FORM 20-F (Mark One)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Essilorluxottica 28 May 2019 Update to Credit Analysis Following Affirmation of A2

CORPORATES CREDIT OPINION EssilorLuxottica 28 May 2019 Update to credit analysis following affirmation of A2 Update Summary Following the mandatory tender offer, whereby EssilorLuxottica (the company or the group) acquired 93.3% of Luxottica's shares, the company subsequently launched a sellout and squeeze-out of the remaining shares for a combination of stock issuances and a cash consideration of about €640 million. As of March 5, 2019, EssilorLuxottica controlled all the RATINGS share capital of Luxottica, whose shares have been delisted from the Italian stock exchange. EssilorLuxottica Domicile France EssilorLuxottica's A2 rating continues to reflect (1) its position as the global leader in Long Term Rating A2 corrective lenses and eyewear market by a large margin to its competitors, illustrating the Type LT Issuer Rating - Fgn group's strong innovation capabilities and brand portfolio; (2) the group's wide offering Curr within its product category and its vertical integration, which allow it to cater to a variety Outlook Stable of customers and develop strong relationships with opticians; (3) a very solid track record Please see the ratings section at the end of this report of steady growth and resilient operating performance; and (4) the group's strong financial for more information. The ratings and outlook shown profile, underpinned by a healthy free cash flow (FCF) generation. reflect information as of the publication date. EssilorLuxottica's rating also factors in (1) the group's concentration of sales generated by its corrective lenses and frames business, as well as its relative concentration in the US market; Contacts (2) the still subdued economic environment in some of the group's key markets, which can Knut Slatten +33.1.5330.1077 weigh on lenses' renewal rates or result in some trading down by consumers; (3) the risk of a VP-Senior Analyst competitor making a breakthrough innovation; and (4) a degree of uncertainty around future [email protected] financial policies and the group's appetite for future external growth. -

Postgraduate Courses Undergraduate and Five Schools: Mathematical, Physical and Graduate Levels

unige.it STUDENT FACULTY ENROLLMENT More than 1,300 More than 30,000 faculty members students at both distribuited over Postgraduate courses undergraduate and five schools: Mathematical, Physical and graduate levels. Natural Sciences 2018/2019 Medical and Pharmaceutical Sciences Polytechnic Social Sciences Humanities Università di Genova The University of Genoa (UNIGE) is vides a truly multi-disciplinary international companies (e.g. IIT). Via Balbi 5 - 16126 Genova one of the most ancient of the Euro- teaching offer. • UNESCO Chair “Anthropology of pean large universities; with about 280 • The “Scuola superiore dell’Università Health. Biosphere and Healing Sys- +39 010 20991 educational paths distributed in the degli Studi di Genova (IANUA)” tems” established in 2014 headquarters in Genoa and the learn- encourages advanced educational LIBRARIES unige.it ing centres of Imperia, Savona and La paths of didactic and scientific ex- The University Library and the City Spezia, it comes up to the community cellences for worthy students se- Library System of Genoa have merged as a well-established reality through- lected by public contest. their services to create a single Inte- out the region. grated Library System. The broad ar- Located at the heart of a superb city, RESEARCH ray of services offered by the Univer- offering splendors of its medieval and sity Library includes both traditional @unigenova baroque heritage and site of the largest • Worldwide experts in all domains involving the sea: its habitat, its text consultation and innovative, high and most productive harbour in Eu- tech services. rope, the University of Genoa is one of economy, its exploitation. the most renowned multidisciplinary public universities in Italy, with peaks • Tight connections with one of the CAMPUS of excellence in several scientific and biggest oncological research hospi- • The oldest Campus, site of the Social technological domains. -

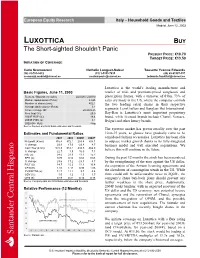

LUXOTTICA BUY the Short-Sighted Shouldn’T Panic PRESENT PRICE: €10.70 TARGET PRICE: €13.50 INITIATION of COVERAGE

European Equity Research Italy – Household Goods and Textiles Madrid, June 12, 2003 LUXOTTICA BUY The Short-sighted Shouldn’t Panic PRESENT PRICE: €10.70 TARGET PRICE: €13.50 INITIATION OF COVERAGE Carlo Scomazzoni Nathalie Longuet-Saleur Tousette Yvonne Edwards (34) 91-701-9432 (33) 1-5353-7435 (49) 69-91507-357 [email protected] [email protected] [email protected] Luxottica is the world’s leading manufacturer and Basic Figures, June 11, 2003 retailer of mid- and premium-priced sunglasses and Reuters / Bloomberg codes: LUX.MI / LUX IM prescription frames, with a turnover of €3bn. 73% of Market capitalisation (€ mn): 4,825 sales are made in the US, where the company controls Number of shares (mn): 452.1 the two leading retail chains in their respective Average daily volume (€ mn): 3.1 52-week range (€): 20.20-9.25 segments: LensCrafters and Sunglass Hut International. Free float (%): 25.0 Ray-Ban is Luxottica’s most important proprietary 2003E ROE (%): 18.4 brand, while licensed brands include Chanel, Versace, 2003E P/BV (x): 3.1 Bvlgari and other luxury brands. 2002-04F PEG: Neg Source: Reuters and SCH Bolsa estimates and forecasts. The eyewear market has grown steadily over the past Estimates and Fundamental Ratios 10-to-15 years, as glasses have gradually come to be 2001 2002 2003E 2004F considered fashion accessories. Luxottica has been able Net profit (€ mn): 316.4 372.1 283.4 308.1 to outpace market growth thanks to its fully-integrated % change: 23.9 17.6 -23.8 8.7 business model and well executed acquisitions. -

PERSONAL INFORMATION Daniele Ferrari, Piazza Di Pellicceria, N. 3/11

PERSONAL INFORMATION Daniele Ferrari, Piazza di Pellicceria, n. 3/11, 16121 Genova, [email protected] Sex Male - Date of birth 28/10/1984 – Nationality: Italian EDUCATION AND TRAINING 19 December 2014, PhD in Costitutional Law, University of Genoa, Faculty of Law, Supervisor: Professor Pasquale Costanzo, Subject: Costitutional Law – Ecclesiastical Law, Title: “La libertà di coscienza multilivello” 22 October 2008, Master Degree in Law, Vote: 110/110 with honors, University of Pisa, Faculty of Law, Supervisor: Professor R. Tarchi, Subject: Comparative Legal Systems - Ecclesiastical Law, Title: “Il principio di laicità e la libertà di manifestazione religiosa: itinerari di giurisprudenza nel contesto europeo” CURRENT POSITIONS Since 2017- Researcher in ecclesiastical and canon law, Department of Law, University of Siena, Italy Since 2017- Teaching assistant, Introduction to gender studies, Department of Law, University of Genoa, Italy Since 2016- Trainer, Ministry of Interior, Prefecture of Genoa Since 2016- Trainer, ARCI Association, Project “P.In. Pienamente Inclusivi” – Prog. 320 Fondo Asilo, Migrazione e Integrazione (FAMI) 2014-2020, Italy Since 2016- Post-doc researcher, Groupe Sociétés, Religions, Laïcités (GSRL), CNRS-EPHE, Paris Since 2016-Trainer Program “Immigrazione: ingresso e condizione degli stranieri in Italia”, Prefecture of Genoa, Italy Since 2016, Lawyer, Refugee Service, Association P.A. Croce Bianca Genovese, Genova, Italy Since 2015- Teaching Assistant, Public Law, Department of Political Science, University of Genoa, Italy Since 2012- Trainer, Order of Genoa lawyers, Italy Since 2011- Lawyer, Order of Genoa lawyers, Italy PREVIOUS POSITIONS 01.01.2010-19.12.2015- PhD Student, “Studi costituzionalistici italiani, europei e transnazionali”, XXV ciclo, University of Genoa, Department of Jurisprudence. -

Consent Solicitation: Approval of the Transfer of the Notes from Luxottica to Essilorluxottica

NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION IN OR INTO THE UNITED STATES, OR TO ANY PERSON LOCATED OR RESIDENT IN, ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO RELEASE, PUBLISH OR DISTRIBUTE THIS DOCUMENT Consent solicitation: approval of the transfer of the Notes from Luxottica to EssilorLuxottica Charenton-le-Pont, France (November 26, 2019 – 6:00 pm) – Further to the press release dated 24 October 2019, Luxottica Group S.p.A. (“Luxottica”) and EssilorLuxottica S.A. (“EssilorLuxottica”) announce that in relation to the Euro 500,000,000 2.625 per cent. fixed rate notes due 10 February 2024 (ISIN: XS1030851791) issued by Luxottica in 2014 (the "Notes"), the meeting of the holders of the Notes today approved the transfer of the Notes from Luxottica to EssilorLuxottica, the release of the guarantors under the Notes, and certain modifications to the conditions of the Notes, all as further described in the Consent Solicitation Memorandum dated 24 October 2019, a copy of which is available under the “Consent solicitation” section on Luxottica’s website at http://www.luxottica.com/en/investors/consent-solicitation. Luxottica and EssilorLuxottica draw the attention of the holders of the Notes that as described in the Consent Solicitation Memorandum, the transfer will be effective as from the Implementation Date. ### EssilorLuxottica EssilorLuxottica is a global leader in the design, manufacture and distribution of ophthalmic lenses, frames and sunglasses. Formed in 2018, its mission is to help people around the world to see more, be more and live life to its fullest by addressing their evolving vision needs and personal style aspirations. -

Mark Dincecco 1

MARK DINCECCO University of Michigan Department of Political Science Ann Arbor, MI 48109 [email protected] Current Positions Associate Professor of Political Science, University of Michigan, 2019- Affiliate, Program in International and Comparative Studies (PICS), University of Michigan, 2013- Past Positions Assistant Professor of Political Science, University of Michigan, 2013-19 Assistant Professor, IMT Institute for Advanced Studies, Lucca, 2006-13 Visiting Positions Visiting Scholar, Social and Political Sciences, Bocconi University, 2021 (March) Visiting Scholar, Economics, University of Bologna, 2021 (April) Edward Teller National Fellow, Hoover Institution, Stanford University, 2016-17 Visiting Scholar, Economic History Laboratory, UC Berkeley, 2012 (October) Visiting Scholar, STICERD, London School of Economics, 2011 (November) Visiting Scholar, IGIER, Bocconi University, 2011 (October) Visiting Scholar, Leitner Program in Political Economy, Yale University, 2011 (September) Education PhD, Economics, UCLA, 2006 (Advisor: Jean-Laurent Rosenthal) MA, Economics, UCLA, 2003 BA, summa cum laude, University of Arizona, 1999 (Cumulative GPA: 4.000) Fields Historical Political Economy, Political Economy of Development, International Political Economy Books 1. From Warfare to Wealth: The Military Origins of Urban Prosperity in Europe, Cambridge University Press, Political Economy of Institutions and Decisions Series, 2017 (With Massimiliano Onorato) Winner, William H. Riker Best Book Award, 2018 2. State Capacity and Economic Development: Present and Past, Cambridge University Press, Elements in Political Economy Series, 2017 Inaugural book in this series 3. Political Transformations and Public Finances: Europe, 1650-1913, Cambridge University Press, Polit- ical Economy of Institutions and Decisions Series, 2011 (Paperback Edition, 2013; China Edition, Forthcoming) 1 Journal Publications 1. The Budgetary Origins of Fiscal-Military Prowess, Journal of Politics, Forthcoming (With Gary Cox) 2. -

Form 20-F. in 2016

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F (Mark One) អ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ፤ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2016 OR អ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR អ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission file number 1-10421 LUXOTTICA GROUP S.p.A. (Exact name of Registrant as specified in its charter) (Translation of Registrant’s name into English) REPUBLIC OF ITALY (Jurisdiction of incorporation or organization) PIAZZALE L. CADORNA 3, MILAN 20123, ITALY (Address of principal executive offices) Michael A. Boxer, Esq. Executive Vice President and Group General Counsel Piazzale L. Cadorna 3, Milan 20123, Italy Tel: +39 02 8633 4052 [email protected] (Name, Telephone, Email and/or Facsimile Number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act. Title of each class Name of each exchange of which registered ORDINARY SHARES, PAR VALUE NEW YORK STOCK EXCHANGE EURO 0.06 PER SHARE* AMERICAN DEPOSITARY NEW YORK STOCK EXCHANGE SHARES, EACH REPRESENTING ONE ORDINARY SHARE * Not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the New York Stock Exchange Securities registered or to be registered pursuant to Section 12(g) of the Act. -

Luxottica Admitted to the Cooperative Compliance Scheme with the Italian Revenue Agency

Luxottica admitted to the Cooperative Compliance scheme with the Italian Revenue Agency Milan, 29 December 2020 – Luxottica was admitted by the Italian Revenue Agency to the Cooperative Compliance scheme under legislative decree no. 128/2015. The aim of the Cooperative Compliance scheme, in accordance with current legislation to prevent tax risk and permit a further increase in the level of certainty regarding important fiscal matters, is to strengthen the relationship of trust and transparency between Luxottica and the Italian Revenue Agency. The admission to the scheme was preceded by an assessment performed by the Revenue Agency examining the full adequacy of Tax Governance and the Tax Control Framework adopted by Luxottica for the detection, measurement, management, and control of potential tax risk. Adherence to this regime is part of a wider Luxottica strategy aimed at the preventative management of risk based on transparency with financial administrations at a global level for the benefit of all stakeholders. Contacts: Oriana Pagano Group Corporate Media Relations Manager Email: [email protected] Luxottica Group S.p.A. About Luxottica Group Luxottica is a leader in the design, manufacture and distribution of fashion, luxury and sports eyewear. Its portfolio includes proprietary brands such as Ray-Ban, Oakley, Costa, Vogue Eyewear, Persol, Oliver Peoples and Alain Mikli, as well as licensed brands including Giorgio Armani, Burberry, Bulgari, Chanel, Coach, Dolce&Gabbana, Ferrari, Michael Kors, Prada, Ralph Lauren, Tiffany & Co., Valentino and Versace. The Group’s global wholesale distribution network covers more than 150 countries and is complemented by an extensive retail network of approximately 9,000 stores, with LensCrafters and Pearle Vision in North America, OPSM, LensCrafters and Spectacle Hut in Asia -Pacific, GMO and Óticas Carol in Latin America, Salmoiraghi & Viganò in Italy and Sunglass Hut worldwide. -

PEARLE VISION UNVEILS NEW STORE DESIGN and CELEBRATES GRAND OPENING in CLEVELAND - Leading Optical Franchise Celebrates with Ribbon-Cutting Ceremony on Sept

\ MEDIA CONTACTS: Amanda DelPrete 954-893-9150 [email protected] Emily Ryan 513-765-3358 [email protected] PEARLE VISION UNVEILS NEW STORE DESIGN AND CELEBRATES GRAND OPENING IN CLEVELAND - Leading Optical Franchise Celebrates with Ribbon-Cutting Ceremony on Sept. 17- MASON, Ohio (September 11, 2013) – Pearle Vision, one of North America’s largest and most trusted licensed optical brands, announced today plans to unveil its new store design on Sept. 17 in Cleveland, Ohio. A ribbon-cutting ceremony will be held at 11:30 a.m. at the center in Legacy Village, located at 24539 Cedar Road, Lyndhurst, Ohio. The new Cleveland neighborhood eye care center features Pearle Vision’s completely remodeled design, which includes everything from a new, iconic brand logo and signage to modernized displays and a completely transformed floor plan. “For more than 50 years, Pearle Vision has been committed to providing genuine eye care to our patients; and now, in 2013, we are proud to unveil the first of our newly designed neighborhood eye care centers,” said Srinivas Kumar, senior vice president and general manager, Pearle Vision. “We are excited to share the new design elements with our entire network, and believe that everyone will love the new look and feel of our center, which incorporates our rich history, provides a welcoming atmosphere, and features eclectic displays and modern retail space.” Earlier this year, Pearle Vision unveiled at its annual licensee conference the new brand image with an updated logo and re-designed color palette for its centers. The new eyeglass icon speaks to the genuine heritage of Dr. -

Genoa Center - Report 2005

McLeod Institute of Simulation Science Genoa Center - Report 2005 MISS Genoa Center Savona Campus & Savona Labs via Cadorna 2 17100 Savona, Italy Tel +39 019 264 555 Fax +39 019 264 558 URL www.simulationscience.org EMAIL [email protected] MISS - Genoa DIP University of Genoa Email: [email protected] URL: http://st.itim.unige.it The research group of MISS-DIP of Genoa University is active from ‘60 in Simulation applied to Industrial Engineering. The activities involve modeling, simulation, VV&A and analysis of Industrial Applications and Services (design, re-engineering, management, training etc.) as: Chemical Facilities Power Plants PM Harbor Terminals Public Services Environment Manufacturing Assembling Logistics Public Transportation The Department staff is in touch world-wide with the simulation community and is present actively to conferences, exhibitions and working meetings with the major Associations, Agencies and Companies. 20 MISS Centers World -Wide MISS - DIP University of Genoa & 5 Satellite Centers Liophant Simulation Club DIP - University of Genoa DIP was founded in 1997 as evolution of the Institute of Technology and Industrial Management (ITIM) that was operative from ‘60. DIP is composed by about 40 faculty members, 15 technicians and administrative, plus several PhD Students, external Researchers and Consultants. DIP teachers are involved in Undergraduate, Postgraduate and Professional activities in Engineering, Management. DIP active in R&D Projects for major Institutions, Companies and Governmental Organisations. DIP co-operates actively with major Excellence Centers World-Wide. Currently DIP is changing name to DIPTEM. University of Genoa: an Overview The University of Genoa is one of the oldest in Italy and in the World (founded in 1471 AD), it is located in middle of Italian Riviera. -

International Conference Narrating EU Integration: Speeches And

DISPO (Unige) Albergo dei Poveri, Piazzale E. Brignole, 2/A Genoa Genoa, 3-5 February 2021 Join the Web conference on Microsoft Teams, code: g1fbtnf International Conference Narrating EU Integration: Speeches and Speakers from 1946 to 2018 Programme 11.30 -13.00 Chair: Michael Gehler, 3 February: 9.30-13.00 University of Hildesheim Presentation of a series of “Speeches on Europe” • Francesco Pierini, Friends and Sponsors of the New Europe: selected by the students of the high schools A Discourse Analysis on Churchill’s speech at the University involved in the Jean Monnet Projet of Zurich 19 September 1946, University of Genoa • Giuliana Laschi, “La Communauté européenne est l’une des Liceo Classico Andrea D’Oria-Genoa plus grandes conceptions politiques de l’Occident”. Liceo Linguistico Grazia Deledda-Genoa Walter Hallstein et l’Europe, University of Bologna Liceo Linguistico Della Rovere- Savona • Jean-Marie Palayret, The Schuman Declaration of 9th May 1950: Memory and Topicality of a founding speech, 4 February Historical Archives of the EU, Florence 9.00 - Welcome address by the Head of the School Discussion of Social Sciences - Prof. Luca Beltrametti 9.15 - Welcome address by the Director of Speeches on Europe from the “Long 1970s” to the the Department - Prof.ssa Daniela Preda Recovery of the European Community Video with the results of the research project with 14.30 -16.00 Chair: Massimiliano Guderzo, the High Schools University of Siena Michael Gehler, Hans-Dietrich Genscher “European Commu- Speeches on the birth of the European -

LA LANTERNA LIGHTHOUSE of GENOA, LIGURIA, ITALY by Annamaria “Lilla” Mariotti

Reprinted from the U. S. Lighthouse Society’s The Keeper’s Log ‑ Spring 2011 <www.uslhs.org> LA LANTERNA LIGHTHOUSE OF GENOA, LIGURIA, ITALY By Annamaria “Lilla” Mariotti enoa is an important city—whose Bonfires were already lighted on the hills nickname is “La Superba” (“The surrounding Genoa to guide the ships, but that Proud”)—located on the hills was not enough. A light became necessary in overlooking the Ligurian Sea. the harbor to safely guide the incoming ships. With a population of more than 700,000 in- The origins of the lighthouse of Genoa habitants, it has a busy harbor full of contain- are uncertain and half legendary, but some er ships, ferries, and cruise ships. On its east sources say the first tower was built around side is the eastern Riviera and on its west side 1129 on a rock called Capo di Faro (Light- the western Riviera, both very modern and house Cape) on the west side of the town, loved by the tourists for their mild climate at the base of the San Benigno hill, a name and their beaches. But this is today’s history. derived from a monastery then exiting on In the Middle Ages, navigation had im- the top. By a decree called delle prestazioni proved both during the day and night, and (about services), responsibility for the light Genoa was already an important commercial was entrusted to the surrounding inhabit- center. Since 950 A.D., the city was an inde- ants Habent facere guardiam ad turrem capiti pendent municipality, and with Amalfi, Ven- fari which, in Latin, simply means “to keep ice, and Pisa, one of the four strongest mari- the light on.” time republics, all fighting among themselves Nobody knows the shape of this first for domination of the Mediterranean Sea.