona Noonan A thesis submitted in fulfilment of the requirements of the degree of Doctor of Philosophy. Centre for Cultural Policy Research Department of Theatre, Film and Television University of Glasgow Glasgow G12 8QQ December 2008 © Caitriona Noonan, 2008 Abstract This thesis examines the way in which media professionals negotiate the occupational challenges related to television and radio production. It has used the subject of religion and its treatment within the BBC as a microcosm to unpack some of the dilemmas of contemporary broadcasting. In recent years religious programmes have evolved in both form and content leading to what some observers claim is a “renaissance” in religious broadcasting. However, any claims of a renaissance have to be balanced against the complex institutional and commercial constraints that challenge its long-term viability. This research finds that despite the BBC’s public commitment to covering a religious brief, producers in this style of programming are subject to many of the same competitive forces as those in other areas of production. Furthermore those producers who work in-house within the BBC’s Department of Religion and Ethics believe that in practice they are being increasingly undermined through the internal culture of the Corporation and the strategic decisions it has adopted. This is not an intentional snub by the BBC but a product of the pressure the Corporation finds itself under in an increasingly competitive broadcasting ecology, hence the removal of the protection once afforded to both the department and the output. -

University of Salford Signs Mediacityuk Deal

NEWS RELEASE 13 January 2009 University of Salford signs MediaCityUK deal The University of Salford has signed an agreement for lease with developer Peel Media for a new innovative higher education centre at the heart of the MediaCityUK development in Salford Quays. The University is the second anchor tenant at MediaCityUK. In 2011, when the first phase of development is complete, it will enjoy a prime waterside location next to the BBC, which has already announced that it is moving five departments (currently based in London) to the site. The new University hub will comprise 100,000 sq ft over four floors and will be linked to the University’s four faculties on the main campus at Peel Park. With state-of-the-art facilities, it will focus on employer-led and postgraduate learning and research collaboration, and will act as a gateway to the University’s full range of services for its industry and community partners. The University is already a higher education partner with the BBC, which will relocate BBC Sport, Children’s (including CBeebies), Future Media and Technology, Radio 5 Live, Learning, and all local and network broadcasting currently based in Manchester city centre, to MediaCityUK. The University’s centre at MediaCityUK will include a broadcast zone, digital media zone, virtual laboratory, digital performance space and creative spaces for use in academic teaching, project-based learning and user-centred design and innovation. Digital media specialist John Holland, a former Head of Interactive TV and Digital Text Services at the BBC, has been appointed by the University to lead its new initiatives relating to MediaCityUK. -

BBC Radio Northampton and CSV Media

Thank you for your interest in the volunteering opportunities that have been made available at BBC Radio Northampton thanks to a partnership with the national charity CSV Media and funding from the European Social Fund. This pack will give you details about the partnership. Once you have read the enclosed information we hope you will want to become a CSV Media Volunteer and complete the enclosed application form. Upon receipt of your application you will be invited to an informal meeting with the CSV Media Action Producer for BBC Radio Northampton who will talk through the role of volunteers and discuss your reasons for wanting to get involved in the Service. After that meeting a letter will be sent to you to confirm whether you have been selected to join our team of volunteers. We look forward to hearing from you. BBC Radio Northampton and CSV Media GUIDANCE NOTES CSV MEDIA ACTION DESK VOLUNTEERS What is CSV Media? CSV Media is part of the national charity, Community Service Volunteers, which has established a UK wide network of partnerships with BBC Local Radio to provide social action broadcasting and support services designed to get people actively involved in their local communities. How does CSV Media work with BBC Radio Northampton? CSV Media has recruited a Producer for each BBC Local Radio Station in the Country. At BBC Radio Northampton the Producer works with the station’s already successful Action Team. What is Action? Action provides a response/helpline service for listeners, charities, community and voluntary groups in the county. Those requests are then broadcast on BBC Radio Northampton throughout the day and together with our listeners we can help those individuals and organisations find the answers and help for a whole range of questions and queries. -

Culture, Media and Sport Committee

House of Commons Culture, Media and Sport Committee Future of the BBC Fourth Report of Session 2014–15 Report, together with formal minutes relating to the report Ordered by the House of Commons to be printed 10 February 2015 HC 315 INCORPORATING HC 949, SESSION 2013-14 Published on 26 February 2015 by authority of the House of Commons London: The Stationery Office Limited £0.00 The Culture, Media and Sport Committee The Culture, Media and Sport Committee is appointed by the House of Commons to examine the expenditure, administration and policy of the Department for Culture, Media and Sport and its associated public bodies. Current membership Mr John Whittingdale MP (Conservative, Maldon) (Chair) Mr Ben Bradshaw MP (Labour, Exeter) Angie Bray MP (Conservative, Ealing Central and Acton) Conor Burns MP (Conservative, Bournemouth West) Tracey Crouch MP (Conservative, Chatham and Aylesford) Philip Davies MP (Conservative, Shipley) Paul Farrelly MP (Labour, Newcastle-under-Lyme) Mr John Leech MP (Liberal Democrat, Manchester, Withington) Steve Rotheram MP (Labour, Liverpool, Walton) Jim Sheridan MP (Labour, Paisley and Renfrewshire North) Mr Gerry Sutcliffe MP (Labour, Bradford South) The following Members were also a member of the Committee during the Parliament: David Cairns MP (Labour, Inverclyde) Dr Thérèse Coffey MP (Conservative, Suffolk Coastal) Damian Collins MP (Conservative, Folkestone and Hythe) Alan Keen MP (Labour Co-operative, Feltham and Heston) Louise Mensch MP (Conservative, Corby) Mr Adrian Sanders MP (Liberal Democrat, Torbay) Mr Tom Watson MP (Labour, West Bromwich East) Powers The Committee is one of the Departmental Select Committees, the powers of which are set out in House of Commons Standing Orders, principally in SO No 152. -

Transcript of a Press Conference Given by the Prime Minister of Singapore, Mr. Lee Kuan Yew, at Broadcasting House, Singapore, A

1 TRANSCRIPT OF A PRESS CONFERENCE GIVEN BY THE PRIME MINISTER OF SINGAPORE, MR. LEE KUAN YEW, AT BROADCASTING HOUSE, SINGAPORE, AT 1200 HOURS ON MONDAY 9TH AUGUST, 1965. Question: Mr. Prime Minister, after these momentous pronouncements, what most of us of the foreign press would be interested to learn would be your attitude towards Indonesia, particularly in the context of Indonesian confrontation, and how you view to conduct relations with Indonesia in the future as an independent, sovereign nation. Mr. Lee: I would like to phrase it most carefully because this is a delicate matter. But I think I can express my attitude in this way: We want to be friends with Indonesia. We have always wanted to be friends with Indonesia. We would like to settle any difficulties and differences with Indonesia. But we must survive. We have a right to survive. And, to survive, we must be sure that we cannot be just overrun. You know, invaded by armies or knocked out by rockets, if they have rockets -- which they have, ground-to-air. I'm not sure whether they lky\1965\lky0809b.doc 2 have ground-to-ground missiles. And, what I think is also important is we want, in spite of all that has happened -- which I think were largely ideological differences between us and the former Central Government, between us and the Alliance Government -- we want to-operate with them, on the most fair and equal basis. The emphasis is co-operate. We need them to survive. Our water supply comes from Johore. Our trade, 20-odd per cent -- over 20 per cent; I think about 24 per cent -- with Malaya, and about 4 to 5 per cent with Sabah and Sarawak. -

This Is an A-Z Guide of Mediacityuk, Containing Useful Information to Both Staff and Students

This is an A-Z guide of MediaCityUK, containing useful information to both staff and students. Typical information includes travel advice, catering facilities and how to book rooms and equipment. A - Access The University is introducing a single card system, all staff and students of the University are provided with the single card ID and access card. As the ground floor of MediaCityUK is open to all students and the general public, the single card is only operational in staff areas and teaching spaces. All staff and students must have their single ID card clearly visible at all times. You will need this card to access rooms you have booked for timetabled events or meetings. If you have booked out a room or studio you will only be granted access for the duration of your booking. The staff areas on floors 2 and 3 are gated off and your single card will allow you access into this. If you are meeting visitors or students you will need to arrange for suitable access to controlled spaces or to use the open meeting areas. The single card will allow you to access your printing from any printer in the building. Students will be issued with single cards at registration and will then liaise with Student Life. - Address Organisation Professor Smith Building Name University of Salford (working name) Thoroughfare Name Pink Locality MediaCityUK Post Town SALFORD Postcode M50 2HE - Announcements – any daily communication will be displayed on the plasma screens. - Assignment submission – There will be a drop box facility for handing in assignments on the mezzanine area of the 1st floor.