Housing Market Intelligence Report 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Unit Medic Aids 29 Blackberry Lane, Hasbury, Halesowen, West Midlands

SAFETY DATA SHEET 1. IDENTIFICATION OF THE PREPARATION AND THE COMPANY. Product name. BIODIS Intended Use: QUATERNARY AMMONIUM BASED SANITISER Supplier: Unit Medic Aids 29 Blackberry Lane, Hasbury, Halesowen, West Midlands. B63 4NX TEL: 01215502222 2. COMPOSITION/INFORMATION ON INGREDIENTS. INGREDIENT: EINECS CAS NO CONTENTS SYMBOL Quaternary Ammonium Compounds 264-151-6 63449-41-2 0-1% C,N 21/22 34 50 C13-15 Alcohol Ethoxylate (7EO) 68131-39-5 0-1% Xn Xi 22, 41,50 3. HAZARDS IDENTIFICATION. Not clasified as Hazardous 4. FIRST AID ACTION (SYMPTOMS) 4. FIRST AID ACTION (ACTION) Eye contact: Promptly wash eyes with plenty of water while lifting the eye lids Skin contact: Wash skin with soap and water Inhalation: Not relevant. Inhalation unlikely Ingestion: Do not induce vomiting. Drink a few classes of water or milk. Get medical attention 5. FIRE FIGHTING MEASURES. Extinguishing Media: This material is not flammable. Use extinguishing media appropriate for surrounding fire. If involved in fire, may emit noxious fumes Fire & Explosion Hazards Protective clothing and respiratory protection should be worn when tackling fires involving this product. 6. ACCIDENTAL RELEASE MEASURES. Peronal precautions: No special protective clothing Large spillages or uncontrolled discharges into rivers or streams must be reported to The Environment Agency or other regulatory body Clean-up procedures: Small quantities may be flushed to drains with plenty of water. Large spills: Absorb in vermiculate, dry sand or earth and place into containers. Send for disposal by approved waste collector. 7. HANDLING AND STORAGE. Handling: No specific usage precautions noted. Store at moderate temperatures in dry, well ventilated area. -

New Members at 12.2106

SCHOOLS FORUM MEMBERSHIP at 1.2.2016 GOVERNORS/Non Schools - 3 year term of office Headteachers/PRU - 3 year term of office 1 May 2013 1 May 2014 1 May 2015 1 November 1 November 1 November Date of SCHOOL MEMBERS DUDLEY SCHOOLS FORUM CONSTITUTION to 30 April to 30 April to 30 April 2013 to 31 2014 to 31 2015 to 31 Appointment 2016 2017 2018 October 2016 October 2017 October 2018 Nursery School Headteachers One nursery headteacher Netherton Park Nursery Mrs Helen Ruffles, Netherton Park Children's Centre, Netherton, Dudley DY2 9QF Nov-13 √ Primary School Headteachers One primary school headteacher for each of the five townships Mrs M Stowe, Crestwood Park, Lapwood Avenue, Crestwood Park Estate, √ Brierley Hill Kingswinford, DY6 8RP Nov-13 Mr Damien Ward, Sledmere Primary, The School Drive, Buffery Road, Dudley, DY2 Central Dudley Nov-15 √ 8EH M/s Pauline Rogers, St Margaret's at Hasbury Church of England Primary School, Halesowen Nov-15 √ Hagley Road, Hasbury, Halesowen, B63 4QD North Dudley Mrs Ruth Wylie, Wrens Nest Primary School, Marigold Crescent, Dudley, DY1 3NX Jan-14 √ Mrs Angela Hannaway , Headteacher, Gigmill Primary, The Broadway, Norton, DY8 Stourbridge Nov-14 √ 3HL. Primary School Governors One primary school governor for each of the five townships Brierley Hill Mr Len Ridney, The Dingle Primary School √ May-13 Mr Brendan Oakley, Sledmere Primary School, Buffery Road, Dudley, West Central Dudley √ May-14 Midlands, DY2 8EH Halesowen Vacant post Halesowen (ex MPW). No Nominations March 15 √ North Dudley Vacant post Dudley North -

Dudley in the County of West Midlands

LOCAL BOUNDARY FOR ENGLAND REPORT HO. LOCAL G BOUNDARY FOR ENGLAND NO. LOCAL OOVKKNKKUT BOUNDARY CO','MISSION FOK fc.'GLAUD CHAIRMAN Sir Nicholas Morrison KCB DEPUTY CHAIRMAN Mr J M Rankin QC MEM3EHS Lady Bowden Mr J T Brockbank Mr R R Thornton CB DL Mr D P Harrison Professor G E Cherry Secretary of State for the Home Department PROPOSALS FOR REVISED ELECTORAL ARRANGEMEMTS FOR THE METROPOLITAN BOROUGH OF DUDLEY IN THE COUNTY OF WEST MIDLANDS 1. We, the Local Government Boundary Commission for England, having carried out our initial review of the electoral arrangements for the metropolitan borough of Dudley in accordance with the requirements of section 63 of, and Schedule 9 to, the Local Government Act 1972, present our proposals for the future electoral arrangements for that borough. 2. In accordance with the procedure laid down in section 60(l) and (2) of the 1972 Act, notice was given on 8 August 1975 that we were to undertake this review. This was incorporated in a consultation letter addressed to the Dudley Borough Council, copies of which were circulated to the West Midlands County Council, the Members of Parliament for the constituencies concerned, and the headquarters of the main political parties. Copies were also sent to the editors of local newspapers circulating in the area and of the local government press. Notices inserted in the local press announced the start of the review and invited comments from members of the public and from interested bodies, 3. Dudley Borough Council were invited to prepare a draft scheme of representation for our consideration. -

Unit Medic Aids 29 Blackberry Lane, Hasbury, Halesowen, West Midlands

SAFETY DATA SHEET 1. IDENTIFICATION OF THE PREPARATION AND THE COMPANY. Product name. BODY SPILL GRANULES Intended Use: EMERGENCY SPILLAGE COMPOUND Supplier: Unit Medic Aids 29 Blackberry Lane, Hasbury, Halesowen, West Midlands. B63 4NX TEL: 01215502222 2. COMPOSITION/INFORMATION ON INGREDIENTS. INGREDIENT: EINECS CAS NO CONTENTS SYMBOL Cross linked Sodium Polyacrylate 9003-04-7 70-90 % Dolomite 16389-88-1 20-30 % Zeolite 1-5 % 3. HAZARDS IDENTIFICATION. Main hazards: No significant hazard 4. FIRST AID ACTION (SYMPTOMS) 4. FIRST AID ACTION (ACTION) Eye contact: Bathe the eye with running water for 15 minutes. If eye irritation persists, consult a specialist. Skin contact: Wash immediately with plenty of soap and water Inhalation: Remove any material from the mouth & free the airway. remove the person to fresh air. Ingestion: Water may be given to wash out the mouth if the person is concious and not convulsing. Seek medical advice if necessary. 5. FIRE FIGHTING MEASURES. Extinguishing Media: If involved in a fire use dry foam powder, water spray. Unsuitable extinguishing media for safety reasons: Carbon Dioxide, water jet. Fire & Explosion Avoid whirling up the material/product because of dust explosion. Hazards 6. ACCIDENTAL RELEASE MEASURES. Peronal precautions: Do not create dust Clean-up procedures: Transfer to a suitable container. Avoid contact with acids. 7. HANDLING AND STORAGE. Handling: Keep in a dry area, Keep in sealed containers. Keep away from children Storage: Avoid wet, humid conditions 8. EXPOSURE CONTROLS & PERSONAL PROTECTION. Respiratory: If the dust level cannot be controlled by ventilation use an approved respirator. Hand: Use latex gloves Eye: Use suitable protective goggles if airborne concentrations are high. -

Delegated Capital Budget

Agenda Item No. 12 Halesowen Area Committee – 24th January 2008 Report of the Area Liaison Officer Delegated Capital Budget Purpose of Report 1. To recommend grants from the Committee’s Capital Budget Allocation and associated matters. Background 2. The criteria against which allocations from the delegated capital budget should be considered are set out in the Appendix. The Area Committee has previously agreed that contributions from the budget will be limited to £5,000 unless exceptional circumstances can be demonstrated. A copy of the applications referred to in this report are available to Members on request. Cradley Girls Group (Barnardos) 3. Cradley Girls Group promotes life and social skills by encouraging members to participate in a wide range of activities that enhance confidence and self esteem. These activities include arts and crafts, taster sports, cookery and social events. 4. The Group has requested funding amounting to £1,000 for a laptop and associated software to promote topics of interest. 5. I have consulted colleagues in the Directorate of Adult, Community and Housing Services who support the application. I am, therefore, recommending a grant of £1,000 for the purchase of these items. UWest Midlands Police (PCSOs) 6. A request has been received for funding from the West Midlands Police to enable the purchase of bikes and associated safety equipment/uniforms for use by two PCSOs who currently cover the Uffmoor, Hayley Green, Hagley Road and Hasbury areas on foot. 7. The application has been submitted through the Friends of Huntingtree Park, who fully supports the application and have confirmed that there has been a significant decrease in anti-social behaviour on the park and nearby areas due to the visibility of PCSOs in and around the area. -

Lettings Policy Jan 2020

Hasbury Christian Fellowship 26 Albert Road, Halesowen, West Midlands, B63 4SW Church Tel: 0121 550 8269 www.hasbury.org Hasbury Christian Fellowship Lettings Policy (January 2020) Rationale At the discretion of the Governing Body of the church (Trustees and Church Council) the church premises may be let to outside organisations during times when the facility is not required by Hasbury Christian Fellowship. This policy ensures that all hirers are given equal opportunities within the guidance set out by the Governing Body. Any hiring of the church premises to persons/organisations will need careful consideration by the Trustees due to equipment and resources in the church premises. Church and other statutory requirements take precedence over any other use. Procedures All hirers should complete an application form, which must be updated on an annual basis. Each request will be considered by the Church Council on behalf of the Trustees using the following criteria: a. To treat all requests in a fair and equitable manner b. Give due regard to equality of opportunity c. To determine who should be responsible for the building during the lettings Booking Arrangements The facilities can be booked through the Church bookings Coordinator at Hasbury Christian Fellowship, 26 Albert Road, Halesowen, West Midlands B63 4SW. [email protected] Charges Charging rates, as set out in the tables below, consist of several elements including: • An administrative charge • Caretaking & basic cleaning charges • Heating • Lighting • Additional cleaning charges may be made if necessary, eg. following spillages on carpets/upholstery. Payments will be made on the day of the hire for one off bookings. -

Appendix 1 Directorate of Education and Lifelong Learning Consultation

Appendix 1 Directorate of Education and Lifelong Learning Consultation Document Consultation on: Primary Education in Halesowen Proposal for the Establishment of a New Voluntary Aided Church of England Primary School for Halesowen. Summary: This consultation proposes the closure of Halesowen CE and Hasbury CE primary schools and their replacement by a new Church of England Aided Primary School serving Halesowen. The Council’s preferred location for the development is the site of the current Hasbury School, although other options are set out in the paper. In addition to setting out the various options for the delivery of the project, the paper provides information about the position of staff and pupils affected by these changes, should they proceed and the likely timetable for the development of the project. Deadline: All responses must be received by 31 January 2004 Consultees: Parents and Carers of pupils attending either school Staff members at both schools The Governing Bodies of both schools All other interested parties Chairs of other Governing Bodies Headteachers Councillors Members of the Lifelong Learning Select Committee Members of Parliament The Black Country Learning and Skills Council Dudley Lifelong Learning Partnership Further Education Colleges Directorate staff Unions and Professional Associations Early Years Development and Childcare Partnership Standing Advisory Council on Religious Education Dudley MBC - Corporate Board Primary Care Trusts West Midlands Police Worcester Diocesan Education Committee Roman Catholic Diocesan -

Dudley MBC and Worcester Diocesan Board of Education

Appendix 4 Dudley Council and Worcester Diocesan Board of Education Part 1 Notice is hereby given in accordance with the School Standards and Framework Act 1998 ("The Act"), that Dudley Council propose: In accordance with section 29(1) of the Act, with effect from 31 August 2006, to discontinue: • Halesowen C of E Primary School, High Street, Halesowen, West Midlands, B63 3BB; and • Hasbury C of E Primary School, Hagley Road, Hasbury, Halesowen, West Midlands, B63 4QD. It is proposed that pupils currently attending these schools will transfer to a new Church of England Voluntary Aided School to be established on the Hasbury site, as proposed in Part 2 below. Admission may also be sought to other schools which have places available. The Halesowen C of E Primary School buildings and site will continue to be used as part of the new school until the required construction work on the Hasbury site is completed. No transport arrangements are required. Part 2 Notice is hereby given in accordance with the School Standards and Framework Act 1998 ("The Act") that Worcester Diocesan Board of Education propose: In accordance with section 28(2) of the Act, to establish a new Voluntary Aided Primary school for 480 boys and girls between the ages of 3 and 11 from 1 September 2006. This will include nursery provision with 60 full time places for children aged 3 - 4 years. There will also be provision for children with significant receptive communication disorders. The provision will have 12 places based on 2 groups of six pupils on a part-time basis (2 days per pupil). -

An Economic Strategy for Dudley Borough

AN ECONOMIC STRATEGY FOR DUDLEY BOROUGH 2008/09 Economic Strategy 2008/2009 - 1 - Economic Regeneration Division Directorate of the Urban Environment Dudley MBC Contents Page Number 1.0 Foreword 3 2.0 Introduction 4 3.0 Strategic Context 7 4.0 Dudley’s Economy 21 5.0 Key Economic Issues – Global, National 38 & Regional 6.0 Strategic Action Plan 42 7.0 Glossary 88 8.0 Appendices 91 Appendix 1 Key Achievements – 2007/08 91 Appendix 2 Strategic Context 98 Appendix 3 Key Partnerships and Agencies Influencing Economic Strategy Implementation 103 Appendix 4 Equality and Diversity 104 Economic Strategy 2008/2009 - 2 - Economic Regeneration Division Directorate of the Urban Environment Dudley MBC 1.0 Foreword Welcome to the seventh edition of the Economic Strategy which brings together the economic regeneration activities that are either planned and/or underway in Dudley Borough, delivered by the Council and a range of external partner organisations, and aimed at achieving sustained growth and development of Dudley’s economy. There have been many achievements during 2007/08. The endorsement of the Phase One Revision to the West Midlands Regional Spatial Strategy, which recognises Brierley Hill as a strategic centre in the Black Country, represents a significant milestone for Dudley Borough and will enable development plans to go ahead for more shops, leisure facilities, offices and housing. In terms of the Borough’s overall economic situation, although Dudley’s position is ahead of its neighbouring authorities in the Black Country in a number of areas – including employment, business formations and unemployment – it still lags behind regional and national performance levels. -

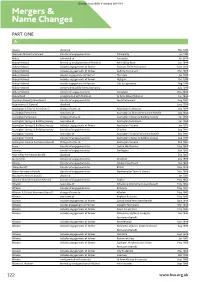

Mergers & Name Changes

Extract from BSA Yearbook 2018/19 Mergers & Name Changes PART ONE A Abacus dissolved Mar 1979 Aberavon Mutual Permanent transfer of engagements to Principality Jan 1974 Abbey rebranded to Santander Jan 2010 Abbey National formed by amalgamation of National with Abbey Road Jan 1944 Abbey National includes engagements of former Swansea Thrift Permanent Sept 1949 Abbey National includes engagements of former Definite Permanent Mar 1968 Abbey National incudes engagements of former The State Jan 1970 Abbey National includes engagements of former Highgate Oct 1974 Abbey National incudes engagements of former Oak Co-operative Aug 1979 Abbey National converted to public limited company July 1989 Abbey National transfer of engagements to Santander Nov 2004 Abbey Road amalgamated with National to form Abbey National Jan 1944 Aberdeen Property Investment transfer of engagements to Leeds Permanent Aug 1961 Accountants & General dissolved June 1939 Accrington & District Perm Benefit change of name to Accrington Permanent July 1938 Accrington Permanent new name of Accrington & District Permanent Benefit July 1938 Accrington Permanent change of name to Accrington Savings & Building Society Jan 1958 Accrington Savings & Building Society new name of Accrington Permanent Jan 1958 Accrington Savings & Building Society includes engagements of former Accrington Victoria Jan 1975 Accrington Savings & Building Society transfer of engagements to Cheshire July 1982 Accrington Victoria new name of Accrington Victoria Permanent Benefit Dec 1961 Accrington Victoria -

Integrated Public Transport Prospectus a World Class Public Transport System for the West Midlands, to Support Long Term Growth and Regeneration Contents

Integrated Public Transport Prospectus A world class public transport system for the West Midlands, to support long term growth and regeneration Contents 1. Context 4 2. Principles Underlying the Development of the Prospectus 14 3. The Prospectus 16 Rail and Rapid Transit Network 22 Principal Bus Corridors 30 Local Bus Networks 33 Complementary Travel Services 39 4. Benefits of the Integrated Public Transport Network 47 5. Key Performance Indicators 48 6 Delivery and Funding 49 7. Supporting Transport and Spatial Development Strategy 52 8. Governance 57 9. Concluding Remarks 58 10. Glossary 59 Appendix 1 Strategic Documents Relating to the Regeneration and Growth Agenda 63 Appendix 2 List of Principal Bus Corridors 67 3 1. Context 1.1 The West Midlands Regional Economic Strategy has will be achieved by accommodating an additional net a vision for the West Midlands Region “to be a global increase of between 365,000 and 398,000 new homes centre where people and business choose to connect”. in the Region by 2026, of which at least 164,500 will Its headline target is to reduce the annual £15 billion be in the Metropolitan Area. regional output gap (GVA) compared to the UK average, through improved productivity and by increasing the 1.5 In order for the Region to succeed in all numbers of people in work: economic inclusion. three areas, the West Midlands Metropolitan Area has to “punch its weight”. This sets the 1.2 These are particularly critical issues in the current scene for the Long Term Regeneration and economic climate where efforts are essential to minimise Growth Agenda of the Metropolitan Area. -

192 Bus Time Schedule & Line Route

192 bus time schedule & line map 192 Halesowen - Hagley - Kidderminster View In Website Mode The 192 bus line (Halesowen - Hagley - Kidderminster) has 2 routes. For regular weekdays, their operation hours are: (1) Halesowen: 7:00 AM - 5:55 PM (2) Kidderminster: 7:35 AM - 6:30 PM Use the Moovit App to ƒnd the closest 192 bus station near you and ƒnd out when is the next 192 bus arriving. Direction: Halesowen 192 bus Time Schedule 28 stops Halesowen Route Timetable: VIEW LINE SCHEDULE Sunday Not Operational Monday 7:00 AM - 5:55 PM Kidderminster Bus Station, Kidderminster Tuesday 7:00 AM - 5:55 PM Town Hall, Kidderminster Exchange Street, Kidderminster Wednesday 7:00 AM - 5:55 PM Oxford Street, Kidderminster Thursday 7:00 AM - 5:55 PM Friday 7:00 AM - 5:55 PM Kidderminster Railway Station, Kidderminster Comberton Hill, Kidderminster Saturday 7:00 AM - 5:55 PM Lorne Street, Kidderminster Villiers Street, Kidderminster 192 bus Info Cricket Ground, Kidderminster Direction: Halesowen Stops: 28 Bowling Green, Greenhill Trip Duration: 34 min Line Summary: Kidderminster Bus Station, Land Oak, Greenhill Kidderminster, Town Hall, Kidderminster, Oxford Street, Kidderminster, Kidderminster Railway Station, 55 Birmingham Road, Kidderminster Kidderminster, Lorne Street, Kidderminster, Villiers Bruce Road, Greenhill Street, Kidderminster, Cricket Ground, Kidderminster, Bowling Green, Greenhill, Land Oak, Greenhill, Bruce Birmingham Road, Kidderminster Road, Greenhill, Hurcot Lane, Hurcott, Hodge Hill Hurcot Lane, Hurcott Nurseries, Hurcott, Park Hall,