Radio: the Implications of Digital Britain for Localness Regulation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Local Commercial Radio Content

Local commercial radio content Qualitative Research Report Prepared for Ofcom by Kantar Media 1 Contents Contents ................................................................................................................................................. 2 1 Executive summary .................................................................................................................... 5 1.1 Background .............................................................................................................................. 5 1.2 Summary of key findings .......................................................................................................... 5 2 Background and objectives ..................................................................................................... 10 2.1 Background ............................................................................................................................ 10 2.2 Research objectives ............................................................................................................... 10 2.3 Research approach and sample ............................................................................................ 11 2.3.1 Overview ............................................................................................................................. 11 2.3.2 Workshop groups: approach and sample ........................................................................... 11 2.3.3 Research flow summary .................................................................................................... -

Radio City 2 and City Talk Requests to Change Formats

Radio City 2 and City Talk Requests to change Formats Consultation Publication date: 21 July 2015 Closing date for responses: 2 September 2015 Requests to change Formats – Radio City 2 and City Talk Contents Section Page 1 About this document 2 2 Details and background information 3 Annex Page 1 Responding to this consultation 6 2 Ofcom’s consultation principles 8 3 Consultation response cover sheet 9 4 Consultation questions 11 5 Format Change Requests - Radio City 2 & City Talk 22 6 Existing Formats of Radio City & City Talk 23 7 Other commercial and community radio stations in the Liverpool area 24 1 Requests to change Formats – Radio City and City Talk Section 1 1 About this document 1.1 Ofcom has received two Format change requests from Radio City (Sound of Merseyside) Ltd, which holds an AM and two FM commercial radio licences for Liverpool. 1.2 A station’s Format describes the type of programme service which it is required to provide, and forms part of the station’s licence. 1.3 Radio City (Sound of Merseyside) Ltd wishes to change the ‘Character of Service’ of its AM licence (currently Radio City 2) and one of its FM licences (currently City Talk). 1.4 Radio City 2’s published Format requires the service to broadcast “a classic soft pop music-led service”. The licensee wishes to change this to a service of “rock hits with news, local sport and information programming.” 1.5 City Talk’s published Format requires the service to broadcast “speech and soft pop- led music programming”. -

Analogue Commercial Radio Licence: Format Change Request Form

Analogue Commercial Radio Licence: Format Change Request Form Date of request: 16.11.18 Station Name: Radio City 2 to become Greatest Hits Radio (Liverpool) Licensed area and licence Liverpool and surrounding area number: AL 321-1 Licensee: Radio City (Sound of Merseyside) Ltd Contact name: Peter Davies Details of requested change(s) to Format Character of Service Existing Character of Service: Complete this section if you are requesting a change to this part of your Format Proposed new Character of Service: Programme sharing and/or co- Current arrangements: location arrangements Complete this section if you are requesting a change to this part of your Format Proposed new arrangements: Locally-made hours and/or Current obligations: local news bulletins At least 7 hours a day during daytime weekdays (must include breakfast). Complete this section if you are requesting a change to this At least 4 hours daytime Saturdays and part of your Format Sundays. Version 9 – amended May 2018 Proposed new obligations: At least 3 hours a day during daytime weekdays The holder of an analogue local commercial radio licence may apply to Ofcom to have the station’s Format amended. Any application should be made using the layout shown on this form, and should be in accordance with Ofcom’s published procedures for Format changes.1 Under section 106(1A) of the Broadcasting Act 1990 (as amended), Ofcom may consent to a change of a Format only if it is satisfied that at least one of the following five statutory criteria is satisfied: (a) that the departure would -

Pledge 15 2019-20 Q3 Leisure and Culture For

Wirral Plan 2019-20 Q3 - Pledge Overview Report Leisure and cultural opportunities for all Overview from Lead Cabinet Member Leisure Strategy It’s great news that Landican Cemetery achieved the Green Flag for the first time this year, recognising the staff and volunteers who work tirelessly to maintain the high standards demanded by the Green Flag Award. This brings Wirral’s total to 27 up from 26 last year and we now have more Green Flags than any other local authority in the whole of the North of England. Birkenhead Park’s application for World Heritage Site status is progressing well following the International Council on Monuments and Sites meeting in October. A total of 475 young people were engaged in the National Citizens Service programme and 80 young people engaged with the Pathfinders project which focused workshops on knife crime, serious crime and the Cells Project who’s primary aim is to educate youngsters about how crime effects all it touches, acting as a deterrent & also a conduit to positive progression. The Macmillan project is now in its final year of funding which ends April 2020. The project is exceeding expectations and targets. Within the first year of the project was targeted to support 250 people affected by cancer on the Wirral but has in fact managed to support over 700 in the first year and achieved its 2-year target within 8 months. The project has also been shortlisted for a National Macmillan Excellence award. Culture Strategy Wirral’s Borough of Culture has been a phenomenal year, celebrating an abundance of local talent and creativity and also bringing in fantastic, internationally - renowned artists to showcase Wirral locally, regionally, nationally and on a global scale in some cases. -

3 Radio and Audio Content 3 3.1 Recent Developments in Scotland

3 Radio and audio content 3 3.1 Recent developments in Scotland Real Radio Scotland has been rebranded as Heart In February 2014 Capital Scotland was sold to the Irish media holding company, Communicorp. It was sold as part of eight stations divested by Global Radio to satisfy the UK regulatory authorities following the acquisition, two years ago, of GMG Radio from Guardian Media Group. Under a brand licensing agreement, Communicorp has rebranded the 'Real' stations under the 'Heart' franchise and plans to relaunch the 'Smooth' stations following the reintroduction of local programming. Therefore, Real Radio Scotland was rebranded as Heart Scotland in May 2014. XFM Scotland was re-launched by its owners, Global Radio, in March 2014. 3.2 Radio station availability Five new community radio stations are available to listeners in Scotland Scotland’s community radio industry has continued to grow. There are now 23 community stations on air, out of the 31 licences that have been awarded in Scotland. New to air in 2013/14 were East Coast FM, Irvine Beat FM, Crystal Radio, and K107 FM. Irvine Beat FM has received funding from the Lottery Awards for All fund to build a training studio. Nevis Radio, which serves Fort William and the surrounding areas, was originally licensed as a commercial radio service, but having chosen to become a community radio service it was awarded this licence instead, on application. The remaining eight of the most recent round of licence awards are preparing to launch. A licensee has two years from the date of the licence award in which to launch a service. -

Pocketbook for You, in Any Print Style: Including Updated and Filtered Data, However You Want It

Hello Since 1994, Media UK - www.mediauk.com - has contained a full media directory. We now contain media news from over 50 sources, RAJAR and playlist information, the industry's widest selection of radio jobs, and much more - and it's all free. From our directory, we're proud to be able to produce a new edition of the Radio Pocket Book. We've based this on the Radio Authority version that was available when we launched 17 years ago. We hope you find it useful. Enjoy this return of an old favourite: and set mediauk.com on your browser favourites list. James Cridland Managing Director Media UK First published in Great Britain in September 2011 Copyright © 1994-2011 Not At All Bad Ltd. All Rights Reserved. mediauk.com/terms This edition produced October 18, 2011 Set in Book Antiqua Printed on dead trees Published by Not At All Bad Ltd (t/a Media UK) Registered in England, No 6312072 Registered Office (not for correspondence): 96a Curtain Road, London EC2A 3AA 020 7100 1811 [email protected] @mediauk www.mediauk.com Foreword In 1975, when I was 13, I wrote to the IBA to ask for a copy of their latest publication grandly titled Transmitting stations: a Pocket Guide. The year before I had listened with excitement to the launch of our local commercial station, Liverpool's Radio City, and wanted to find out what other stations I might be able to pick up. In those days the Guide covered TV as well as radio, which could only manage to fill two pages – but then there were only 19 “ILR” stations. -

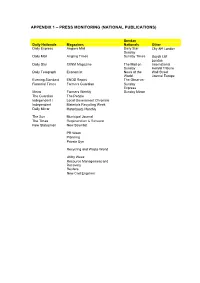

Appendix 1 – Press Monitoring (National Publications)

APPENDIX 1 – PRESS MONITORING (NATIONAL PUBLICATIONS) Sunday Daily Nationals Magazines Nationals Other Daily Express Anglers Mail Daily Star City AM London Sunday Daily Mail Angling Times Sunday Times Lloyds List London Daily Star CIWM Magazine The Mail on International Sunday Herald Tribune Daily Telegraph Economist News of the Wall Street World Journal Europe Evening Standard ENDS Report The Observer Financial Times Farmers Guardian Sunday Express Metro Farmers Weekly Sunday Mirror The Guardian The People Independent i Local Government Chronicle Independent Materials Recycling Week Daily Mirror Motorboats Monthly The Sun Municipal Journal The Times Regeneration & Renewal New Statesman New Scientist PR Week Planning Private Eye Recycling and Waste World Utility Week Resource Management and Recovery Reuters New Civil Engineer APPENDIX 2 – PRESS MONITORING (NATIONAL KEY WORDS) Keyword Keyword Description Agriculture - Environment Important mentions of farming or agriculture ICW the environment. Carbon Emissions All mentions of carbon emissions OICW climate change, global warming etc. Climate Change All mentions of climate change. Coastal Erosion All mentions of coastal erosion. DEFRA All mentions of Department for Environment, Food and Rural Affairs (DEFRA). Department of Energy & Climate All mentions of the Department of Energy & Climate Change Change (DECC) Drought Main focus mentions of droughts in the UK Environment All mentions of environmental issues Environment - Emissions Important mentions of emissions and their effect on the environment. Environment Agency All mentions of the Environment Agency. Fishing All mentions of fishing ICW the environment. Flooding - Environmental Impact Important Mentions of floods OICW effects on the environment and homes Fly Tipping All mentions of fly tipping Hosepipes All mentions of hosepipes Nuclear Power - Environmental Main focus mentions of environmental effects of nuclear power. -

RAJAR DATA RELEASE QUARTER 4, 2008 January 29, 2009

RAJAR DATA RELEASE QUARTER 4, 2008 January 29, 2009 COMPARATIVE CHARTS ¾ National stations ¾ Scottish stations ¾ London stations ¾ National & London stations – Breakfast shows RAJAR Quarterly Summary of Radio Listening - Quarter 4, 2008 NATIONAL STATIONS RELEASED AT 07.00HRS THURSDAY JANUARY 29, 2009 KEY Quarter 4, 2007 in green Quarter 3, 2008 in blue Quarter 4, 2008 in pink % Change Y/Y and Q/Q for reach only * = less than 0.05% TERMS WEEKLY REACH: The number in thousands of the UK/area adult population who listen to a station for at least 5 minutes in the course of an average week. SHARE OF LISTENING: The percentage of total listening time accounted for by a station in the UK/area in an average week TOTAL HOURS: The overall number of hours of adult listening to a station in the UK/area in an average week SAMPLE SIZE Q4 2008: Survey Period - Code Q (Quarter): 33,326 Adults 15+ / Code H (Half year): 66,175 Adults 15+ TOTAL HOURS (in thousands): A LL BBC Q4 07 564034 Q3 08 550398 Q4 08 564437 TOTAL HOURS (in thousands): A LL COMMERCIAL Q4 07 431319 Q3 08 432016 Q4 08 427050 STATION SURVEY REACH REACH REACH % CHANGE % CHANGE SHARE SHARE SHARE PERIOD '000 '000 '000 REACH Y/Y REACH Q/Q % % % Q4 07 Q3 08 Q4 08 Q4 08 vs Q4 07 Q4 08 vs Q3 08 Q4 07 Q3 08 Q4 08 ALL RADIO Q 44952 45084 45511 1.2% 0.9% 100.0 100.0 100.0 ALL BBC Q 33139 32981 33520 1.1% 1.6% 55.4 54.9 55.7 15-44 Q 15331 15248 15548 1.4% 2.0% 44.2 44.0 44.8 45+ Q 17808 17734 17972 0.9% 1.3% 64.7 63.7 64.5 ALL BBC NETWORK RADIO Q 29234 29331 29923 2.4% 2.0% 45.4 45.5 46.4 BBC RADIO -

Heart (Yorkshire)

Analogue Commercial Radio Licence: Format Change Request Form Date of request: 14th December 2018 Station Name: Heart Yorkshire Licensed area and licence South and West Yorkshire number: Licence Number: AL000269BA/4 Licensee: Real Radio (Yorkshire) Limited Contact name: Colin Everitt Details of requested change(s) to Format Character of Service Existing Character of Service: Complete this section if you are requesting a change to this part of your Format Proposed new Character of Service: Programme sharing and/or co- Current arrangements: location arrangements Complete this section if you are requesting a change to this part of your Format Proposed new arrangements: Locally-made hours and/or Current obligations: local news bulletins Locally-made hours: At least 7 hours a day during daytime weekdays Complete this section if you are (must include breakfast). At least 4 hours daytime requesting a change to this Saturdays and Sundays. part of your Format Local News bulletins: At least hourly during daytime weekdays and peak- time weekends. At other times UK-wide, nations and international news should feature. Version 9 – amended May 2018 Proposed new obligations: Locally-made hours: At least 3 hours a day during daytime weekdays. Local news bulletins: No change. The holder of an analogue local commercial radio licence may apply to Ofcom to have the station’s Format amended. Any application should be made using the layout shown on this form, and should be in accordance with Ofcom’s published procedures for Format changes.1 Under section 106(1A) -

Kind to Your Mind Campaign Briefing This Is a Short Briefing About the New ‘Kind to Your Mind’ Campaign

Supporting the mental wellbeing of our key workers and residents in Cheshire and Merseyside Kind to your mind campaign briefing This is a short briefing about the new ‘Kind to your mind’ campaign. It will be running in April 2020 and aims to support the mental wellbeing of those living and working in Cheshire and Merseyside during the Coronavirus outbreak. It is being led jointly by Champs Public Health Collaborative and the Cheshire and Merseyside Health and Care Partnership. How you can help Please support this important campaign and encourage your local colleagues and residents to visit the webpage www.kindtoyourmind.org for information and resources to help improve mental wellbeing during the Coronavirus outbreak. Why do we need this campaign? Both key workers and members of the public are likely to be feeling stress or anxiety at this difficult time as we make major changes to how we live and work. It is more important than ever that we look after our mental wellbeing and encourage others to do the same. This will help us during the pandemic and aid our recovery. The Kind to your mind campaign will utilise the national ‘Every Mind Matters’ messages and materials and will promote awareness of a wellbeing portal that has been exclusively developed by Cheshire and Merseyside for Cheshire and Merseyside residents and workers. The campaign will link to a landing page branded ‘Kind to your mind’ which will signpost people to these resources. Every Mind Matters Every Mind Matters is a joint NHS and Public Health England campaign. The purpose of the campaign is to support people with advice and resources to look after their mental health and wellbeing. -

Competition Commission by EMAIL ONLY Dear Daniel Information

As of 9 November 2012 [] Competition Commission BY EMAIL ONLY Dear Daniel Information requested on 22 October 2012 (i) information as to Global Radio's current competitors in the radio services industry in the UK, and what new competitors Global Radio may face in the future; TCB is a predominantly Welsh-based and focussed broadcasting organisation and therefore this response is limited to the Welsh radio market. Global Radio’s current competitors for revenue are other commercial radio station operators, Commercial TV (including S4C in Wales); other forms of alternative marketing spend including press, internet, outdoor etc. TCB is a direct competitor for audience and revenue of GMG in Wales. The coverage area of Real Radio Wales wholly overlaps all 7 of TCB’s Welsh services and also of Global Radio in Cardiff and Newport and to a lesser extent Bridgend where the coverage area of Capital South Wales is overlapped by Nation Radio and Bridge FM. 1 We wish to correct the assertion made to the OFT by Global Radio in respect of North Wales as we do not consider that Radio Ceredigion competes with Global Radio’s existing stations in North Wales. In fact, the surveyed audience areas of Radio Ceredigion and Heart North Wales for RAJAR do not 2 3 appear to overlap at all (Appendix 3) and the measured coverage area (MCA) shows an overlap of just 132 adults representing significantly less than 1% of either station’s overall MCA. We accept that GMG’s Real Radio service wholly overlaps with Radio Ceredigion however we understand that the transmission configuration of Real Radio would not allow a client to purchase advertising into Ceredigion only. -

Metro Radio Is Very Much in Touch with ‘Love of Life Round Here’

1 2 With Key 103 & Magic 1152’s weekly audience of 532,000 we can fill the Manchester Arena capacity 25 times! Source: RAJAR, Key 103 TSA. 6 Months, PE Sep 2012. Key 103 & Magic 1152 = Bauer Manchester 3 AUDIENCE POTENTIAL : 2,445,000 Male = 1,211,000 Female = 1,234,000 Source: RAJAR, Key 103 TSA. 6 Months, PE Sep 2012. 4 “Key 103 & Magic 1152 – Still Manchester’s Number One” • Key 103 and Magic 1152 retain their position as the commercial market leader in Greater Manchester with 532,000 listeners tuning into the stations each week. • Key 103’s Mike and Chelsea is Manchester’s most listened to commercial Breakfast show with 320,000 listeners tuning in each week, and OJ Borg’s Home time show continues to grow, increasing the station’s share in the afternoon to 8.9% (from 8) • In our core 25–44 demographic Key 103 remains number 1 for reach & share commercially, with a 17% higher share than Capital and 97.2% higher share for the demo than Smooth Source: RAJAR, Key 103 TSA. 6 Months, PE Sep 2012. Key 103 & Magic 1152 = Bauer Manchester 5 Combined Audience Mixed of adult contemporary music with unrivalled news and sports coverage, phone-ins and local information 61% 53% 47% 44% 39% 34% 22% Men Wome n 15 -24 25- 44 45+ ABC1 C2DE This shows a breakdown of our demographic here at Key103 & Magic 1152 to show a representation of the type of listeners we have and potential customers you could have. Breakdown by gender, age & social class in percentages respectively.