Metlifecare Limited 2020 Notice of Meeting and Scheme Booklet

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

December 2013 Investment Survey

MJW Survey – December 2013 Quarterly market overview Investments KiwiSaver Wholesale funds & KiwiSaver results January 2014 Market returns Quarter (%) Year (%) Quarter (%) Year (%) NZX 50 (including imputation credits) 0.2 17.9 NZX NZ Government Bond 0.5 -2.0 S&P/ASX 200 (NZD) 0.1 3.8 NZX Corporate A Grade 0.6 1.9 MSCI World - Local Currency 8.4 28.9 NZ All Swaps -0.3 -1.6 MSCI World - Hedged 8.3 30.6 Barclays Global Aggregate 0.9 2.2 MSCI World - Unhedged 9.3 27.0 Citigroup WGBI 0.7 2.5 MSCI Emerging Markets - Unhedged 3.1 -2.4 90 Day Bank Bill 0.7 2.7 NZX Property -0.5 3.9 NZ $ / US $ -1.2 -0.2 UBS Global Property 0.2 6.5 NZ $ / A $ 3.3 15.8 1 Quarterly market overview NZ cash and fixed interest: It was a better quarter for NZ bonds with the yield on 10 year government stock rising from 4.1% to 4.6% over the period, resulting in a NZX Government Stock Index return for the quarter of 0.5%. For the one year period, the return was a disappointing -2.0%; in contrast the NZX Corporate A Grade Index returned 1.90% for the year. Global bonds did slightly better with the hedged BGA index returning 0.9% for the quarter and 2.2% for the year. Cash continued to achieve solid albeit sub 3% returns at 2.7%. Australasian shares: While NZ investors had a weak quarter, up just 0.2% the 1 year number was solid at 17.9%. -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

The Climate Risk of New Zealand Equities

The Climate Risk of New Zealand Equities Hamish Kennett Ivan Diaz-Rainey Pallab Biswas Introduction/Overview ØExamine the Climate Risk exposure of New Zealand Equities, specifically NZX50 companies ØMeasuring company Transition Risk through collating firm emission data ØCompany Survey and Emission Descriptives ØPredicting Emission Disclosure ØHypothetical Carbon Liabilities 2 Measuring Transition Risk ØTransition Risk through collating firm emissions ØAimed to collate emissions for all the constituents of the NZX50. ØUnique as our dataset consists of Scope 1, Scope 2, and Scope 3 emissions, ESG scores and Emission Intensities for each firm. ØCarbon Disclosure Project (CDP) reports, Thomson Reuters Asset4, Annual reports, Sustainability reports and Certified Emissions Measurement and Reduction Scheme (CEMAR) reports. Ø86% of the market capitilisation of the NZX50. 9 ØScope 1: Classified as direct GHG emissions from sources that are owned or controlled by the company. ØScope 2: Classified as indirect emissions occurring from the generation of purchased electricity. ØScope 3: Classified as other indirect GHG emissions occurring from the activities of the company, but not from sources owned or controlled by the company. (-./01 23-./014) Ø Emission Intensity = 6789 :1;1<=1 4 Company Survey Responses Did not Email No Response to Email Responded to Email Response Company Company Company Air New Zealand Ltd. The a2 Milk Company Ltd. Arvida Group Ltd. Do not report ANZ Group Ltd. EBOS Ltd. Heartland Group Holdings Ltd. Do not report Argosy Property Ltd. Goodman Property Ltd. Metro Performance Glass Ltd. Do not report Chorus Ltd. Infratil Ltd. Pushpay Holdings Ltd. Do not report Contact Energy Ltd. Investore Property Ltd. -

Glen Sowry on the First Lockdown

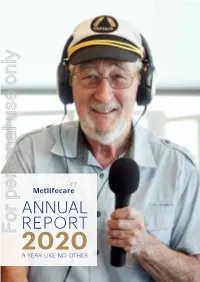

ANNUAL REPORT For personal use only 2020 A YEAR LIKE NO OTHER A Year Like No Other “From the outset, we 002 put the safety and 003 wellbeing of residents and staff at the centre of all decision-making. Our shared philosophy was simple - protecting our team of 7,000.” CEO GLEN SOWRY ON METLIFECARE’S COVID-19 RESPONSE For personal use only Pinesong resident Heather (right) has Front Cover: Resident village DJ Eddy Cross, Forest Lake Gardens a laugh with a friend on Grandparents Day METLIFECARE LIMITED ANNUAL REPORT 2020 Contents COMPANY OVERVIEW 06 At a Glance 08 Chair and CEO Report 16 Performance Overview 17 How We Create Value 18 Thriving Through Disruption 24 Becoming Future Fit 30 A Place to be You • Saluting Our People • Increasing Sustainability 44 Our Board of Directors 46 Our Executive Team 49 Corporate Governance Statement 53 5-Year Performance Summary 55 Underlying Profit Reconciliation 004 GROUP FINANCIAL STATEMENTS 005 58 Consolidated Statement of Comprehensive Income 59 Consolidated Statement of Movements in Equity 60 Consolidated Balance Sheet 61 Consolidated Cash Flow Statement 63 Notes to the Group Financial Statements 91 Independent Auditor’s Report STATUTORY INFORMATION 100 Interests Register 102 Director Information 103 Other Statutory Information 105 Shareholder and Bondholder Information 107 Directory This Annual Report is signed for and on behalf of the Board of the Company by: For personal use only K.R. Ellis A.B. Ryan CHAIR DIRECTOR Antoinette Rodahl and family 9 September 2020 9 September 2020 in fits of laughter, The Poynton METLIFECARE LIMITED ANNUAL REPORT 2020 Creating extraordinary 1 BAY OF ISLANDS living experiences AUCKLAND 15 4 At a glance HAMILTON 1 5 BAY OF PLENTY 006 At Metlifecare, we’re in the business of providing retirement communities in which people 007 are empowered to be the very best version of themselves. -

Annual Report 2014 Crestwood

METLIFECARE LIMITED Annual Report 2014 Crestwood This Annual Report is signed for and on behalf of the Board of the Company by: K.R. Ellis A.B. Ryan Chair Director 15 September 2014 15 September 2014 C over image: Ros from Pinesong was one of the first vets in New Zealand. One of her passions as a girl and young woman was sailing on the family launch with her father (a violinist) and mother. Ros still loves the ocean and her home is filled with landscapes of the sea and NZ beaches. The heart Ros is holding features a rope from a sailing boat with a sailing slip knot. 2 | METLIFECARE LIMITED ANNUAL REPORT 2014 1 & OVE HIG H LIG R VIEW H T S C ontents 2 S FIN T A A TEMENT N C I A Section 1 - Highlights & Overview L Our Business 6 S Our Five Year Transition 8 FY14 At a Glance 10 Chair’s Report 12 3 INFO S 15 T Chief Executive Officer’s Report A TUT ector Profiles 18 R Dir M O A R 20 TION Executive Team Profiles Y Y Overview of Financials 22 Family of Villages 24 Construction & Development Locations 25 Section 2 - Financial Statements Directors’ Report 28 Statements of Comprehensive Income 29 Statements of Movements in Equity 30 Balance Sheets 31 Cash Flow Statements 32 Notes to the Financial Statements 33 Independent Auditor’s Report 69 Section 3 - Statutory Information Corporate Governance Statement 74 Interests Register 83 Other Director Information 86 Other Statutory Information 88 Shareholder Information 90 Directory 92 ANNUAL REPORT 2014 METLIFECARE LIMITED | 3 Dannemora Gardens 4 | METLIFECARE LIMITED ANNUAL REPORT 2014 1 & OVE HIG -

Metlifecare 2020 Annual Report

ANNUAL REPORT 2020 A YEAR LIKE NO OTHER A Year Like No Other “From the outset, we 002 put the safety and 003 wellbeing of residents and staff at the centre of all decision-making. Our shared philosophy was simple - protecting our team of 7,000.” CEO GLEN SOWRY ON METLIFECARE’S COVID-19 RESPONSE Pinesong resident Heather (right) has Front Cover: Resident village DJ Eddy Cross, Forest Lake Gardens a laugh with a friend on Grandparents Day METLIFECARE LIMITED ANNUAL REPORT 2020 Contents COMPANY OVERVIEW 06 At a Glance 08 Chair and CEO Report 16 Performance Overview 17 How We Create Value 18 Thriving Through Disruption 24 Becoming Future Fit 30 A Place to be You • Saluting Our People • Increasing Sustainability 44 Our Board of Directors 46 Our Executive Team 49 Corporate Governance Statement 53 5-Year Performance Summary 55 Underlying Profit Reconciliation 004 GROUP FINANCIAL STATEMENTS 005 58 Consolidated Statement of Comprehensive Income 59 Consolidated Statement of Movements in Equity 60 Consolidated Balance Sheet 61 Consolidated Cash Flow Statement 63 Notes to the Group Financial Statements 91 Independent Auditor’s Report STATUTORY INFORMATION 100 Interests Register 102 Director Information 103 Other Statutory Information 105 Shareholder and Bondholder Information 107 Directory This Annual Report is signed for and on behalf of the Board of the Company by: K.R. Ellis A.B. Ryan CHAIR DIRECTOR Antoinette Rodahl and family 9 September 2020 9 September 2020 in fits of laughter, The Poynton METLIFECARE LIMITED ANNUAL REPORT 2020 Creating extraordinary 1 BAY OF ISLANDS living experiences AUCKLAND 15 4 At a glance HAMILTON 1 5 BAY OF PLENTY 006 At Metlifecare, we’re in the business of providing retirement communities in which people 007 are empowered to be the very best version of themselves. -

Flexshares 2018 Semiannual Report

FlexShares® Trust Semiannual Report April 30, 2018 FlexShares® Morningstar US Market Factor Tilt Index Fund FlexShares® Morningstar Developed Markets ex-US Factor Tilt Index Fund FlexShares® Morningstar Emerging Markets Factor Tilt Index Fund FlexShares® Currency Hedged Morningstar DM ex-US Factor Tilt Index Fund FlexShares® Currency Hedged Morningstar EM Factor Tilt Index Fund FlexShares® US Quality Large Cap Index Fund FlexShares® STOXX® US ESG Impact Index Fund FlexShares® STOXX® Global ESG Impact Index Fund FlexShares® Morningstar Global Upstream Natural Resources Index Fund FlexShares® STOXX® Global Broad Infrastructure Index Fund FlexShares® Global Quality Real Estate Index Fund FlexShares® Real Assets Allocation Index Fund FlexShares® Quality Dividend Index Fund FlexShares® Quality Dividend Defensive Index Fund FlexShares® Quality Dividend Dynamic Index Fund FlexShares® International Quality Dividend Index Fund FlexShares® International Quality Dividend Defensive Index Fund FlexShares® International Quality Dividend Dynamic Index Fund FlexShares® iBoxx 3-Year Target Duration TIPS Index Fund FlexShares® iBoxx 5-Year Target Duration TIPS Index Fund FlexShares® Disciplined Duration MBS Index Fund FlexShares® Credit-Scored US Corporate Bond Index Fund FlexShares® Credit-Scored US Long Corporate Bond Index Fund FlexShares® Ready Access Variable Income Fund FlexShares® Core Select Bond Fund Table of Contents Statements of Assets and Liabilities ................................................ 2 Statements of Operations................................................................ -

At a Glance December 2008 Quarter

December 2008 Quarter Dear Shareholders Kingfish was established in 2004 The last quarter of 2008 ended, for to invest, through its manager, in a most, with a big sigh of relief. portfolio of well researched small cap at a glance New Zealand companies. It provides The Kingfish portfolio suffered some of its Performance for period 31/03/04 a single vehicle through which to heaviest falls in its history. The Net Asset to 31/12/2008 (since listing) invest in these stocks, primarily on Value dropped 18% from $1.19 to $0.98, Net Asset Value $0.98 1.3%* a long term buy and hold basis. The while the share price declined from $0.96 Dividends Paid $0.15 15.0% tax structure is efficient, especially to $0.84 – a period end discount of 14% Share Price $0.84 -16.0% now that Kingfish has “PIE” status. to the underlying NAV. Share volumes *Based on adjusted Net Asset Value Despite the difficult current market per Share at listing of $0.9684, traded during the quarter were relatively representing the issue price of $1.00 conditions, directors consider that light – 2.3% of the total shares outstanding. less issue costs of $0.0316 per share. the company’s investment rationale This perhaps reflects that shareholders and focus remain as relevant today as continue to recognise the underlying Performance for the three months when the company was established. 30/9/2008 to 31/12/2008 value of the portfolio companies and are “holding on” during the rough patch. The company’s bias is towards Net Asset Value -17.7% capital growth but during the past Share Price -12.5% This newsletter contains, among other five years a total of 15 cents per matters: share has been paid in dividends. -

28 April 2020 Metlifecare Rejects Notice to Terminate

MEDIA RELEASE 28 APRIL 2020 METLIFECARE REJECTS NOTICE TO TERMINATE SCHEME IMPLEMENTATION AGREEMENT Metlifecare Limited (NZX: MET, ASX: MEQ) has today received a notice to terminate the Scheme Implementation Agreement (SIA) entered with Asia Pacific Village Group Limited (APVG), an entity owned by EQT Infrastructure IV fund and managed by EQT Fund Management S.à.r.l. The Metlifecare Board has rejected the notice to terminate from APVG as entirely invalid and reiterates its belief, based on legal advice, that there is no lawful basis for APVG to terminate the SIA. Under New Zealand law, an invalid termination is treated as a ‘repudiation’ of the contract enabling the non-defaulting party to elect to either (i) cancel the contract and seek damages or (ii) continue with the contract and require the defaulting partly to perform its obligations. Metlifecare remains strongly committed to the successful completion of the scheme in the interests of all shareholders and remains on track to dispatch the scheme materials ahead of a shareholder meeting to vote on the scheme, intended to be held at 11am on 9 June as a ‘virtual’ meeting, subject to receipt of orders from the High Court. Metlifecare Chair Kim Ellis said: “The fundamental assumptions that APVG uses to justify its Notice to Terminate are simply wrong. There has been no breach of the ‘Material Adverse Change’ (MAC) metrics and/or any ‘Prescribed Occurrence’, as claimed by APVG, and such breaches, if they were to occur, would be covered in either case by specific exceptions under the SIA. Metlifecare considers APVG and its parent company EQT have misstated the terms of the SIA and are wrongly attempting to withdraw from an agreement they willingly entered less than four months ago. -

STOXX Pacific 100 Last Updated: 01.08.2017

STOXX Pacific 100 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) AU000000CBA7 6215035 CBA.AX 621503 Commonwealth Bank of Australia AU AUD Y 98.1 1 1 AU000000WBC1 6076146 WBC.AX 607614 Westpac Banking Corp. AU AUD Y 72.3 2 2 AU000000ANZ3 6065586 ANZ.AX 606558 Australia & New Zealand Bankin AU AUD Y 58.9 3 3 AU000000BHP4 6144690 BHP.AX 614469 BHP Billiton Ltd. AU AUD Y 56.2 4 5 AU000000NAB4 6624608 NAB.AX 662460 National Australia Bank Ltd. AU AUD Y 54.3 5 4 AU000000CSL8 6185495 CSL.AX 618549 CSL Ltd. AU AUD Y 38.8 6 6 AU000000TLS2 6087289 TLS.AX 608545 Telstra Corp. Ltd. AU AUD Y 33.0 7 7 AU000000WES1 6948836 WES.AX 694883 Wesfarmers Ltd. AU AUD Y 31.3 8 8 AU000000WOW2 6981239 WOW.AX 698123 Woolworths Ltd. AU AUD Y 23.4 9 9 AU000000RIO1 6220103 RIO.AX 622010 Rio Tinto Ltd. AU AUD Y 18.9 10 11 AU000000MQG1 B28YTC2 MQG.AX 655135 Macquarie Group Ltd. AU AUD Y 18.6 11 10 AU000000TCL6 6200882 TCL.AX 689933 Transurban Group AU AUD Y 15.9 12 12 AU000000SCG8 BLZH0Z7 SCG.AX AU01Z4 SCENTRE GROUP AU AUD Y 14.9 13 14 AU000000WPL2 6979728 WPL.AX 697972 Woodside Petroleum Ltd. AU AUD Y 14.4 14 13 AU000000SUN6 6585084 SUN.AX 658508 SUNCORP GROUP LTD. AU AUD Y 12.5 15 15 AU000000AMC4 6066608 AMC.AX 606660 Amcor Ltd. AU AUD Y 12.0 16 16 AU000000QBE9 6715740 QBE.AX 671574 QBE Insurance Group Ltd. -

Feltex • the Liquidators Have Now Put the Directors on Notice of Possible Actions Against Them

August 2007 HOW TO REALLY ANNOY SHAREHOLDERS As many of you will already know, we recently wrote to the shareholders in Tourism Holding Limited (THL). We were concerned that the purchaser of the company, should the takeover be successful, were in effect paying the THL management for procuring the success of the bid. We were also concerned that the company was using shareholders’ funds to pay a break fee to the purchaser of the company’s shares, should the deal not proceed (in limited circumstances admittedly). Our mail out clearly struck a note with THL shareholders, as we have had numerous letters of support of our actions and condemnation of the board’s actions on the issues we raised in our letter to shareholders. The THL Board then took exception to our correspondence and wrote to all shareholders of THL and among other things told shareholders that they felt our comments were defamatory of the Board and management. Shortly after the THL letter to their shareholders, our mail box filled with membership applications and cheques, and we thank all those THL shareholders who have joined NZSA and hope that they will value their membership of the NZSA as much or more than they value their continuing shareholding in THL. The bid for THL failed. But unlike THL, we will aspire to deliver value for your confidence in this Association and we welcome each of you aboard. For you to get full value out of the NZSA you should, if you are available, attend your local branch meetings, which have solid attendances. -

International Smallcap Separate Account As of July 31, 2017

International SmallCap Separate Account As of July 31, 2017 SCHEDULE OF INVESTMENTS MARKET % OF SECURITY SHARES VALUE ASSETS AUSTRALIA INVESTA OFFICE FUND 2,473,742 $ 8,969,266 0.47% DOWNER EDI LTD 1,537,965 $ 7,812,219 0.41% ALUMINA LTD 4,980,762 $ 7,549,549 0.39% BLUESCOPE STEEL LTD 677,708 $ 7,124,620 0.37% SEVEN GROUP HOLDINGS LTD 681,258 $ 6,506,423 0.34% NORTHERN STAR RESOURCES LTD 995,867 $ 3,520,779 0.18% DOWNER EDI LTD 119,088 $ 604,917 0.03% TABCORP HOLDINGS LTD 162,980 $ 543,462 0.03% CENTAMIN EGYPT LTD 240,680 $ 527,481 0.03% ORORA LTD 234,345 $ 516,380 0.03% ANSELL LTD 28,800 $ 504,978 0.03% ILUKA RESOURCES LTD 67,000 $ 482,693 0.03% NIB HOLDINGS LTD 99,941 $ 458,176 0.02% JB HI-FI LTD 21,914 $ 454,940 0.02% SPARK INFRASTRUCTURE GROUP 214,049 $ 427,642 0.02% SIMS METAL MANAGEMENT LTD 33,123 $ 410,590 0.02% DULUXGROUP LTD 77,229 $ 406,376 0.02% PRIMARY HEALTH CARE LTD 148,843 $ 402,474 0.02% METCASH LTD 191,136 $ 399,917 0.02% IOOF HOLDINGS LTD 48,732 $ 390,666 0.02% OZ MINERALS LTD 57,242 $ 381,763 0.02% WORLEYPARSON LTD 39,819 $ 375,028 0.02% LINK ADMINISTRATION HOLDINGS 60,870 $ 374,480 0.02% CARSALES.COM AU LTD 37,481 $ 369,611 0.02% ADELAIDE BRIGHTON LTD 80,460 $ 361,322 0.02% IRESS LIMITED 33,454 $ 344,683 0.02% QUBE HOLDINGS LTD 152,619 $ 323,777 0.02% GRAINCORP LTD 45,577 $ 317,565 0.02% Not FDIC or NCUA Insured PQ 1041 May Lose Value, Not a Deposit, No Bank or Credit Union Guarantee 07-17 Not Insured by any Federal Government Agency Informational data only.