Parenthood Is an Adventure Saving for Their College Education Is Simple

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vanguard 2019 Investment Stewardship Semiannual

Vanguard 2019 Investment Stewardship Semiannual Engagement Update Semiannual Engagement Update Introduction 1 Board composition 2 Oversight of strategy and risk 6 Executive compensation 8 Governance structures 10 Company engagements 12 b Good governance can enhance and protect shareholder value over time. Boards that are well-composed for today and tomorrow have independent, experienced, and diverse members capable of overseeing strategy, governing risk, setting appropriate compensation, and embracing policies that give voice to shareholders. One of the hallmarks of good governance is engagement with shareholders. Each year, on behalf of Vanguard funds, our Investment Stewardship team meets with hundreds of portfolio companies. In these interactions, we have open, constructive dialogues about corporate governance. This semiannual engagement update provides snapshots of some of the discussions we held in the six months ended December 31, 2018. The substance of those discussions was framed by Vanguard’s four principles of corporate governance: Board Oversight of Executive Governance composition strategy & risk compensation structures These pillars cover topics such as board independence, alignment of strategy to long-term value creation, and linkage of pay to performance. Although these discussions can vary widely by company, sector, and region, our engagements tend to fall into three broad categories. Strategic engagements are meetings in which we learn about—but don’t seek to direct—a company’s long- term strategy. These enable us to understand the board’s approach to overseeing and aligning governance practices with the company’s long-term goals. Event-driven engagements focus on specific ballot items—often contentious—or a leadership change or company crisis. -

THE VOICE of CHESTER COUNTY Voice MARCH 2015

the THE VOICE OF CHESTER COUNTY Voice MARCH 2015 The Chester County Chamber Foundation Gala A night of fun for a great cause! Last Saturday the Chester County Chamber Foundation hosted the 2015 Auction Gala and what a night it was! Gala attendees put on their most fashionable 1960’s outfits and made their way to White Manor Country Club. Upon arrival, guests were greeted with champagne and appetizers. Between networking and catching up with friends, ordering a signature drink and checking out the Silent Auction-- the buzz coming from cocktail hour was remarkable. As the ballroom doors opened, guests were led to the Wine Wall, photo booth, and delicious food stations. It wasn’t long before the Smooth Sounds of Steve Silicato had everyone on the dance floor. Amongst all the good times, it was important to remember why we were there. All the proceeds from the raffles, games, and Live & Silent auctions will fund our Youth Leadership Program. Thank you to all who came to support this event and our mission at the Chamber Foundation. 1 Join the Chamber at our Annual State of the County Luncheon Featuring Chester County Commissioners Terence Farrell, Michelle Kichline, and Kathi Cozzone, CCCBI hosts the Chester County Commissioners for our State of the County Luncheon on Wednesday, April 8th. This event provides an update on Chester County and draws hundreds of business and community leaders. We’ll be honoring the recipient of the Boling Award, presented to a person who exemplifies the meaning of a dedicated public servant who excelled in his accomplishments on behalf of the public. -

Vanguard Money Market Funds Annual Report August 31, 2018

Annual Report | August 31, 2018 Vanguard Money Market Funds Vanguard Prime Money Market Fund Vanguard Federal Money Market Fund Vanguard Treasury Money Market Fund Vanguard’s Principles for Investing Success We want to give you the best chance of investment success. These principles, grounded in Vanguard’s research and experience, can put you on the right path. Goals. Create clear, appropriate investment goals. Balance. Develop a suitable asset allocation using broadly diversified funds. Cost. Minimize cost. Discipline. Maintain perspective and long-term discipline. A single theme unites these principles: Focus on the things you can control. We believe there is no wiser course for any investor. Contents Your Fund’s Performance at a Glance. 1 CEO’s Perspective. 3 Advisor’s Report. 5 Prime Money Market Fund. .7 Federal Money Market Fund. 26 Treasury Money Market Fund. 42 About Your Fund’s Expenses. 55 Trustees Approve Advisory Arrangements. .57 Glossary. 59 Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus. See the Glossary for definitions of investment terms used in this report. Your Fund’s Performance at a Glance • For the 12 months ended August 31, 2018, Vanguard Prime Money Market Fund returned 1.59% for Investor Shares and 1.66% for Admiral Shares. Vanguard Federal Money Market Fund returned 1.42% and Vanguard Treasury Money Market Fund 1.43%. -

Vanguard® Value Index Fund

Vanguard® Vanguard® Value Index Fund Product Summary Vanguard Style View : Large Value Seeks to track the performance of the CRSP US Large Cap Value Index portfolio of large-capitalization value stocks. Index. Investment style Value Blend Growth Large-cap value equity. Passively managed, full-replication approach. Large Fund remains fully invested. Mid Low expenses minimize net tracking error. Small Note: The Investor Shares are closed to new investors. Market capitalization Central tendency Expected range of fund holdings Quarterly Commentary People and Process The human toll of COVID-19 further mounted during the second Vanguard Value Index Fund seeks to track the investment quarter of 2021 amid fresh outbreaks of the virus and new performance of the CRSP US Large Cap Value Index, an variants. The global economy nevertheless continued to rebound unmanaged benchmark representing U.S. large-capitalization value sharply if unevenly. Countries that have better succeeded in stocks. The fund attempts to replicate the target index by containing the virus—whether through vaccinations, lockdowns, or investing all, or substantially all, of its assets in the stocks that both—tended to fare the best. With the reopening of economies make up the index, holding each stock in approximately the same and pent-up demand boosting corporate profits, global stocks proportion as its weighting in the index. The experience and finished the quarter significantly higher. U.S. stocks outperformed stability of Vanguard’s Equity Index Group have permitted other developed markets as a whole as well as emerging markets. continuous refinement of techniques for reducing tracking error. The group uses proprietary software to implement trading The combination of faster economic growth, a recovery in decisions that accommodate cash flow and maintain close commodity prices, ongoing fiscal and monetary stimulus, and a correlation with index characteristics. -

Vanguard Balanced Portfolio Semiannual Report

Semiannual Report | June 30, 2021 Vanguard Variable Insurance Funds Balanced Portfolio Contents About Your Portfolio’s Expenses ..................... 1 Financial Statements ................................ 3 Trustees Approve Advisory Arrangement ............31 Liquidity Risk Management..........................32 About Your Portfolio’s Expenses As a shareholder of the portfolio, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a portfolio's gross income, directly reduce the investment return of the portfolio. A portfolio's expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your portfolio and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period. The accompanying table illustrates your portfolio's costs in two ways: • Based on actual portfolio return. This section helps you to estimate the actual expenses that you paid over the period. The ”Ending Account Value“ shown is derived from the portfolio's actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the portfolio. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your portfolio under the heading ”Expenses Paid During Period.“ • Based on hypothetical 5% yearly return. -

403(B)/403(B)(7) Providers

403(b)/403(b)(7) Providers AIG RETIREMENT SERVICES www.aig.com/retirementservices 800-448-2542 AMERICAN CENTURY INVESTMENTS www.americancentury.com/enroll 800-345-3533 AMERICAN FIDELITY ASSURANCE ANNUITIES ¹ www.afadvantage.com 800-654-8489 AMERICAN FUNDS DISTRIBUTORS, INC. www.americanfunds.com/ 800-421-9900 AMERICAN UNITED LIFE INSURANCE COMPANY www.oneamerica.com 800-249-6269 AMERICO FINANCIAL LIFE AND ANNUITY INS. CO. www.americo.com 800-231-0801 AMERIPRISE FINANCIAL SERVICES, INC. www.ameriprise.com 800-862-7919 ASPIRE FINANCIAL SERVICES, INC. www.aspireonline.com/enrollment 866-634-5873 ATHENE USA ¹ www.athene.com 800-225-8073 EQUITABLE LIFE INSURANCE COMPANY www.equitable.com 800-628-6673 FEDERATED FUNDS www.federatedinvestors.com 800-245-4770 FIDELITY SECURITY LIFE INS COMPANY www.fslins.com 800-648-8624 FRANKLIN TEMPLETON INVESTMENTS www.franklintempleton.com 800-527-2020 GENERAL AMERICAN LIFE INSURANCE COMPANY ¹ www.metlife.com 800-638-9294 GLOBAL ATLANTIC FINANCIAL GROUP www.globalatlantic.com 508-460-2401 GLP AND ASSOCIATES, INC. www.glpwins.com 877-457-9467 GREAT AMERICAN INSURANCE GROUP ¹ www.gafri.com 800-789-6771 GREAT SOUTHERN LIFE ¹ www.greatsouthern.com 800-231-0801 GWN SECURITIES, INC. www.gwnsecurities.com 561-472-2700 GUGGENHEIM INVESTMENTS (Formerly Rydex Investments)¹ www.guggenheiminvestments.com 800-820-0888 HORACE MANN www.horacemann.com 800-999-1030 HORACE MANN INVESTORS, Inc. www.horacemann.com 800-999-1030 INDUSTRIAL ALLIANCE PACIFIC LIFE INS. & FINANCIAL SVCS. INC.¹ www.iaamerican.com 888-473-5540 INVESCO INVESTMENT SERVICES www.invesco.com 800-959-4246 ISC GROUP, INC. www.iscgroup.com 800-888-3520 JACKSON NATIONAL LIFE INS. -

US Mainstream Media Index May 2021.Pdf

Mainstream Media Top Investors/Donors/Owners Ownership Type Medium Reach # estimated monthly (ranked by audience size) for ranking purposes 1 Wikipedia Google was the biggest funder in 2020 Non Profit Digital Only In July 2020, there were 1,700,000,000 along with Wojcicki Foundation 5B visitors to Wikipedia. (YouTube) Foundation while the largest BBC reports, via donor to its endowment is Arcadia, a Wikipedia, that the site charitable fund of Lisbet Rausing and had on average in 2020, Peter Baldwin. Other major donors 1.7 billion unique visitors include Google.org, Amazon, Musk every month. SimilarWeb Foundation, George Soros, Craig reports over 5B monthly Newmark, Facebook and the late Jim visits for April 2021. Pacha. Wikipedia spends $55M/year on salaries and programs with a total of $112M in expenses in 2020 while all content is user-generated (free). 2 FOX Rupert Murdoch has a controlling Publicly Traded TV/digital site 2.6M in Jan. 2021. 3.6 833,000,000 interest in News Corp. million households – Average weekday prime Rupert Murdoch Executive Chairman, time news audience in News Corp, son Lachlan K. Murdoch, Co- 2020. Website visits in Chairman, News Corp, Executive Dec. 2020: FOX 332M. Chairman & Chief Executive Officer, Fox Source: Adweek and Corporation, Executive Chairman, NOVA Press Gazette. However, Entertainment Group. Fox News is owned unique monthly views by the Fox Corporation, which is owned in are 113M in Dec. 2020. part by the Murdoch Family (39% share). It’s also important to point out that the same person with Fox News ownership, Rupert Murdoch, owns News Corp with the same 39% share, and News Corp owns the New York Post, HarperCollins, and the Wall Street Journal. -

Investment Profile

Vanguard® Vanguard® Windsor™ Fund Product Summary Vanguard Style View : Large Value Large- and mid-cap value equity. Portfolio emphasizing large- and mid-capitalization value stocks. Seeks long-term capital appreciation and growth of income. Investment style Value Blend Growth Diversified, multimanager structure. Fundamental research approach. Large Opportunistic, contrarian stock selection style. Mid Small Market capitalization Central tendency Expected range of fund holdings Quarterly Commentary People and Process The human toll of COVID-19 further mounted during the second Vanguard Windsor Fund seeks long-term capital appreciation and quarter of 2021 amid fresh outbreaks of the virus and new income by investing in mid- and large-capitalization value stocks, variants. The global economy nevertheless continued to rebound using a multimanager structure that provides diversification and sharply if unevenly. Countries that have better succeeded in mitigates risk. The fund’s two investment advisors employ containing the virus—whether through vaccinations, lockdowns, or intensive fundamental research and strict valuation disciplines to both—tended to fare the best. With the reopening of economies construct portfolios of undervalued and out-of-favor stocks. The and pent-up demand boosting corporate profits, global stocks combination of two distinctly different approaches to valuation, finished the quarter significantly higher. U.S. stocks outperformed stock selection, and portfolio construction enhances diversification other developed markets as a whole as well as emerging markets. while maintaining the fund’s value character. In addition, Vanguard may invest the fund’s cash flows in equity index futures and/or For the quarter, U.S. stocks returned 8.24%, as measured by the exchange-traded funds to manage liquidity needs while ensuring Russell 3000 Index. -

Vanguard Total Bond Market Index Fund Annual Report December 31

Annual Report]%FDFNCFS 7BOHVBSE5PUBM#POE.BSLFU*OEFY'VOE Contents Your Fund’s Performance at a Glance. 1 About Your Fund’s Expenses. 2 Performance Summary. .4 Financial Statements. 8 Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus. :PVS'VOET1FSGPSNBODFBUB(MBODF t 'PSUIFNPOUITFOEFE%FDFNCFS SFUVSOTGPS7BOHVBSE5PUBM#POE .BSLFU*OEFY'VOESBOHFEGSPNGPS*OWFTUPS4IBSFTUPGPS*OTUJUVUJPOBM 4FMFDU4IBSFT5IJTQFSGPSNBODFXBTJOMJOFXJUIUIFSFUVSOPGUIFCFODINBSL JOEFYBGUFSUBLJOHUIFDPTUTPGSVOOJOHUIFGVOEJOUPBDDPVOU t 5IFFNFSHFODFPG$07*%JOFBSMZUVSOFEJOUPBHMPCBMIFBMUIDSJTJT BOE BHHSFTTJWFBUUFNQUTUPDPOUBJOJUSFTVMUFEJOBTIBSQEPXOUVSOJOFDPOPNJDBDUJWJUZ 6OFNQMPZNFOUTQJLFE BOETFDUPSTXIFSFTPDJBMEJTUBODJOHJTOUQPTTJCMFXFSFIJUIBSE 1PMJDZNBLFSTXFSFRVJDLUPQSPWJEFSPCVTUGJTDBMBOENPOFUBSZTUJNVMVTUPCMVOUUIF QBOEFNJDTFDPOPNJDJNQBDU.BOZDFOUSBMCBOLTTMBTIFETIPSUUFSNJOUFSFTUSBUFT BOEFYQBOEFEPSFYUFOEFEBTTFUQVSDIBTFQSPHSBNT t 8JUIZJFMETGBMMJOHBOEQSJDFTSJTJOH 645SFBTVSJFTQPTUFEBSFUVSOPG .PSUHBHFCBDLFETFDVSJUJFTSFUVSOFEMFTTUIBOUIBU BTMPXNPSUHBHFSBUFTMFEUPQMFOUZ PGTVQQMZCVUDPSQPSBUFCPOETGBSFEFWFOCFUUFSUIBO5SFBTVSJFT SFUVSOJOH t #ZDSFEJURVBMJUZ MPXFSSBUFEJOWFTUNFOUHSBEFCPOETHFOFSBMMZEJECFUUFSUIBO IJHIFSSBUFEPOFTCZNBUVSJUZ CPOETXJUINBUVSJUJFTPGZFBSTPSNPSFTJHOJGJDBOUMZ PVUQFSGPSNFE .BSLFU#BSPNFUFS "WFSBHF"OOVBM5PUBM3FUVSOT -

Schwab Treasury Inflation Protected Securities Index Fund

All Information as of June 30, 2021 unless otherwise indicated Asset Management SWRSX Schwab Treasury Inflation Protected Securities Index Fund Investment objective The fund’s goal is to track as closely as possible, before fees and expenses, the total return of an index composed of inflation-protected U.S. Treasury securities. Fund highlights • A straightforward, low-cost fund with no investment minimum • The Fund can serve as part of the core of a diversified portfolio • Simple access to the U.S. Treasury-Inflation Protected Securities (TIPS) market • Invests in the overall U.S. TIPS market Fund details Cumulative Annualized Performance (%) Total net assets $2,216,208,923 3 Year to 1 3 5 10 Since as of 6/30/21 Inception date 03/31/06 Months Date Year Years Years Years Inception 2 Expense ratio1 0.05% Fund 3.27 1.71 6.45 6.47 4.10 3.23 4.14 Bloomberg Barclays US Treasury Inflation-Linked Ticker symbol SWRSX 3.25 1.73 6.51 6.53 4.17 3.40 4.51 Bond Index (Series-L)3 Number of securities 44 Category Average3 2.93 2.01 7.04 5.93 3.88 2.85 — Distribution frequency Quarterly Annual total returns CUSIP 808517817 20.0 Bloomberg Barclays US Treasury 12.80 10.88 Index name Inflation-Linked Bond 10.0 6.59 8.38 4.47 Index (Series-L) 3.48 2.94 0.0 Portfolio turnover rate 25.39% -1.61 -1.32 Minimum initial investment None -10.0 -8.83 Minimum balance None -20.0 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Loads/12b-1 fees None Performance data quoted represents past performance and is no guarantee of future results. -

IBM 401(K) Plus Plan

IBM 401(k) Plus Plan Individual Fund Flyer Total Stock Market Index Fund This investment option is a unitized fund and not a mutual fund and as such is not registered with the Securities Exchange Commission (SEC). The performance presented for this option may not be calculated in the same manner as the performance of mutual funds. Other data shown also may not be comparable to mutual fund data. The most current fund performance for this option can be found on netbenefits.com/ibm either under Investment Performance & Research or in the Performance & Risk section for this individual fund. Core Building Block Funds 3.IM-C-777D.112 Flyer 20 of 38 Equity Style Value Blend Growth 401(k) Plus Plan Large Market Cap Weightings Total Stock Market Index Fund (as of 12/31/17) Medium This document constitutes part of a prospectus covering securities that have been registered under the Securities Act of 1933. Lighter Medium Small Objective & Strategy Risk/Return Profile Heavier The Total Stock Market Index Fund, a unit- The Total Stock Market Index Fund may When investing in stock funds, short-term ized fund, seeks long-term growth of capital be appropriate for investors with a long- losses (or gains) are common, largely as and income. It attempts to match the invest- term (more than five years) investment a result of sudden movements in stock ment results of the Dow Jones U.S. Total horizon who are seeking long-term prices as views change about the economy Stock Market Index, which covers all regularly and individual companies. -

Applied Investment Management (AIM) Program

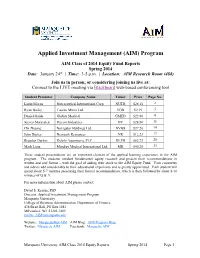

Applied Investment Management (AIM) Program AIM Class of 2014 Equity Fund Reports Spring 2014 Date: January 24th | Time: 3-5 p.m. | Location: AIM Research Room (488) Join us in person, or considering joining us live at: Connect to the LIVE meeting via Blackboard web-based conferencing tool Student Presenter Company Name Ticker Price Page No. Louie Moran Nutraceutical International Corp. NUTR $26.10 2 Ryan Bailey Taseko Mines Ltd. TGB $2.19 5 Daniel Gaide Globus Medical GMED $22.88 8 Steven Marszalek Dycom Industries DY $28.80 11 Chi Zhuang Navigator Holdings Ltd. NVGS $27.20 14 John Hurley Newpark Resources NR $12.23 17 Brendan Durkin Delphi Automotive PLC DLPH $62.73 20 Mark Long Mindray Medical International Ltd. MR $40.20 23 These student presentations are an important element of the applied learning experience in the AIM program. The students conduct fundamental equity research and present their recommendations in written and oral format – with the goal of adding their stock to the AIM Equity Fund. Your comments and advice add considerably to their educational experience and is greatly appreciated. Each student will spend about 5-7 minutes presenting their formal recommendation, which is then followed by about 8-10 minutes of Q & A. For more information about AIM please contact: David S. Krause, PhD Director, Applied Investment Management Program Marquette University College of Business Administration, Department of Finance 436 Straz Hall, PO Box 1881 Milwaukee, WI 53201-1881 mailto: [email protected] Website: MarquetteBuz/AIM AIM Blog: AIM Program Blog Twitter: Marquette AIM Facebook: Marquette AIM Marquette University AIM Class 2014 Equity Reports Spring 2014 Page 1 Nutraceutical International Corp.