Chapter III Compliance Audit DEPARTMENT of COOPERATION

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Odisha District Gazetteers Nabarangpur

ODISHA DISTRICT GAZETTEERS NABARANGPUR GOPABANDHU ACADEMY OF ADMINISTRATION [GAZETTEERS UNIT] GENERAL ADMINISTRATION DEPARTMENT GOVERNMENT OF ODISHA ODISHA DISTRICT GAZETTEERS NABARANGPUR DR. TARADATT, IAS CHIEF EDITOR, GAZETTEERS & DIRECTOR GENERAL, TRAINING COORDINATION GOPABANDHU ACADEMY OF ADMINISTRATION [GAZETTEERS UNIT] GENERAL ADMINISTRATION DEPARTMENT GOVERNMENT OF ODISHA ii iii PREFACE The Gazetteer is an authoritative document that describes a District in all its hues–the economy, society, political and administrative setup, its history, geography, climate and natural phenomena, biodiversity and natural resource endowments. It highlights key developments over time in all such facets, whilst serving as a placeholder for the timelessness of its unique culture and ethos. It permits viewing a District beyond the prismatic image of a geographical or administrative unit, since the Gazetteer holistically captures its socio-cultural diversity, traditions, and practices, the creative contributions and industriousness of its people and luminaries, and builds on the economic, commercial and social interplay with the rest of the State and the country at large. The document which is a centrepiece of the District, is developed and brought out by the State administration with the cooperation and contributions of all concerned. Its purpose is to generate awareness, public consciousness, spirit of cooperation, pride in contribution to the development of a District, and to serve multifarious interests and address concerns of the people of a District and others in any way concerned. Historically, the ―Imperial Gazetteers‖ were prepared by Colonial administrators for the six Districts of the then Orissa, namely, Angul, Balasore, Cuttack, Koraput, Puri, and Sambalpur. After Independence, the Scheme for compilation of District Gazetteers devolved from the Central Sector to the State Sector in 1957. -

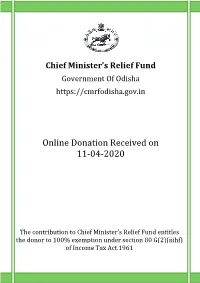

Online Donation Re Donation Received on 11-04-2020 On

Chief Minister’s Relief Fund Government Of Odisha https://cmrfodisha.gov.in Online Donation Received on 11-04-2020 The contribution to Chief Minister's Relief Fund entitles the donor to 100% e xemption under section 80 G(2)(iiihf) of Income Tax Act.1961 https://cmrfodisha.gov.in Donor Details Sl. Name and Address of Donor Amount Abinash Sahoo 1 100000 Khurdha Neha Enterprises 2 100000 Khurda Pawan Consumer Care 3 100000 Khurda Alekha Kumar Das 4 51000 Khurdha Sumanta Sathua 5 51000 Puri Chandra Mohan Behera 6 25000 Mayurbhanj Puspita Behera 7 25000 Mayurbhanj Asruta Pritam 8 20000 Bhadrak Forest Range Office Bargarh 9 15790 Bargarh Head Master And Staff 10 15000 Rayagada Turunji Christian Mandali 11 13000 Nabarangpur Basanta Kumar Tripathy 12 11111 Bhubaneswar Soumyakanta Mahalik 13 11111 Angul Ms Krishna Rig Service 14 11000 Kalahandi Prafulla Kumar Gachhayat 15 10001 Khordha Trilochan Mahanta 16 10001 Kendujhar Abhinaba Kumar Rao 17 10000 Sambalpur Bc Kavya 18 10000 Puri Online Donation Received on 11-04-2020 Page 2 https://cmrfodisha.gov.in Bikash Prasad Das 19 10000 Cuttack Debasmita Sahu 20 10000 Jharsuguda Gayatri Jena 21 10000 Cuttack Kumar Sourabh 22 10000 Keonjhar Sanjeeb Kumar Mohanty 23 10000 Khurda S P Kar 24 10000 Sundargarh Sudarshan Send 25 10000 Balasore Veer Surendra Sai Institute Of Medical Science And Research 26 8200 Sambalpur Mohini Hota 27 8096 Sambalpur Santanu Sengupta 28 8000 Sambalpur Prabhu Panda 29 7500 Bhadrak Priyadarshinee Naik 30 5100 Kalahandi Benjamin Kujur 31 5001 Rourkela Mandakini Kar 32 5001 Keonjhar -

Name of the District Name of the Block Sl No Name of the L.I.Projects Ty Pe Ayacut Scheme Date of Energisation Expenditure I

LIST OF L.I.PROJECTS ENERGISED DURING 2ND QUARTER OF THE FY 2018-19 Name of the District Name of the Block Sl Name of the L.I.Projects Scheme Date of Expenditure Name of the PP No Type energisation incurred Ayacut in Rs I II III IV V VI VII VIII IX X Angul Angul 1 Talabahal RL 20 RIDF 2018-19 30.08.2018 1347200 Brahmanidei P.P. Angul Angul 2 Badabahal RL 20 RIDF 2018-19 30.08.2018 1347200 Basantadei P.P. Angul Chhendipada 3 Bhejidiha-I RL 20 RIDF 2018-19 07.09.2018 1296800 Maa Jharikuandei P.P. Angul Chhendipada 4 Bhejidiha-Ii RL 20 RIDF 2018-19 07.09.2018 1338400 Maa Dakinakali P.P. Angul Pallahara 5 Benipathar-I RL 20 RIDF 2018-19 31.08.2018 1243200 Maa Hingula P.P. Angul Pallahara 6 Benipathar-II RL 20 RIDF 2018-19 31.08.2018 1152000 Maa Tarini P.P. Balangir Agalpur 7 Gandapali(B)-IV RL 20 RIDF 2018-19 30.07.2018 1478300 Dhananjaya P.P. Balasore Remuna 8 Baduan-VI TW 20 RIDF 2018-19 30.07.2018 1448000 Baduan-VI Balasore (Jls) Basta 9 Naikudi-IV TW 20 RIDF 2018-19 27.09.2018 1488000 Raghunath Jew Balasore (Jls) Bhograi 10 Bartana-VI RL 20 RIDF 2018-19 27.09.2018 1016000 Aurobindo Balasore (Jls) Bhograi 11 Hadaki RL 20 RIDF 2018-19 27.09.2018 1166000 Indu Balasore (Jls) Jaleswar 12 Olinda-II TW 20 RIDF 2018-19 30.07.2018 1292000 Subarnarekha Bargarh Gaisilat 13 Jankeda-VI RL 20 RIDF 2018-19 30.07.2018 1509000 Bajrangbali PP Bargarh Gaisilat 14 Bheluapadar-VI RL 20 RIDF 2018-19 25.08.2018 2063000 Bheluapadar-VI PP Bargarh Jharbandh 15 Badkunjari-IV RL 20 RIDF 2018-19 28.09.2018 2012000 Maa Ghanteswari PP Bargarh Padampur 16 Kumunibahali-III -

CLINICAL ESTABLISHMENTS in KHURDA C.E Period of Validity Sl

CLINICAL ESTABLISHMENTS IN KHURDA C.E Period of Validity Sl. Name of the Clinical Name of the Name of the I/C Bed District Regd. No. Establishment Proprietor Doctor Strength No. From To Biswanath Nursing Home, Dr. Prasanta Dr. Prasanta Kumar 1 Khurda 018/98 12 23-05-2007 22-05-2009 Jatni, Plot No- 146, Khurda Kumar Panda Panda, MBBS Sayed Memorial Hospital, Dr. Md. Zahir Dr. Md. Zahir Baig, 2 Khurda 210/03 40 27-05-2014 26-05-2016 Kudiarybazar, Jatni Baig MBBS AVA Hospital, Main Road, Smt. Jharana Dr. Gangadhar 3 Khurda 361/04 6 09-09-2010 08-09-2014 Balugaon Mohapatra Satpathy Smt. Sangita Health Care Nursing Home, Dr. Satya Ranjan 4 Khurda Samanta & 510/06 6 24-04-2010 23-04-2012 Mangalanagar Das, MD Sorojini Swain Sri Sibananda Dr. Suresh Ch. 5 Biswal Patho Lab., Balakati Khurda 586/06 07-11-2010 06-11-2012 Biswal Pradhan Smt. Prachi Hospital & Research Dr. Gagan Bihari 6 Khurda Truptimayee 608/06 14 23-12-2010 22-12-2012 Centre, At-Paltan Padia, Nayak, MBBS Devi Sri Maa Clinial Laboratory, Dr. Nagen Ku. 7 Khurda Ramesh Ch. Sahu 751/07 28-08-2008 27-08-2010 At/Po- Jatin Debata Sulavita Patho. Logical Clinic, Smt. Snigdha Dr. Girish Ch. 8 Buxi -Lane-chritian-Sahi, Khurda 945/08 18-01-2011 17-01-2013 Behera Mishra,MD (Patho.) Khurda. Dr. Manmohan Hospital & Dr. Manmohan Dr. Manmohan 9 Khurda 990/08 22-02-2009 21-02-2011 Research Centre, Balugaon Mohapatra,MBBS Mohapatra, MBBS Dr. Ashok Ku. -

Orissa High Court Filing Report As on :29/10/2020

ORISSA HIGH COURT FILING REPORT AS ON :29/10/2020 SL FILING NO NAME OF PETNR./APPEL COUNSEL FOR PETNR./APPEL PS CASE/LOWER COURT CASE/DISTRICT 1 BLAPL/0007835/2020 HEMANT DAS TANMAYA KUMAR MOHANTY ANGUL TOWN /1109 /2020 VS VS S.D.J.M. CIVIL JUDGE (JD),ANGUL(Anugul *) STATE OF ODISHA GR/0001832/2020 2 BLAPL/0007836/2020 D. DURGA JULU KHANSAMA BIRMAHARAJPUR /120 /2020 VS VS S.D.J.M.,BIRAMAHARAJPUR(Sonapur *) STATE OF ODISHA GR/0000212/2020 3 BLAPL/0007837/2020 HARIRAM GANDA DIGAMBAR SETHI ORKEL /13 /2020 VS VS SPECIAL JUDGE,MALKANGIRI(Malkangiri *) STATE OF ODISHA TR/0000018/2020 4 BLAPL/0007838/2020 BANAMALI PRADHAN @ BANU R.N.MOHANTY SATYABADI /28 /2020 VS VS S.D.J.M.,PURI(Puri) STATE OF ODISHA GR/0000205/2020 5 BLAPL/0007839/2020 GADA @ GADADHAR NAYAK @ DASARATHI PARTHANAYAK SARATHI DAS BAGHAMARI /55 /2020 VS VS S.D.J.M.,KHURDA(Khordha *) STATE OF ODISHA GR/0000623/2020 6 BLAPL/0007840/2020 DEBENDRA MANDAL UMAKANTA BARIK UMERKOTE /112 /2020 VS VS ADJ,UMERKOTE(Nabarangapur *) STATE OF ODISHA CT/0000032/2020 7 BLAPL/0007841/2020 ANIL SAHANI S.K.BHANJADEO BORIGUMMA /68 /2018 VS VS SESSIONS JUDGE-CUM-SPL.JUDGE,KORAPUT(Koraput) STATE OF ODISHA TR/0000016/2018 8 BLAPL/0007842/2020 CHANDAN NAIK S.K.BHANJADEO ANGUL TOWN /570 /2020 VS VS S.D.J.M. CIVIL JUDGE (JD),ANGUL(Anugul *) STATE OF ODISHA GR/0000898/2020 9 BLAPL/0007843/2020 NABA @ NABINA NAIK @ NAVEENA NAIK S.K.BHANJADEO ANGUL TOWN /937 /2019 VS VS S.D.J.M. -

Defaulter-Private-Itis.Pdf

PRIVATE DEFAULTER ITI LIST FOR FORM FILL-UP OF AITT NOVEMBER 2020 Sl. No. District ITI_Code ITI_Name 1 ANGUL PR21000166 PR21000166-Shivashakti ITC, AT Bikash Nagar Tarang, Anugul, Odisha, -759122 2 ANGUL PR21000192 PR21000192-Diamond ITC, At/PO Rantalei, Anugul, Odisha, -759122 3 ANGUL PR21000209 PR21000209-Biswanath ITC, At-PO Budhapanka Via-Banarpal, Anugul, Odisha, - 759128 4 ANGUL PR21000213 PR21000213-Ashirwad ITC, AT/PO Mahidharpur, Anugul, Odisha, -759122 5 ANGUL PR21000218 PR21000218-Gayatri ITC, AT-Laxmi Bajar P.O Vikrampur F.C.I, Anugul, Odisha, - 759100 6 ANGUL PR21000223 PR21000223-Narayana Institute of Industrial Technology ITC, AT/PO Kishor, Anugul, Odisha, -759126 7 ANGUL PR21000231 PR21000231-Orissa ITC, AT/PO Panchamahala, Anugul, Odisha, -759122 8 ANGUL PR21000235 PR21000235-Guru ITC, At.Similipada, P.O Angul, Anugul, Odisha, -759122 9 ANGUL PR21000358 PR21000358-Malayagiri Industrial Training Centre, Batisuand Nuasahi Pallahara, Anugul, Odisha, -759119 10 ANGUL PR21000400 PR21000400-Swami Nigamananda Industrial Training Centre, At- Kendupalli, Po- Nukhapada, Ps- Narasinghpur, Cuttack, Odisha, -754032 11 ANGUL PR21000422 PR21000422-Matrushakti Industrial Training Institute, At/po-Samal Barrage Town ship, Anugul, Odisha, -759037 12 ANGUL PR21000501 PR21000501-Sivananda (Private) Industrial Training Institute, At/Po-Ananda Bazar,Talcher Thermal, Anugul, Odisha, - 13 ANGUL PU21000453 PU21000453-O P Jindal Institute of Technology & Skills, Angul, Opposite of Circuit House, Po/Ps/Dist-Angul, Anugul, Odisha, -759122 14 BALASORE -

Cultural Life of the Tribals of the Koraput Region

Odisha Review ISSN 0970-8669 Cultural Life of the Tribals of the Koraput Region Rabindra Nath Dash If one thinks of cultural history of primitive tribes Literarily the definition of their culture is so broad one must turn towards south Odisha, the hub of that we appreciate and accept every aspect of tribals. So this Koraput region, the domain of their life style which is associated with culture. tribals has become centre of study and research. In 1863 this region was under direct Although the tribal population in Odisha administration of British. The Government of India has around 25%, their contribution in the Act of 1919 declared the entire area of Koraput development process of the state is outstanding. district as Scheduled Area and the major tribes Their tradition and culture is broad and inhabiting the district have been declared as uncommon. And the cultural history of tribals of scheduled tribes. this undivided Koraput has special importance all over India. The tribal population consists of Normally the primitive tribes express the 53.74% in the undivided Koraput (now divided cultural identity through their custom, tradition, into 4 districts Koraput, Rayagada, Nawarangpur, festivals, dress and ornaments. Every tribe has a and Malkangiri) as per 2001 census. The certain place of origin and its spreading. They anthropologist study gives an account that there have their own oral and written language for are 62 types of tribes in Odisha. They all live in interaction of each other. The matrimonial alliance the above districts although their number is so of a tribe is arranged byits own community as small. -

List of Engineering Colleges Under Bput Odisha

LIST OF ENGINEERING COLLEGES UNDER BPUT ODISHA SN NAME OF THE COLLEGE Category Address-I Address-II Address-III Dist PIN Name of the Trust Chairman Principal/Director Contact No. e-mail ID 1 ADARSHA COLLEGE OF ENGINEERING, Private Saradhapur Kumurisingha Angul 759122 Adarsha Educational Trust Mr. Mahesh Chandra Dhal Dr. Akshaya Kumar Singh 7751809969 [email protected] ANGUL 2 AJAY BINAY INSTITUTE OF TECHNOLOGY, Private Plot No.-11/1/A Sector-1 CDA Cuttack 753014 Ajay Binay Institute of Technology- Dr. K. B. Mohapatra Dr. Leena Samantaray 9861181558 [email protected] CUTTACK Piloo Mody College of Achitecture 3 APEX INSTITUTE OF TECHNOLOGY & Private On NH-5 Pahala Bhubaneswar Khurda 752101 S.J.Charitable Trust Smt. Janaki Mudali Dr. Ashok Kumar Das 9437011165 MANAGEMENT, PAHALA 4 ARYAN INSTITUTE OF ENGINEERING & Private Barakuda Panchagaon Bhubaneswar Khurda 752050 Aryan Educational Trust Dr. Madhumita Parida Prof.9Dr.) Sudhansu Sekhar 9437499464 [email protected] TECHNOLOGY, BHUBANESWAR Khuntia 5 BALASORE COLLEGE OF ENGINEERING & Private Sergarh Balasore 756060 Fakirmohan Educational & Charitable Mr. Manmath Kumar Biswal Prof. (Dr) Abhay Kumar 9437103129 [email protected] TECHNOLOGY, BALASSORE Trust Panda 6 BHADRAK INSTITUTE OF ENGINEERING Private Barapada Bhadrak 756113 Barapada School of Engineering & Sri Laxmi Narayan Mishra Prof.(Dr.) Mohan Charan 9556041223 [email protected] AND TECHNOLOGY, BHADRAK Technology Society Panda 7 BHUBANESWAR COLLEGE OF Private Khajuria Jankia Khurda Oneness Eductationa & Charitable -

The Orissa G a Z E T T E

The Orissa G a z e t t e EXTRAORDINARY PUBLISHED BY AUTHORITY No. 412 CUTTACK, FRIDAY, MARCH 24, 2006 / CHAITRA 3, 1928 LAW DEPARTMENT NOTIFICATION The 23rd March, 2006 S. R. O. No. 104/2006—In pursuance of section 11-A of the Legal Services Authorities Act, 1987 (39 of 1987), read with rule 13 of the Orissa State Legal Services Authority Rules, 1996, the State Government in consultation with the Chief Justice of the Orissa High Court, do hereby nominate the other members required under sub-rule (3) of rule 13 of the said rules as specified in column (3) of the Schedule below for the Taluk Legal Services Committee of the State mentioned against each in column (2) thereof constituted in the notification of the Orissa State Legal Services Authority No. 1519-A/1997, dated the 16th August 1997, No. 156-A/1997, dated the 30th January 1997 and No. 3/2002, dated the 12th December 2002. SCHEDULE Sl. Name of the Taluk Name of the other members of No. Legal Services Committee the Taluk Legal Services Committee under sub-rule (3) of rule 13 (1) (2) (3) 1 Athagarh . (1) Shri Debendra Kumar Behera, Journalist, Medical Road, At/P.O. Athagarh, Dist. Cuttack. (2) Smt. Puspalata Mohanty (Social Worker), (Life Member, Bharat Krushak Samaj), At Talagarh, P. O. Kulailo, Dist. Cuttack. 2 Banki . (1) Shri Samanta Narayan Srichandan Mohapatra, At-Bankigarh, P.O. Durgapur, Dist. Cuttack. (2) Shri Sarat Ch. Mohapatra, At Patapur, P.O. Patapur, Dist. Cuttack. 3 Khurdha . (1) Nirupama Mishra, At Indira Gandhi Padia (Khurdha Town), P.O./Dist. -

Health Centers

LIST OF HEALTH CENTERS OF NUAPADA DISTRICT SL.No Name of the Block Name of the CHC Name of the Sector Name of the SC Name of the PHC(N) 1 Beltukuri PHC(N), BELTUKRI 2 Beltukri Bisora 3 Bhaleswar 4 Biromal PHC(N), BIROMAL 5 Jampani Biromal 6 Kuliabandha 7 Kodomeri 8 Darlimunda PHC(N) ,DARLIMUNDA 9 Saipala 10 Maulibhata Darlimunda 11 Tanwat 12 Godfula NUAPADA CHC, KHARIAR ROAD 13 Kotenchuan 14 Dharambandha PHC(N),DHARAMBANDHA 15 Motanuapada 16 Kendubahara Dharambandha 17 Amanara 18 Sarabong 19 Maraguda 20 Parkod CHC Khariar road 21 Jenjera 22 Khariar road Amsena 23 Gotma 24 Khariar Road 25 Tarbod PHC(N), TARBOD 26 Jatgarh 27 Darlipada 28 Turbod Siallati 29 Kurumpuri 30 Samarsingh 31 Lakhna 32 Budhikomna PHC(N), BUDHHIKOMNA Budhikomna CHC,KOMNA & CHC , KOMNA BHELLA 33 Kandetara 34 Budhikomna Nuagaon 35 Gandamer PHC(N) ,DARLIPADA CHC,KOMNA & CHC , 36 KOMNA Suklimundi BHELLA 37 Bhella PHC(N),SUNABEDA 38 Agren 39 Rajna Bhela 40 Chhata 41 Bisibahal 42 Sunabeda 43 Konabira 44 Pendrawan 45 Komna Tikrapada 46 Udyanbandh 47 Komna 48 Duajhar PHC(N),DUAJHAR 49 Kotamal 50 Nehena 51 DUAJHAR Kirkita 52 Dhanksar 53 Birighat 54 Lanji PHC(N), TUKLA 55 Bargaon 56 Khudpej KHARIAR CHC,KHARIAR 57 Bargaon Badmaheswar 58 Bhojpur PHC(N), LANJI 59 Bhuliasikuan 60 Amlapali 61 Lachhipur 62 Badi Khariar 63 Khasbahal 64 Khariar 65 Tukla 66 Sinapali PHC(N) ,LIAD Sinapali SINAPALI CHC,SINAPALI 67 Bramhaniguda 68 Bargaon Sinapali 69 Gandabahali 70 Godal 71 Singhjhar 72 Hatibandha PHC(N),HATIBANDHA 73 Chalna Hatibandha 74 Bharuamunda 75 SINAPALI CHC,SINAPALI Makhapadar 76 Timanpur PHC(N), TIMANPUR 77 Timnapur Niljee 78 Gorla 79 Kendumunda 80 Badibahal Kendumunda 81 Kuliadunguri 82 Nagalbod 83 Boden Bhainsadani PHC(N) Bhainsadani 84 Boden 85 BODEN Boirgaon 86 BODEN Damjhar PHC(N),DAMJHAR 87 BODEN Nagpada 88 BODEN Sunapur 89 BODEN Karlakot 90 BODEN Khaira 91 BODEN Karangamal Karngamal PHC(N), KARANGAMAL CHC,BODEN 92 BODEN Kulekela 93 BODEN Farsara 94 BODEN Larka 95 BODEN Litisargi 96 BODEN Rokal 97 BODEN 98 BODEN. -

EXTRAORDINARY PUBLISHED by AUTHORITY No.231, CUTTACK, FRIDAY, FEBRUARY 16, 2018 / MAGHA 27, 1939

EXTRAORDINARY PUBLISHED BY AUTHORITY No.231, CUTTACK, FRIDAY, FEBRUARY 16, 2018 / MAGHA 27, 1939 FOOD SUPPLIES & CONSUMER WELFARE DEPARTMENT NOTIFICATION The 9th February, 2018 No. 2821–CW-40/2018 — In exercise of the powers conferred under section 8-A of the Consumer Protection Act, 1986 and rule 11 of the Odisha Consumer Protection Rules, 1988, the State Government do hereby constitute the District Consumer Protection Council for the District of Nuapada (mentioned hereinafter as the District Council ) with the following members :— (I) Collector, Nuapada .. Chairman (II) Sri Arka Keshari Singh Deo, Hon’ble M.P., Kalahandi or his Representative. .. Member (III) 1. Sri Basanta Kumar Panda ,Hon’ble M.L.A., Nuapada or his representative. .. Member 2. Sri Duryodhan Majhi, Hon’ble M.L.A., Khariar or his Representative. .. Member (IV) Smt. Namita Pradhan, President , Zilla Parishad , Nuapada or her representative. .. Member (V) 1. Smt. Tareswari Sahu, Chaiperson, Nuapada Panchyat Samiti. .. Member 2. Smt. Tapaswini Majhi,Chairperson, Sinapali Panchayat Samiti. .. Member (VI) 1.Smt. Sunita Jain, Chairperson, N.A.C., Khariar Road .. Member 2.Smt. Lileswari Majhi, Chairperson, N.A.C., Nuapada .. Member 3. Smt. Jhulana Behera, Chairperson, N.A.C., Khariar .. Member (VII) Superintendent of Police, Nuapada or his representative (Not below the rank of DSP) .. Member (VIII) DSP, Vigilance, Nuapada .. Member (IX) Asst. Controller of Legal Metrology, Nuapada .. Member (X) Marketing Intelligence Officer, Bhawanipatna, Kalahandi. .. Member (XI) Asst. Commercial Tax Officer, Nuapada .. Member (XII) District Manager, FCI, Titilagarh, Bolangir. .. Member (XIII) District Co-ordinator, IOCL, Sambalpur. .. Member (XIV) Representative of OSWC .. Member (XV) Representative of State Consumer Federation . -

MAYURBHANJ C.E Period of Validity Sl

CLINICAL ESTABLISHMENTS IN MAYURBHANJ C.E Period of Validity Sl. Name of the Clinical Name of the Bed District Name of the I/C Doctor Regd. No. Establishment Proprietor Strength No. From To Dr. Durga Nursing Home, Dr. S.S.Khandelwal, 1 Mayurbhanj S.S.Khandelw 097/01 50 23-05-2013 22-05-2015 Baripada, Mayurbhanj MBBS al Orissa Nursing Home & Dr. Arun Ku. Dr. Arun Ku. 2 Mayurbhanj 151/01 5 23-05-2012 22-05-2014 Research Centre, Baripada Goswami Goswami,MBBS Dr. Salim's Nursing Home, Dr. Ghazala 3 Mayurbhanj Dr. Ghazala Salim 153/01 8 01-03-2003 28-02-2005 Karanjia, Salim Laxmikanta Sai X-Ray & Pathology, Pati, Dr. Prafulla Kumar 4 Mayurbhanj 157/02 06-08-2004 05-08-2006 Baripada Samerendra Kar Pati Smt. Jeevan Jyoti Hospital, G.B. Dr. Pradip Ch. 5 Mayurbhanj Chinmayee 311/04 01-03-2004 28-02-2006 Nagar Block Mahanta Satpathy Sarathi Nursing Home, At:- Capt.Partha 6 Mayurbhanj Dr. Kasinath Bisoi,MS 430/05 9 24-05-2013 23-05-2015 Shankhapata, Baripada Sarathi Jena Jaya Pathology, Hospital Sukanta Ku. Dr. R.K.Sahoo, 7 Mayurbhanj 449/05 09-09-2014 08-09-2016 Square, Ward No:-4,Baripada Dash M.B.B.S City Clinic, Hospital Square, Dr. Malaya 8 Mayurbhanj Dr. Malaya Ku. Panda 462/05 16-11-2005 15-11-2007 Baripada Ku. Panda Health Care Pathology Dr. Ramesh Dr. Ramesh Chandra 9 Laboratory & Clinic, Ganesh Mayurbhanj Chandra 511/06 15-04-2013 14-04-2015 Panigrahi,MD-Patho Market, Ward-6, Baripada Panigrahi Gayatri Nursing Hospital & Sri Gadadhar Dr.