Annual Report 2015 Ordinary H-Share Stock Code: 3988 Offshore Preference Share Stock Code: 4601

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Global Fraud & Financial Crime

GLOBAL FRAUD & FINANCIAL CRIME | SEPTEMBER 15-17, 2020 | VIRTUAL EVENT FREE TO ATTEND* GLOBAL FRAUD & FINANCIAL CRIME 3RD ANNUAL | SEPTEMBER 15-17, 2020 | VIRTUAL EVENT Analyzing the risks to determine the solutions in combating Fraud and Financial Crime KEY TOPICS BEING COVERED INCLUDE: COVID-19 APPLICATION FRAUD INTERNAL FRAUD Reviewing the impact of COVID-19 on Detection and identification of fraudulent Identifying internal weaknesses and increased fraudulent activity applications ensuring consistent employee checks GLOBAL COLLABORATION SANCTIONS RISK CULTURE Developing collaboration efforts across Ensuring compliance with global Developing an effective risk culture and institutions and jurisdictions sanctions requirements setting the tone from the top APP FRAUD AI & MACHINE LEARNING TRANSACTION MONITORING Mitigating against authorised Next generation of fraud and financial Reviewing emerging trends in transaction push payment fraud crime prevention techniques monitoring to detect fraudulent activity SPEAKERS INCLUDE Sabeena Liconte Andrew Barnett Andrew Jensen Lester Joseph Head of Legal Head of Fraud Management Global Head of Sanctions Head, Global Financial and Compliance Nordea Scotiabank Crimes Intelligence Group BOC International (USA) Wells Fargo & Company Tim Lutz Corey A. Reason Jayati Chaudhury Dr Liliya Gelemerova Director, Financial Head of Compliance Financial Crime, AML Director, Senior Financial Intelligence Unit Clarien Bank Limited Transaction Monitoring, Crime Advisor U.S. Bank Global IB Lead Commerzbank AG Barclays CO-SPONSORS: ASSOCIATE SPONSOR: CPE ACCREDITATION: [email protected] | +44 (0) 207 164 6582 / +1 888 677 7007 www.cefpro.com/global-fraud GLOBAL FRAUD & FINANCIAL CRIME | SEPTEMBER 15-17, 2020 | VIRTUAL EVENT CO-SPONSORS: Aerospike, the global leader in next-generation, real-time NoSQL data solutions, powers payment transactions and machine learning for fraud prevention at unprecedented speed, scale and low TCO. -

CISI Completes USD3BN Multi-Tranche Senior Bond Offerings for Chemchina

PRESS RELEASE CISI Completes USD3BN Multi-tranche Senior Bond Offerings for ChemChina (Hong Kong, 13 July 2017) China Industrial Securities International Financial Group (“CISI” or the “Group”, stock code: 8407.HK)completed a Reg S USD3bn Multi- tranche senior unsecured bond offering (the “Transaction”) for China National Chemical Corporation (“ChemChina”) on 13 July 2017 as the Joint Bookrunner. The Transaction included USD500mm 3-year bond, USD1.5bn 5-year bond, and USD1.0bn 10-year bond, with coupon rate of 3%,3.5%,4.125% respectively. The expected rating of the senior bond is BBB by S&P and A- by Fitch, and will be listed on the Singapore Stock Exchange(SGX). Since ChemChina is a Chinese key state-owned enterprise, which is not common in international debt capital market year-to-date, the Transaction attracted extensive market attention in the roadshows. The order book of the three tranches were 3.9x oversubscribed, as the orders mounted to USD11.7bn with overwhelming demand from global investors, mostly from Asia and Europe. The final prices, which were 3.027% or T3+150bps,3.532% or T5+165 bps,4.178% or T10+185 bps respectively, tightened by 35 bps from the initial price guidance. The bond also received warm response in the secondary market, as the prices of all tranches rose after the completion of the issuance. CISI served as the Joint Bookrunner of the Transaction as well as the only overseas investment bank with PRC brokerage firm background in the syndicate group. Other syndicate banks in the Transaction included BNP PARIBAS, BOC International, China CITIC Bank International, Credit Suisse, HSBC (B&D), Morgan Stanley, Cr é dit Agricole CIB, Natixis, Rabobank, Shanghai Pudong Development Bank Co., Ltd. -

Board of Directors and Senior Management Directors

Board of Directors and Senior Management DIRECTORS Mr TIAN Guoli Chairman Aged 54, is the Chairman of the Board of Directors and the Chairman of the Nomination Committee of the Company and BOCHK. He is currently the Chairman and Executive Director of BOC and also a Director of BOC (BVI) and BOCHKG. Prior to joining BOC in April 2013, Mr TIAN served as Vice Chairman of the Board of Directors and General Manager of China CITIC Group from December 2010 to April 2013. During this period, he served as Chairman of the Board of Directors and Non-executive Director of China CITIC Bank. From April 1999 to December 2010, Mr TIAN successively served as Vice President and President of China Cinda Asset Management Company, and Chairman of the Board of Directors of China Cinda Asset Management Corporation Limited. From July 1983 to April 1999, Mr TIAN held various positions in China Construction Bank (“CCB”), including General Manager of sub-branch, Deputy Branch General Manager, Department General Manager of CCB Head Office and Assistant Executive President of CCB. Mr TIAN graduated from Hubei Institute of Finance and Economics in 1983 and was awarded a Bachelor’s Degree in Economics. Mr CHEN Siqing Vice Chairman (appointment as Vice Chairman effective from 25 March 2014) Aged 54, is the Vice Chairman of the Board of Directors and a member of the Remuneration Committee and the Nomination Committee of the Company and BOCHK. He is currently the Vice Chairman, Executive Director and President of BOC. He is also a Director of BOC (BVI) and BOCHKG. -

Kuwait China Silk Road Development Fund 1 Initial Proposal DDR

DRAFT Kuwait China Silk Road Development Fund 1 Initial Proposal DDR May 2016 0 Executive Summary • US$1.2 bn Kuwait China Silk Road Development Fund 1 (“Fund 1”) to be jointly sponsored by the designated investors Fund from the State of Kuwait (“Kuwait”) and the People’s Republic of China (“China”) • Fund 1 would be dedicated to invest in three selected strategic projects to support Kuwait to achieve its second five-year Development Plan 2015-2020’s (“Kuwait’s Development Plan“) vision of deepening the country's economic growth potential and economic diversification by moving away from a predominately oil-based economy • The selected projects are involved in sectors aligned with Kuwait’s Development Plan’s targeted sectors including power, renewable energy, desalination and waste management. The selected projects are: Objectives • Az–Zour North Phase 2 Independent Water & Power Project • The Kabd Municipal Solid Waste Project • Al Abdaliyah Integrated Solar Combined Cycle Project • Fund 1 would also support Kuwait’s Development Plan’s initiative to encourage the deployment of public-private partnership (“PPP”) framework to deepen the contribution of the private sector to the country's economic growth; spur private sector job creation; introduce economic efficiencies; and facilitate the adoption of new technologies and know-how DDR • The target size of Fund 1 will be US$1.2 bn • the State of Kuwait • Silk Road Finance Corporation (“SRFC”) to raise a significant portion from designated Chinese investors Commitment • China Communications -

Aftermarket Research Source Book

Aftermarket Research Source Book November 2020 Refinitiv Aftermarket research collections provide the most comprehensive offering in the marketplace, with over 30 million research reports from over 1,900 sources. This document provides an index of the available research sources across the following collections: Subscription / Investext® Collection Pay-Per-View (PPV) / Research Select and Market Research Collections Aftermarket Research Source Book - November 2020 2 New Contributors Added Year to Date 81 contributors from 34 countries have been added to the collection since the beginning of 2020 Australia 3 Ireland 1 South Africa 1 Brazil 1 Japan 4 South Korea 1 Canada 5 Kenya 2 Spain 2 Chile 1 Lebanon 1 Switzerland 1 China 4 Liechtenstein 1 Turkey 2 Colombia 1 Nigeria 4 United Arab Emirates 6 France 2 Peru 1 United Kingdom 5 Germany 1 Philippines 1 United States 11 Ghana 1 Russia 1 Uzbekistan 2 Hong Kong 6 Saudi Arabia 1 Vietnam 1 India 3 Singapore 2 Indonesia 1 Slovenia 1 Contributor Highlights Refinitiv is pleased to announce that BofA Global Research has joined the list of exclusive BofA Global Research contributors only accessible, by qualifying users, through our Aftermarket Research collection. • A team of 285 analysts covering approximately 3,100 companies in 24 global industries – one of the largest research providers worldwide and with more sector coverage than anyone else. • More coverage (2,832) in large- and mid-caps than bulge-bracket peers. • One of the largest producers of equity research with approximately 47,000 documents published in 2019. GraniteShares is an entrepreneurial ETF provider focused on providing innovative, cutting-edge alternative investment solutions. -

The Asset Triple a Regional House and Deal Awards 2013

The Asset Triple A Regional House and Deal Awards 2013 Best deals – Equity Best equity BTS Rail Mass Transit Growth Infrastructure Fund US$2.1 billion IPO Joint global coordinators and bookrunners: Morgan Stanley, Phatra Securities, UBS Sole domestic financial adviser: Phatra Securities Best IPO China Cinda Asset Management Company US$2.5 billion IPO Joint global coordinators: Bank of America Merrill Lynch (BoAML), BOCI Asia, CCB International, Credit Suisse, Goldman Sachs, Morgan Stanley, UBS Joint bookrunners and lead managers (international offering): ABCI Capital, BoAML, BOCI Asia, Bocom International Securities, CCB International, China Merchants Securities, CICC Hong Kong Securities, Cinda International Securities, Citic Securities Corporate Finance, CMB International Capital, Credit Suisse, Essence International Securities, Goldman Sachs, ICBC International Capital, Jefferies, Morgan Stanley, Standard Chartered Securities, UBS Best ADR 58.com US$215 million IPO Joint bookrunners: Citi, Credit Suisse, Morgan Stanley Best mid-cap equity Paul Y Engineering US$411 million share placement and CB Sole placing agent: CLSA Best small-cap equity Just Dial US$167 million IPO Joint bookrunning lead managers: Citi, Morgan Stanley Best block trade No winner Best secondary offering Matahari Department Store US$1.5 billion re-IPO Joint global coordinators and bookrunners: CIMB Investment Bank, Morgan Stanley, UBS Underwriters: Mandiri Sekuritas, Maybank Investment Bank, Standard Chartered Best Reit Mapletree Greater China Commercial Trust S$1.68 -

Table of Contents ○○○○○○○○○○○○○○○○○○○

Table of Contents ○○○○○○○○○○○○○○○○○○○ Financial Highlights ○○○○○○○○○○○○○ 2 ○○○○○○○○○○○ Our Mission ○○○○○○○○○○○○○○○○○○○○○○○○○ 4 Honorary Chairperson of the Board ○○○○○○○○○○○○○○○○○○○○○○ 5 ○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○ 2004 Milestones ○○○○ 6 Message from the Chairman ○○○○○○○○○○○○○○○○○○○○○○○○○○○12 Bank Information ○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○14 Organizational Chart ○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○15 Directors, Supervisors, Senior Management and Staff ○○○○○○○○○○○○18 ○○○○○○○○○○○○○○○○○○○ Joint Stock Reform ○○○○○○○○○○○○○ 25 Corporate Governance ○○○○○○○○○○○○○○○○○○○○○○○○○○○○○○27 ○○○○○○ Management Discussion and Analysis ○○○○○○○○○○○○○○○ 30 ○○○○○○○○○○○○○○○○○ Economic and Regulatory Environment ○○○○○ 30 Financial Statement Analysis ○○○○○○○○○○○○○○○○○○○○○○○○○○○○30 ○○○○○○○○○○○○○○○○○○○○○○○○○○○○○ Business Review ○○○○○○ 40 ○○○○○○○○ Segment Reporting by Region ○○○○○○○○○○○○○○○○○○○ 48 ○○○○○○○○○ Risk Management ○○○○○○○○○○○○○○○○○○○○○○○○○ 50 Financial Statements and Report of the Auditors ○○○○○○○○○○○○○○○62 List of Branches and Subsidiaries ○○○○○○○○○○○○○○○○○○○○○○○○127 Financial Highlights 2004 20031 Profit and loss items (RMB million) Net interest income 84,985 71,904 Non-interest income 19,752 13,781 Operating profit 57,841 47,672 Impairment losses (23,797) (16,432) Profit before tax 34,576 31,419 Net Profit 20,932 21,553 Balance sheet items (RMB million) Loans, net 2,071,693 1,921,131 Total assets 4,270,443 3,979,965 Customer deposits 3,342,477 3,035,956 Total liabilities 4,037,705 3,750,489 Owner's equity 205,351 203,752 Financial ratios(%) Return on average total assets 0.61 0.68 Return on average owner’s equity 10.04 10.582 Non-performing loan ratio 5.12 16.28 Provision coverage ratio 68.02 67.29 Cost to income ratio 40.02 39.73 Capital adequacy ratio 10.04 N/A 1 The profit and loss items and financial ratios for 2003 exclude the net gain from the sale of shares of Bank of China (Hong Kong) Limited (‘BOCHK’) in the amount of RMB 7,154 million. -

1Q 2019 Relationship Management Purpose-Built for Finance Learn More at Affinity.Co

Co-sponsored by Global League Tables 1Q 2019 Relationship Management Purpose-Built for Finance Learn more at affinity.co IMPROVE ELIMINATE SUPPORT DISCOVER PROPIERTARY CROSSING YOUR NEW EXECUTIVE DEAL FLOW WIRES PORTFOLIO CONNECTIONS Learn why 500+ firms use Affinity's patented technology to leverage their network and increase deal flow “Within weeks of moving “The biggest problems Affinity “Let’s be honest, no one wants to Affinity, we were able to helps me solve are how to to use Salesforce reporting. easily discover and manage track all of my activity and how Affinity isn’t just better for most the 1,000s of entrepreneur to prioritize my time. It makes teams, it’ll make the difference and venture community me a better investor. All of the between managing your relationships already latent things I need to do on a day-to- pipeline to success, versus not within our team." day basis I now do in Affinity.” tracking it at all.” ERIC EMMONS KYLE LUI KEVIN ZHANG Managing Director Partner Principal MassMutual Ventures DCM Ventures Bain Capital Ventures [email protected]@affinity.co AffinityAffinity is a relationship is a relationship intelligence intelligence platform platform built to builtexpand to expandand evolve and theevolve traditional the traditional CRM. AffinityCRM. Affinityinstantly instantly surfaces surfaces all all www.affinity.cowww.affinity.co of yourof team’s your team’sdata to data show to you show who you is bestwho issuited best tosuited make to the make crucial the crucialintroductions introductions you need you to need close to your close next your big next deal. big deal. -

Sinic Holdings (Group) Company Limited 新力控股(集團)有限公司 (Incorporated in the Cayman Island with Limited Liability) (Stock Code: 2103)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. This announcement does not constitute an offer to sell or the solicitation of an offer to buy any securities in the United States or any other jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. The securities referred to herein will not be registered under the Securities Act, and may not be offered or sold in the United States except pursuant to an exemption from, or a transaction not subject to, the registration requirements of the Securities Act. Any public offering of securities to be made in the United States will be made by means of a prospectus. Such prospectus will contain detailed information about the company making the offer and its management and financial statements. The Company does not intend to make any public offering of securities in the United States. The communication of this announcement and any other document or materials relating to the issue of the Notes offered hereby is not being made, and such documents and/or materials have not been approved, by an authorized person for the purposes of section 21 of the United Kingdom’s Financial Services and Markets Act 2000, as amended (the “FSMA”). -

Ukef Aviation Finance Boc Aviation Latam Eetc Investing in Lessors Black Swans

ISSUE TWENTYSIX MAY/JUNE 2015 THE LEADING GLOBAL PUBLICATION FOR OPERATORS OF AND INVESTORS IN AIRCRAFT AND ENGINES UKEF AVIATION FINANCE BOC AVIATION LATAM EETC INVESTING IN LESSORS BLACK SWANS www.aviationnews-online.com Talking Bonds Following on from the article in Issue 25 on corporate bond issuance, Airline Economics speaks to Robert Martin, chief executive of BOC Aviation, about the lessor’s financing strategy. n March 2015, the global aircraft billion Global Medium Term Note to 28% of its total debt portfolio today. leasing company, BOC Aviation, (GMTN) Program. The largest share of its portfolio remains launched its inaugural issuance This is BOC Aviation’s largest bond commercial bank debt, which it has of Rule 144A/Regulation S transaction to date. Over the past three traditionally used for its funding needs, US$750 million five-year fixed years, the company has been steadily with export credit-guaranteed funding Irate senior unsecured notes, which growing the capital markets portion of its comprising around 20% of its total was issued under BOC Aviation’s US$5 overall debt financing portfolio, from 5% portfolio. BOC Aviation’s debt portfolio 32 Airline Economics May/June 2015 www.airlineeconomics.co will continue to change since the lessor “In our industry, you need to make turns, we have those sources of funding has another US$2bn remaining to issue sure that you maintain your access with export credit as a backstop and our under its US$5bn GMTN program. to debt at all points in the cycle,” says parent company Bank of China.” Robert Martin, chief executive of BOC Martin. -

CO., LTD. (Incorporated in the People’S Republic of China with Limited Liability)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. This announcement is for information purposes only and does not constitute an invitation or offer to acquire, purchase or subscribe for securities. NOTICE OF LISTING ON THE STOCK EXCHANGE OF HONG KONG LIMITED BRIGHT FOOD HONG KONG LIMITED (incorporated in Hong Kong with limited liability) U.S.$500,000,000 3.00 per cent. Guaranteed Notes due 2018 (the “Notes”) (Stock Code: 5948) unconditionally and irrevocably guaranteed by BRIGHT FOOD (GROUP) CO., LTD. (incorporated in the People’s Republic of China with limited liability) Joint Global Coordinators (in alphabetical order) BOC International HSBC The Royal Bank of Scotland Joint Lead Managers and Joint Bookrunners (in alphabetical order) ANZ Bank of Communications Co., Ltd. Barclays Hong Kong Branch BOC International HSBC ING J.P. Morgan National Australia Bank Limited Rabobank International The Royal Bank of Scotland Application has been made to The Stock Exchange of Hong Kong Limited for the listing of and permission to deal in the Notes by way of debt issues to professional investors only as described in the Offering Circular relating thereto dated 13 May 2013. Permission for the listing of, and dealing in, the Notes is expected to become effective on 22 May 2013. Hong Kong, 21 May 2013 As at the date of this announcement, the directors of Bright Food Hong Kong Limited are CAO Xiaofeng and LI Lin. -

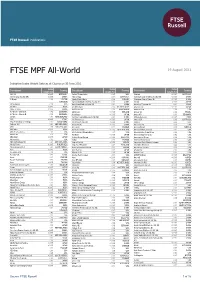

MPF All-World

2 FTSE Russell Publications 19 August 2021 FTSE MPF All-World Indicative Index Weight Data as at Closing on 30 June 2021 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) 1&1 AG <0.005 GERMANY Agilent Technologies 0.07 USA Alumina <0.005 AUSTRALIA 360 Security (A) (SC SH) <0.005 CHINA AGL Energy 0.01 AUSTRALIA Aluminum Corp of China (A) (SC SH) <0.005 CHINA 3i Group 0.02 UNITED Agnico Eagle Mines 0.02 CANADA Aluminum Corp of China (H) <0.005 CHINA KINGDOM Agricultural Bank of China (A) (SC SH) 0.01 CHINA Amada <0.005 JAPAN 3M Company 0.18 USA Agricultural Bank of China (H) 0.02 CHINA Amadeus IT Group SA 0.05 SPAIN 3M India <0.005 INDIA Ahold Delhaize 0.05 NETHERLANDS Amano Corp <0.005 JAPAN 3SBio (P Chip) <0.005 CHINA AIA Group Ltd. 0.23 HONG KONG Amazon.Com 2.28 USA A P Moller - Maersk A 0.02 DENMARK AIB Group <0.005 IRELAND Ambev SA 0.02 BRAZIL A P Moller - Maersk B 0.03 DENMARK Aica Kogyo <0.005 JAPAN Ambu A/S 0.01 DENMARK a2 Milk 0.01 NEW ZEALAND Aier Eye Hospital Group (A) (SC SZ) 0.01 CHINA Ambuja Cements <0.005 INDIA A2A <0.005 ITALY Ain Pharmaciez <0.005 JAPAN Amcor CDI 0.03 AUSTRALIA AAC Technologies Holdings 0.01 HONG KONG Air China (A) (SC SH) <0.005 CHINA Amdocs 0.02 USA Aalberts NV 0.01 NETHERLANDS Air China (H) <0.005 CHINA Ameren Corp 0.03 USA ABB 0.09 SWITZERLAND Air Liquide 0.12 FRANCE America Movil L 0.03 MEXICO ABB India <0.005 INDIA Air New Zealand <0.005 NEW ZEALAND American Airlines Group 0.01 USA Abbott Laboratories 0.31 USA Air Products & Chemicals Inc