Proposed Acquisition of 160A Gul Circle

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

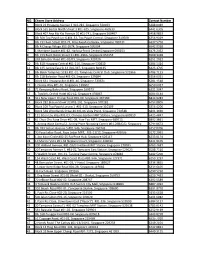

Ministry of Health List of Approved Providers for Antigen Rapid Testing for COVID-19 at Offsite Premises List Updated As at 6 Aug 2021

Ministry of Health List of Approved Providers for Antigen Rapid Testing for COVID-19 at Offsite Premises List updated as at 6 Aug 2021. S/N Service Provider Site of Event Testing Address of Site Date of Event Contact No. 1 OCBC Square 1 Stadium Place #01-K1/K2, Wave - Mall, Singapore 397628 57 Medical Clinic (Geylang Visitor Centre of Singapore Sports Hub 8 Stadium Walk, Singapore 397699 - 66947078 Bahru) Suntec Singapore Convention and Exhibition 1 Raffles Boulevard Singapore 039593 - Centre 2 57 Medical Clinic (Yishun) Holiday Inn Singapore Atrium 317 Outram Road, Singapore 169075 - 62353490 3 Asiamedic Wellness Asiamedic Astique The Aesthetic Clinic Pte. 350 Orchard Road #10-00 Shaw House - 67898888 Assessment Centre Ltd. Singapore 238868 4 Former Siglap Secondary School 10 Pasir Ris Drive 10, Singapore Acumen Diagnostics Pte. Ltd. - 69800080 519385 5 9 Dec 2020 13 and 14 Jan 2021 10 Bayfront Avenue, Singapore 24 and 25 Jan 2021 Sands Expo and Convention Centre 018956 4 Feb 2021 24 and 25 Mar 2021 19 Apr 2021 PUB Office 40 Scotts Road, #22-01 Environment - Building, Singapore 228231 The Istana 35 Orchard Road, Singapore 238823 3 and 4 Feb 2021 Ally Health 67173737 11 Feb 2021 One Marina Boulevard 1 Marina Boulevard, Singapore 018989 11 Feb 2021 Rasa Sentosa Singapore 101 Siloso Road, Singapore 098970 Shangri-La Hotel Singapore 22 Orange Grove Road, Singapore 22 Apr 2021 258350 D'Marquee@Downtown East 1 Pasir Ris Close, Singapore 519599 - Intercontinental Hotel 80 Middle Road, Singapore 188966 - Palfinger Asia Pacific Pte Ltd 4 Tuas Loop, Singapore 637342 - Page 1 of 148 ST ENGINEERING MARINE LTD. -

Passanger Terminal Buildings and SATS Inflight Catering Centre)

<Restricted># Appendix C Annex B1 CT2010B019 Page 1 of 6 TENDER FOR THE PROVISION OF TAXI SERVICE FROM 1 MAY 2021 TO 30 APRIL 2024 (WITH AN OPTION FOR EXTENSION FOR ANOTHER 2 YEARS) ` Rate of One-Way Trip from/to Place of Residence to/from Changi Airport (Passanger Terminal Buildings and SATS Inflight Catering Centre) OPTION YEAR POSTAL MAJOR HOUSING ESTATES AND RATE FOR ONE-WAY TRIP RATE FOR ONE-WAY TRIP ZONE DISTRICT ROADS IN ZONE 1ST YEAR 2ND YEAR 3RD YEAR 4TH YEAR 5TH YEAR 01XXXX a) Marina Grove b) Marina Mall 1 02XXXX a) Marina East (reclaimed land at end of ECP) 03XXXX a) Raffles Boulevard b) Temasek Boulevard 04XXXX a) Fullerton Road/Collyer Quay 05XXXX a) Smith St/Sago Lane/Upp Pickering St 06XXXX a) Cecil St/Telok Ayer St 2 07XXXX a) Anson Rd/Prince Edward Rd 08XXXX a) Tanjong Pagar/Cantonment Rd 09XXXX a) Bukit Purmei/Kampong Bahru Rd/Sentosa 10XXXX a) Telok Blangah/Gillman Heights 11XXXX a) South Bouna Vista Rd b) Pasir Panjang Rd/West Coast Highway 3 12XXXX a) Clementi Town b) West Coast Rd/Faber Drive c) Commonwealth Ave West 13XXXX a) Dover Road/North Bouna Vista Rd 14XXXX a) Stirling Rd b) Tanglin Halt Rd/Commonwealth Cres 4 15XXXX a) Lengkok Bahru/Bukit Merah 16XXXX a) Tiong Bahru/Indus Rd 17XXXX a) North Bridge Rd/Stamford Rd 18XXXX a) Bras Basah Rd/Selegie Rd/Beach Rd 19XXXX a) Jalan Sultan/Rochor Canal Rd 5 20XXXX a) Jalan Besar 21XXXX a) Serangoon Road 22XXXX a) Scotts Rd/Cairnhill Rd 23XXXX a) Orchard Rd/Clemenceau Ave 24XXXX a) Grange Rd/Tanglin Rd 25XXXX a) Stevens Rd/Cluny Rd 6 26XXXX a) Farrer Rd/King's Rd 27XXXX -

NO. Cheers Store Address Contact Number 1 Block 23 Hougang

NO. Cheers Store Address Contact Number 1 Block 23 Hougang Avenue 3 #01-281, Singapore 530023 6288 0049 2 Block 539 Bedok North Street 3 #01-625, Singapore 460539 6441 6305 3 Block 407 Ang Mo Kio Avenue 10 #01-741, Singapore 560407 6458 9853 4 Blk 500 Toa Payoh Lor 6 #01-33, Toa Payoh Central, Singapore 310500 6356 9029 5 Blk 231 Bain Street #01-21, Bras Basah Complex, Singapore 180231 6337 5750 6 Blk 4 Changi Village #01-2074, Singapore 500004 6542 9318 7 1 Maritime Square #01-82, HarbourFront Centre,Singapore 099253 6376 2452 8 Blk 153 Bukit Batok Street 11 #01-296A, Singapore 650153 6569 3418 9 269 Balestier Road #01-02/03, Singapore 329720 6251 2912 10 Blk 810 Hougang Central #01-214, Singapore 530810 6386 5414 11 Blk 135 Jurong East St 13 #01-337, Singapore 600135 6425 1705 12 Blk 866A Tampines St 83 #01-01, Tampines Central Club, Singapore 521866 6786 7113 13 Blk 218 Balestier Road #01-03, Singapore 329684 6256 6351 14 Block 631 Hougang Ave 8 #01-10, Singapore 530631 6281 4518 15 1 Create Way #01-01, Singapore 138602 6659 6017 16 71 Kampong Bahru Road, Singapore 169373 6221 3047 17 1 Traslink, Orchid Hotel #01-12, Singapore 078867 6604 6144 18 311 New Upper Changi Road #01-09, Singapore 467360 6844 9283 19 Block 282 Bishan Street 22 #01-101, Singapore 570282 6454 8805 20 Block 109 Toa Payoh Lorong 1 #01-310, Singapore 310109 6256 4206 21 Block 548 Woodlands Drive 44 #01-06 Vista Point, Singapore 730548 6891 1690 22 151 Boon Lay Way #01-03, Chinese Garden MRT Station, Singapore 609959 6425 4847 23 61 Choa Chu Kang Drive #01-09, Yew -

Toll City 60 Pioneer Road, Singapore 628509

WELCOME TO TOLL CITY A definitive travel TUAS ROAD TUAS guide to Toll City GUL CIRCLE Toll City 60 Pioneer Road, EW30 Singapore 628509 GUL CIRCLE MRT • 650 M away from Toll City side TUAS ROAD TUAS entrance • Designated walkway to Toll City from MRT EXIT A • Walk along Tuas Rd passing Jt Premier Pte and C & P Asia Pte TUAS AVE 5 GUL CIRCLE GUL CIRCLE GUL CIRCLE GUL CIRCLE BEF TUAS AVE 5 (NEAR W3) • Stop ID: 24521 • Bus Service: 193 AFT GUL LANE TUAS ROAD TUAS • Direction: CRES GUL (NEAR W2) From Boon Lay Int Tuas Terminal • Stop ID: 24209 JT Premier Pte Ltd • 23 Stops (Boon Lay Int • Bus Service: 255 included), get down at 24th • Direction: To Joo Koon Int (One stop. direction only) • 10 mins away from Opp • Recommended to take to and Fairprice Hub / 4 Stops after work GUL LANE GUL LANE • Recommended to take to work • 8 Stops (Joo Koon Int included), C & P Asia (S) Pte Ltd • Opp Bus Stop: Aft Tuas Ave 5 get down at 9th stop. GUL CRES GUL TUAS ROAD TUAS TUAS AVE 3 TOLL CITY PassengerCRES GUL Vehicle Entrance via Gul Cres Entrance TUAS ROAD TUAS GUL LANE GUL CRES GUL CRES GUL CRES BROADWAY CANTEEN TUAS ROAD TUAS Heavy Vehicle Entrance via Pioneer Road Entrance GUL LANE PIONEER ROAD PIONEER ROAD CANTEEN PIONEER ROAD AFT TUAS RDPIONEER (NEAR ROAD W1) PIONEER ROAD CHUANG HOCK • Stop ID: 24691 TUAS AMENITY • Direction: To Joo Koon Int CENTRE (One direction only) • Bus Service: 254 • Recommended to take after work TUAS ROAD TUAS • Opp Bus Stop: Bef Tuas Rd NTUC FAIRPRICE HUB PETROL. -

Terms and Conditions for Dash to Cheers Promotion

Terms and Conditions for Dash to Cheers Promotion 1. These Terms and Conditions for the Dash to Cheers (“Promotion”) are binding on all persons participating in the Promotion jointly organised by Telecom Equipment Pte Ltd (“Singtel”) and Cheers Holdings (2004) Pte Ltd (“Merchant” or “Cheers”) 2. The Promotion shall be a period starting from 23rd July 2020 to 31st August 2020 (inclusive of both dates), or upon the completion of the first 3,000 redemptions (“Promotion Period”), whichever is earlier. 3. Under the Promotion, and subject to these Terms and Conditions, Singtel Dash customers (“Eligible Customers”) who purchase S$10 or more worth of items at the following selected Cheers’ and/or FairPrice Xpress’ outlets during the Promotion Period, will enjoy a discount of S$1 off their purchases provided that they have successfully made full payment using Singtel Dash QR Code: Postal S/N Store Name Stores Address Code 1 Cheers Hougang Central CHGD Blk 810 Hougang Central #01-214 530810 2 Cheers Hougang Ave 8 CHG631 Block 631 Hougang Ave 8, #01-10 530631 3 Cheers SMRT Punggol SPUNGOL 70 Punggol Central, #01-02, Punggol NEL MRT station 828868 4 Cheers Seletar mall CSLML 33 Sengkang West Avenue #01-57/58/59 797653 5 Cheers Sengkang Community Hospital CSKCH 1 Anchorvale Street, Sengkang Community Hospital #01-23 544835 6 Cheers Downtown East CDTE 1 Pasir Ris Close Downtown East (“Resort”) #01-336 519599 7 Cheers Changi Village CHCV Blk 4 Changi Village #01-2074, 500004 8 Cheers Tampines Central Club CTMC Blk 866A Tampines St 83 #01-01, Tampines -

Dear Guest, a Very Warm Welcome to the Fullerton Bay Hotel

Dear Guest, A very warm welcome to The Fullerton Bay Hotel Singapore. Your comfort, safety and well-being are our top priority. From the moment you arrive, you will experience an elevated level of protection with the enhanced safety and cleanliness measures that we have put in place. Take your pick from a selection of cuisines and restaurants as you soak up the spectacular view of the Marina Bay waterfront, including classic French fare in a bistro setting at La Brasserie, a classic afternoon tea at The Landing Point, and bespoke cocktails at Gin Parlour or Lantern rooftop bar. Make your stay one to remember with a range of exciting Fullerton Experiences tailored just for you. This compendium provides you with information about the various services which you can enjoy during your stay with us. Our Fullerton Express team is also available to provide any assistance that you may require. Please do not hesitate to contact us at any time. We wish you a wonderful stay and many warm memories at The Fullerton Bay Hotel Singapore! Yours sincerely, Cavaliere Giovanni Viterale General Manager DIRECTORY OF SERVICES FULLERTON EXPRESS Fullerton Express has been established to ensure a quick response to telephone requests for the following areas: Duty Manager, Cashier/Front Desk, Housekeeping, Laundry/Valet, Engineering/Room Maintenance. If you require any assistance during your stay, please dial Fullerton Express using your in-room phone. ADAPTORS & TRANSFORMERS Please dial Fullerton Express using your in-room phone. AIR CONDITIONING Your room is fully air-conditioned. You may adjust the ventilation and the temperature level on the wall-mounted thermostat. -

G178 Bus Time Schedule & Line Route

G178 bus time schedule & line map G178 Tuas Naval Base View In Website Mode The G178 bus line Tuas Naval Base has one route. For regular weekdays, their operation hours are: (1) Tuas Naval Base: 6:05 AM Use the Moovit App to ƒnd the closest G178 bus station near you and ƒnd out when is the next G178 bus arriving. Direction: Tuas Naval Base G178 bus Time Schedule 14 stops Tuas Naval Base Route Timetable: VIEW LINE SCHEDULE Sunday Not Operational Monday 6:05 AM Buangkok Dr - Aft Sengkang East Dr (67739) Tuesday 6:05 AM Sengkang East Rd - Bef Sengkang East Ave (67469) Wednesday 6:05 AM Thursday 6:05 AM Sengkang East Rd - Sengkang General Hosp (67419) Friday 6:05 AM Punggol Way - Aft Tpe (65439) Saturday Not Operational 217D Sumang Lane, Singapore Punggol Way - Soo Teck Stn (65149) 21 Punggol Way, Singapore G178 bus Info Punggol Ctrl - Opp Blk 264a (65401) Direction: Tuas Naval Base Punggol Central, Singapore Stops: 14 Trip Duration: 75 min Punggol Ctrl - Blk 303d (65221) Line Summary: Buangkok Dr - Aft Sengkang East Dr 303D Punggol Place, Singapore (67739), Sengkang East Rd - Bef Sengkang East Ave (67469), Sengkang East Rd - Sengkang General Punggol Rd - Opp Blk 296 (65089) Hosp (67419), Punggol Way - Aft Tpe (65439), 195A Punggol Road, Singapore Punggol Way - Soo Teck Stn (65149), Punggol Ctrl - Opp Blk 264a (65401), Punggol Ctrl - Blk 303d Punggol Rd - Blk 102c (65079) (65221), Punggol Rd - Opp Blk 296 (65089), Punggol 102C Punggol Field, Singapore Rd - Blk 102c (65079), Tuas Rd - Gul Circle Stn Exit A (24511), Pioneer Rd - Hiap Teck Metal Co (24671), Tuas Rd - Gul Circle Stn Exit A (24511) Gul Rd - Opp Ge Keppel Energy Svcs (24389), Gul Rd - 7A Tuas Road, Singapore Opp Asia Ind Gases (24379), Tuas Naval Base (Drop Off Point) Pioneer Rd - Hiap Teck Metal Co (24671) 17 Gul Lane, Singapore Gul Rd - Opp Ge Keppel Energy Svcs (24389) Gul Rd - Opp Asia Ind Gases (24379) 21 Gul Road, Singapore Tuas Naval Base (Drop Off Point) G178 bus time schedules and route maps are available in an o«ine PDF at moovitapp.com. -

192 Bus Time Schedule & Line Route

192 bus time schedule & line map 192 Boon Lay Int View In Website Mode The 192 bus line (Boon Lay Int) has 2 routes. For regular weekdays, their operation hours are: (1) Boon Lay Int: 12:00 AM - 11:46 PM (2) Tuas Ter: 5:45 AM - 11:30 PM Use the Moovit App to ƒnd the closest 192 bus station near you and ƒnd out when is the next 192 bus arriving. Direction: Boon Lay Int 192 bus Time Schedule 33 stops Boon Lay Int Route Timetable: VIEW LINE SCHEDULE Sunday 12:00 AM - 11:46 PM Monday 12:00 AM - 11:46 PM Tuas West Dr - Tuas Ter (25009) 3 Tuas West Road, Singapore Tuesday 12:00 AM - 11:46 PM Tuas West Dr - Opp Tuas Link Stn (25421) Wednesday 12:00 AM - 11:46 PM Tuas West Dr - Super Continental (25431) Thursday 12:00 AM - 11:46 PM 21 Tuas West Drive, Singapore Friday 12:00 AM - 11:46 PM Tuas West Dr - Bef Pioneer Rd (25441) Saturday 12:00 AM - 11:46 PM 31 Tuas West Drive, Singapore Pioneer Rd - Bef Tuas West Ave (25681) 122 Pioneer Road, Singapore 192 bus Info Pioneer Rd - Tuas West Rd Stn Exit B (24711) Direction: Boon Lay Int 131 Pioneer Road, Singapore Stops: 33 Trip Duration: 45 min Tuas Ave 12 - Michelman (25511) Line Summary: Tuas West Dr - Tuas Ter (25009), 2A Tuas Avenue 12, Singapore Tuas West Dr - Opp Tuas Link Stn (25421), Tuas West Dr - Super Continental (25431), Tuas West Dr - Bef Tuas Ave 12 - Siem Seng Hing (25811) Pioneer Rd (25441), Pioneer Rd - Bef Tuas West Ave 8A Tuas Avenue 12, Singapore (25681), Pioneer Rd - Tuas West Rd Stn Exit B (24711), Tuas Ave 12 - Michelman (25511), Tuas Ave Tuas Ave 12 - Aft Tuas Ave 7 (25091) 12 -

IHP GP Clinic List.Pdf

IHP- NETWORK OF CLINICS IHP NETWORK OF CLINICS : Updated on 27 August 2021. Subject to changes without prior notice. Please contact IHP Helpdesk 6715 9422 or [email protected] for enquiries NOTE: The clinics details and operating hours indicated are correct at the time of update but you are advised to call the clinic prior to your visit (especially during festive periods/30min before closing hours) to avoid unnecessary inconvenience. Public Health Preparedness Clinic (PHPC) scheme consolidates the primary care clinic response to public health emergencies such as influenza pandemic, haze and anthrax outbreak into a single scheme for better management. For updated information clinic information within PHPC scheme, please refer to "https://www.flugowhere.gov.sg/" S/N IHP CLINIC ID REGION AREA CLINIC NAME ADDRESS POSTAL CODE TEL NO. FAX NO MON - FRI SAT SUN PUBLIC HOLIDAY REMARKS CHANGES OF THE MONTH PHPC SURCHARGE APPLICABLE WEEKDAYS AFTER 9PM: $15 39 JALAN TIGA 0800-1300 0800-1300 1 CG325 CENTRAL AIRPORT ROAD NORTHEAST (KALLANG) MEDICAL GROUP 390039 62413298 62413219 0800-1800 0800-1300 SAT AFTER 1PM: $15 1 #01-01 1400-2200 1800-2200 SUN: $15 PH: $15 460 ALEXANDRA ROAD 0830-1300 REGISTRATION ENDS 15MIN BEFORE 2 CG213 CENTRAL ALEXANDRA FULLERTON HEALTHCARE @ GETHIN-JONES MEDICAL PRACTICE PTE LTD (ALEXANDRA) 119963 63333636 62721049 CLOSED 0900-1200 0900-1200 1 #02-18 ALEXANDRA RETAIL CENTRE 1400-1800 CLOSING TIME 460 ALEXANDRA ROAD 0830-1300 3 CG1060 CENTRAL ALEXANDRA SHENTON MEDICAL GROUP (ALEXANDRA) 119963 63761630 CLOSED CLOSED CLOSED -

A Forward Force

A Forward Force Annual Report 2021 ABOUT AIMS APAC REIT (“AA REIT”) is a real estate investment trust listed on the AIMS APAC REIT Mainboard of the Singapore Exchange Securities Trading Limited (“SGX-ST”) since 2007. The principal investment objective of AA REIT is to invest in a diversified portfolio of income-producing industrial, logistics and business park real estate located throughout the Asia Pacific region. The real estate assets are utilised for a variety of purposes, including but not limited to warehousing & distribution activities, business parks activities and manufacturing activities. AA REIT’s portfolio consists of 28 properties, of which 26 properties are located throughout Singapore, and 2 in Australia. VISION MISSION To be the preferred Asia To provide investors with sustainable Pacific industrial, logistics long-term returns through strategic and business park real acquisitions and partnerships, prudent estate solutions provider to capital management and proactive asset our tenants and partners. management of a high quality industrial, logistics and business park real estate portfolio throughout Asia Pacific. On the Cover Breathtaking waterfalls are carved through nature’s rhythmic motion over geological timescales. They showcase how environmental elements can be forceful yet gentle, gradual yet radical, resilient yet flexible. It is a persistent progression, a continuous flow of energy and life. In similar fashion, our growth is a result of our unwavering dedication to seek constant progress. A strong flow of balanced -

001 210608 STELLAR ACE Ratebook.Pdf

2 3 STELLAR ACE With close to 100 stations and 2,200 billboards all over the island, we are definitely Singapore’s largest out-of-home marketing and advertising network. From digital screens and interactive ads in our stations, to ads carried around Singapore by our buses and taxis, or even vast on-site campaigns and installations, we have the perfect platform for you to advertise, create and engage the millions using our network daily. Speak to us, and let us provide you with unparalleled visibility to deliver your message and brand to large captive audiences. One of Singapore’s Largest Digital and OOH Media Company YOUR CUSTOMERS REACH AND ACTIVATE , CONNECT *Source: Marketing Magazine 2012, 2013 & 2014 WE 4 5 STELLAR ACE CONNECT ACTIVATE 21.1 million riders weekly • 296 trains • 105 stations • 1,450 buses • 3,380 taxis • 2,500 digital screens 2,297 billboards • 147 event spaces • 5 mobile advertising trucks • 6 outdoor digital billboards 20 hot food vending machines REACH DIGITAL YOUR CUSTOMERS REACH AND ACTIVATE , CONNECT WE STELLAR ACE COVERAGE MAP NS 10 NS 11 NS 12 NS 8 Fajar NS 13 BP 10 Segar BP 11 BP 9 Bangkit NS 14 Jelapang BP 12 BP 8 Pending Senja BP 13 BP 7 Petir NS 7 NS 15 Phoenix BP 5 NS 16 BP 4 Teck Whye NS 5 BP 3 Keat Hong EW 33 EW 1 CC 14 CC 16 BP 2 South View NS 18 EW 2 EW 32 DT 32 NS 19 CC 12 EW 31 EW 3 EW 5 CC 11 EW 30 NS 20 NS 3 EW 6 CG 2 EW 29 CC 20 EW 7 EW 28 NS 2 CC 21 EW 27 EW 9 NS 23 CC 8 EW 26 EW 25 EW 23 EW 22 EW 10 EW 20 CC 23 EW 11 CC 7 EW 19 CC 24 EW 18 CC 2 CC 6 EW 17 CC 25 CC 5 CC 3 CC 26 33 34 DT DT CC -

HENG HARDWARE ENGINEERING PTE LTD LISTS of PROJECTS USING HENG LIGHTNING PROTECTION SYSTEM Project Type:Industrial

HENG HARDWARE ENGINEERING PTE LTD LISTS OF PROJECTS USING HENG LIGHTNING PROTECTION SYSTEM Project Type:Industrial S/N PROJECT 1 10 SAKRA AVE ON JURONG ISLAND 2 104 Gul Circle 3 12 Gul Street 3 4 15 Gul Way 5 15 Gul Way 6 158 Kallang Way 7 18 Tractor Road 8 19 Gul Lane 9 2 STOREY PODIUM & 7 STOREY TOWER BLOCK AT CHANGI EAST 10 20 Gul Way 11 20 Gul Way Phase 3 12 21 Sakra Road Jurong Island 13 2m2p Science Park 14 2NOS OF RC BUILDING AT CHANGI EAST 15 2STOREY FACTORY AT SENOKO AVENUE 16 3 Storey Office at Mountbatten Road 17 31 INTERNATIONAL BUSINESS PARK CREATIVE 18 400KV SUBSTATION AT AYER RAJAH CRESCENT 19 47 Jalan Buroh 20 47 Tuas View Circuit 21 5 Neythal Road 22 5 Neythal Road Phase 2 23 5 Storey Multi User Industrial Building 24 50 Tuas Link 4 25 5A Toh Guan Road East 26 6STOREY WAREHOUSE AT CHANGI SOUTH 27 6-STY INDUSTRIAL BUILDING 28 7 Changi South Lane 29 7 STOREY BENDEEMER WAREHOUSE 30 7 STR IND AVIATION COMPLEX AT SELETARE AERO-SPACE 31 75 Science Park 32 8 Sty General Idustrial Building at Sengkang Kadut Street 3 33 8STOREY FLATTED FACTORY AT GEYLANG LORONG 23 34 9 Sungei Kadut St 3 35 95 Mega Yard 36 96A Jalan Senang 37 A & A CADBURY SCHWEPPERS AT 346 JALAN BOON LAY 38 A & A TO 7 STOREY WAREHOUSE AT TUAS 39 A Rc Building at PLAB 40 A&A to 273 Jalan Ahamad Ibrahim 41 A&A to 56 Woodlands Terrace 42 ABB FACTORY (A & A WORKS) NO.7 YISHUN INDUSTRIAL STREET 1, #01-48 NORTH SPRING BIZHUB, S(768162) TEL:68464111 FAX:68464222 Web:www.heng.com.sg Email:[email protected] HENG HARDWARE ENGINEERING PTE LTD LISTS OF PROJECTS USING HENG