OCL India Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Defaulter-Private-Itis.Pdf

PRIVATE DEFAULTER ITI LIST FOR FORM FILL-UP OF AITT NOVEMBER 2020 Sl. No. District ITI_Code ITI_Name 1 ANGUL PR21000166 PR21000166-Shivashakti ITC, AT Bikash Nagar Tarang, Anugul, Odisha, -759122 2 ANGUL PR21000192 PR21000192-Diamond ITC, At/PO Rantalei, Anugul, Odisha, -759122 3 ANGUL PR21000209 PR21000209-Biswanath ITC, At-PO Budhapanka Via-Banarpal, Anugul, Odisha, - 759128 4 ANGUL PR21000213 PR21000213-Ashirwad ITC, AT/PO Mahidharpur, Anugul, Odisha, -759122 5 ANGUL PR21000218 PR21000218-Gayatri ITC, AT-Laxmi Bajar P.O Vikrampur F.C.I, Anugul, Odisha, - 759100 6 ANGUL PR21000223 PR21000223-Narayana Institute of Industrial Technology ITC, AT/PO Kishor, Anugul, Odisha, -759126 7 ANGUL PR21000231 PR21000231-Orissa ITC, AT/PO Panchamahala, Anugul, Odisha, -759122 8 ANGUL PR21000235 PR21000235-Guru ITC, At.Similipada, P.O Angul, Anugul, Odisha, -759122 9 ANGUL PR21000358 PR21000358-Malayagiri Industrial Training Centre, Batisuand Nuasahi Pallahara, Anugul, Odisha, -759119 10 ANGUL PR21000400 PR21000400-Swami Nigamananda Industrial Training Centre, At- Kendupalli, Po- Nukhapada, Ps- Narasinghpur, Cuttack, Odisha, -754032 11 ANGUL PR21000422 PR21000422-Matrushakti Industrial Training Institute, At/po-Samal Barrage Town ship, Anugul, Odisha, -759037 12 ANGUL PR21000501 PR21000501-Sivananda (Private) Industrial Training Institute, At/Po-Ananda Bazar,Talcher Thermal, Anugul, Odisha, - 13 ANGUL PU21000453 PU21000453-O P Jindal Institute of Technology & Skills, Angul, Opposite of Circuit House, Po/Ps/Dist-Angul, Anugul, Odisha, -759122 14 BALASORE -

Odisha State Profile 2017-18

ODISHA STATE PROFILE 2017-18 (MICRO AND SMALL SCALE ENTERPRISES RELATED INFORMATION) Prepared By Dr. Pragyansmita Sahoo Deputy Director (E.I) MICRO, SMALL & MEDIUM ENTERPRISES – DEVELOPMENT INSTITUTE GOVERNMENT OF INDIA, MINISTRY OF MSME VIKASH SADAN, COLLEGE SQUARE, CUTTACK-753003 ODISHA F O R E W O R D Micro, Small & Medium Enterprises (MSMEs) in the economic and social development of the country is well established. This sector is a nursery of entrepreneurship, often driven by individual creativity and innovation. This sector contributes 8 per cent of the country’s GDP, 45 per cent of the manufactured output and 43 percent of its exports. The MSMEs provide employment to about 60 million persons through 26 million enterprises. The labour capital ratio in MSMEs and the overall growth in the MSME sector is much higher than in the large industries. In the present world scenario, there is an urgency to give a boost to industrial activity for a faster growth of economy for which, there is a need for getting relevant information to instill the confidence among entrepreneurs to plan for an appropriate investment strategy either to set up new industry or to enlarge the existing activity in the State. MSMEDI, Cuttack has brought out the new edition of Odisha State Profile (MSME related information) in the year 2017-18 as per the guide lines issued by the office of the Development Commissioner (MSME), Ministry of MSME, Government of India, New Delhi by incorporating all the relevant information including opportunities to set up and develop industries in the state, latest information on infrastructure development, present status of industries, availability of natural resources and other raw materials, human resources, support and assistance available from technical and financial institutions, new initiative undertaken by MSMEDO, etc to provide adequate exposure both prospective and existing entrepreneurs in the state. -

Western Electricity Supply Company of Odisha Ltd., Corporate Office, Burla, Sambalpur-768017 (Orissa)

Western Electricity Supply Company of Odisha Ltd., Corporate Office, Burla, Sambalpur-768017 (Orissa) PUBLIC NOTICE Publication of Applications u/S. 64(2) of the Electricity Act, 2003, read with Reg. 53(7) of the OERC (Conduct of Business) Regulations, 2004 for Approval of Aggregate Revenue Requirement and Determination of Retail Supply Tariff for the FY 2015-16 filed by Western Electricity Supply Company of Orissa Ltd. (WESCO) before the Odisha Electricity Regulatory Commission, Bhubaneswar 1. Western Electricity Supply Company of Orissa Ltd (in short WESCO), holder of the Odisha Distribution and Retail Supply Licensee, 1999 (4/99), a deemed Distribution Licensee under Sec. 14 of the Electricity Act, 2003 has submitted its Application to the Odisha Electricity Regulatory Commission on 29.11.2014 for approval of its Aggregate Revenue Requirement and determination of Retail Supply Tariff for the financial year 2015-16, which has been registered as Case No.70/2014. The application has been filed under Section 62 and other applicable provisions of the Electricity Act, 2003 read with OERC (Terms and Conditions for Determination of Tariff) Regulations, 2004 and OERC (Conduct of Business) Regulations, 2004. The Commission have decided to dispose of the case through a public hearing. 2. Copies of the aforesaid filing together with supporting materials are available with the Managing Director, WESCO, Burla and all Executive Engineers in charge of Distribution Divisions, viz (i) Rourkela Electrical Division, Udit Nagar, Rourkela (ii) Rourkela -

NEW RAILWAYS NEW ODISHA a Progressive Journey Since 2014 Sundargarh Parliamentary Constituency

TIVE Y INDICA MAP IS ONL Shri Narendra Modi Hon'ble Prime Minister NEW RAILWAYS NEW ODISHA A progressive journey since 2014 Sundargarh Parliamentary Constituency SUNDARGARH RAILWAYS’ DEVELOPMENT IN ODISHA (2014-PRESENT) SUNDARGARH PARLIAMENTARY CONSTITUENCY A. ASSEMBLY SEGMENTS : Talsara, Sundargarh, Biramitrapur, Raghunathpali, Rourkela, Rajgangpur, Bonai RAILWAY STATIONS COVERED : Rourkela, Rajgangpur, Bamra, Bondamunda, Garposh, Kanshbahal, Panposh, Kalunga, Tangarmunda, Sonakhan, Sagra, Daghora, Bisra, Nuagaon, Jamga, Himgir, Chandiposi, Kuarmunda, Bimlagarh Junction, Birmitrapur, Barsuan, Dumerta, Lathikata, Dharuadihi, Dhutra, Karampada, Barajamda, Gua, Goilkera, Posoita, Manoharpur, Jaraikela, Bhalulata, Orga B. WORKS COMPLETED IN LAST FIVE YEARS : B.1. New Trains and Stoppages / Extension / Increase in Frequency : Train No. 58660-58659, Rourkela- Hatia-Rourkela passenger started from 09.02.2015. Train No. 78103-78104 Rourkela- Sambalpur-Rourkela DMU started from 07.06.2015. Train No. 12101-12102, Jnaneswari Deluxe Howrah-Lokmanya Tilak Terminus-Howrah provided stoppage at Jharsuguda from 09.05.2017. Train No. 18110-18109, Jammu Tawi MURI Rourkela Express extended from Jammu Tawi to Rourkela and further extended upto Sambalpur w.e.f.12.08.2017. Train No. 18417-18418, Rajya Rani Exp from Rourkela to Bhubaneswar extended upto Gunupur from 21.03.2017. Train No. 18415/18416 Puri-Barbil-Puri Express has been extended upto Rourkela. Train No. 18451/18452 Tapaswini Express has been provided additional stoppage at Kalunga. Train No. 18107/18108 Rourkela-Jagdalpur-Rourkela Express has been provided additional stoppage at Rajgangpur. Train No. 18108/18107 Rourkela - Koraput - Rourkela Express extended upto Jagdalpur. Frequency of 18117/18118 Rourkela-Gunupur-Rourkela Rajyarani Express has been increased to run Daily. B.2. Improvement of Passenger Amenities : Escalators at important stations - 2 Nos at Rourkela at a cost of `1.060 Crore. -

(O&M) Division, Rajgangpur Dist

ODISHA POWER TRANSMISSION CORPORATION LTD. II OFFICE OF THE DEPUTY GENERAL MANAGER Co)Uii3! Ufa/.Tlft of OriSsa E.H.T. (O&M) DIVISION, RAJGANGPUR DIST.-SUNDARGARH P.O.--769004, (ORISSA), PHONE 1FAX- 9438907627 TENDER CALL NOTICE-(O 21 19-20) Sealed Tenders are invited by the undersigned from the Manufacturers 1Authorized Dealers and registered suppliers having valid PAN, authorised dealership Certificate, OST Registration certificate, to supply the following materials. SL. DESCRIPTION QTY MAKE . COST OF DATE OF NO TENDER ESTIMATED DELIVERY PAPER (NON COST REFUNDABL E) 1 01 Channel 125 MTR, 100 x 50 x 6 mm 1195KG TATA/RIN LISAILiJI NDALIRE OI Pipes 40mm 30 days from the 2 60MTR LlBLE/BH dia,3.5 mm thickness Rs. 2000/- + issue of purchase Rs 1,53,872/- USHAN 18%GST order. MAKE 01 Pipes 50 mm 3 24MTR dia,3.5 mm thickness The tender document can be made avatlable In the office of the undersigned on wntten request and payment of requisite amount towards cost of tender document by cash/ Bank draft drawn in favour of E.RT. (O&M) Division, OPTCL, Rajgangpur, payable at Kalunga. Additional amount ofRs. 100/- (Rupees one hundred) only may be paid for postal delivery of Tender document. The undersigned shall not be held responsible for any postal delay. The bid must be accompanied with an amount equal to 1% (one percent) of the estimated cost i.e Rs 1,539/- EMD in shape of DO/Cash drawn in favour of E.RT. (O&M) ) Division, OPTCL, Rajgangpur, payable at Kalunga, and will be opened in presence of Tenderers or their authorised representatives possessing original authorisation letter. -

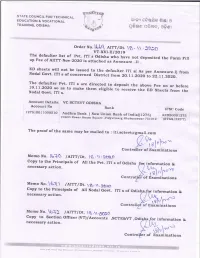

OCL INDIA LIMITED CIN No.: L26942OR1949PLC000185 Regd

OCL INDIA LIMITED CIN No.: L26942OR1949PLC000185 Regd. Office: Rajgangpur- 770 017, District Sundargarh, Odisha Tel. No. :(06624)221212, 220121 Website: www.oclindialtd.in, E-mail: [email protected] COURT CONVENED MEETING OF THE SECURED CREDITORS COURT CONVENED MEETING OF SECURED CREDITORS Day Sunday Date November 27, 2016 Time 2.00 p.m. Venue OCL India Limited’s premises at Rajgangpur- 770 017, District Sundargarh, Odisha INDEX SL No Content Page Number 1 Notice of Court Convened Meeting of the Secured Creditors of OCL 1 - 2 India Limited as per the direction of Hon’ble High Court of Orissa, at Cuttack vide its order dated October 06, 2016 in Company Petition No. 37 of 2016. 2 Explanatory Statement under Section 393 and other applicable 3 - 22 provisions of the Companies Act, 1956 3 Scheme of Arrangement and Amalgamation amongst OCL India Provided Limited, Dalmia Cement East Limited, Shri Rangam Securities & separately Holdings Limited, Dalmia Bharat Cements Holdings Limited and Odisha Cement Limited and their respective shareholders and creditors 4 Fairness Opinion dated March 28, 2016 issued by Axis Capital 23 – 28 Limited 5 Copy of Observation Letters issued by BSE Limited and National 29 – 33 Stock Exchange of India Limited, both dated July 12, 2016 6 Complaints Report dated May 26, 2016 submitted by OCL India 34 Limited with BSE Limited and National Stock Exchange of India Limited 7 Form of Proxy 35 – 36 8 Attendance Slip 37 In the Hon’ble High Court of Orissa, Cuttack Original Jurisdiction Company Petition No. 37 of 2016 In the matter of Companies Act, 1956 AND In the matter of Sections 391 to 394 of the Companies Act, 1956 AND In the matter of Scheme of Arrangement and Amalgamation amongst OCL India Limited, Dalmia Cement East Limited, Shri Rangam Securities & Holdings Limited, Dalmia Bharat Cements Holdings Limited and Odisha Cement Limited and their respective shareholders and creditors OCL India Limited ) a company incorporated under the provisions of the ) Companies Act, 1913, having its registered office at ) Rajgangpur-770017, Dist. -

![(AI) Details [District Wise]](https://docslib.b-cdn.net/cover/3941/ai-details-district-wise-1193941.webp)

(AI) Details [District Wise]

National Institute of Open Schooling Regional Centre, Bhubaneswar Study Centre (AI) Details [District Wise] Sl No. AI/ Study Centre Code Name & Address of Study Centre (AI) District 1 150147/410104 Govt. High School,Phulamba, Po-Kalyanpur,Via-Rajkishore Nagar Dist-Angul, Angul Orissa, PIN-759126 Mob:9438511716. 2 150146/410103 Govt. Girls High School, At/Po-Jamardini, Via-Pallahara, Dist-Angul, Orissa, Angul Mb-9338842157,9583491446 3 150037 Jawahar Navodaya Vidyalaya, At-F.C.I, Po-Vikrampur, Via-Talcher, Dist-Angul, Angul Orissa-759106, Ph: 06760-262626, Mb: 9437665821. 4 150028 Kendriya Vidyalaya, NTPC, Koniha, P.O. - Deepshikha, Distt.-Angul. Orrisa - Angul 759147. Ph.No. 06760-243658, Fax : 243658,MOB:9937616275 5 150140/410097 Govt.(SSD) Higher Sec. School, At/Po-Malpada, Via-H.S.Road, Dist-Balangir, Balangir Orissa, Mob:9437917452. 6 150059/410021 Govt. High School(SSD), At-Rampur, Block-Agalpur, Tehsil-Loisingha, Dist- Balangir Balangir, Orissa-767021, Mob:9937485942,9439225778,9438283911 7 150058/410020 Govt. High School(SSD), At-Desil, Block/Tehsil-Titlagarh, Dist-Balangir, Orissa- Balangir 767033, Mob:9658253599,9437429416 8 150139/410096 Govt.(SSD) Girls High School, At/Po-Saintala, Dist-Balangir, Orissa, Mob: Balangir 9437429188. 9 150026 Shree Dadiji Mandir Trust, Prabhavati Public School, At Pipalpadar, Dist. Balangir Balangir, Orissa - 767033 Phone No 06655 220272 10 150032 Oriental Public School, At/PO Malamunda, Distt. Bolangir - 767002, Ph. No. Balangir 06652-230025, 09437223303 11 150096/410052 Govt.(SSD) Girls Higj School, At/Po-Tenda, Via-Sajangarh, Dist-Balasore, Balasore Orissa, Mob::9668222895, 9937302394. 12 150097/410053 Govt. High School, At/Po-Kabatghati, Via-Hatigarh, Dist-Balasore-756033, Balasore Orissa. -

Sl. No. TIN Name of the Dealer Address 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 LIST of DEALERS SELECTE

LIST OF DEALERS SELECTED FROM SUNDERGARH RANGE FOR TAX AUDIT DURING 2011-12 Sl. TIN Name of the dealer Address No. 1 21302000022 L & T LTD. KANSBAHAL, SUNDARGARH 2 21072000003 EAST INDIA STEEL PVT.LTD. INDUSTRIAL AREA,ROURKELA 3 SHREE GANESH METALICK 21022000079 LTD. HARIHAR PUR,KUARMUNDA 4 21352000043 PRABHU SPONGE IRON(P)LTD OCL APPROACH ROAD,ROURKELA 5 KOSHALA PLOT NO- 10/310,, PANPOSH 21812003961 AUTOMOBILES(P)LTD. ROAD,ROURKELA 6 21842000016 GRUHASTI UDYOG CHHEND BASTI, ROURKELA 7 PLOT NO-98,GOIBHANGA, INDUSTRIAL 21382000075 Time Steel & Power Ltd. ESTATE,, SUNDARGARH 8 BAJRANGA STEEL & ALLOYES 21082000046 PVT.LTD. PLOT NO-31, GOBHANGA, SUNDARGARH 9 UTKAL FLOUR MILLS(RKL) 21742000071 PVT.LTD. INDUSTRIAL AREA,, SUNDARGARH 10 21452003092 T.R.CHEMICALS LTD. BARPALLI,RAJGANGPUR 11 BARPALI KESARMAL(RAJGANGPUR) 21632000083 SURAJ PRODUCTS LTD. ROURKELA SUNDARGRAH 12 P-25,CTS, P-25,CTS, SUNDARGARH, 21312000065 M/S.SHIVA CEMENT LTD ROURKELA 13 RAJGANGPUR, RAJGANGPUR, 21062001318 HARI MACHINES L.T.D RAJGANGPUR, SUNDARGARH, 770017 14 IDCO PLOT NO- 76, INDUSTRIAL ESTATE, 21182000088 UTKAL METALLICS LTD KALUNGA, SUNDARGARH, 15 RAMABAHAL, RAJGANGPUR, 21192000034 M/S SCAN STEELS LTD. RAJGANGPUR, SUNDARGARH, 770017 16 BIJABAHAL KUARMUNDA KUARMUNDA 21202000077 PAWANJOY SPONGE IRON LTD SUNDARGARH 17 M/S SARVESH REFRACTORIES KUARMUNDA, KUARMUNDA, 21372000032 LTD KUARMUNDA, SUNDARGARH 770039 18 BALLANDA BALLANDA BALANDA,RKL 21422000053 M/S.MAA TARINI (P) LTD SUNDARGARH 19 SHREE RAM SPONGE BILAIGARH, BILAIGARH, BILAIGARH, 21442003243 &STEEL(P) LTD SUNDARGARH, 770034 20 BARPALI, BARPALLI, RAJGANGPUR, 21452003092 T.R. CHEMICALS LIMITED SUNDARGARH, 770017 21 RAJGANGPUR RAJGANGPUR 21482002542 M/S SHREE CHEM RESIN LTD . RAJGANGPUR SUNDARGARH 22 GOIBHARGA,KALUNGA 21592000008 KALINGA SPONGEIRONLTD GOIBHARGA,KALUNGA ROURKELA 23 INDERA MOTORS (PROP. -

Sundargarh District at a Glance

Govt. of India MINISTRY OF WATER RESOURCES CENTRAL GROUND WATER BOARD OF SUNDERGARH DISTRICT CENTRAL GROUND WATER BOARD SOUTH EASTERN REGION BHUBANESWAR March, 2013. 1 SUNDARGARH DISTRICT AT A GLANCE I. General Particulars (a) Location : 21o 35' and 22o 32' North latitudes 83o 32' and 85o 22' East longitudes (b) Area : 9,712 Km2 (c) District Head quarters : Sundargarh (d) Subdivision : 3(three) – 1. Sundargarh 2.Panposh 3.Bonaigarh (e)Tehsils 9(nine) (f) Blocks : 17(seventeen) 9.kutra 1.Balisankara 10.Lahunipada 2.Baragaon 11.Lathikata 3.Bisra 12.lephripada 4.Bonaigarh 13.Nuagaon 5.Gurundia 14.Rajgangapur 6.Hemagiri 15. Subdega 7.Koida 16. Sundargarh 8. Kuarmunda 17. Tangarpalli (g) Population : 20,80,664 (as per 2011 census) II Climatology : (a) Normal annual rainfall : 1647.6 mm (b) Maximum temperature : 48 o C (c) Minimum temperature : 6o C III Land use : (a) Total forest area : 146061 Ha (b) Net area sown : 257927Ha IV Irrigation potential created (source Kharif Rabi wise) (upto 2000-01) (a) Minor irrigation Projects : 15425 Ha 1358 Ha (flow) 2 (b) Lift Irrigation Projects : 6925 Ha 2884 Ha (c) Ground water Structures : 10277 Ha V Exploratory wells : Bore wells drilled by CGWB : 101 EW &26 OW under Normal Exploration Programme (As 0n 31.03.2011) VI Ground Water Resources a) Annual ground water : 1668914 ham resource assessed b) Annual ground water draft (for : 436202 ham all uses) c) Balance ground water : 1201460 ham resource for irrigation use VII Stage of ground water : 26.14% development 3 1.0. INTRODUCTION Sundargarh district with an area of 9712 sq km and population of 1830673 (as per 2001 census) is the northern most district of Orissa. -

The High Court of Orissa,Cuttack List of Business for Tuesday the 28Th January 2020 Chief Justice's Court (Old Building)

SUPPLEMENTARY LIST THE HIGH COURT OF ORISSA,CUTTACK LIST OF BUSINESS FOR TUESDAY THE 28TH JANUARY 2020 CHIEF JUSTICE'S COURT (OLD BUILDING) AT 10:30 AM THE HON'BLE THE ACTING CHIEF JUSTICE AND THE HON'BLE MR. JUSTICE S.K.SAHOO (CRIMINAL APPLICATIONS & MOTIONS.) FRESH ADMISSION - TRANSFER OF O.A. 1. WP(C)/26484/2019 KISHORE CHANDRA PANDA M/S. MANAS RANJAN DAS (With defect.) V/S J.RATH, R.SINGH STATE OF ORISSA 2. WP(C)/793/2020 MOHAN TANTI M/S.SUMANTA KUMAR NAYAK (With defect.) V/S A.B.PARIDA, S.DASH, S.K.SAHU STATE OF ODISHA 3. WP(C)/1031/2020 TRILOCHAN SAHU M/S. B.S.MISHRA (With defect.) V/S A.R.MISHRA STATE OF ODISHA 4. WP(C)/1056/2020 SANTOSH KUMAR SAHU M/S.K.N.DAS (With defect.) V/S S.PATTNAIK DG AND IG OF POLICE, CTC 5. WP(C)/1057/2020 UMESH CHANDRA DAS M/S.K.N.DAS (With defect.) V/S S.PATTNAIK STATE OF ORISSA 6. WP(C)/1060/2020 AROOP KUMAR MOHANTY M/S.K.N.DAS (With defect.) V/S S.PATTNAIK STATE OF ORISSA 7. WP(C)/1249/2020 MANOJ KUMAR SAHOO M/S.PITAMBAR JENA V/S STATE OF ODISHA 8. WP(C)/1482/2020 DEBASISA PATTNAYAK SIDHESWAR MALLIK (With defect.) V/S P.C.DAS, M.MALLIK, S.MALLICK, A.P.MOHANTY STATE OF ODISHA 9. WP(C)/1483/2020 SRIDHAR SAHOO M/S.DR.J.K.LENKA (With defect.) V/S P.K.BEHERA, P.DAS STATE OF ODISHA 10. -

Sambalpur-Ll 1 NR Buildi

Name of the SI. Name of the Works Amount Remarks t& B ) Division No. Required (1) (2) (3) И) (5) Sambalpur-ll 1 N.R. Building such as concreting to ramp of UG 4.50 Boys hostel and painting works to Boys hostel No,5 of VIMSAR Burla 2 N.R. Building such as providing leak proofing 4.20 treatment to old central store of VIMSAR Burela 3 N.R. Building such as repair and renovation to 4.00 Old CT scan of VIMSAR Burla 4 N.R. Building such as U,G, Ladies hostel of 1.90 VIMSAR Burla 5 N.R. Building such as repair and renovaiton to 3.50 ТВ ward of VIMSAR Burla 6 N.R. Building such as repair to approach road 4.00 of Ladies hostel No.3 of VSS IMSAR Burla. 7 Administrative office Building such as leak 5.00 proof treatment of ITI at Hirakud 8 S/R such as Painting works outside of Boys 5.00 Hostel at Hirakud ( 1st Floor) 9 Sub-Collector office such as renovation of sub 4.50 register section. 10 N/R building such as repair & renovation to 5.00 the cancer ward of VIMSAR. 11 N/R building such as leak proof treatment to 5.00 Nursing SchooL,Burla . 12 N.R. Building such as providing plastic emulsion 2.80 paint and weather coat to Ladies Hostel No.1 of VIMSAR, Burla 13 N/R building such as Repair & Renovation to 4.90 PWD Subdivision office,Burla . 14 N/R building such as providing & fixing 4.60 designer tiles in front of PWD Subdivision off ice, Burla . -

Sl. ANGUL MIS Code MIS Code Trade 1 ANGUL Govt. ITI, Talcher GU21000531 Talcher Tech

DRAFT LIST OF TRADE TESTING CENTRES (TTCs) WITH TAGGED ITIS FOR AITT JULY/AUGUST 2018 Sl. ANGUL MIS Code MIS Code Trade 1 ANGUL Govt. ITI, Talcher GU21000531 Talcher Tech. Education Dev. Centre, ITC Tentulei, (TTEDC) Bidyut PU21000024 Colony, Talcher, Angul-759106. ANGUL GU21000531 ESSEL ITC, At/PO- Kaniha Talcher, Dist.-Angul, PR21000219 ANGUL GU21000531 Regional ITC, Banarpal, Angul-759128 PU21000005 ANGUL GU21000531 Biswanath ITC, At/PO - Budhapanka Banarpal, Dist.- Angul, PR21000209 ANGUL GU21000531 Sivananda Private ITI PR21000501 2 ANGUL Adarsha ITC, At/PO-Rantalei,Dist- Angul, PR21000142 Vasudev ITC,Angul PR21000319 ANGUL PR21000142 Satyanarayan ITC, At-Boinda, PO-Kishoreganj, Dist-Angul – 759127 PR21000122 (105) ANGUL PR21000142 Gayatree ITC PR21000218 ANGUL PR21000142 OP Jindal Institute of Technology & Skills ITC, Near S.P. Office, PU21000453 At/Po/Dist-Angul, 3 ANGUL Akhandalmani ITC , At/Po. Banarpal, Dist- Angul- 759128. PR21000410 Govt. ITI, Talcher GU21000531 ANGUL PR21000410 Maa Budhi ITC,l. At-Maratira,P.O-Tubey, DIST-Anugul-759145. PU21000086 4 ANGUL Guru Krupa ITC, At-Jagannathpur, Via-Talcher, Dist-Angul- PR21000113 Shree Dhriti ITC, Jagannath Nagar, At/Po-Gotamara, Dist-Angul- PR21000323 759101. 759135 ANGUL PR21000113 Swami Nigamananda ITC Narsingpur Cuttack PR21000400 5 ANGUL ITC, Angul, RCMS, Campus, Hakimpada, Anugul-759143. PU21000001 Aluminium ITC At-kandasara, Nalconagar, Anugul-759122. PR21000104 ANGUL PU21000001 Adarsha ITC, At/PO-Rantalei,Dist- Angul, PR21000142 PU21000001 Diamond ITC, At/PO-Rantalei, Dist- Angul-759122, PR21000192 6 ANGUL ITC, Rengali, Rengali dam site, Dist. Angul, PIN-759105. PR21000335 Pallahara Institute of Industrial Training & Skill ITC, At - Subarnapali, PR21000216 Seegarh, Dist.- Angul, ANGUL PR21000335 Malyagiri ITC, Batisuan, Nuasahi Dimiria Pallahara, Anugul, PR21000358 7 ANGUL Kaminimayee ITC, At/Po-Chhendipada, Angul.