Essilor and Luxottica – Clearance Determination

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Essilorluxottica 28 May 2019 Update to Credit Analysis Following Affirmation of A2

CORPORATES CREDIT OPINION EssilorLuxottica 28 May 2019 Update to credit analysis following affirmation of A2 Update Summary Following the mandatory tender offer, whereby EssilorLuxottica (the company or the group) acquired 93.3% of Luxottica's shares, the company subsequently launched a sellout and squeeze-out of the remaining shares for a combination of stock issuances and a cash consideration of about €640 million. As of March 5, 2019, EssilorLuxottica controlled all the RATINGS share capital of Luxottica, whose shares have been delisted from the Italian stock exchange. EssilorLuxottica Domicile France EssilorLuxottica's A2 rating continues to reflect (1) its position as the global leader in Long Term Rating A2 corrective lenses and eyewear market by a large margin to its competitors, illustrating the Type LT Issuer Rating - Fgn group's strong innovation capabilities and brand portfolio; (2) the group's wide offering Curr within its product category and its vertical integration, which allow it to cater to a variety Outlook Stable of customers and develop strong relationships with opticians; (3) a very solid track record Please see the ratings section at the end of this report of steady growth and resilient operating performance; and (4) the group's strong financial for more information. The ratings and outlook shown profile, underpinned by a healthy free cash flow (FCF) generation. reflect information as of the publication date. EssilorLuxottica's rating also factors in (1) the group's concentration of sales generated by its corrective lenses and frames business, as well as its relative concentration in the US market; Contacts (2) the still subdued economic environment in some of the group's key markets, which can Knut Slatten +33.1.5330.1077 weigh on lenses' renewal rates or result in some trading down by consumers; (3) the risk of a VP-Senior Analyst competitor making a breakthrough innovation; and (4) a degree of uncertainty around future [email protected] financial policies and the group's appetite for future external growth. -

Monthly Amendments Individual Additions

Monthly Amendments Individual Additions GOC Title Forenames Surname Company Name Address 1 Address 2 Address 3 Town County Postcode Country Join Date Number 01-30601 Mr Damien Greene Roscrea 02/11/2017 01-30602 Miss Aisha Bhatti Boots Opticans 177-185 High Ilford Essex IG1 1DG UNITED 01/11/2017 Road KINGDOM 01-30603 Mr Robert Slupek Specsavers 78 Commercial Batley West Yorkshire WF17 5DS UNITED 03/11/2017 Opticians Street KINGDOM 01-30604 Miss Kirandeep Ubi iOptics 376 Bath Road Hounslow TW4 7HT United Kingdom 03/11/2017 01-30605 Miss Sonia Jabbar Glasgow 03/11/2017 01-30607 Mr Rishi Hirani Tesco Opticians Brookfield Cheshunt Waltham Cross Hertfordshire EN8 0TA United Kingdom 03/11/2017 Centre 01-30608 Mr Hassan Iqbal Rochdale 03/11/2017 01-30609 Mr Kultaar Singh Specsavers 201 High Street Kirkcaldy Fife KY1 1JD UNITED 03/11/2017 Opticians KINGDOM 01-30610 Ms Kerrie Mcgarvey Specsavers 21-25 Week Maidstone Kent ME14 1QS United Kingdom 03/11/2017 Opticians Street 01-30611 Ms Maryum Mahmood Specsavers 7B Crown Matlock Derbyshire DE4 3AT United Kingdom 03/11/2017 Opticians Square 01-30612 Mr Naveed Akmal Specsavers 22 London road Bognor Regis West Sussex PO21 1PY UNITED 06/11/2017 KINGDOM 01-30613 Miss Rebecca Martinez Specsavers 65-66 Taff Street Pontypridd Rhondda Cynon CF37 4TD United Kingdom 06/11/2017 Opticians Taff 01-30614 Mr Eoin O'Connor Ratoath 07/11/2017 01-30615 Miss Alicia Kaushal Specsavers Unit 2 11-16 Biggin Dover Kent CT16 1BD UNITED 08/11/2017 Opticians Street KINGDOM 01-30616 Miss Katie Carmichael Boots Opticians Clayton -

Specsavers Opticians Is the Largest Privately Owned Opticians in the World and One of the UK’S Most Successful Retailers (Source: Retail Week 2005)

34069_CSB_094-095_Specsav 4/6/2007 06:55 Page 94 Specsavers Opticians is the largest privately owned opticians in the world and one of the UK’s most successful retailers (Source: Retail Week 2005). Nearly one in three people who wear glasses in the UK buy them from Specsavers. Run by husband and wife founders Doug and Mary Perkins, Specsavers is also a success abroad, where it has 270 stores in Europe, plus a rapidly expanding supply chain in Australia. which were through the NHS. A further 252,000 eye examinations were conducted in Republic of Ireland stores and 14,000 in the Channel Islands where there is no NHS. Much of Specsavers’ success can be attributed to its joint venture concept. Stores are owned and run by more than 1,000 optician joint venture or franchise partners, while a full range of support services, from accounting to marketing, are provided by a team of professionals, freeing the optician to do what he does best – provide the highest quality customer service. Achieving exacting standards in a high volume business requires state-of-the-art operations, so Specsavers has invested heavily in new systems and equipment to ensure that its supply chain partners attain world-class standards. Market record like-for-like increases in 2007 and Product The current UK market for eyecare products record sales of £16 million in one week. Specsavers Opticians has maintained the and services is estimated at more than Expansion in Europe, where Specsavers is Perkins’ philosophy of providing affordable, £2 billion, with less than 40 per cent still one of the few British retail success stories, fashionable eyecare for everyone. -

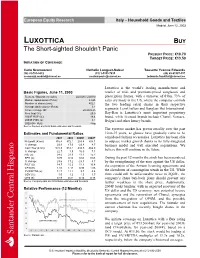

LUXOTTICA BUY the Short-Sighted Shouldn’T Panic PRESENT PRICE: €10.70 TARGET PRICE: €13.50 INITIATION of COVERAGE

European Equity Research Italy – Household Goods and Textiles Madrid, June 12, 2003 LUXOTTICA BUY The Short-sighted Shouldn’t Panic PRESENT PRICE: €10.70 TARGET PRICE: €13.50 INITIATION OF COVERAGE Carlo Scomazzoni Nathalie Longuet-Saleur Tousette Yvonne Edwards (34) 91-701-9432 (33) 1-5353-7435 (49) 69-91507-357 [email protected] [email protected] [email protected] Luxottica is the world’s leading manufacturer and Basic Figures, June 11, 2003 retailer of mid- and premium-priced sunglasses and Reuters / Bloomberg codes: LUX.MI / LUX IM prescription frames, with a turnover of €3bn. 73% of Market capitalisation (€ mn): 4,825 sales are made in the US, where the company controls Number of shares (mn): 452.1 the two leading retail chains in their respective Average daily volume (€ mn): 3.1 52-week range (€): 20.20-9.25 segments: LensCrafters and Sunglass Hut International. Free float (%): 25.0 Ray-Ban is Luxottica’s most important proprietary 2003E ROE (%): 18.4 brand, while licensed brands include Chanel, Versace, 2003E P/BV (x): 3.1 Bvlgari and other luxury brands. 2002-04F PEG: Neg Source: Reuters and SCH Bolsa estimates and forecasts. The eyewear market has grown steadily over the past Estimates and Fundamental Ratios 10-to-15 years, as glasses have gradually come to be 2001 2002 2003E 2004F considered fashion accessories. Luxottica has been able Net profit (€ mn): 316.4 372.1 283.4 308.1 to outpace market growth thanks to its fully-integrated % change: 23.9 17.6 -23.8 8.7 business model and well executed acquisitions. -

Consent Solicitation: Approval of the Transfer of the Notes from Luxottica to Essilorluxottica

NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION IN OR INTO THE UNITED STATES, OR TO ANY PERSON LOCATED OR RESIDENT IN, ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO RELEASE, PUBLISH OR DISTRIBUTE THIS DOCUMENT Consent solicitation: approval of the transfer of the Notes from Luxottica to EssilorLuxottica Charenton-le-Pont, France (November 26, 2019 – 6:00 pm) – Further to the press release dated 24 October 2019, Luxottica Group S.p.A. (“Luxottica”) and EssilorLuxottica S.A. (“EssilorLuxottica”) announce that in relation to the Euro 500,000,000 2.625 per cent. fixed rate notes due 10 February 2024 (ISIN: XS1030851791) issued by Luxottica in 2014 (the "Notes"), the meeting of the holders of the Notes today approved the transfer of the Notes from Luxottica to EssilorLuxottica, the release of the guarantors under the Notes, and certain modifications to the conditions of the Notes, all as further described in the Consent Solicitation Memorandum dated 24 October 2019, a copy of which is available under the “Consent solicitation” section on Luxottica’s website at http://www.luxottica.com/en/investors/consent-solicitation. Luxottica and EssilorLuxottica draw the attention of the holders of the Notes that as described in the Consent Solicitation Memorandum, the transfer will be effective as from the Implementation Date. ### EssilorLuxottica EssilorLuxottica is a global leader in the design, manufacture and distribution of ophthalmic lenses, frames and sunglasses. Formed in 2018, its mission is to help people around the world to see more, be more and live life to its fullest by addressing their evolving vision needs and personal style aspirations. -

Form 20-F. in 2016

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F (Mark One) អ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ፤ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2016 OR អ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR អ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission file number 1-10421 LUXOTTICA GROUP S.p.A. (Exact name of Registrant as specified in its charter) (Translation of Registrant’s name into English) REPUBLIC OF ITALY (Jurisdiction of incorporation or organization) PIAZZALE L. CADORNA 3, MILAN 20123, ITALY (Address of principal executive offices) Michael A. Boxer, Esq. Executive Vice President and Group General Counsel Piazzale L. Cadorna 3, Milan 20123, Italy Tel: +39 02 8633 4052 [email protected] (Name, Telephone, Email and/or Facsimile Number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act. Title of each class Name of each exchange of which registered ORDINARY SHARES, PAR VALUE NEW YORK STOCK EXCHANGE EURO 0.06 PER SHARE* AMERICAN DEPOSITARY NEW YORK STOCK EXCHANGE SHARES, EACH REPRESENTING ONE ORDINARY SHARE * Not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the New York Stock Exchange Securities registered or to be registered pursuant to Section 12(g) of the Act. -

Luxottica Admitted to the Cooperative Compliance Scheme with the Italian Revenue Agency

Luxottica admitted to the Cooperative Compliance scheme with the Italian Revenue Agency Milan, 29 December 2020 – Luxottica was admitted by the Italian Revenue Agency to the Cooperative Compliance scheme under legislative decree no. 128/2015. The aim of the Cooperative Compliance scheme, in accordance with current legislation to prevent tax risk and permit a further increase in the level of certainty regarding important fiscal matters, is to strengthen the relationship of trust and transparency between Luxottica and the Italian Revenue Agency. The admission to the scheme was preceded by an assessment performed by the Revenue Agency examining the full adequacy of Tax Governance and the Tax Control Framework adopted by Luxottica for the detection, measurement, management, and control of potential tax risk. Adherence to this regime is part of a wider Luxottica strategy aimed at the preventative management of risk based on transparency with financial administrations at a global level for the benefit of all stakeholders. Contacts: Oriana Pagano Group Corporate Media Relations Manager Email: [email protected] Luxottica Group S.p.A. About Luxottica Group Luxottica is a leader in the design, manufacture and distribution of fashion, luxury and sports eyewear. Its portfolio includes proprietary brands such as Ray-Ban, Oakley, Costa, Vogue Eyewear, Persol, Oliver Peoples and Alain Mikli, as well as licensed brands including Giorgio Armani, Burberry, Bulgari, Chanel, Coach, Dolce&Gabbana, Ferrari, Michael Kors, Prada, Ralph Lauren, Tiffany & Co., Valentino and Versace. The Group’s global wholesale distribution network covers more than 150 countries and is complemented by an extensive retail network of approximately 9,000 stores, with LensCrafters and Pearle Vision in North America, OPSM, LensCrafters and Spectacle Hut in Asia -Pacific, GMO and Óticas Carol in Latin America, Salmoiraghi & Viganò in Italy and Sunglass Hut worldwide. -

Monthly Amendments Individual Additions

Monthly Amendments Individual Additions GOC Title Forenames Surname Company Name Address 1 Address 2 Town County Postcode Country Join Date Number 01-31384 Ms Benazir Premji Spring Valley 16/01/2019 01-31385 Mr Mohammed Ahmed Leeds 17/01/2019 Ishaque 01-31387 Miss Beatriz Gallego-Collado Specsavers 50 Stepney Llanelli Carmarthenshire SA15 3TR UNITED 28/01/2019 Opticians Street KINGDOM Swansea 01-31388 Miss Syieqa Malik Dhahran 29/01/2019 D-17190 Mr Kishan Chudasama Specsavers Unit 31 Leicester Leicestershire LE4 1DF United Kingdom 04/01/2019 Opticians Beaumont Leys shopping Centre Leicester D-17191 Mr George Browne Wilkinson 90 High Street Tonbridge Kent TN9 1AP UNITED 04/01/2019 Eyewear Studio KINGDOM Gillingham D-17193 Mr David Belcher David H Myers 72-74 Albion Leeds West Yorkshire LS1 6AD 08/01/2019 Opticians Street D-17194 Miss Jodian Malcolm Boots Opticians 36 Poultry London London EC2R 8AJ UNITED 09/01/2019 KINGDOM London D-17197 Miss Kavita Patel Kenton 11/01/2019 D-17201 Miss Deborah Mahoney Specsavers 25 South Main Wexford IRELAND 23/01/2019 Opticians street Wexford D-17203 Mr Cedric Martial Oakley Store 1-4 King Street London WC2E 8HH United Kingdom 28/01/2019 Welling D-17204 Mrs Georgia Papakonstantinou Focus Optical 82A Papandreou Thessaloniki Thessalonki 56728 GREECE 29/01/2019 Street Thessaloniki D-17205 Mrs Lito Chatziphilippidou FOCUS L.Stratou 41 Thessaloniki 54639 Greece 29/01/2019 OPTICAL Panorama Individual Restorations GOC Title Forenames Surname Company Name Address 1 Address 2 Address 3 Town County Postcode Country -

PEARLE VISION UNVEILS NEW STORE DESIGN and CELEBRATES GRAND OPENING in CLEVELAND - Leading Optical Franchise Celebrates with Ribbon-Cutting Ceremony on Sept

\ MEDIA CONTACTS: Amanda DelPrete 954-893-9150 [email protected] Emily Ryan 513-765-3358 [email protected] PEARLE VISION UNVEILS NEW STORE DESIGN AND CELEBRATES GRAND OPENING IN CLEVELAND - Leading Optical Franchise Celebrates with Ribbon-Cutting Ceremony on Sept. 17- MASON, Ohio (September 11, 2013) – Pearle Vision, one of North America’s largest and most trusted licensed optical brands, announced today plans to unveil its new store design on Sept. 17 in Cleveland, Ohio. A ribbon-cutting ceremony will be held at 11:30 a.m. at the center in Legacy Village, located at 24539 Cedar Road, Lyndhurst, Ohio. The new Cleveland neighborhood eye care center features Pearle Vision’s completely remodeled design, which includes everything from a new, iconic brand logo and signage to modernized displays and a completely transformed floor plan. “For more than 50 years, Pearle Vision has been committed to providing genuine eye care to our patients; and now, in 2013, we are proud to unveil the first of our newly designed neighborhood eye care centers,” said Srinivas Kumar, senior vice president and general manager, Pearle Vision. “We are excited to share the new design elements with our entire network, and believe that everyone will love the new look and feel of our center, which incorporates our rich history, provides a welcoming atmosphere, and features eclectic displays and modern retail space.” Earlier this year, Pearle Vision unveiled at its annual licensee conference the new brand image with an updated logo and re-designed color palette for its centers. The new eyeglass icon speaks to the genuine heritage of Dr. -

CORPORATE EYECARE Protect Your Employees’ Eyesight the Easy Way – with the SPECSAVERS ANSWER Specsavers Corporate Eyecare

Welcome CORPORATE EYECARE Protect your employees’ eyesight the easy way – with THE SPECSAVERS ANSWER Specsavers Corporate Eyecare. Our voucher offers are simple FOR ALL YOUR BUSINESS to understand, virtually administration-free, and excellent EYECARE REQUIREMENTS value for money. From VDU glasses for clerical staff, prescription safety eyewear for workshop staff and eye examinations for drivers of company cars and other commercial vehicles, there’s a voucher offer to meet your needs. Furthermore, corporate client employees can also take advantage of the Premium Club. This is an exclusive corporate discount enabling them, and their family members, to enjoy further savings on Specsavers’ already affordable prices. You will also have the peace of mind that you are caring for your organisations most important assets, your employees. Protect your business the simple way – with Specsavers Corporate Eyecare. Your requirements as a company How we can help you As an employer, you will recognise that any At Specsavers, we understand your needs business’s greatest asset is its workforce. as an employer, and have designed four Safe, healthy and happy employees help any corporate eyecare offers: business thrive. • VDU Eyecare vouchers You are legally obliged under Health and • Safety Eyewear vouchers Safety regulations to provide eyecare to • Optical Care vouchers certain parts of your workforce. Basic • Premium Club vouchers advice can avoid some potential eyesight The vouchers cover all aspects of eyecare difficulties – for example, correct lighting, for employees at all levels, and are designed screen breaks, or machine safety guards. with you, the employer, in mind. Whether your employees are in front Cost-effective: Our vouchers offer unrivalled of a computer monitor, in an industrial value for money. -

FORM 20-F (Mark One)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F (Mark One) ፬ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ፤ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2013 OR ፬ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ፬ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission file number 1-10421 LUXOTTICA GROUP S.p.A. (Exact name of Registrant as specified in its charter) (Translation of Registrant's name into English) REPUBLIC OF ITALY (Jurisdiction of incorporation or organization) VIA C. CANTÙ 2, MILAN 20123, ITALY (Address of principal executive offices) Michael A. Boxer, Esq. Executive Vice President and Group General Counsel 12 Harbor Park Drive Port Washington, NY 11050 Tel: (516) 484-3800 Fax: (516) 706-4012 (Name, Telephone, Email and/or Facsimile Number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act. Title of each class Name of each exchange of which registered ORDINARY SHARES, PAR VALUE NEW YORK STOCK EXCHANGE EURO 0.06 PER SHARE* AMERICAN DEPOSITARY NEW YORK STOCK EXCHANGE SHARES, EACH REPRESENTING ONE ORDINARY SHARE * Not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the New York Stock Exchange Table of Contents Securities registered or to be registered pursuant to Section 12(g) of the Act. -

Mintel Reports Brochure

Optical Goods Retailing - UK - February 2020 The above prices are correct at the time of publication, but are subject to Report Price: £1995.00 | $2693.85 | €2245.17 change due to currency fluctuations. “This is a highly concentrated sector, dominated by three major retail brands. Specsavers has been mopping up independent retailers and has now reached 900 UK outlets, raising the question of how much more growth is realistic for this highly successful business.” – Jane Westgarth, Senior Retail Analyst This report looks at the following areas: BUY THIS Vision Express took a leap forward with the acquisition of Tesco Opticians in 2017, bringing its store REPORT NOW numbers up to almost 600, and Boots Opticians continues to benefit from the heritage strength of its parent company brand. More than 100 independents have taken shelter by joining the Hakim Group and only a handful of smaller chains demonstrate an appetite for growth. Meanwhile the long-awaited VISIT: growth of online selling is becoming a reality. Shopping online for contact lenses can offer considerable store.mintel.com savings, but none of the healthcare that an optician delivers, while online selling of glasses is beginning to benefit from digital developments that allow customers to visualise how they will look in their glasses. CALL: EMEA • Online selling is building momentum +44 (0) 20 7606 4533 • New wave of opticians with personality and a DTC model • What is the relevance of supermarkets in optics? Brazil 0800 095 9094 Americas +1 (312) 943 5250 China +86 (21) 6032 7300 APAC +61 (0) 2 8284 8100 EMAIL: [email protected] This report is part of a series of reports, produced to provide you with a DID YOU KNOW? more holistic view of this market reports.mintel.com © 2020 Mintel Group Ltd.