UBA Member Bankers Association Bank Ceos

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Former DFCU Bank Bosses Charged Over Global Fund Scam

4 NEW VISION, Thursday, April 3, 2014 NATIONAL NEWS Former DFCU Bank bosses charged over Global Fund scam By Edward Anyoli Lule, while employed by Lule through manipulation of 300 sub-recipients and DFCU – a company in which Former Global Global Fund foreign exchange, individuals be audited further Two former managers of DFCU the Government had shares – falsely claiming that it was and that former health minister, Bank have been charged with directed the bank to convert Fund boss Dr. commission fees for soliciting Maj. Gen. Jim Muhwezi and abuse of office, costing the $2m Global Fund money into Global Fund business. his deputies; Mike Mukula Government sh479m. the local currency at an inflated Muhebwa was last Kantuntu, Lule and Kituuma and Alex Kamugisha, be Robert Katuntu, the former foreign exchange rate of Magala (a city lawyer, who is prosecuted. managing director of DFCU sh1,839 per dollar, which was week charged with summoned to appear in court This resulted into the and Godffrey Lule, the bank’s higher than the rate of sh1,815, on April 11) are jointly facing establishment of the anti- former head of treasury, were raising a difference of sh48m. causing financial the charges with Dr. Tiberius corruption division of the yesterday charged before the On another charge, Lule Muhebwa, the former Global High Court in December Anti-Corruption Court chief is accused of fraudulently loss of sh108m Fund project co-ordinator. 2008, which has convicted magistrate. They denied the directing the bank staff to Muhebwa has been charged two suspects; Teddy Cheeye charges and were granted cash convert $1m Global Fund with causing financial loss of the presidential adviser on bail of sh3m each. -

Tumusiime Claire.Pdf

EVALUATION OF CREDIT POLICY MANAGEMENT AND PERFORMANCE OF MICRO-FINANCE INSTITUTIONS IN UGANDA A CASE STUDY OF PRIDE MICROFINANCE BY Tumusiime Clare BBA/6067/ 41/DU SUPERVISED BY: Mr. Naleela Kizito RESEARCH REPORT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF A BACHELOR DEGREE IN BUSINESS ADMINISTRATION AND MANAGEMENT OF KAMP AlA INTERNATIONAL UNIVERSITY • August, 2006 DECLARATION I Tumusiime Clare hereby declare that the following research report under the title "Evaluation of Credit Policy Management and Performance of Micro finance Institutions" has never been submitted to any college or university for any award. It is my original work. Signed: ~ ------------------ Tumusiime Clare BBA/ 6067/ 41/DU Date~. ~r.!.~.h .~_gl.U.J] .... ~ .Qh/' APPROVAL This research report on "evaluation of credit policy and performance of Micro- finance Institutions" in Uganda has been carried out by Tumusiime Clare under my supervision and is now ready for submission to Kampala International University. Signed:---~ ------------------------·· Mr. Naleela Kizito S~rvisor Date: ..... ~3 .. l.~ .. r.~.fe................ 11 DEDICATION I dedicate this project to my mum and Dad, Father Bonny, my sisters and brothers. May the Lord God reward them more abundantly. l1l ACKNOWLEDGEMENT With deep pleasure I wish to extend my sincere appreciation to Almighty God for giving me life and blessing my studies. My esteem love goes to my brothers; Francis, Justus, Julius, and my sisters; Rita and Sharon who had to endure a long period of struggles to support me as their sister. My sincere thanks also go to the entire staff of Kampala International University for their love and services rendered. -

Public Notice

PUBLIC NOTICE PROVISIONAL LIST OF TAXPAYERS EXEMPTED FROM 6% WITHHOLDING TAX FOR JANUARY – JUNE 2016 Section 119 (5) (f) (ii) of the Income Tax Act, Cap. 340 Uganda Revenue Authority hereby notifies the public that the list of taxpayers below, having satisfactorily fulfilled the requirements for this facility; will be exempted from 6% withholding tax for the period 1st January 2016 to 30th June 2016 PROVISIONAL WITHHOLDING TAX LIST FOR THE PERIOD JANUARY - JUNE 2016 SN TIN TAXPAYER NAME 1 1000380928 3R AGRO INDUSTRIES LIMITED 2 1000049868 3-Z FOUNDATION (U) LTD 3 1000024265 ABC CAPITAL BANK LIMITED 4 1000033223 AFRICA POLYSACK INDUSTRIES LIMITED 5 1000482081 AFRICAN FIELD EPIDEMIOLOGY NETWORK LTD 6 1000134272 AFRICAN FINE COFFEES ASSOCIATION 7 1000034607 AFRICAN QUEEN LIMITED 8 1000025846 APPLIANCE WORLD LIMITED 9 1000317043 BALYA STINT HARDWARE LIMITED 10 1000025663 BANK OF AFRICA - UGANDA LTD 11 1000025701 BANK OF BARODA (U) LIMITED 12 1000028435 BANK OF UGANDA 13 1000027755 BARCLAYS BANK (U) LTD. BAYLOR COLLEGE OF MEDICINE CHILDRENS FOUNDATION 14 1000098610 UGANDA 15 1000026105 BIDCO UGANDA LIMITED 16 1000026050 BOLLORE AFRICA LOGISTICS UGANDA LIMITED 17 1000038228 BRITISH AIRWAYS 18 1000124037 BYANSI FISHERIES LTD 19 1000024548 CENTENARY RURAL DEVELOPMENT BANK LIMITED 20 1000024303 CENTURY BOTTLING CO. LTD. 21 1001017514 CHILDREN AT RISK ACTION NETWORK 22 1000691587 CHIMPANZEE SANCTUARY & WILDLIFE 23 1000028566 CITIBANK UGANDA LIMITED 24 1000026312 CITY OIL (U) LIMITED 25 1000024410 CIVICON LIMITED 26 1000023516 CIVIL AVIATION AUTHORITY -

Managing Director's Statement

Summary Financial Statements Housing Finance Bank 2020 Performance Highlights For The Year Ended 31 December 2020 Report Of The Independent Auditor On The Summary Financial Statements To The Shareholders Of Housing Finance Bank Limited I II Statement Of Financial Position As At 31 December 2020 Our Opinion The Audited Financial Statements And 2020 2019 Our Report Thereon Assets Ushs '000 Ushs '000 In our opinion, the accompanying sum- Cash and balances with the central bank 78,801,610 115,135,554 mary financial statements of Housing Fi- We expressed an unmodified audit opin- Deposits and balances due from other banks 48,823,936 56,228,534 nance Bank Limited (“ the Bank”) for the ion on the audited financial statements of Government securities at FVPL 146,919,395 1,364,818 1,108 BN 654.2 BN 551 BN 20.69 BN 250.1 BN year ended 31 December 2020 are con- the Bank for the year ended 31 December Government securities at amortised cost 212,748,084 117,349,831 Total Assets Customer Net Loans Profit After Shareholders’ sistent, in all material respects, with the 2020 in our report dated 21 April 2021. Loans and advances (net) 550,608,755 553,524,657 Deposits Tax Equity audited financial statements of the Bank That report also includes the communi- Other assets 22,568,678 23,346,460 for the year ended 31 December 2020, in cation of a key audit matter. A key audit Property and equipment 31,789,871 29,171,335 Total assets Customer Net loans and Profit After Tax Shareholders’ accordance with the Financial Institutions matter is that which in our professional Intangible assets 7,032,093 6,212,368 increased by 22% deposits advances to declined by 8% equity increased (External Auditors) Regulations, 2010 and judgement, is of most significance in our Capital work in progress 739,311 2,002,197 from Shs 912 increased by 17% customers from Shs 22.5 by 18% from Shs the Financial Institutions Act, 2004. -

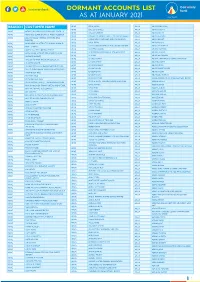

1612517024List of Dormant Accounts.Pdf

DORMANT ACCOUNTS LIST AS AT JANUARY 2021 BRANCH CUSTOMER NAME APAC OKAE JASPER ARUA ABIRIGA ABUNASA APAC OKELLO CHARLES ARUA ABIRIGA AGATA APAC ACHOLI INN BMU CO.OPERATIVE SOCIETY APAC OKELLO ERIAKIM ARUA ABIRIGA JOHN APAC ADONGO EUNICE KAY ITF ACEN REBECCA . APAC OKELLO PATRICK IN TRUST FOR OGORO ISAIAH . ARUA ABIRU BEATRICE APAC ADUKU ROAD VEHICLE OWNERS AND OKIBA NELSON GEORGE AND OMODI JAMES . ABIRU KNIGHT DRIVERS APAC ARUA OKOL DENIS ABIYO BOSCO APAC AKAKI BENSON INTRUST FOR AKAKI RONALD . APAC ARUA OKONO DAUDI INTRUST FOR OKONO LAKANA . ABRAHAM WAFULA APAC AKELLO ANNA APAC ARUA OKWERA LAKANA ABUDALLA MUSA APAC AKETO YOUTH IN DEVELOPMENT APAC ARUA OLELPEK PRIMARY SCHOOL PTA ACCOUNT ABUKO ONGUA APAC AKOL SARAH IN TRUST FOR AYANG PIUS JOB . APAC ARUA OLIK RAY ABUKUAM IBRAHIM APAC AKONGO HARRIET APAC ARUA OLOBO TONNY ABUMA STEPHEN ITO ASIBAZU PATIENCE . APAC AKULLU KEVIN IN TRUST OF OLAL SILAS . APAC ARUA OMARA CHRIST ABUME JOSEPH APAC ALABA ROZOLINE APAC ARUA OMARA RONALD ABURA ISMAIL APAC ALFRED OMARA I.T.F GERALD EBONG OMARA . APAC ARUA OMING LAMEX ABURE CHRISTOPHER APAC ALUPO CHRISTINE IN TRUST FOR ELOYU JOVIN . APAC ARUA ONGOM JIMMY ABURE YASSIN APAC AMONG BEATRICE APAC ARUA ONGOM SILVIA ABUTALIBU AYIMANI APAC ANAM PATRICK APAC ARUA ONONO SIMON ACABE WANDI POULTRY DEVELPMENT GROUP APAC ANYANGO BEATRASE APAC ARUA ONOTE IRWOT VILLAGE SAVINGS AND LOAN ACEMA ASSAFU APAC ANYANZO MICHEAL ITF TIZA BRENDA EVELYN . APAC ARUA OPIO JASPHER ACEMA DAVID APAC APAC BODABODA TRANSPORTERS AND SPECIAL APAC ARUA OPIO MARY ACEMA ZUBEIR APAC APALIKA FARMERS ASSOCIATION APAC ARUA OPIO RIGAN ACHEMA ALAHAI APAC APILI JUDITH APAC ARUA OPIO SAM ACHIDRI RASULU APAC APIO BENA IN TRUST OF ODUR JONAN AKOC . -

THE REPUBLIC of UGANDA in the CHIEF MAGISTRATES COURT of MAKINDYE at MAKINDYE CRIMINAL REGISTRY CAUSELIST for the SITTINGS of : 07-10-2019 to 11-10-2019

THE REPUBLIC OF UGANDA IN THE CHIEF MAGISTRATES COURT OF MAKINDYE AT MAKINDYE CRIMINAL REGISTRY CAUSELIST FOR THE SITTINGS OF : 07-10-2019 to 11-10-2019 MONDAY, 07-OCT-2019 MAGISTRATE GRADE I MBABAZI EDITH BEFORE:: MARY Case Nature of Time Case number Pares Charge CRB No Sing Type Category Appl./Appeal Hearing - Criminal UGANDA VS 1. 09:00 MAK-00-CR-CO-1260-2018 THEFT Kabalagala/1118/2018 prosecuon Offence BIKOLIMANA ALEX case UGANDA VS BUKENYA STEALING BY AGENTS- Hearing - Criminal 2. 09:00 MAK-00-CR-CO-0961-2018 BRIAN & KAWOOYA PROPERTY WHICH HAS Katwe/854/2018 prosecuon Offence FRED BEEN RECEIV case UGANDA VS Hearing - Traffic TRAFFIC-RECKLESS 3. 09:00 MAK-00-CR-TO-0010-2019 MUSINGUZI Katwe/22/2019 prosecuon Offence DRIVING CHRISTOPHER case Hearing - Criminal UGANDA VS NSUBUGA 4. 09:00 MAK-00-CR-CO-0847-2019 BREAKING/BURGLARY-(A-B) Katwe/1155/2019 prosecuon Offence JAMIRU case Hearing - Criminal UGANDA VS KAVUMA 5. 09:00 MAK-00-CR-CO-0606-2019 STEALING VEHICLE Katwe/2000/2018 prosecuon Offence ABDUL case Hearing - Criminal UGANDA VS KIBIRIGE 6. 09:00 MAK-00-CR-CO-0511-2019 THEFT Kabalagala/542/2019 prosecuon Offence DAN case Hearing - Criminal UGANDA VS MUGISHA 7. 09:00 MAK-00-CR-CO-0169-2019 THEFT Kabalagala/152/2019 prosecuon Offence ABEL case UGANDA VS Hearing - Criminal 8. 09:00 MAK-00-CR-CO-1451-2018 SSEMWOGERERE BREAKING/BURGLARY-(A-B) Kabalagala/129/2018 prosecuon Offence MATIYA case 9. 09:00 MAK-00-CR-CO-1218-2018 Criminal UGANDA VS KANGABE BREAKING/BURGLARY-(A-B) Katwe/1533/2018 Hearing - Offence KRARISA prosecuon case CARELESS OR Hearing - Traffic UGANDA VS MUJUNI 10. -

Bernard Bahemuka

Resume: Bernard Bahemuka Personal Information Application Title CHIEF CREDIT OFFICE First Name Bernard Middle Name N/A Last Name Bahemuka Email Address [email protected] Cell Nationality Uganda Gender Male Category Banking/ Finance Sub Category Private Banking Job Type Full-Time Highest Education University Total Experience 16 Year Date of Birth 27-03-1977 Work Phone +2560782366689 Home Phone N/A Date you can start 01-10-2020 Driving License Yes License No. 10143096/2/1 Searchable Yes I am Available Yes Address Address Address Hoima District City Hoima State N/A Country Uganda Institutes Institute Kampala International University City Kampala State N/A Country Uganda Address Kampala,Uganda Certificate Name Bachelors Degree in Business Administration Study Area Accounting & Management Institute Institute Of Teachers Education Kyambogo City Kampala State N/A Country Uganda Address Kampala, Uganda Certificate Name Diploma in Business Education Study Area Business Education Employers Employer Employer Encot Microfinance Limited Position Credit Manager Responsibilities Maintain and preserve Credit Operations policies , manage Credit Operations activities,Manage Credit Risk and grow the portfolio and clientele qualitatively Pay Upon Leaving 5,000,000 uganda Shillings Supervisor Chief Operating Officer From Date 01-10-2017 To Date N/A Leave Reason Carrier Growth City Kampala State N/A Country Uganda Phone N/A Address P.O.Box 389 Masindi Employer Employer Finance Trust Bank Position Branch Manager Responsibilities Over seeing general Branch -

Undp Uganda Annual Report 2014

2014 Annual report UNITED NATIONS DEVELOPMENT PROGRAMME - UGANDA About UNDP We are committed to supporting the Government of Uganda to achieve sustainable development, create opportunities for empowerment, protect the environment, minimise natural and man-made disasters, build strategic partnerships, and improve the quality of life for all citizens, as set out in the Country Programme Action Plan (CPAP) for the years 2010 to 2015, and the United Nations Development Assistance Framework (UNDAF) for Uganda. UNDP UGANDA ANNUAL REPORT 2014 Publisher: UNDP-Uganda Published by the Communications Unit: Sheila C. Kulubya - Communication Analyst and Head Unit Doreen Kansiime - Communication Assistant Design & Layout: www.thenomadagency.com Photographs: UNDP Uganda 2014 Copyright © 2014 United Nations Development Programme Annual Report 2014 Contents Foreword 4 Democratic Governance 6 Community Policing promotes peace in Karamoja Region 10 Inclusive and Sustainable Development 12 Value Chains: Supporting inclusive markets in Agriculture 17 and Trade to improve lives of farmers in Uganda Climate and Disaster Resilience 20 Gender Equality and Women Empowerment 25 Equipping girls with vocational skills to increase their chances 27 of employment UN Volunteers Programme in Uganda 29 The Post 2015 Process in Uganda 30 Our 2014 Highlights 34 3 Foreword Dear Reader, am pleased to present to you this Annual Report, which chronicles our key programme successes and stories of human empowerment and community Itransformation in Uganda in 2014. Overall, the country continued to make progress in pursuit of sustainable development, maintaining an average growth rate of 6.4 percent in 2013, and a ranking of 19th out of 52 countries in the Ibrahim Index of African Governance. -

SERENA HOTELS and an Extension to the 5-Star Profile of the Flagship Kampala Serena Hotel, SAFARI LODGES .HOTELS

FACT SHEET The Resort is styled to replicate the lines of a classically rustic Roman Villa which might just as easily stand amid the sunflowers of the Tuscan Hills, as on the shores of Africa’s largest lake. This resort will offer both a contrast SERENA HOTELS and an extension to the 5-star profile of the flagship Kampala Serena Hotel, SAFARI LODGES .HOTELS. RESORTS thus ensuring that the Serena Portfolio embraces all the aspects of Uganda’s social and cooperate life. Future developments on the property include a golf-course, marina and luxury residential complex. LAKE VICTORIA SERENA RESORT GUESTROOM INFORMATION DINING AND BAR ACTIVITIES Total number of rooms and suites The Citadel All Day Restaurant 124 The Lake View Pool Terrace Standard rooms 114 The Courtyard Lounge General Manager Executive rooms 8 The Piano Bar Terrace Wilfred Shirima State Suites 2 Kigo Lounge Bar Direct Contact Lake Victoria Serena Resort FRONT DESK SERVICES P.O.Box 37761, Kampala, Uganda Express Check-in and Check-out BUSINESS CENTER SERVICES Lweza-Kigo Road, Off Entebbe Road facilities Fully equipped Business Tel: +256 41 7121 000 24 hrs Currency Exchange Center. Fax: +256 41 7121 550 Facilities Private boardrooms Email: [email protected] Secretarial Services Website: www.serenahotels.com Faxing Services TRANSPORTATION TO/FROM THE HOTEL Entebbe International Airport is CONFERENCE ROOM 35 kilometers away. FACILITIES Taxis and Shuttle services Reservations Spacious, well appointed Available Kampala Serena Hotel meeting rooms with modern Limousine Services Available Tel: +256 41 4309 000 facilities Fax: +256 41 4259 130 Banquet and catering services Email: [email protected] GUEST ROOM FACILITIES Remote controlled air conditioning Other Conference facilities in all the rooms. -

Absa Bank 22

Uganda Bankers’ Association Annual Report 2020 Promoting Partnerships Transforming Banking Uganda Bankers’ Association Annual Report 3 Content About Uganda 6 Bankers' Association UBA Structure and 9 Governance UBA Member 10 Bank CEOs 15 UBA Executive Committee 2020 16 UBA Secretariat Management Team UBA Committee 17 Representatives 2020 Content Message from the 20 UBA Chairman Message from the 40 Executive Director UBA Activities 42 2020 CSR & UBA Member 62 Bank Activities Financial Statements for the Year Ended 31 70 December 2020 5 About Uganda Bankers' Association Commercial 25 banks Development 02 Banks Tier 2 & 3 Financial 09 Institutions ganda Bankers’ Association (UBA) is a membership based organization for financial institutions licensed and supervised by Bank of Uganda. Established in 1981, UBA is currently made up of 25 commercial banks, 2 development Banks (Uganda Development Bank and East African Development Bank) and 9 Tier 2 & Tier 3 Financial Institutions (FINCA, Pride Microfinance Limited, Post Bank, Top Finance , Yako Microfinance, UGAFODE, UEFC, Brac Uganda Bank and Mercantile Credit Bank). 6 • Promote and represent the interests of the The UBA’s member banks, • Develop and maintain a code of ethics and best banking practices among its mandate membership. • Encourage & undertake high quality policy is to; development initiatives and research on the banking sector, including trends, key issues & drivers impacting on or influencing the industry and national development processes therein through partnerships in banking & finance, in collaboration with other agencies (local, regional, international including academia) and research networks to generate new and original policy insights. • Develop and deliver advocacy strategies to influence relevant stakeholders and achieve policy changes at industry and national level. -

Notes to the Financial Statements 34

Secure Online Payments Open your online store to international customers by accepting & payments. Transactions are settled NO FOREX UGX USD in both UGX and USD EXPOSURE Powered by for more Information 0417 719229 [email protected] XpressPay is a registered TradeMark Secure Online Payments 2016 ANNUAL REPORT Open your online store to international customers by accepting & payments. Transactions are settled NO FOREX UGX USD in both UGX and USD EXPOSURE Powered by for more Information 0417 719229 [email protected] XpressPay is a registered TradeMark ENJOY INTEREST OF UP TO 7% P.A. WITH OUR PREMIUM CURRENT ACCOUNT INTEREST IS CALCULATED DAILY AND PAID MONTHLY. CONTENTS Overview About Us 6 Our Branch Network 7 Our Corporate Social Responsibility 8 Corporate Information 11 Governance Chairman’s Statement 12 Managing Director/CEO’s Statement 14 Board of Directors’ Profiles 18 Executive Committee 20 Directors’ Report 21 Statement of Directors’ Responsibilities 23 Report of the Independent Auditors 24 Orient Bank Limited Annual Report and Consolidated 04 Financial Statements For the year ended 31 December 2016 OVERVIEW GOVERNANCE FINANCIAL STATEMENTS Financial Statements Consolidated Statement of Comprehensive Income 26 Bank Statement of Comprehensive Income 27 Consolidated Statement of Financial Position 28 Bank Statement of Financial Position 29 Consolidated Statement of Changes in Equity 30 Bank Statement of Changes in Equity 31 Consolidated Statement of Cash flows 32 Bank Statement of Cash flows 33 Notes to the Financial Statements 34 Orient Bank Limited Annual Report and Consolidated Financial Statements For the year ended 31 December 2016 05 ...Think Possibilities ABOUT US Orient Bank is a leading private sector commercial Bank in Uganda. -

List of URA Service Offices Callcenter Toll Free Line: 0800117000 Email: [email protected] Facebook: @Urapage Twitter: @Urauganda

List of URA Service Offices Callcenter Toll free line: 0800117000 Email: [email protected] Facebook: @URApage Twitter: @URAuganda CENTRAL REGION ( Kampala, Wakiso, Entebbe, Mukono) s/n Station Location Tax Heads URA Head URA Tower , plot M 193/4 Nakawa Industrial Ara, 1 Domestic Taxes/Customs Office P.O. Box 7279, Kampala 2 Katwe Branch Finance Trust Bank, Plot No 115 & 121. Domestic Taxes 3 Bwaise Branch Diamond Trust Bank,Bombo Road Domestic Taxes 4 William Street Post Bank, Plot 68/70 Domestic Taxes Nakivubo 5 Diamond Trust Bank,Ham Shopping Domestic Taxes Branch United Bank of Africa- Aponye Hotel Building Plot 6 William Street Domestic Taxes 17 7 Kampala Road Diamond Trust Building opposite Cham Towers Domestic Taxes 8 Mukono Mukono T.C Domestic Taxes 9 Entebbe Entebbe Kitooro Domestic Taxes 10 Entebbe Entebbe Arrivals section, Airport Customs Nansana T.C, Katonda ya bigera House Block 203 11 Nansana Domestic Taxes Nansana Hoima road Plot 125; Next to new police station 12 Natete Domestic Taxes Natete Birus Mall Plot 1667; KyaliwajalaNamugongoKira Road - 13 Kyaliwajala Domestic Taxes Martyrs Mall. NORTHERN REGION ( East Nile and West Nile) s/n Station Location Tax Heads 1 Vurra Vurra (UG/DRC-Border) Customs 2 Pakwach Pakwach TC Customs 3 Goli Goli (UG/DRC- Border) Customs 4 Padea Padea (UG/DRC- Border) Customs 5 Lia Lia (UG/DRC - Border) Customs 6 Oraba Oraba (UG/S Sudan-Border) Customs 7 Afogi Afogi (UG/S Sudan – Border) Customs 8 Elegu Elegu (UG/S Sudan – Border) Customs 9 Madi-opei Kitgum S/Sudan - Border Customs 10 Kamdini Corner